SSRN Id3198093

SSRN Id3198093

You might also like

- Doom GrinderDocument2 pagesDoom Grindermonel_24671No ratings yet

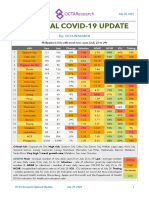

- National COVID-19 Update by Octa Research On July 30, 2021Document2 pagesNational COVID-19 Update by Octa Research On July 30, 2021RapplerNo ratings yet

- Climate Change & Disaster Management in Pakistan Challenges & Way ForwardDocument57 pagesClimate Change & Disaster Management in Pakistan Challenges & Way ForwardiqraNo ratings yet

- Salm Aer 2021Document11 pagesSalm Aer 2021Septy KawaiNo ratings yet

- Uganda National Planning Authority Coronavirus Position PaperDocument46 pagesUganda National Planning Authority Coronavirus Position PaperAfrican Centre for Media Excellence100% (1)

- Climate Change Impacts On Infectious Diseases in The EasternDocument17 pagesClimate Change Impacts On Infectious Diseases in The EasternYasmine HusseinNo ratings yet

- 2022 Quiz BeeDocument27 pages2022 Quiz BeepatrimoniomicaNo ratings yet

- Investigating The Relationship Between National Income, Carbon Emissions, and Food ProductionDocument6 pagesInvestigating The Relationship Between National Income, Carbon Emissions, and Food ProductionDanial IhsanNo ratings yet

- BP Energy Outlook 2019 Chart Data PackDocument143 pagesBP Energy Outlook 2019 Chart Data PackheminNo ratings yet

- Real GDPValuesDocument84 pagesReal GDPValuesdanilkrivov23No ratings yet

- Country RichDocument37 pagesCountry RichYash ChaurasiaNo ratings yet

- 1.1) Sectorial Composition of GDP of Pakistan.2Document1 page1.1) Sectorial Composition of GDP of Pakistan.2Syed Ashar ShahidNo ratings yet

- Gono Aer 2022 Report FinalDocument10 pagesGono Aer 2022 Report FinalLIFO LIFO (Magazine)No ratings yet

- New Educational Patway For Global Public Health SecurityDocument34 pagesNew Educational Patway For Global Public Health SecurityJay Ann LucasNo ratings yet

- Coronavirus Disease (COVID-19) : Situation Report - 198Document19 pagesCoronavirus Disease (COVID-19) : Situation Report - 198CityNewsTorontoNo ratings yet

- Mortality Analyses - Johns Hopkins Coronavirus Resource CenterDocument1 pageMortality Analyses - Johns Hopkins Coronavirus Resource CenterMarina SturichNo ratings yet

- GDPper CapitaDocument9 pagesGDPper Capitajupiter00071No ratings yet

- Porumbul În Funcție de Suprafață, Producție Și UmiditateDocument10 pagesPorumbul În Funcție de Suprafață, Producție Și UmiditateAncuta DanielaNo ratings yet

- Current Protected Area (Pa) Coverage of Alliance For Zero Extinction (Aze) Sites by Country (Data Supplied by Birdlife International)Document4 pagesCurrent Protected Area (Pa) Coverage of Alliance For Zero Extinction (Aze) Sites by Country (Data Supplied by Birdlife International)rezaNo ratings yet

- Vexp 22Document2 pagesVexp 22Jamal SalmanNo ratings yet

- List of TablesDocument129 pagesList of Tablesဒုကၡ သစၥာNo ratings yet

- Assignment I: Statistics For Agricultural Research VAR3013 Second Semester 2017/2018 LecturerDocument3 pagesAssignment I: Statistics For Agricultural Research VAR3013 Second Semester 2017/2018 LecturerEmilna SuzanneNo ratings yet

- Climate Change (POLIGON)Document16 pagesClimate Change (POLIGON)Nurdayanti SNo ratings yet

- USR2021 - Publications On Cross-Cutting Strategic TechnologiesDocument590 pagesUSR2021 - Publications On Cross-Cutting Strategic TechnologiesjosebermardorafaelNo ratings yet

- SAC 1 - Data Analysis - 1. PRE DATADocument2 pagesSAC 1 - Data Analysis - 1. PRE DATAyeeeetNo ratings yet

