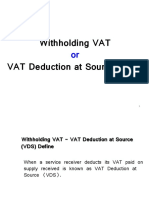

2021 Week 56 VAT

2021 Week 56 VAT

You might also like

- Chase 1099int 2013Document2 pagesChase 1099int 2013Srikala Venkatesan100% (1)

- Bac03-Chapter 5Document25 pagesBac03-Chapter 5Rea Mariz JordanNo ratings yet

- Vat Training ModuleDocument59 pagesVat Training Modulebandajobanda100% (3)

- Chapt-13 Income Taxes - Partnerships, Estates & TrustsDocument11 pagesChapt-13 Income Taxes - Partnerships, Estates & Trustshumnarvios100% (6)

- Fast FormulasDocument185 pagesFast FormulasMurali KrishnaNo ratings yet

- Value Added Tax ActDocument18 pagesValue Added Tax ActStephen Amobi OkoronkwoNo ratings yet

- VAT Taxpayer Guide (Input Tax)Document54 pagesVAT Taxpayer Guide (Input Tax)NstrNo ratings yet

- Sample Assessment Questions: Formative Activity: / Summative AssessmentDocument15 pagesSample Assessment Questions: Formative Activity: / Summative AssessmentEli_Hux50% (2)

- IAS 12 TaxationDocument30 pagesIAS 12 Taxationwakemeup143No ratings yet

- VAT Basics - July 2023Document8 pagesVAT Basics - July 2023maharajabby81No ratings yet

- VAT Guide 2023Document46 pagesVAT Guide 2023ELIJAHNo ratings yet

- VAT 404 - Guide For Vendors - External GuideDocument110 pagesVAT 404 - Guide For Vendors - External Guidesimphiwe8043No ratings yet

- VAT Guide For VendorsDocument106 pagesVAT Guide For VendorsUrvashi KhedooNo ratings yet

- 7179226899VAT Deduction at Sources 2015-2016Document16 pages7179226899VAT Deduction at Sources 2015-2016Saiful IslamNo ratings yet

- HANDOUT FOR VAT-NewDocument25 pagesHANDOUT FOR VAT-NewCristian RenatusNo ratings yet

- Vat 1Document77 pagesVat 1Shajid HassanNo ratings yet

- VAT ERROR Madurai 19092015 Session VDocument40 pagesVAT ERROR Madurai 19092015 Session VsolomonNo ratings yet

- Cenvat - Overview: V S DateyDocument33 pagesCenvat - Overview: V S Dateygsanjay84No ratings yet

- A Overview of Maharashtra Value Added Tax: IndexDocument10 pagesA Overview of Maharashtra Value Added Tax: IndexAdnan ParkarNo ratings yet

- VAT Taxpayer Guide - VAT Return FilingDocument16 pagesVAT Taxpayer Guide - VAT Return FilingNeeyum Njaanum0021No ratings yet

- (H) VISem BCH6.2 GST Week3 AnkitaTomarDocument23 pages(H) VISem BCH6.2 GST Week3 AnkitaTomarRAJBIR SINGH TADANo ratings yet

- Day 1 - Training MaterialsDocument12 pagesDay 1 - Training MaterialsFarjana AkterNo ratings yet

- Level 2 2010 MAY Vat Study Pack (2011)Document66 pagesLevel 2 2010 MAY Vat Study Pack (2011)Tawanda Tatenda HerbertNo ratings yet

- "VAT, VAT Audit and Statutory Role of Cost Accountant": Name - Richard D'silva Roll No - 09Document12 pages"VAT, VAT Audit and Statutory Role of Cost Accountant": Name - Richard D'silva Roll No - 09Richard DsilvaNo ratings yet

- Module ObjectivesDocument9 pagesModule ObjectivesKyrzen NovillaNo ratings yet

- Royal Malaysian Customs: Guide Approved Toll Manufacturer SchemeDocument15 pagesRoyal Malaysian Customs: Guide Approved Toll Manufacturer SchemetenglumlowNo ratings yet

- Basic Features of Value Added Tax (VAT) For ItesDocument24 pagesBasic Features of Value Added Tax (VAT) For ItesDebashishDolonNo ratings yet

- VAT GuideZRADocument56 pagesVAT GuideZRADaniel Glen-WilliamsonNo ratings yet

- VAT Questions For Professional Stage Knowledge LevelDocument14 pagesVAT Questions For Professional Stage Knowledge LevelFahimaAkterNo ratings yet

