Download as pdf or txt

You might also like

- Summary Of "The Age Of Empire (1875-1914)" By Eric Hobsbawm: UNIVERSITY SUMMARIESFrom EverandSummary Of "The Age Of Empire (1875-1914)" By Eric Hobsbawm: UNIVERSITY SUMMARIESRating: 1 out of 5 stars1/5 (1)

- Essentials of Economics 3rd Edition Krugman Solutions ManualDocument25 pagesEssentials of Economics 3rd Edition Krugman Solutions ManualAlexanderBoyerwoit100% (54)

- Pre-Filling Report 2017: Taxpayer DetailsDocument2 pagesPre-Filling Report 2017: Taxpayer DetailsUsama AshfaqNo ratings yet

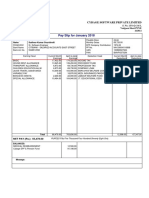

- Pay Slip For January 2018: Cybage Software Private LimitedDocument1 pagePay Slip For January 2018: Cybage Software Private LimitedSudheer0% (1)

- Completo ResumenDocument22 pagesCompleto Resumenamparooo20No ratings yet

- U.1Economic HistoryDocument5 pagesU.1Economic HistoryJoseNo ratings yet

- British Economy and SocialDocument7 pagesBritish Economy and SocialAlwi YoniNo ratings yet

- Baten and Ruben NotesDocument17 pagesBaten and Ruben NoteszeushathawayNo ratings yet

- The Making of A Global World: I) The Pre-Modern World # Silk Routes Link The WorldDocument5 pagesThe Making of A Global World: I) The Pre-Modern World # Silk Routes Link The Worldalok nayakNo ratings yet

- The Great Divergence Debate 28-11Document3 pagesThe Great Divergence Debate 28-11luciagabriela.theoktisto01No ratings yet

- Labor and GlobalizationDocument21 pagesLabor and GlobalizationScott Abel100% (1)

- The Atlantic World Slave Economy and The Development Process in EnglandDocument12 pagesThe Atlantic World Slave Economy and The Development Process in EnglandRachel RoseNo ratings yet

- Text 1 A Historical Perspective On GlobalizationDocument12 pagesText 1 A Historical Perspective On GlobalizationMihaela BudulanNo ratings yet

- Economic History - 1 February 13th, 2020Document54 pagesEconomic History - 1 February 13th, 2020GediminasNo ratings yet

- SST Class 10th ProjectDocument11 pagesSST Class 10th Projectnishitasingh.dhandhuNo ratings yet

- Economics NotesDocument11 pagesEconomics Notesgigasmartina8No ratings yet

- Apuntes HistoriaDocument19 pagesApuntes Historiaamparooo20No ratings yet

- ST TH TH THDocument3 pagesST TH TH THorchuchiNo ratings yet

- Globalization Timeline (Data Gathering Notes)Document9 pagesGlobalization Timeline (Data Gathering Notes)18105231No ratings yet

- Socail PreseDocument12 pagesSocail Presegbenga.sylvan.qatarNo ratings yet

- Globalization: Massachusetts Institute of TechnologyDocument14 pagesGlobalization: Massachusetts Institute of TechnologyHa LinhNo ratings yet

- Linea Del Tiempo Del Comercio Internacional Sandra MartinezDocument9 pagesLinea Del Tiempo Del Comercio Internacional Sandra MartinezSandra MartinezNo ratings yet

- Industrialization and Economic DevelopmentDocument24 pagesIndustrialization and Economic DevelopmentJenishNo ratings yet

- UK Economy Since Early YearsDocument11 pagesUK Economy Since Early YearsAlexia GabrielaNo ratings yet

- Study Guide 1Document4 pagesStudy Guide 1danaNo ratings yet

- EC2096 L4 Economic History C3Document95 pagesEC2096 L4 Economic History C3Jimmy ZhengNo ratings yet

- Making of Global WorldDocument20 pagesMaking of Global WorldANUGRAH SMIJESH THIRUMANGALATHNo ratings yet

- World Growth Since 1800: Presented by Anam Sohail Rubail ShahidDocument23 pagesWorld Growth Since 1800: Presented by Anam Sohail Rubail Shahidrubailshahid41No ratings yet

- Global Markets and Geopolitics ClassDocument50 pagesGlobal Markets and Geopolitics ClassHimanshu BohraNo ratings yet

- Lesson 2: The Global Economy and Market Integration: Learning OutcomesDocument11 pagesLesson 2: The Global Economy and Market Integration: Learning OutcomesMARK 2020No ratings yet