- World-Wide Direct Uses of Geothermal Energy 2000: John W. Lund, Derek H. FreestonDocument40 pagesWorld-Wide Direct Uses of Geothermal Energy 2000: John W. Lund, Derek H. FreestonGloria Luciana Muñoz VillalobosNo ratings yet

- Gold Mining Production Volumes DataDocument6 pagesGold Mining Production Volumes DataM Rallupy MeyraldoNo ratings yet

- E.1c World Per Capita Total Primary Energy Consumption, 1980-2006Document24 pagesE.1c World Per Capita Total Primary Energy Consumption, 1980-2006mihir_mhkNo ratings yet

- Covid Status Bulletin: Government of Telangana Office of The Director of Public Health and Family WelfareDocument9 pagesCovid Status Bulletin: Government of Telangana Office of The Director of Public Health and Family Welfareunbeliavble videosNo ratings yet

- Press-release-Ember-European-Electricity-Review-2024Document6 pagesPress-release-Ember-European-Electricity-Review-2024lolsolo5500No ratings yet

- Textile and The EU-Pakistan Trade Relations:: Past Perspective and Future ProspectsDocument25 pagesTextile and The EU-Pakistan Trade Relations:: Past Perspective and Future Prospectssams007No ratings yet

- India: Confectionery & SnacksDocument11 pagesIndia: Confectionery & SnacksNitu PathakNo ratings yet

- A Comparative Analysis of GDP Patterns in Bangladesh and Sri LankaDocument17 pagesA Comparative Analysis of GDP Patterns in Bangladesh and Sri LankaBlah BlahNo ratings yet

- Measles 2019 AerDocument9 pagesMeasles 2019 AerJose BritesNo ratings yet

- Disasters: An OverviewDocument21 pagesDisasters: An OverviewfirsamNo ratings yet

- Exports of Goods - % of GDPDocument5 pagesExports of Goods - % of GDPmeibrahim10No ratings yet

- Giignl 2021 Annual Report Apr27Document2 pagesGiignl 2021 Annual Report Apr27Andres SerranoNo ratings yet

- WHO COVID-19 Report For August 4, 2020Document18 pagesWHO COVID-19 Report For August 4, 2020CityNewsTorontoNo ratings yet

- Capacity Factors by Energy SourceDocument2 pagesCapacity Factors by Energy SourceSatyender Kumar JainNo ratings yet

- Statistical Annex WCR 2022Document30 pagesStatistical Annex WCR 2022Lorena PérezNo ratings yet

- Group # Vol of Water Added (ML) Compaction Mold (KG) Mold + Soil (KG) Empty Tin (G) Tin + Moist Soil (G) Tin+Dry Soil (G)Document7 pagesGroup # Vol of Water Added (ML) Compaction Mold (KG) Mold + Soil (KG) Empty Tin (G) Tin + Moist Soil (G) Tin+Dry Soil (G)Jose Raul Zela ConchaNo ratings yet

- Countries in The World by Population (2020)Document3 pagesCountries in The World by Population (2020)Judith AlindayoNo ratings yet

- Smart Home Fullpagedownload StatistaDocument11 pagesSmart Home Fullpagedownload Statistakpankaj88No ratings yet

- Linear Regression AssignmentDocument15 pagesLinear Regression AssignmentrizkaNo ratings yet

- World Population Data 2023Document27 pagesWorld Population Data 2023yogitagamimakNo ratings yet

- Findings, Results and Interpretations 4.1 Data Analysis On Incidence and Severity of FAWDocument3 pagesFindings, Results and Interpretations 4.1 Data Analysis On Incidence and Severity of FAWAlinaitwe GodfNo ratings yet

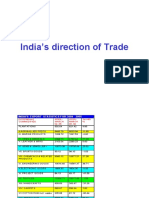

- India's Direction of TradeDocument16 pagesIndia's Direction of TradepanchnaNo ratings yet

- Countries and AreasDocument7 pagesCountries and AreasDevrajNo ratings yet

- USR2021 - Table - World Shares by Broad Field of Scientific PublishingDocument6 pagesUSR2021 - Table - World Shares by Broad Field of Scientific PublishingjosebermardorafaelNo ratings yet

- Aging Population (Assgt)Document27 pagesAging Population (Assgt)Thessa Lonica GarciaNo ratings yet