- Input Tax Credit (GST)Document16 pagesInput Tax Credit (GST)ravi.pansuriya07No ratings yet

- PWC Newsletter - Value Added Tax Regulations, 2015 - Updated VersionDocument5 pagesPWC Newsletter - Value Added Tax Regulations, 2015 - Updated VersionAnonymous FnM14a0No ratings yet

- Value Added Tax - VatDocument37 pagesValue Added Tax - VatTimoth MbwiloNo ratings yet

- Input Tax Apportionment Guide EN - 31 12 2019Document25 pagesInput Tax Apportionment Guide EN - 31 12 2019Fazlihaq DurraniNo ratings yet

- Tybcom Tax Theory Sem 6Document4 pagesTybcom Tax Theory Sem 6y.zadaneNo ratings yet

- LU1 - Value-Added TaxDocument24 pagesLU1 - Value-Added Taxmandisanomzamo72No ratings yet

- Tax Guide Test 2Document15 pagesTax Guide Test 2Luyanda MhlongoNo ratings yet

- Chapter 3. CITDocument57 pagesChapter 3. CITKhuất Thanh HuếNo ratings yet

- VAT DiscussionDocument5 pagesVAT DiscussionArcide Rcd ReynilNo ratings yet

- Chapter 5 Levy and Collection of GSTDocument59 pagesChapter 5 Levy and Collection of GSTMitanshi KhannaNo ratings yet

- Value Added Tax (Vat)Document40 pagesValue Added Tax (Vat)Phuong TrangNo ratings yet

- India Localization With Respect To INDIA: Modus Operandi Session IDocument31 pagesIndia Localization With Respect To INDIA: Modus Operandi Session IpsroyalNo ratings yet

- What Are The Restrictions in Claiming Input VAT Adjustment Against Output VAT? (D-16)Document10 pagesWhat Are The Restrictions in Claiming Input VAT Adjustment Against Output VAT? (D-16)Javed AhmedNo ratings yet

- Cin Kss SessionDocument71 pagesCin Kss SessionAjay DayalNo ratings yet

- Sales Tax PesentationDocument19 pagesSales Tax PesentationMukund MungalparaNo ratings yet

- VAT Guide 2021Document56 pagesVAT Guide 2021C ChamaNo ratings yet

- Service TaxDocument10 pagesService TaxMonika GuptaNo ratings yet

- 11-Sales TaxDocument20 pages11-Sales Taxabdulsammad13690No ratings yet

- SlideshowDocument37 pagesSlideshowBhavesh AgrawalNo ratings yet

- Value Added TaxDocument11 pagesValue Added TaxPreethi RajasekaranNo ratings yet

- Duties and Taxes For Govt Purchase ProposalsDocument45 pagesDuties and Taxes For Govt Purchase Proposalsdate_milindNo ratings yet

- Value Added Tax (Vat) : Page 1 of 12Document12 pagesValue Added Tax (Vat) : Page 1 of 12regnaldwilliam97No ratings yet

- Supllimentary Duty, Submission of Vat ReturnDocument51 pagesSupllimentary Duty, Submission of Vat ReturnKhadeeza ShammeeNo ratings yet

- VDS Guideline and VAT Rate For The FY 2020-2021 in Comparison With The FY 2019-2020Document9 pagesVDS Guideline and VAT Rate For The FY 2020-2021 in Comparison With The FY 2019-2020Masum GaziNo ratings yet

- Intermediate Examination: Suggested Answers To QuestionsDocument13 pagesIntermediate Examination: Suggested Answers To Questionsnarendra225No ratings yet

- Input Vat: Prepared By: Mrs. Nelia I. Tomas, CPA, LPTDocument28 pagesInput Vat: Prepared By: Mrs. Nelia I. Tomas, CPA, LPTAjey MendiolaNo ratings yet

- VATGuide2014 PDFDocument22 pagesVATGuide2014 PDFAkash TeeluckNo ratings yet

- Lecture VAT With ExercisesDocument82 pagesLecture VAT With ExercisesAko C JamzNo ratings yet

- Sales Tax NotesDocument49 pagesSales Tax NotesMudassar AliNo ratings yet

- 4 Chapter04Document40 pages4 Chapter04Kalkidan ZerihunNo ratings yet

- Remission of Duties & Taxes On Exported Products (Rodtep) SchemeDocument21 pagesRemission of Duties & Taxes On Exported Products (Rodtep) SchemeAnupam BaliNo ratings yet

