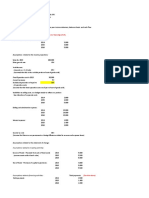

Crazy Loops - Accounting Cycle

Crazy Loops - Accounting Cycle

You might also like

- ACCN 304 Revision QuestionsDocument11 pagesACCN 304 Revision Questionskelvinmunashenyamutumba100% (1)

- Quizzer - Financial Accounting ProcessDocument8 pagesQuizzer - Financial Accounting ProcessLuisitoNo ratings yet

- Tax1 Q Chapter-11 12 13 With-AnswerDocument2 pagesTax1 Q Chapter-11 12 13 With-AnswerPrincess Edelyn CastorNo ratings yet

- Act1111 Final ExamDocument7 pagesAct1111 Final ExamHaidee Flavier SabidoNo ratings yet

- Absolute and Conditional SalesDocument8 pagesAbsolute and Conditional SalesDumstey0% (1)

- Competitive Strategy of Amazon WebsiteDocument3 pagesCompetitive Strategy of Amazon WebsiteAkshat MehtaNo ratings yet

- Samsung Tab InvoiceDocument1 pageSamsung Tab InvoiceShantanu BhardwajNo ratings yet

- Star Wars7 - Accounting CycleDocument8 pagesStar Wars7 - Accounting CyclemillionextupNo ratings yet

- January February March Beginning Cash BalanceDocument6 pagesJanuary February March Beginning Cash BalanceALBERTO MARIO CHAMORRO PACHECONo ratings yet

- Handsout 06 Chap 03 Part 02Document4 pagesHandsout 06 Chap 03 Part 02Shane VeiraNo ratings yet

- BT Ias1 (SV)Document3 pagesBT Ias1 (SV)HÀ THỚI NGUYỄN NGÂNNo ratings yet

- 助教課講義 Ch.4Document12 pages助教課講義 Ch.45213adamNo ratings yet

- Group Assignment On Fundamentals of Accounting IDocument6 pagesGroup Assignment On Fundamentals of Accounting IKaleab ShimelsNo ratings yet

- Soal Mojakoe-UTS Akuntansi Keuangan 1 Ganjil 2020-2021Document9 pagesSoal Mojakoe-UTS Akuntansi Keuangan 1 Ganjil 2020-2021Vincenttio le CloudNo ratings yet

- Exam 2021 (Resolution)Document9 pagesExam 2021 (Resolution)Chi Kei KeungNo ratings yet

- Chapter 4 Review Principles of Accounting AnswersDocument3 pagesChapter 4 Review Principles of Accounting AnswersChien Phuong ThanhNo ratings yet

- Tugas Accounting 1 With NotesDocument14 pagesTugas Accounting 1 With Notesvico lorenzoNo ratings yet

- Seminar 4 - QsDocument3 pagesSeminar 4 - QsMaman AbdurrahmanNo ratings yet

- Practice Exam FinalsDocument2 pagesPractice Exam FinalsPauline Jasmine Sta AnaNo ratings yet

- Classroom Exerisises On Presentation of Financial Statements PDFDocument2 pagesClassroom Exerisises On Presentation of Financial Statements PDFalyssaNo ratings yet

- Far01 - The Financial Statements PresentationDocument10 pagesFar01 - The Financial Statements PresentationRNo ratings yet

- IFRS Week 6Document4 pagesIFRS Week 6AleksandraNo ratings yet

- 1 Partnership-YTDocument7 pages1 Partnership-YTSherwin DueNo ratings yet

- Mockbiard Questions - Practical 1Document10 pagesMockbiard Questions - Practical 1Regina Clarete0% (1)

- Adjusting EntriesDocument5 pagesAdjusting EntriesM Hassan BrohiNo ratings yet

- Exercises On Projected Financial StatementsDocument2 pagesExercises On Projected Financial StatementsSharmaine LiasosNo ratings yet

- Accounting TestDocument4 pagesAccounting Testdinda ardiyaniNo ratings yet

- Exercise 5 - Completing The Accounting Cycle For Merchandising and Service BusinessDocument4 pagesExercise 5 - Completing The Accounting Cycle For Merchandising and Service BusinessShiela Rengel0% (2)