- 10 1111@jog 14382 PDFDocument7 pages10 1111@jog 14382 PDFJoie C. BesinanNo ratings yet

- Presented By:: Shahid Sohail Director STP (CDA)Document29 pagesPresented By:: Shahid Sohail Director STP (CDA)ssohail100% (1)

- 2024 PredicitionDocument40 pages2024 PredicitionjameschandruuNo ratings yet

- Demo Ndivind$defaultview SpreadsheetDocument19 pagesDemo Ndivind$defaultview SpreadsheetDaniela TunaruNo ratings yet

- Food - Good Bad and The UglyDocument19 pagesFood - Good Bad and The UglyAbdul JohnyyNo ratings yet

- GED102 Module 3 Project: Group Members: Raynard Yu John Luis Arce Miguel Agustin Galang Paul Cauman Renz Eugene GurionDocument6 pagesGED102 Module 3 Project: Group Members: Raynard Yu John Luis Arce Miguel Agustin Galang Paul Cauman Renz Eugene GurionqwertasdfgNo ratings yet

- Samoa External Debt by Tarun Das Part 2 TablesDocument8 pagesSamoa External Debt by Tarun Das Part 2 TablesProfessor Tarun DasNo ratings yet

- Ukraine Development Impact UNDPDocument10 pagesUkraine Development Impact UNDPValentin FilipNo ratings yet

- Greenbook Chapter 14a 4september2023Document54 pagesGreenbook Chapter 14a 4september2023shubham198No ratings yet

- Seminar QN - Econometrics - June2024Document6 pagesSeminar QN - Econometrics - June2024Juma RidhiwaniNo ratings yet

- IHS 2022w29998Document12 pagesIHS 2022w29998Sebastián IsaíasNo ratings yet

- Gregory 2023 SSRNDocument43 pagesGregory 2023 SSRNSebastián IsaíasNo ratings yet

- Mossin Econometrica1966Document16 pagesMossin Econometrica1966Sebastián IsaíasNo ratings yet

- Coase at Sixty - Medema - Steve - Mars2018Document126 pagesCoase at Sixty - Medema - Steve - Mars2018Sebastián IsaíasNo ratings yet

- Debreu Based ModelDocument6 pagesDebreu Based ModelSebastián IsaíasNo ratings yet

- Final IRP MCMCDocument25 pagesFinal IRP MCMCSamiullah ShaikhNo ratings yet

- SIGNALMAN by Charles DickensDocument8 pagesSIGNALMAN by Charles DickensAdeel MuzaffarNo ratings yet

- Guidelines For Proposals 2012Document202 pagesGuidelines For Proposals 2012thedukeofsantiagoNo ratings yet

- 4 Reasons To Consider The Monolithic Dome!Document2 pages4 Reasons To Consider The Monolithic Dome!nithya kjNo ratings yet

- Introduction To DisastersDocument52 pagesIntroduction To DisastersNmn FaltuNo ratings yet

- Accomplishment Report DRRMDocument9 pagesAccomplishment Report DRRMPalmes Joseph100% (1)

- Appendix 2Document45 pagesAppendix 2rufino delacruzNo ratings yet

- Explanation Text by AndresDocument4 pagesExplanation Text by AndresAndi Resky Putri AnggelikaNo ratings yet

- Hazard Vulnerability Analysis WorkheetDocument10 pagesHazard Vulnerability Analysis WorkheetFines AdemukhlisNo ratings yet

- Schools Division of Nueva Ecija SDO Guimba East Annex: Annex V. I. ObjectivesDocument4 pagesSchools Division of Nueva Ecija SDO Guimba East Annex: Annex V. I. ObjectivesNatividad Jo Ann CuadroNo ratings yet

- INSTUTIONALIZATION PrgramDocument4 pagesINSTUTIONALIZATION PrgramHEMS SAMCHNo ratings yet

- 01 - Emergency Responce - DisasterDocument29 pages01 - Emergency Responce - DisasterIkhsan Sri MartadiNo ratings yet

- Singapore City Skyline at Night PowerPoint Template #54219Document20 pagesSingapore City Skyline at Night PowerPoint Template #54219Faaz ZubairNo ratings yet