- The 19TH Century 19 20Document3 pagesThe 19TH Century 19 20Belén OroNo ratings yet

- Globalization in 21st CenturyDocument15 pagesGlobalization in 21st CenturyInciaNo ratings yet

- Globalization: Vasudhaiva Kutumbakam - The World Is A FamilyDocument17 pagesGlobalization: Vasudhaiva Kutumbakam - The World Is A FamilyTusharNo ratings yet

- Asias Great MigrationsDocument17 pagesAsias Great Migrationssaran ravipatiNo ratings yet

- American Rev IndusDocument30 pagesAmerican Rev IndusKevin CharlesNo ratings yet

- University of Karachi: Department of History (Industrial Revolution) (1760-1850)Document11 pagesUniversity of Karachi: Department of History (Industrial Revolution) (1760-1850)Syed Mohsin Mehdi TaqviNo ratings yet

- The Industrial RevolutionDocument35 pagesThe Industrial RevolutionSmaranda LeordaNo ratings yet

- Origin and History of GlobalizationDocument5 pagesOrigin and History of GlobalizationGerald Jaboyanon MondragonNo ratings yet

- Summary of When Did Globalization Begin?'Document8 pagesSummary of When Did Globalization Begin?'smrithiNo ratings yet

- The Industrial RevolutionDocument14 pagesThe Industrial RevolutionManel MamitooNo ratings yet

- The Making of A Global World - Short Notes - by @PWD - BKUPDocument5 pagesThe Making of A Global World - Short Notes - by @PWD - BKUPLokesh YadavNo ratings yet

- Distances Getting Shorter, Things Moving Closer. It Pertains To The Increasing Case With WhichDocument52 pagesDistances Getting Shorter, Things Moving Closer. It Pertains To The Increasing Case With WhichReema JoshiNo ratings yet

- History of EuropeDocument3 pagesHistory of EuropeEesha Abdul KhaliqNo ratings yet

- GE 3 L2 Origins and History of GlobalizationDocument6 pagesGE 3 L2 Origins and History of GlobalizationBlescel AntongNo ratings yet

- The BackgroundDocument5 pagesThe BackgroundAashish ChhabraNo ratings yet

- Mercantilism Mercantilist Use On International TheoryDocument9 pagesMercantilism Mercantilist Use On International TheoryUdhaya KumarNo ratings yet

- A Brief History of GlobalizationDocument9 pagesA Brief History of GlobalizationLaa BelaNo ratings yet

- Word Events 1800-1900Document2 pagesWord Events 1800-1900nehapanditayinNo ratings yet

- World Economy HistoryDocument6 pagesWorld Economy HistoryMark Tolentino GomezNo ratings yet

- Mercantilism: Mercantilism Is An Economic Policy That Is Designed ToDocument14 pagesMercantilism: Mercantilism Is An Economic Policy That Is Designed ToPat ONo ratings yet

- Wolf 0405Document13 pagesWolf 0405Joe JosephNo ratings yet

- The Industrial RevolutionDocument4 pagesThe Industrial Revolutionvats ujjwalNo ratings yet

- A Brief History of GlobalizationDocument25 pagesA Brief History of GlobalizationZiennard GeronaNo ratings yet

- GlobalizationDocument4 pagesGlobalizationAndrelina Sheila Mae GoNo ratings yet

- The Making of A Global World: World Trade Pre-Modern To 18 CenturyDocument4 pagesThe Making of A Global World: World Trade Pre-Modern To 18 CenturyRounak Basu0% (1)

- IEPH 2024-25 Lecture notes on Great Divergence and Reversal of FortuneDocument5 pagesIEPH 2024-25 Lecture notes on Great Divergence and Reversal of FortuneishikaNo ratings yet

- Ancient Silk Roads Image: FlickrDocument8 pagesAncient Silk Roads Image: FlickrEntertainment Happenings PHNo ratings yet

- Lecturas Historia - Gulag - FreeDocument37 pagesLecturas Historia - Gulag - FreeLuis Fernández ChacónNo ratings yet

- World & Indian History (Prelim & Mains)Document191 pagesWorld & Indian History (Prelim & Mains)Gurmeet100% (1)

- INDUSTRIAL REVOLUTION and FRENCH REVOLUTIONDocument4 pagesINDUSTRIAL REVOLUTION and FRENCH REVOLUTIONMuhammad HasnatNo ratings yet

- The Globalization of World EconomicsDocument32 pagesThe Globalization of World EconomicsDencio PrimaveraNo ratings yet