- Chapter 5 Exercises-Exercise BankDocument9 pagesChapter 5 Exercises-Exercise BankPATRICIUS ALAN WIRAYUDHA KUSUMNo ratings yet

- Long Quiz P1Document2 pagesLong Quiz P1chonana0408No ratings yet

- Accounting 2Document18 pagesAccounting 2cherryannNo ratings yet

- Amended - Final - Unit 5 - AAB-Accounting Principles - A2Document6 pagesAmended - Final - Unit 5 - AAB-Accounting Principles - A2Quang MinhNo ratings yet

- Statement of Cash FlowsDocument6 pagesStatement of Cash FlowsLuiNo ratings yet

- Asdos Pert 2Document2 pagesAsdos Pert 2mutiaoooNo ratings yet

- Account AssignmentDocument4 pagesAccount AssignmentNavjeet SandhuNo ratings yet

- Acc5115 - Intermediate Financial Reporting Statement of Comprehensive Income and Changes in Owner'S Equity Problem ADocument6 pagesAcc5115 - Intermediate Financial Reporting Statement of Comprehensive Income and Changes in Owner'S Equity Problem ARachel LuberiaNo ratings yet

- 6727 Statement of Financial PositionDocument3 pages6727 Statement of Financial PositionJane ValenciaNo ratings yet

- 2019-06 ICMAB FL 001 PAC Year Question JUNE 2019Document3 pages2019-06 ICMAB FL 001 PAC Year Question JUNE 2019Mohammad ShahidNo ratings yet

- Intermediate Accounting 2 Topic: Unearned RevenuesDocument5 pagesIntermediate Accounting 2 Topic: Unearned RevenuesJhazreel BiasuraNo ratings yet

- Problem Cash FlowDocument3 pagesProblem Cash FlowKimberly AnneNo ratings yet

- Instructions: Amazon Seller Buys Printer Supplies For $29 With CashDocument1 pageInstructions: Amazon Seller Buys Printer Supplies For $29 With CashJorge FloresNo ratings yet

- P1 QuestionsDocument31 pagesP1 QuestionsWillen Christia M. MadulidNo ratings yet

- Auditing Problem Assignment Lyeca JoieDocument12 pagesAuditing Problem Assignment Lyeca JoieEsse ValdezNo ratings yet

- Acc 1 QuizDocument7 pagesAcc 1 QuizAyat MukahalNo ratings yet

- Revision Pack QuestionsDocument12 pagesRevision Pack QuestionsAmmaarah PatelNo ratings yet

- Soal Tugas Akm Is - ST o FP - CFDocument6 pagesSoal Tugas Akm Is - ST o FP - CFElyssa Fiqri Fauziah0% (1)

- Accounting Yr11 2022Document8 pagesAccounting Yr11 2022keishacamilleriNo ratings yet

- Solving - Business Finance 1-6Document28 pagesSolving - Business Finance 1-6Samson, Ma. Louise Ren A.No ratings yet

- Session 11,12&13 AssignmentDocument3 pagesSession 11,12&13 AssignmentMardi SutiosoNo ratings yet

- Cash and Accrual BasisDocument4 pagesCash and Accrual BasisBwwwiiiii100% (1)

- P1 - ReviewDocument14 pagesP1 - ReviewEvitaAyneMaliñanaTapit0% (2)

- Semi-Finals Financial Accounting and ReportingDocument23 pagesSemi-Finals Financial Accounting and Reportingjoyce KimNo ratings yet

- Exercises III - Accruals and Deferrals Adjusting EntriesDocument2 pagesExercises III - Accruals and Deferrals Adjusting EntriesJowjie TV50% (2)

- IAET TaxationDocument2 pagesIAET TaxationRandy Manzano100% (1)

- Mittens Kittens CompanyDocument5 pagesMittens Kittens CompanyDianna EsmerayNo ratings yet

- Fina 470 Project Two - Check PointDocument9 pagesFina 470 Project Two - Check PointMitchell ParrottNo ratings yet