- Brian K. Shaw - Homeland Security Is More Than Homeland DefenseDocument47 pagesBrian K. Shaw - Homeland Security Is More Than Homeland DefenseDrift0242No ratings yet

- Types of DisasterDocument39 pagesTypes of DisasterAna Mae CerdanioNo ratings yet

- Cot 1-2022Document6 pagesCot 1-2022Lemuel Jr MitchaoNo ratings yet

- AltLM Lesson 4 PDFDocument9 pagesAltLM Lesson 4 PDFJoan F. MaligNo ratings yet

- Netw Rks Guided Reading Activity: Essential Question: How Does Geography Influence TheDocument3 pagesNetw Rks Guided Reading Activity: Essential Question: How Does Geography Influence TheRamses octavio Rodriguez ocanasNo ratings yet

- Disaster Management ACt, 2005Document2 pagesDisaster Management ACt, 2005aswin donNo ratings yet

- Term Paper in EthicsDocument16 pagesTerm Paper in Ethicspriyabrata8No ratings yet

- Doll House As Modern TragedyDocument9 pagesDoll House As Modern TragedyMuneeb Tahir SaleemiNo ratings yet

- EQR UttarkashiDocument8 pagesEQR UttarkashiArjunNo ratings yet

- Risk Assessment of Seismic Vulnerability of All Hospitals in Manila Using Rapid Visual Screening (RVS)Document7 pagesRisk Assessment of Seismic Vulnerability of All Hospitals in Manila Using Rapid Visual Screening (RVS)Stephen John ClementeNo ratings yet

- Black Death Research PaperDocument7 pagesBlack Death Research PaperBrian ToNo ratings yet

- Climate Change and PovertyDocument49 pagesClimate Change and Povertykshahyd05No ratings yet

- 2230 Insert ON 2011 P1 and P2 Brunei GeographyDocument3 pages2230 Insert ON 2011 P1 and P2 Brunei GeographyNadd Azis100% (1)

- Demo Lesson Plan - SecondgradingDocument6 pagesDemo Lesson Plan - Secondgradingmary grace100% (1)

- Executive Order BDRRMCDocument3 pagesExecutive Order BDRRMCJeverlyn Enriquez FlamencoNo ratings yet

- Brmedj04058 0036eDocument1 pageBrmedj04058 0036ekoidanaNo ratings yet

Download as pdf or txt

You might also like

- Doom GrinderDocument2 pagesDoom Grindermonel_24671No ratings yet

- National COVID-19 Update by Octa Research On July 30, 2021Document2 pagesNational COVID-19 Update by Octa Research On July 30, 2021RapplerNo ratings yet

- Climate Change & Disaster Management in Pakistan Challenges & Way ForwardDocument57 pagesClimate Change & Disaster Management in Pakistan Challenges & Way ForwardiqraNo ratings yet

- Salm Aer 2021Document11 pagesSalm Aer 2021Septy KawaiNo ratings yet

- Uganda National Planning Authority Coronavirus Position PaperDocument46 pagesUganda National Planning Authority Coronavirus Position PaperAfrican Centre for Media Excellence100% (1)

- Climate Change Impacts On Infectious Diseases in The EasternDocument17 pagesClimate Change Impacts On Infectious Diseases in The EasternYasmine HusseinNo ratings yet

- 2022 Quiz BeeDocument27 pages2022 Quiz BeepatrimoniomicaNo ratings yet

- Investigating The Relationship Between National Income, Carbon Emissions, and Food ProductionDocument6 pagesInvestigating The Relationship Between National Income, Carbon Emissions, and Food ProductionDanial IhsanNo ratings yet

- BP Energy Outlook 2019 Chart Data PackDocument143 pagesBP Energy Outlook 2019 Chart Data PackheminNo ratings yet

- Real GDPValuesDocument84 pagesReal GDPValuesdanilkrivov23No ratings yet

- Country RichDocument37 pagesCountry RichYash ChaurasiaNo ratings yet

- 1.1) Sectorial Composition of GDP of Pakistan.2Document1 page1.1) Sectorial Composition of GDP of Pakistan.2Syed Ashar ShahidNo ratings yet

- Gono Aer 2022 Report FinalDocument10 pagesGono Aer 2022 Report FinalLIFO LIFO (Magazine)No ratings yet

