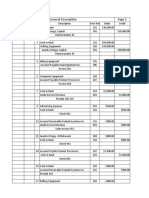

Week13 Seminar Assignment - F23xlsx

Week13 Seminar Assignment - F23xlsx

You might also like

- Manduleli Victor Bikitsha Nsualwhk ArchivedDocument10 pagesManduleli Victor Bikitsha Nsualwhk ArchivedManduleli BikitshaNo ratings yet

- Tugas Pengantar Akuntansi-1Document23 pagesTugas Pengantar Akuntansi-1Wiedya fitrianaNo ratings yet

- Gold Business Account 82Document1 pageGold Business Account 82nicole.philippsNo ratings yet

- Sample Small Law Firm Chart of AccountsDocument3 pagesSample Small Law Firm Chart of AccountsYasmin ZainuzzamanNo ratings yet

- This Study Resource Was: Problem 1Document5 pagesThis Study Resource Was: Problem 1xicoyiNo ratings yet

- Ais Draft TaskDocument21 pagesAis Draft TaskHazel DimaanoNo ratings yet

- Bookkeeping FinalExam - Answers2022 - GG1712Document8 pagesBookkeeping FinalExam - Answers2022 - GG1712Karan KhannaNo ratings yet

- 27 Mar 2020 - (Free) ..Chqmwuilbna - Fawfawn - Ehqjeqx - B31yax1ycmcgaadwdnf3ag8jbnjyc3eiaakgcnj1cw8idgf7dxvycqDocument2 pages27 Mar 2020 - (Free) ..Chqmwuilbna - Fawfawn - Ehqjeqx - B31yax1ycmcgaadwdnf3ag8jbnjyc3eiaakgcnj1cw8idgf7dxvycqkhuthadzoNo ratings yet

- Exercise 7-9 Credit Card and Debit Card Transactions LO5Document2 pagesExercise 7-9 Credit Card and Debit Card Transactions LO5Jehiel Mathew100% (1)

- Rie March2018Document1 pageRie March2018Zairo MosesNo ratings yet

- Demo Problem #1 Bank Rec Solution (White)Document2 pagesDemo Problem #1 Bank Rec Solution (White)Anu kahtterNo ratings yet

- Accounting Cycle ReviewerDocument20 pagesAccounting Cycle ReviewerKriezl Labay CalditoNo ratings yet

- Cash Additional ProblemsDocument2 pagesCash Additional ProblemsRed TigerNo ratings yet

- Tugas 3 (Revisi) - Proses Posting-Ricky Andrian K. RumereDocument23 pagesTugas 3 (Revisi) - Proses Posting-Ricky Andrian K. RumererickyNo ratings yet

- Cash On Hand Cash in BankDocument2 pagesCash On Hand Cash in BankCristina Melloria100% (1)

- Exercise 7.1: S.O. Heater Installations: Bank Reconciliation Statement As at 31 July 2015Document12 pagesExercise 7.1: S.O. Heater Installations: Bank Reconciliation Statement As at 31 July 2015Doan Chan PhongNo ratings yet

- AFA241Document5 pagesAFA241sarah josephNo ratings yet

- Accounting ExercisesDocument41 pagesAccounting ExercisesKayla MirandaNo ratings yet

- Nissan Renault Financial Services India Private Limited: Loan Account Statement For DBAN136091Document4 pagesNissan Renault Financial Services India Private Limited: Loan Account Statement For DBAN136091shashiNo ratings yet

- Topic 7: Cash Management and Control, Preparation Bank Reconciliations and Maintaining A Petty Cash System Solutions To Tutorial QuestionsDocument3 pagesTopic 7: Cash Management and Control, Preparation Bank Reconciliations and Maintaining A Petty Cash System Solutions To Tutorial QuestionsMitchell BylartNo ratings yet

- Accn June Memo 2015Document18 pagesAccn June Memo 2015Abrar DhoratNo ratings yet

- 18 Apr 2020 - (Free) ..cg11NTQKdgU - FXpwFhZhdQVyA3wCGXwCdhwEBxp-CHEOcw0DfBkIdgdzBQR1dgh2B3MDBn11DnECcgwHcQDocument1 page18 Apr 2020 - (Free) ..cg11NTQKdgU - FXpwFhZhdQVyA3wCGXwCdhwEBxp-CHEOcw0DfBkIdgdzBQR1dgh2B3MDBn11DnECcgwHcQLovemore Mutyambizi MuchenjeNo ratings yet