- Goods and Services Tax (GST) in India: Input Tax Credit (ITC)Document24 pagesGoods and Services Tax (GST) in India: Input Tax Credit (ITC)Noman AreebNo ratings yet

- 1040 Exam Prep Module III: Items Excluded from Gross IncomeFrom Everand1040 Exam Prep Module III: Items Excluded from Gross IncomeRating: 1 out of 5 stars1/5 (1)

- MIAA v. CA (Dela Cruz)Document8 pagesMIAA v. CA (Dela Cruz)Carl IlaganNo ratings yet

- Chapter 1 - General Principles of TaxationDocument4 pagesChapter 1 - General Principles of TaxationCedrickBuenaventuraNo ratings yet

- FABM2 Week 12 13 AsynchDocument8 pagesFABM2 Week 12 13 AsynchKhaira PeraltaNo ratings yet

- Compre 3 Business Law and TaxationDocument10 pagesCompre 3 Business Law and TaxationMary Alyssa Claire Capate IINo ratings yet

- De Minimis BenefitsDocument11 pagesDe Minimis BenefitsJoeban R. PazaNo ratings yet

- City of Iloilo v. Smart Communications, 580 SCRA 332Document1 pageCity of Iloilo v. Smart Communications, 580 SCRA 332nnn aaaNo ratings yet

- ZIMBABWE INCOME TAX ACT Chapter 23 06Document336 pagesZIMBABWE INCOME TAX ACT Chapter 23 06Riana Theron MossNo ratings yet

- MACEDA vs. MACARAIGDocument4 pagesMACEDA vs. MACARAIGMCNo ratings yet

- 2014-15 Douglas County Secured Assessment RollDocument97 pages2014-15 Douglas County Secured Assessment RollcvalleytimesNo ratings yet

- U.S. Income Tax Return For Estates and Trusts: For Calendar Year 2018 or Fiscal Year Beginning, 2018, and Ending, 20Document2 pagesU.S. Income Tax Return For Estates and Trusts: For Calendar Year 2018 or Fiscal Year Beginning, 2018, and Ending, 20Lauren100% (2)

- Income Tax MCQ PDFDocument26 pagesIncome Tax MCQ PDFArpita DagliaNo ratings yet

- TAXATION - General Principles QuizDocument8 pagesTAXATION - General Principles Quizalcazar rtuNo ratings yet

- Form 16 - FY 20 - 21 - FY 2020 - 2021Document9 pagesForm 16 - FY 20 - 21 - FY 2020 - 2021Amit GautamNo ratings yet

- SEC. 98. Imposition of TaxDocument15 pagesSEC. 98. Imposition of TaxAybern BawtistaNo ratings yet

- RMC No 67-2012Document5 pagesRMC No 67-2012evilminionsattackNo ratings yet

- S8 - Taxation LawsDocument101 pagesS8 - Taxation Lawsaman.saini20No ratings yet

- Tax Midterm CompiledDocument49 pagesTax Midterm CompiledMikMik UyNo ratings yet

- NPC Vs City of CabanatuanDocument2 pagesNPC Vs City of Cabanatuan8111 aaa 1118100% (1)

- Special Economic Zone List in IndiaDocument12 pagesSpecial Economic Zone List in IndiasummernaveenNo ratings yet

- CIR Vs Sinco Education Corporation (1956)Document7 pagesCIR Vs Sinco Education Corporation (1956)Joshua DulceNo ratings yet

- 63.-St. Luke's Medical Center, Inc. v. CIR, G.R No. 195909Document15 pages63.-St. Luke's Medical Center, Inc. v. CIR, G.R No. 195909Christine Rose Bonilla LikiganNo ratings yet

- Taxation PDFDocument59 pagesTaxation PDFElikem Kokoroko100% (1)

- CIT Vs Army Wives Welfare Association Allahabad High CourtDocument8 pagesCIT Vs Army Wives Welfare Association Allahabad High CourtAJEEN KUMARNo ratings yet

- Tax Law Syllabus 2021Document4 pagesTax Law Syllabus 2021Francisco BanguisNo ratings yet

- Real P & TCCDocument9 pagesReal P & TCCCloieRjNo ratings yet

- Reviewer Chapter-3-TAXDocument7 pagesReviewer Chapter-3-TAXCarla January OngNo ratings yet