- CH 3 HistoryDocument9 pagesCH 3 HistoryirfaanffgamingNo ratings yet

- Econ His Notes - 2nd PartialDocument35 pagesEcon His Notes - 2nd PartialAlexis BabakoffNo ratings yet

- Eeb SummaryDocument7 pagesEeb SummaryRohan KabraNo ratings yet

- Monthly Report On Potato For May, 2020Document9 pagesMonthly Report On Potato For May, 2020souravroy.sr5989No ratings yet

- CH 8 International TradeDocument8 pagesCH 8 International TradeAlfian NugrahaNo ratings yet

- PT. Duta Makmur MulyaDocument1 pagePT. Duta Makmur Mulyaduta teknikNo ratings yet

- Patterns and Trends in International TradeDocument16 pagesPatterns and Trends in International TradeManisha SahuNo ratings yet

- DixonDocument2 pagesDixonSajib Dev100% (1)

- The International Monetary SystemDocument51 pagesThe International Monetary Systemtinashe chavundukatNo ratings yet

- Bafm U Vkwa Y Dkwikszjs'Ku Fyfevsm Bafm U Vkwa Y Dkwikszjs'Ku Fyfevsm Bafm U Vkwa Y Dkwikszjs'Ku Fyfevsm Bafm U Vkwa Y Dkwikszjs'Ku FyfevsmDocument1 pageBafm U Vkwa Y Dkwikszjs'Ku Fyfevsm Bafm U Vkwa Y Dkwikszjs'Ku Fyfevsm Bafm U Vkwa Y Dkwikszjs'Ku Fyfevsm Bafm U Vkwa Y Dkwikszjs'Ku FyfevsmAman ThakurNo ratings yet

- Unit 1 PPT 1Document35 pagesUnit 1 PPT 1Shristi SinhaNo ratings yet

- Fin Mar-Chapter9Document2 pagesFin Mar-Chapter9EANNA15No ratings yet

- The Rajahmundry Campus of University of Petroleum & Energy StudiesDocument1 pageThe Rajahmundry Campus of University of Petroleum & Energy StudiesUniversity Of Petroleum And Energy StudiesNo ratings yet

- Monetary Policy Review No.7 2022Document7 pagesMonetary Policy Review No.7 2022Adaderana OnlineNo ratings yet

- Valley View UniversityDocument4 pagesValley View Universitymartin pulpitNo ratings yet

- Vijayawada Municipal Corporation: OriginalDocument4 pagesVijayawada Municipal Corporation: Originallakshmiteja105_18319No ratings yet

- Differences Between The United Kingdom and The PhilippinesDocument10 pagesDifferences Between The United Kingdom and The PhilippinesStingray_jar75% (4)

- Soal InternationalDocument7 pagesSoal InternationalEvendy SetiawanNo ratings yet

- Russia - The End of A Time of Troubles - 1Document2 pagesRussia - The End of A Time of Troubles - 1Vijay Krishnan AnantharamanNo ratings yet

- Payslip For The Month of July-2020: Earnings Amount Deductions AmountDocument1 pagePayslip For The Month of July-2020: Earnings Amount Deductions AmountVikas GuptaNo ratings yet

- CAS Report SitharaDocument7 pagesCAS Report SitharaNAVYA PNo ratings yet

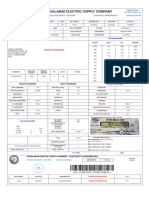

- Fesco Online Bill January 2Document1 pageFesco Online Bill January 2HaseebPirachaNo ratings yet

- Sources of Finance: Name: Mahfooz Alam Shaikh Class: TYBBA Roll No: F39 Subject: Financial ManagementDocument6 pagesSources of Finance: Name: Mahfooz Alam Shaikh Class: TYBBA Roll No: F39 Subject: Financial ManagementMahfooz Alam ShaikhNo ratings yet

- FOREXDocument24 pagesFOREXPrasenjit Chakraborty0% (1)

- Price Action TradingDocument1 pagePrice Action TradingmarketapprenticeNo ratings yet

- Ethiopia Import Sample ReportDocument5 pagesEthiopia Import Sample ReportYimer AliNo ratings yet

- Vote of Thanks - TampletsDocument1 pageVote of Thanks - TampletsarunloveNo ratings yet

- Chapter 7 Practice Questions - MacroDocument2 pagesChapter 7 Practice Questions - MacroAndrew HuangNo ratings yet

- Apex Banks of 20 CountriesDocument12 pagesApex Banks of 20 Countrieskarthik0407No ratings yet