- Statement of Comprehensive IncomeDocument4 pagesStatement of Comprehensive Incomebobo tangaNo ratings yet

- Review For Quiz 3 Part 2Document18 pagesReview For Quiz 3 Part 2Mariah ValizadoNo ratings yet

- Pilot TestDocument6 pagesPilot TestNguyễn Thị Ngọc AnhNo ratings yet

- Wahyudi Syaputra - Assignment Week 13Document11 pagesWahyudi Syaputra - Assignment Week 13Wahyudi SyaputraNo ratings yet

- MOD2 Statement of Cash FlowsDocument2 pagesMOD2 Statement of Cash FlowsGemma DenolanNo ratings yet

- Homework On Statement of Cash FlowsDocument2 pagesHomework On Statement of Cash FlowsAmy SpencerNo ratings yet

- J.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineFrom EverandJ.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineNo ratings yet

- PBL Marketing StrategyDocument4 pagesPBL Marketing StrategyLisna Gitq SilviaNo ratings yet

- Accounting For Merchandising Activities: Solutions Manual For Chapter 6 435Document163 pagesAccounting For Merchandising Activities: Solutions Manual For Chapter 6 435debora yosikaNo ratings yet

- Ch8 Income Statement Worksheet AnswersDocument2 pagesCh8 Income Statement Worksheet Answerssalma RamadanNo ratings yet

- 7.1 - Business Plan SampleDocument1 page7.1 - Business Plan SampleSneha HiraniNo ratings yet

- Supply Chains and The Value Delivery NetworkDocument4 pagesSupply Chains and The Value Delivery NetworkJennyNo ratings yet

- Sales Forcaast and Sales QuotasDocument21 pagesSales Forcaast and Sales QuotasKunal SainiNo ratings yet

- Think Pair Share: Case Snippet 1: 10 MarksDocument2 pagesThink Pair Share: Case Snippet 1: 10 MarksShri RavanNo ratings yet

- Executive Summary: 1.1 Introduction To BeiersdorfDocument19 pagesExecutive Summary: 1.1 Introduction To BeiersdorfLogesh WaranNo ratings yet

- Blood Bananas Case AnalysisDocument1 pageBlood Bananas Case AnalysisVanessa LantajoNo ratings yet

- TotalDocument3 pagesTotalshibbuNo ratings yet

- Ia - 13Document17 pagesIa - 13Ma. Fatima H. FabayNo ratings yet

- Pi 4400000700Document1 pagePi 4400000700KrishnaNo ratings yet

- Business Math Module 4 StudentsDocument26 pagesBusiness Math Module 4 StudentsMarck Lorenz BellenNo ratings yet

- YTDocument3 pagesYTARYAJAI SINGHNo ratings yet

- CPA Review On FARDocument5 pagesCPA Review On FARYlor NoniuqNo ratings yet

- OM Chapter-3Document206 pagesOM Chapter-3TIZITAW MASRESHANo ratings yet

- Far TheoriesDocument6 pagesFar TheoriesallijahNo ratings yet

- P2 - Bba Entrepreneurship Project Log Book Top Sheet 2019-2020Document10 pagesP2 - Bba Entrepreneurship Project Log Book Top Sheet 2019-2020elvee.hrNo ratings yet

- Contract Allocation - Stand Alone Selling PriceDocument19 pagesContract Allocation - Stand Alone Selling Pricenagalakshmi100% (1)

- Business PlanningDocument49 pagesBusiness PlanningMinka BoydNo ratings yet

- A Case Study On Dabur LTDDocument3 pagesA Case Study On Dabur LTDgarimaamityNo ratings yet

- Case 14-63Document2 pagesCase 14-63KamruzzamanNo ratings yet

- ProjectDocument62 pagesProjectprince_soni_9No ratings yet

- ComercialInvoice PCW154986096Document1 pageComercialInvoice PCW154986096Quan VũNo ratings yet

- MGN 806Document14 pagesMGN 806Winnie StellaNo ratings yet

- Unit III Manufacturing ConcernDocument12 pagesUnit III Manufacturing ConcernAlezandra SantelicesNo ratings yet