Download as pdf or txt

You might also like

- Chase 1099int 2013Document2 pagesChase 1099int 2013Srikala Venkatesan100% (1)

- Bac03-Chapter 5Document25 pagesBac03-Chapter 5Rea Mariz JordanNo ratings yet

- Vat Training ModuleDocument59 pagesVat Training Modulebandajobanda100% (3)

- Chapt-13 Income Taxes - Partnerships, Estates & TrustsDocument11 pagesChapt-13 Income Taxes - Partnerships, Estates & Trustshumnarvios100% (6)

- Fast FormulasDocument185 pagesFast FormulasMurali KrishnaNo ratings yet

- Value Added Tax ActDocument18 pagesValue Added Tax ActStephen Amobi OkoronkwoNo ratings yet

- VAT Taxpayer Guide (Input Tax)Document54 pagesVAT Taxpayer Guide (Input Tax)NstrNo ratings yet

- Sample Assessment Questions: Formative Activity: / Summative AssessmentDocument15 pagesSample Assessment Questions: Formative Activity: / Summative AssessmentEli_Hux50% (2)

- IAS 12 TaxationDocument30 pagesIAS 12 Taxationwakemeup143No ratings yet

- VAT Basics - July 2023Document8 pagesVAT Basics - July 2023maharajabby81No ratings yet

- VAT Guide 2023Document46 pagesVAT Guide 2023ELIJAHNo ratings yet

- VAT 404 - Guide For Vendors - External GuideDocument110 pagesVAT 404 - Guide For Vendors - External Guidesimphiwe8043No ratings yet

- VAT Guide For VendorsDocument106 pagesVAT Guide For VendorsUrvashi KhedooNo ratings yet

- 7179226899VAT Deduction at Sources 2015-2016Document16 pages7179226899VAT Deduction at Sources 2015-2016Saiful IslamNo ratings yet

- HANDOUT FOR VAT-NewDocument25 pagesHANDOUT FOR VAT-NewCristian RenatusNo ratings yet

- Vat 1Document77 pagesVat 1Shajid HassanNo ratings yet

- VAT ERROR Madurai 19092015 Session VDocument40 pagesVAT ERROR Madurai 19092015 Session VsolomonNo ratings yet

- Cenvat - Overview: V S DateyDocument33 pagesCenvat - Overview: V S Dateygsanjay84No ratings yet

- A Overview of Maharashtra Value Added Tax: IndexDocument10 pagesA Overview of Maharashtra Value Added Tax: IndexAdnan ParkarNo ratings yet

- VAT Taxpayer Guide - VAT Return FilingDocument16 pagesVAT Taxpayer Guide - VAT Return FilingNeeyum Njaanum0021No ratings yet

- (H) VISem BCH6.2 GST Week3 AnkitaTomarDocument23 pages(H) VISem BCH6.2 GST Week3 AnkitaTomarRAJBIR SINGH TADANo ratings yet

- Day 1 - Training MaterialsDocument12 pagesDay 1 - Training MaterialsFarjana AkterNo ratings yet

- Level 2 2010 MAY Vat Study Pack (2011)Document66 pagesLevel 2 2010 MAY Vat Study Pack (2011)Tawanda Tatenda HerbertNo ratings yet

- "VAT, VAT Audit and Statutory Role of Cost Accountant": Name - Richard D'silva Roll No - 09Document12 pages"VAT, VAT Audit and Statutory Role of Cost Accountant": Name - Richard D'silva Roll No - 09Richard DsilvaNo ratings yet

- Module ObjectivesDocument9 pagesModule ObjectivesKyrzen NovillaNo ratings yet

- Royal Malaysian Customs: Guide Approved Toll Manufacturer SchemeDocument15 pagesRoyal Malaysian Customs: Guide Approved Toll Manufacturer SchemetenglumlowNo ratings yet

- Basic Features of Value Added Tax (VAT) For ItesDocument24 pagesBasic Features of Value Added Tax (VAT) For ItesDebashishDolonNo ratings yet

- VAT GuideZRADocument56 pagesVAT GuideZRADaniel Glen-WilliamsonNo ratings yet

- VAT Questions For Professional Stage Knowledge LevelDocument14 pagesVAT Questions For Professional Stage Knowledge LevelFahimaAkterNo ratings yet