- New Educational Patway For Global Public Health SecurityDocument34 pagesNew Educational Patway For Global Public Health SecurityJay Ann LucasNo ratings yet

- Coronavirus Disease (COVID-19) : Situation Report - 198Document19 pagesCoronavirus Disease (COVID-19) : Situation Report - 198CityNewsTorontoNo ratings yet

- Mortality Analyses - Johns Hopkins Coronavirus Resource CenterDocument1 pageMortality Analyses - Johns Hopkins Coronavirus Resource CenterMarina SturichNo ratings yet

- GDPper CapitaDocument9 pagesGDPper Capitajupiter00071No ratings yet

- Porumbul În Funcție de Suprafață, Producție Și UmiditateDocument10 pagesPorumbul În Funcție de Suprafață, Producție Și UmiditateAncuta DanielaNo ratings yet

- Current Protected Area (Pa) Coverage of Alliance For Zero Extinction (Aze) Sites by Country (Data Supplied by Birdlife International)Document4 pagesCurrent Protected Area (Pa) Coverage of Alliance For Zero Extinction (Aze) Sites by Country (Data Supplied by Birdlife International)rezaNo ratings yet

- Vexp 22Document2 pagesVexp 22Jamal SalmanNo ratings yet

- List of TablesDocument129 pagesList of Tablesဒုကၡ သစၥာNo ratings yet

- Assignment I: Statistics For Agricultural Research VAR3013 Second Semester 2017/2018 LecturerDocument3 pagesAssignment I: Statistics For Agricultural Research VAR3013 Second Semester 2017/2018 LecturerEmilna SuzanneNo ratings yet

- Climate Change (POLIGON)Document16 pagesClimate Change (POLIGON)Nurdayanti SNo ratings yet

- USR2021 - Publications On Cross-Cutting Strategic TechnologiesDocument590 pagesUSR2021 - Publications On Cross-Cutting Strategic TechnologiesjosebermardorafaelNo ratings yet

- SAC 1 - Data Analysis - 1. PRE DATADocument2 pagesSAC 1 - Data Analysis - 1. PRE DATAyeeeetNo ratings yet

- World-Wide Direct Uses of Geothermal Energy 2000: John W. Lund, Derek H. FreestonDocument40 pagesWorld-Wide Direct Uses of Geothermal Energy 2000: John W. Lund, Derek H. FreestonGloria Luciana Muñoz VillalobosNo ratings yet

- Gold Mining Production Volumes DataDocument6 pagesGold Mining Production Volumes DataM Rallupy MeyraldoNo ratings yet

- E.1c World Per Capita Total Primary Energy Consumption, 1980-2006Document24 pagesE.1c World Per Capita Total Primary Energy Consumption, 1980-2006mihir_mhkNo ratings yet

- Covid Status Bulletin: Government of Telangana Office of The Director of Public Health and Family WelfareDocument9 pagesCovid Status Bulletin: Government of Telangana Office of The Director of Public Health and Family Welfareunbeliavble videosNo ratings yet

- Press-release-Ember-European-Electricity-Review-2024Document6 pagesPress-release-Ember-European-Electricity-Review-2024lolsolo5500No ratings yet

- Textile and The EU-Pakistan Trade Relations:: Past Perspective and Future ProspectsDocument25 pagesTextile and The EU-Pakistan Trade Relations:: Past Perspective and Future Prospectssams007No ratings yet

- India: Confectionery & SnacksDocument11 pagesIndia: Confectionery & SnacksNitu PathakNo ratings yet

- A Comparative Analysis of GDP Patterns in Bangladesh and Sri LankaDocument17 pagesA Comparative Analysis of GDP Patterns in Bangladesh and Sri LankaBlah BlahNo ratings yet

- Measles 2019 AerDocument9 pagesMeasles 2019 AerJose BritesNo ratings yet

- Disasters: An OverviewDocument21 pagesDisasters: An OverviewfirsamNo ratings yet

- Exports of Goods - % of GDPDocument5 pagesExports of Goods - % of GDPmeibrahim10No ratings yet

- Giignl 2021 Annual Report Apr27Document2 pagesGiignl 2021 Annual Report Apr27Andres SerranoNo ratings yet

- WHO COVID-19 Report For August 4, 2020Document18 pagesWHO COVID-19 Report For August 4, 2020CityNewsTorontoNo ratings yet