- Inventory Procedures: Step OneDocument12 pagesInventory Procedures: Step OneNoorul HuqNo ratings yet

Download as pdf or txt

You might also like

- ACCN 304 Revision QuestionsDocument11 pagesACCN 304 Revision Questionskelvinmunashenyamutumba100% (1)

- Quizzer - Financial Accounting ProcessDocument8 pagesQuizzer - Financial Accounting ProcessLuisitoNo ratings yet

- Tax1 Q Chapter-11 12 13 With-AnswerDocument2 pagesTax1 Q Chapter-11 12 13 With-AnswerPrincess Edelyn CastorNo ratings yet

- Act1111 Final ExamDocument7 pagesAct1111 Final ExamHaidee Flavier SabidoNo ratings yet

- Absolute and Conditional SalesDocument8 pagesAbsolute and Conditional SalesDumstey0% (1)

- Competitive Strategy of Amazon WebsiteDocument3 pagesCompetitive Strategy of Amazon WebsiteAkshat MehtaNo ratings yet

- Samsung Tab InvoiceDocument1 pageSamsung Tab InvoiceShantanu BhardwajNo ratings yet

- Star Wars7 - Accounting CycleDocument8 pagesStar Wars7 - Accounting CyclemillionextupNo ratings yet

- January February March Beginning Cash BalanceDocument6 pagesJanuary February March Beginning Cash BalanceALBERTO MARIO CHAMORRO PACHECONo ratings yet

- Handsout 06 Chap 03 Part 02Document4 pagesHandsout 06 Chap 03 Part 02Shane VeiraNo ratings yet

- BT Ias1 (SV)Document3 pagesBT Ias1 (SV)HÀ THỚI NGUYỄN NGÂNNo ratings yet

- 助教課講義 Ch.4Document12 pages助教課講義 Ch.45213adamNo ratings yet

- Group Assignment On Fundamentals of Accounting IDocument6 pagesGroup Assignment On Fundamentals of Accounting IKaleab ShimelsNo ratings yet

- Soal Mojakoe-UTS Akuntansi Keuangan 1 Ganjil 2020-2021Document9 pagesSoal Mojakoe-UTS Akuntansi Keuangan 1 Ganjil 2020-2021Vincenttio le CloudNo ratings yet

- Exam 2021 (Resolution)Document9 pagesExam 2021 (Resolution)Chi Kei KeungNo ratings yet

- Chapter 4 Review Principles of Accounting AnswersDocument3 pagesChapter 4 Review Principles of Accounting AnswersChien Phuong ThanhNo ratings yet

- Tugas Accounting 1 With NotesDocument14 pagesTugas Accounting 1 With Notesvico lorenzoNo ratings yet

- Seminar 4 - QsDocument3 pagesSeminar 4 - QsMaman AbdurrahmanNo ratings yet

- Practice Exam FinalsDocument2 pagesPractice Exam FinalsPauline Jasmine Sta AnaNo ratings yet

- Classroom Exerisises On Presentation of Financial Statements PDFDocument2 pagesClassroom Exerisises On Presentation of Financial Statements PDFalyssaNo ratings yet

- Far01 - The Financial Statements PresentationDocument10 pagesFar01 - The Financial Statements PresentationRNo ratings yet

- IFRS Week 6Document4 pagesIFRS Week 6AleksandraNo ratings yet

- 1 Partnership-YTDocument7 pages1 Partnership-YTSherwin DueNo ratings yet

- Mockbiard Questions - Practical 1Document10 pagesMockbiard Questions - Practical 1Regina Clarete0% (1)

- Adjusting EntriesDocument5 pagesAdjusting EntriesM Hassan BrohiNo ratings yet

- Exercises On Projected Financial StatementsDocument2 pagesExercises On Projected Financial StatementsSharmaine LiasosNo ratings yet

- Accounting TestDocument4 pagesAccounting Testdinda ardiyaniNo ratings yet

- Exercise 5 - Completing The Accounting Cycle For Merchandising and Service BusinessDocument4 pagesExercise 5 - Completing The Accounting Cycle For Merchandising and Service BusinessShiela Rengel0% (2)