- Manduleli Victor Bikitsha Nsualwjh ArchivedDocument10 pagesManduleli Victor Bikitsha Nsualwjh ArchivedManduleli BikitshaNo ratings yet

- Acc Chapter 09Document39 pagesAcc Chapter 09Nicholas J W LeeNo ratings yet

- Further Information: Schedule of Accounts Receivable MayDocument6 pagesFurther Information: Schedule of Accounts Receivable MaySaifullah WaqarNo ratings yet

- BTVN Chapter 6 New 1Document21 pagesBTVN Chapter 6 New 1hangptt214051No ratings yet

- 2018 April Resource Booklet L2Document8 pages2018 April Resource Booklet L2Ronald YeeNo ratings yet

- Acc 2018 MemoDocument12 pagesAcc 2018 Memokyle.govender2004No ratings yet

- Unit 2. Audit of Cash and Cash Transactions - Handout - T21920 (Final)Document6 pagesUnit 2. Audit of Cash and Cash Transactions - Handout - T21920 (Final)Alyna JNo ratings yet

- San Andres Branch SOA 02-17-24 Bill DateDocument4 pagesSan Andres Branch SOA 02-17-24 Bill DateAnonymous gV9BmXXHNo ratings yet

- Business Supersave 36Document1 pageBusiness Supersave 36majodinaabegailNo ratings yet

- SWAZI+ONE Accounting ExerciseDocument2 pagesSWAZI+ONE Accounting Exercisekj98mcqc5zNo ratings yet

- Omaha Bank Statement (Card)Document3 pagesOmaha Bank Statement (Card)ВасилийNo ratings yet

- Nama: Melvina Puhut Siregar Nim: 1932150049 E7-23 (Petty Cash) Mcmann, Inc. Decided To Establish A Petty Cash Fund To Help Ensure InternalDocument6 pagesNama: Melvina Puhut Siregar Nim: 1932150049 E7-23 (Petty Cash) Mcmann, Inc. Decided To Establish A Petty Cash Fund To Help Ensure Internalmelvina siregarNo ratings yet

- GR11 Accounting Practice Exam November Paper 1 PDFDocument7 pagesGR11 Accounting Practice Exam November Paper 1 PDFGood LifeNo ratings yet

- San Andres Branch SOA 01-12-24Document4 pagesSan Andres Branch SOA 01-12-24Anonymous gV9BmXXHNo ratings yet

- Bank Reconciliation NotesDocument25 pagesBank Reconciliation NotesJohn Sue HanNo ratings yet

- TRƯƠNG THỊ QUỲNH NHƯ - ESSAY TEST - - ACC101 - IB17CDocument15 pagesTRƯƠNG THỊ QUỲNH NHƯ - ESSAY TEST - - ACC101 - IB17CTrương Thị Quỳnh NhưNo ratings yet

- General DescriptionDocument7 pagesGeneral Description11A Ol MonorothNo ratings yet

- College Accounting 12th Edition Slater Solutions Manual DownloadDocument35 pagesCollege Accounting 12th Edition Slater Solutions Manual DownloadRicardo Rivera100% (27)

- Perilla Geriqjoedn 1Document20 pagesPerilla Geriqjoedn 1Geriq Joeden PerillaNo ratings yet

- FA Assignment 5: Ishani Sathish (PGP/25/331)Document7 pagesFA Assignment 5: Ishani Sathish (PGP/25/331)ishaniNo ratings yet

- LawDocument3 pagesLawKhenett Ramirez PuertoNo ratings yet

- WDC202440Document1 pageWDC202440kennethmwangi2024No ratings yet

- Exercise Chap 2 NLKTDocument10 pagesExercise Chap 2 NLKTalexnguyen21007No ratings yet

- Topic No. 1 - Statement of Financial Position PDFDocument4 pagesTopic No. 1 - Statement of Financial Position PDFSARAH ANDREA TORRESNo ratings yet

- V1620034 - Dzaky FarhansyahDocument11 pagesV1620034 - Dzaky FarhansyahDzaky FarhansyahNo ratings yet

- Philippine Politics and Governance DLPDocument6 pagesPhilippine Politics and Governance DLPDMarrie Abao Boniao-LabadanNo ratings yet

- Trade IncDocument2 pagesTrade IncAnne Angelie Gomez SebialNo ratings yet

- 2022-03-10 Item 6aDocument4 pages2022-03-10 Item 6a视频精选全球No ratings yet

- Financial Accounting Assignment - 1Document17 pagesFinancial Accounting Assignment - 1Yosef MitikuNo ratings yet