- Capacity Factors by Energy SourceDocument2 pagesCapacity Factors by Energy SourceSatyender Kumar JainNo ratings yet

- Statistical Annex WCR 2022Document30 pagesStatistical Annex WCR 2022Lorena PérezNo ratings yet

- Group # Vol of Water Added (ML) Compaction Mold (KG) Mold + Soil (KG) Empty Tin (G) Tin + Moist Soil (G) Tin+Dry Soil (G)Document7 pagesGroup # Vol of Water Added (ML) Compaction Mold (KG) Mold + Soil (KG) Empty Tin (G) Tin + Moist Soil (G) Tin+Dry Soil (G)Jose Raul Zela ConchaNo ratings yet

- Countries in The World by Population (2020)Document3 pagesCountries in The World by Population (2020)Judith AlindayoNo ratings yet

- Smart Home Fullpagedownload StatistaDocument11 pagesSmart Home Fullpagedownload Statistakpankaj88No ratings yet

- Linear Regression AssignmentDocument15 pagesLinear Regression AssignmentrizkaNo ratings yet

- World Population Data 2023Document27 pagesWorld Population Data 2023yogitagamimakNo ratings yet

- Findings, Results and Interpretations 4.1 Data Analysis On Incidence and Severity of FAWDocument3 pagesFindings, Results and Interpretations 4.1 Data Analysis On Incidence and Severity of FAWAlinaitwe GodfNo ratings yet

- India's Direction of TradeDocument16 pagesIndia's Direction of TradepanchnaNo ratings yet

- Countries and AreasDocument7 pagesCountries and AreasDevrajNo ratings yet

- USR2021 - Table - World Shares by Broad Field of Scientific PublishingDocument6 pagesUSR2021 - Table - World Shares by Broad Field of Scientific PublishingjosebermardorafaelNo ratings yet

- Aging Population (Assgt)Document27 pagesAging Population (Assgt)Thessa Lonica GarciaNo ratings yet

- 10 1111@jog 14382 PDFDocument7 pages10 1111@jog 14382 PDFJoie C. BesinanNo ratings yet

- Presented By:: Shahid Sohail Director STP (CDA)Document29 pagesPresented By:: Shahid Sohail Director STP (CDA)ssohail100% (1)

- 2024 PredicitionDocument40 pages2024 PredicitionjameschandruuNo ratings yet

- Demo Ndivind$defaultview SpreadsheetDocument19 pagesDemo Ndivind$defaultview SpreadsheetDaniela TunaruNo ratings yet

- Food - Good Bad and The UglyDocument19 pagesFood - Good Bad and The UglyAbdul JohnyyNo ratings yet

- GED102 Module 3 Project: Group Members: Raynard Yu John Luis Arce Miguel Agustin Galang Paul Cauman Renz Eugene GurionDocument6 pagesGED102 Module 3 Project: Group Members: Raynard Yu John Luis Arce Miguel Agustin Galang Paul Cauman Renz Eugene GurionqwertasdfgNo ratings yet

- Samoa External Debt by Tarun Das Part 2 TablesDocument8 pagesSamoa External Debt by Tarun Das Part 2 TablesProfessor Tarun DasNo ratings yet

- Ukraine Development Impact UNDPDocument10 pagesUkraine Development Impact UNDPValentin FilipNo ratings yet

- Greenbook Chapter 14a 4september2023Document54 pagesGreenbook Chapter 14a 4september2023shubham198No ratings yet

- Seminar QN - Econometrics - June2024Document6 pagesSeminar QN - Econometrics - June2024Juma RidhiwaniNo ratings yet

- IHS 2022w29998Document12 pagesIHS 2022w29998Sebastián IsaíasNo ratings yet

- Gregory 2023 SSRNDocument43 pagesGregory 2023 SSRNSebastián IsaíasNo ratings yet

- Mossin Econometrica1966Document16 pagesMossin Econometrica1966Sebastián IsaíasNo ratings yet

- Coase at Sixty - Medema - Steve - Mars2018Document126 pagesCoase at Sixty - Medema - Steve - Mars2018Sebastián IsaíasNo ratings yet

- Debreu Based ModelDocument6 pagesDebreu Based ModelSebastián IsaíasNo ratings yet