- Chapter 5 Exercises-Exercise BankDocument9 pagesChapter 5 Exercises-Exercise BankPATRICIUS ALAN WIRAYUDHA KUSUMNo ratings yet

- Long Quiz P1Document2 pagesLong Quiz P1chonana0408No ratings yet

- Accounting 2Document18 pagesAccounting 2cherryannNo ratings yet

- Amended - Final - Unit 5 - AAB-Accounting Principles - A2Document6 pagesAmended - Final - Unit 5 - AAB-Accounting Principles - A2Quang MinhNo ratings yet

- Statement of Cash FlowsDocument6 pagesStatement of Cash FlowsLuiNo ratings yet

- Asdos Pert 2Document2 pagesAsdos Pert 2mutiaoooNo ratings yet

- Account AssignmentDocument4 pagesAccount AssignmentNavjeet SandhuNo ratings yet

- Acc5115 - Intermediate Financial Reporting Statement of Comprehensive Income and Changes in Owner'S Equity Problem ADocument6 pagesAcc5115 - Intermediate Financial Reporting Statement of Comprehensive Income and Changes in Owner'S Equity Problem ARachel LuberiaNo ratings yet

- 6727 Statement of Financial PositionDocument3 pages6727 Statement of Financial PositionJane ValenciaNo ratings yet

- 2019-06 ICMAB FL 001 PAC Year Question JUNE 2019Document3 pages2019-06 ICMAB FL 001 PAC Year Question JUNE 2019Mohammad ShahidNo ratings yet

- Intermediate Accounting 2 Topic: Unearned RevenuesDocument5 pagesIntermediate Accounting 2 Topic: Unearned RevenuesJhazreel BiasuraNo ratings yet

- Problem Cash FlowDocument3 pagesProblem Cash FlowKimberly AnneNo ratings yet

- Instructions: Amazon Seller Buys Printer Supplies For $29 With CashDocument1 pageInstructions: Amazon Seller Buys Printer Supplies For $29 With CashJorge FloresNo ratings yet

- P1 QuestionsDocument31 pagesP1 QuestionsWillen Christia M. MadulidNo ratings yet

- Auditing Problem Assignment Lyeca JoieDocument12 pagesAuditing Problem Assignment Lyeca JoieEsse ValdezNo ratings yet

- Acc 1 QuizDocument7 pagesAcc 1 QuizAyat MukahalNo ratings yet

- Revision Pack QuestionsDocument12 pagesRevision Pack QuestionsAmmaarah PatelNo ratings yet

- Soal Tugas Akm Is - ST o FP - CFDocument6 pagesSoal Tugas Akm Is - ST o FP - CFElyssa Fiqri Fauziah0% (1)

- Accounting Yr11 2022Document8 pagesAccounting Yr11 2022keishacamilleriNo ratings yet

- Solving - Business Finance 1-6Document28 pagesSolving - Business Finance 1-6Samson, Ma. Louise Ren A.No ratings yet

- Session 11,12&13 AssignmentDocument3 pagesSession 11,12&13 AssignmentMardi SutiosoNo ratings yet

- Cash and Accrual BasisDocument4 pagesCash and Accrual BasisBwwwiiiii100% (1)

- P1 - ReviewDocument14 pagesP1 - ReviewEvitaAyneMaliñanaTapit0% (2)

- Semi-Finals Financial Accounting and ReportingDocument23 pagesSemi-Finals Financial Accounting and Reportingjoyce KimNo ratings yet

- Exercises III - Accruals and Deferrals Adjusting EntriesDocument2 pagesExercises III - Accruals and Deferrals Adjusting EntriesJowjie TV50% (2)

- IAET TaxationDocument2 pagesIAET TaxationRandy Manzano100% (1)

- Mittens Kittens CompanyDocument5 pagesMittens Kittens CompanyDianna EsmerayNo ratings yet

- Fina 470 Project Two - Check PointDocument9 pagesFina 470 Project Two - Check PointMitchell ParrottNo ratings yet

- Statement of Comprehensive IncomeDocument4 pagesStatement of Comprehensive Incomebobo tangaNo ratings yet