- Input Tax Credit (GST)Document16 pagesInput Tax Credit (GST)ravi.pansuriya07No ratings yet

- PWC Newsletter - Value Added Tax Regulations, 2015 - Updated VersionDocument5 pagesPWC Newsletter - Value Added Tax Regulations, 2015 - Updated VersionAnonymous FnM14a0No ratings yet

- Value Added Tax - VatDocument37 pagesValue Added Tax - VatTimoth MbwiloNo ratings yet

- Input Tax Apportionment Guide EN - 31 12 2019Document25 pagesInput Tax Apportionment Guide EN - 31 12 2019Fazlihaq DurraniNo ratings yet

- Tybcom Tax Theory Sem 6Document4 pagesTybcom Tax Theory Sem 6y.zadaneNo ratings yet

- LU1 - Value-Added TaxDocument24 pagesLU1 - Value-Added Taxmandisanomzamo72No ratings yet

- Tax Guide Test 2Document15 pagesTax Guide Test 2Luyanda MhlongoNo ratings yet

- Chapter 3. CITDocument57 pagesChapter 3. CITKhuất Thanh HuếNo ratings yet

- VAT DiscussionDocument5 pagesVAT DiscussionArcide Rcd ReynilNo ratings yet

- Chapter 5 Levy and Collection of GSTDocument59 pagesChapter 5 Levy and Collection of GSTMitanshi KhannaNo ratings yet

- Value Added Tax (Vat)Document40 pagesValue Added Tax (Vat)Phuong TrangNo ratings yet

- India Localization With Respect To INDIA: Modus Operandi Session IDocument31 pagesIndia Localization With Respect To INDIA: Modus Operandi Session IpsroyalNo ratings yet

- What Are The Restrictions in Claiming Input VAT Adjustment Against Output VAT? (D-16)Document10 pagesWhat Are The Restrictions in Claiming Input VAT Adjustment Against Output VAT? (D-16)Javed AhmedNo ratings yet

- Cin Kss SessionDocument71 pagesCin Kss SessionAjay DayalNo ratings yet

- Sales Tax PesentationDocument19 pagesSales Tax PesentationMukund MungalparaNo ratings yet

- VAT Guide 2021Document56 pagesVAT Guide 2021C ChamaNo ratings yet

- Service TaxDocument10 pagesService TaxMonika GuptaNo ratings yet

- 11-Sales TaxDocument20 pages11-Sales Taxabdulsammad13690No ratings yet

- SlideshowDocument37 pagesSlideshowBhavesh AgrawalNo ratings yet

- Value Added TaxDocument11 pagesValue Added TaxPreethi RajasekaranNo ratings yet

- Duties and Taxes For Govt Purchase ProposalsDocument45 pagesDuties and Taxes For Govt Purchase Proposalsdate_milindNo ratings yet

- Value Added Tax (Vat) : Page 1 of 12Document12 pagesValue Added Tax (Vat) : Page 1 of 12regnaldwilliam97No ratings yet

- Supllimentary Duty, Submission of Vat ReturnDocument51 pagesSupllimentary Duty, Submission of Vat ReturnKhadeeza ShammeeNo ratings yet

- VDS Guideline and VAT Rate For The FY 2020-2021 in Comparison With The FY 2019-2020Document9 pagesVDS Guideline and VAT Rate For The FY 2020-2021 in Comparison With The FY 2019-2020Masum GaziNo ratings yet

- Intermediate Examination: Suggested Answers To QuestionsDocument13 pagesIntermediate Examination: Suggested Answers To Questionsnarendra225No ratings yet

- Input Vat: Prepared By: Mrs. Nelia I. Tomas, CPA, LPTDocument28 pagesInput Vat: Prepared By: Mrs. Nelia I. Tomas, CPA, LPTAjey MendiolaNo ratings yet

- VATGuide2014 PDFDocument22 pagesVATGuide2014 PDFAkash TeeluckNo ratings yet

- Lecture VAT With ExercisesDocument82 pagesLecture VAT With ExercisesAko C JamzNo ratings yet

- Sales Tax NotesDocument49 pagesSales Tax NotesMudassar AliNo ratings yet

- 4 Chapter04Document40 pages4 Chapter04Kalkidan ZerihunNo ratings yet

- Remission of Duties & Taxes On Exported Products (Rodtep) SchemeDocument21 pagesRemission of Duties & Taxes On Exported Products (Rodtep) SchemeAnupam BaliNo ratings yet