- Final IRP MCMCDocument25 pagesFinal IRP MCMCSamiullah ShaikhNo ratings yet

- SIGNALMAN by Charles DickensDocument8 pagesSIGNALMAN by Charles DickensAdeel MuzaffarNo ratings yet

- Guidelines For Proposals 2012Document202 pagesGuidelines For Proposals 2012thedukeofsantiagoNo ratings yet

- 4 Reasons To Consider The Monolithic Dome!Document2 pages4 Reasons To Consider The Monolithic Dome!nithya kjNo ratings yet

- Introduction To DisastersDocument52 pagesIntroduction To DisastersNmn FaltuNo ratings yet

- Accomplishment Report DRRMDocument9 pagesAccomplishment Report DRRMPalmes Joseph100% (1)

- Appendix 2Document45 pagesAppendix 2rufino delacruzNo ratings yet

- Explanation Text by AndresDocument4 pagesExplanation Text by AndresAndi Resky Putri AnggelikaNo ratings yet

- Hazard Vulnerability Analysis WorkheetDocument10 pagesHazard Vulnerability Analysis WorkheetFines AdemukhlisNo ratings yet

- Schools Division of Nueva Ecija SDO Guimba East Annex: Annex V. I. ObjectivesDocument4 pagesSchools Division of Nueva Ecija SDO Guimba East Annex: Annex V. I. ObjectivesNatividad Jo Ann CuadroNo ratings yet

- INSTUTIONALIZATION PrgramDocument4 pagesINSTUTIONALIZATION PrgramHEMS SAMCHNo ratings yet

- 01 - Emergency Responce - DisasterDocument29 pages01 - Emergency Responce - DisasterIkhsan Sri MartadiNo ratings yet

- Singapore City Skyline at Night PowerPoint Template #54219Document20 pagesSingapore City Skyline at Night PowerPoint Template #54219Faaz ZubairNo ratings yet

- Brian K. Shaw - Homeland Security Is More Than Homeland DefenseDocument47 pagesBrian K. Shaw - Homeland Security Is More Than Homeland DefenseDrift0242No ratings yet

- Types of DisasterDocument39 pagesTypes of DisasterAna Mae CerdanioNo ratings yet

- Cot 1-2022Document6 pagesCot 1-2022Lemuel Jr MitchaoNo ratings yet

- AltLM Lesson 4 PDFDocument9 pagesAltLM Lesson 4 PDFJoan F. MaligNo ratings yet

- Netw Rks Guided Reading Activity: Essential Question: How Does Geography Influence TheDocument3 pagesNetw Rks Guided Reading Activity: Essential Question: How Does Geography Influence TheRamses octavio Rodriguez ocanasNo ratings yet

- Disaster Management ACt, 2005Document2 pagesDisaster Management ACt, 2005aswin donNo ratings yet

- Term Paper in EthicsDocument16 pagesTerm Paper in Ethicspriyabrata8No ratings yet

- Doll House As Modern TragedyDocument9 pagesDoll House As Modern TragedyMuneeb Tahir SaleemiNo ratings yet

- EQR UttarkashiDocument8 pagesEQR UttarkashiArjunNo ratings yet

- Risk Assessment of Seismic Vulnerability of All Hospitals in Manila Using Rapid Visual Screening (RVS)Document7 pagesRisk Assessment of Seismic Vulnerability of All Hospitals in Manila Using Rapid Visual Screening (RVS)Stephen John ClementeNo ratings yet

- Black Death Research PaperDocument7 pagesBlack Death Research PaperBrian ToNo ratings yet

- Climate Change and PovertyDocument49 pagesClimate Change and Povertykshahyd05No ratings yet

- 2230 Insert ON 2011 P1 and P2 Brunei GeographyDocument3 pages2230 Insert ON 2011 P1 and P2 Brunei GeographyNadd Azis100% (1)

- Demo Lesson Plan - SecondgradingDocument6 pagesDemo Lesson Plan - Secondgradingmary grace100% (1)

- Executive Order BDRRMCDocument3 pagesExecutive Order BDRRMCJeverlyn Enriquez FlamencoNo ratings yet

- Brmedj04058 0036eDocument1 pageBrmedj04058 0036ekoidanaNo ratings yet