- Review For Quiz 3 Part 2Document18 pagesReview For Quiz 3 Part 2Mariah ValizadoNo ratings yet

- Pilot TestDocument6 pagesPilot TestNguyễn Thị Ngọc AnhNo ratings yet

- Wahyudi Syaputra - Assignment Week 13Document11 pagesWahyudi Syaputra - Assignment Week 13Wahyudi SyaputraNo ratings yet

- MOD2 Statement of Cash FlowsDocument2 pagesMOD2 Statement of Cash FlowsGemma DenolanNo ratings yet

- Homework On Statement of Cash FlowsDocument2 pagesHomework On Statement of Cash FlowsAmy SpencerNo ratings yet

- J.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineFrom EverandJ.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineNo ratings yet

- PBL Marketing StrategyDocument4 pagesPBL Marketing StrategyLisna Gitq SilviaNo ratings yet

- Accounting For Merchandising Activities: Solutions Manual For Chapter 6 435Document163 pagesAccounting For Merchandising Activities: Solutions Manual For Chapter 6 435debora yosikaNo ratings yet

- Ch8 Income Statement Worksheet AnswersDocument2 pagesCh8 Income Statement Worksheet Answerssalma RamadanNo ratings yet

- 7.1 - Business Plan SampleDocument1 page7.1 - Business Plan SampleSneha HiraniNo ratings yet

- Supply Chains and The Value Delivery NetworkDocument4 pagesSupply Chains and The Value Delivery NetworkJennyNo ratings yet

- Sales Forcaast and Sales QuotasDocument21 pagesSales Forcaast and Sales QuotasKunal SainiNo ratings yet

- Think Pair Share: Case Snippet 1: 10 MarksDocument2 pagesThink Pair Share: Case Snippet 1: 10 MarksShri RavanNo ratings yet

- Executive Summary: 1.1 Introduction To BeiersdorfDocument19 pagesExecutive Summary: 1.1 Introduction To BeiersdorfLogesh WaranNo ratings yet

- Blood Bananas Case AnalysisDocument1 pageBlood Bananas Case AnalysisVanessa LantajoNo ratings yet

- TotalDocument3 pagesTotalshibbuNo ratings yet

- Ia - 13Document17 pagesIa - 13Ma. Fatima H. FabayNo ratings yet

- Pi 4400000700Document1 pagePi 4400000700KrishnaNo ratings yet

- Business Math Module 4 StudentsDocument26 pagesBusiness Math Module 4 StudentsMarck Lorenz BellenNo ratings yet

- YTDocument3 pagesYTARYAJAI SINGHNo ratings yet

- CPA Review On FARDocument5 pagesCPA Review On FARYlor NoniuqNo ratings yet

- OM Chapter-3Document206 pagesOM Chapter-3TIZITAW MASRESHANo ratings yet

- Far TheoriesDocument6 pagesFar TheoriesallijahNo ratings yet

- P2 - Bba Entrepreneurship Project Log Book Top Sheet 2019-2020Document10 pagesP2 - Bba Entrepreneurship Project Log Book Top Sheet 2019-2020elvee.hrNo ratings yet

- Contract Allocation - Stand Alone Selling PriceDocument19 pagesContract Allocation - Stand Alone Selling Pricenagalakshmi100% (1)

- Business PlanningDocument49 pagesBusiness PlanningMinka BoydNo ratings yet

- A Case Study On Dabur LTDDocument3 pagesA Case Study On Dabur LTDgarimaamityNo ratings yet

- Case 14-63Document2 pagesCase 14-63KamruzzamanNo ratings yet

- ProjectDocument62 pagesProjectprince_soni_9No ratings yet

- ComercialInvoice PCW154986096Document1 pageComercialInvoice PCW154986096Quan VũNo ratings yet

- MGN 806Document14 pagesMGN 806Winnie StellaNo ratings yet

- Unit III Manufacturing ConcernDocument12 pagesUnit III Manufacturing ConcernAlezandra SantelicesNo ratings yet

- Inventory Procedures: Step OneDocument12 pagesInventory Procedures: Step OneNoorul HuqNo ratings yet