- Goods and Services Tax (GST) in India: Input Tax Credit (ITC)Document24 pagesGoods and Services Tax (GST) in India: Input Tax Credit (ITC)Noman AreebNo ratings yet

- 1040 Exam Prep Module III: Items Excluded from Gross IncomeFrom Everand1040 Exam Prep Module III: Items Excluded from Gross IncomeRating: 1 out of 5 stars1/5 (1)

- MIAA v. CA (Dela Cruz)Document8 pagesMIAA v. CA (Dela Cruz)Carl IlaganNo ratings yet

- Chapter 1 - General Principles of TaxationDocument4 pagesChapter 1 - General Principles of TaxationCedrickBuenaventuraNo ratings yet

- FABM2 Week 12 13 AsynchDocument8 pagesFABM2 Week 12 13 AsynchKhaira PeraltaNo ratings yet

- Compre 3 Business Law and TaxationDocument10 pagesCompre 3 Business Law and TaxationMary Alyssa Claire Capate IINo ratings yet

- De Minimis BenefitsDocument11 pagesDe Minimis BenefitsJoeban R. PazaNo ratings yet

- City of Iloilo v. Smart Communications, 580 SCRA 332Document1 pageCity of Iloilo v. Smart Communications, 580 SCRA 332nnn aaaNo ratings yet

- ZIMBABWE INCOME TAX ACT Chapter 23 06Document336 pagesZIMBABWE INCOME TAX ACT Chapter 23 06Riana Theron MossNo ratings yet

- MACEDA vs. MACARAIGDocument4 pagesMACEDA vs. MACARAIGMCNo ratings yet

- 2014-15 Douglas County Secured Assessment RollDocument97 pages2014-15 Douglas County Secured Assessment RollcvalleytimesNo ratings yet

- U.S. Income Tax Return For Estates and Trusts: For Calendar Year 2018 or Fiscal Year Beginning, 2018, and Ending, 20Document2 pagesU.S. Income Tax Return For Estates and Trusts: For Calendar Year 2018 or Fiscal Year Beginning, 2018, and Ending, 20Lauren100% (2)

- Income Tax MCQ PDFDocument26 pagesIncome Tax MCQ PDFArpita DagliaNo ratings yet

- TAXATION - General Principles QuizDocument8 pagesTAXATION - General Principles Quizalcazar rtuNo ratings yet

- Form 16 - FY 20 - 21 - FY 2020 - 2021Document9 pagesForm 16 - FY 20 - 21 - FY 2020 - 2021Amit GautamNo ratings yet

- SEC. 98. Imposition of TaxDocument15 pagesSEC. 98. Imposition of TaxAybern BawtistaNo ratings yet

- RMC No 67-2012Document5 pagesRMC No 67-2012evilminionsattackNo ratings yet

- S8 - Taxation LawsDocument101 pagesS8 - Taxation Lawsaman.saini20No ratings yet

- Tax Midterm CompiledDocument49 pagesTax Midterm CompiledMikMik UyNo ratings yet

- NPC Vs City of CabanatuanDocument2 pagesNPC Vs City of Cabanatuan8111 aaa 1118100% (1)

- Special Economic Zone List in IndiaDocument12 pagesSpecial Economic Zone List in IndiasummernaveenNo ratings yet

- CIR Vs Sinco Education Corporation (1956)Document7 pagesCIR Vs Sinco Education Corporation (1956)Joshua DulceNo ratings yet

- 63.-St. Luke's Medical Center, Inc. v. CIR, G.R No. 195909Document15 pages63.-St. Luke's Medical Center, Inc. v. CIR, G.R No. 195909Christine Rose Bonilla LikiganNo ratings yet

- Taxation PDFDocument59 pagesTaxation PDFElikem Kokoroko100% (1)

- CIT Vs Army Wives Welfare Association Allahabad High CourtDocument8 pagesCIT Vs Army Wives Welfare Association Allahabad High CourtAJEEN KUMARNo ratings yet

- Tax Law Syllabus 2021Document4 pagesTax Law Syllabus 2021Francisco BanguisNo ratings yet

- Real P & TCCDocument9 pagesReal P & TCCCloieRjNo ratings yet

- Reviewer Chapter-3-TAXDocument7 pagesReviewer Chapter-3-TAXCarla January OngNo ratings yet