- 2018-10-27 PDFDocument2 pages2018-10-27 PDFKhathutshelo KharivheNo ratings yet

- C02 Financial Accounting Fundamentals - Control AccountsDocument7 pagesC02 Financial Accounting Fundamentals - Control AccountsAlfred MakonaNo ratings yet

- 2018-10-27 PDFDocument2 pages2018-10-27 PDFKhathutshelo KharivheNo ratings yet

- Quiz Review CH 5 6 7Document8 pagesQuiz Review CH 5 6 7yanto ismailNo ratings yet

- RTM 2 Pa 1Document3 pagesRTM 2 Pa 1Mega UrjuwanNo ratings yet

- Financial Accounting and Reporting 1Document18 pagesFinancial Accounting and Reporting 1cruzdelica18No ratings yet

- Solutions To More SAC 1 Revision 2021Document5 pagesSolutions To More SAC 1 Revision 2021anshsinghsoniNo ratings yet

- BHN Ajar Samone Equipment Repair Inc - PreparationDocument29 pagesBHN Ajar Samone Equipment Repair Inc - PreparationfghhjjjnjjnNo ratings yet

- PL BS of MD ShafikDocument12 pagesPL BS of MD ShafikanupNo ratings yet

- Seminar Activity (10) - Managing Human ResourcesDocument7 pagesSeminar Activity (10) - Managing Human Resourcesbhattfenil29No ratings yet

- Grit Activity Week 1Document2 pagesGrit Activity Week 1bhattfenil29No ratings yet

- Excel Class FileDocument3 pagesExcel Class Filebhattfenil29No ratings yet

- Grit Activity Week 1Document2 pagesGrit Activity Week 1bhattfenil29No ratings yet

- Week12 SeminarAssignmentDocument13 pagesWeek12 SeminarAssignmentbhattfenil29No ratings yet

- Final Group Project - Opportunity AssessmentDocument7 pagesFinal Group Project - Opportunity Assessmentbhattfenil29No ratings yet

- Week10 SeminarAssignmentDocument7 pagesWeek10 SeminarAssignmentbhattfenil29No ratings yet

- Week11 CH5 SeminarAssignmentDocument10 pagesWeek11 CH5 SeminarAssignmentbhattfenil29No ratings yet

- Week9 - SeminarAssign Ch04Prob4 - 3ADocument12 pagesWeek9 - SeminarAssign Ch04Prob4 - 3Abhattfenil29No ratings yet

- AUDIT PROGRAM For Cash Disbursements 2Document5 pagesAUDIT PROGRAM For Cash Disbursements 2jezreel dela mercedNo ratings yet

- VLAN Setup in MikroTik SwitchOS (SwOS)Document3 pagesVLAN Setup in MikroTik SwitchOS (SwOS)Phạm Đức HạnhNo ratings yet

- SME Company NameDocument12 pagesSME Company NamesahildoraNo ratings yet

- Acct Statement XX8038 12102023Document5 pagesAcct Statement XX8038 12102023middeslifesciencesNo ratings yet

- Updated List of Insurance Entities in Good Standing As at November 20, 2020Document5 pagesUpdated List of Insurance Entities in Good Standing As at November 20, 2020Fuaad DodooNo ratings yet

- CyberSecOp Scoping Questionnaire March2023Document3 pagesCyberSecOp Scoping Questionnaire March2023hemanth_jayaraman100% (1)

- LinkageDocument1 pageLinkagerasool mehrjooNo ratings yet

- SBAA7025Document102 pagesSBAA7025Sharuk HussainNo ratings yet

- Upaya Hukum Otoritas Jasa Keuangan Dalam Mengatasi Layanan Pinjaman Online IlegalDocument12 pagesUpaya Hukum Otoritas Jasa Keuangan Dalam Mengatasi Layanan Pinjaman Online IlegalNursyah RazakNo ratings yet

- Futuristic NursingDocument6 pagesFuturistic NursingAnusha Verghese100% (1)

- Statement (CAD) : Corporate StaysDocument2 pagesStatement (CAD) : Corporate Staysvbt1561No ratings yet

- M/s. Valmind IT Needs Private Limited Pay Slip: Gross Pay 12,083 Net Pay 11,333Document5 pagesM/s. Valmind IT Needs Private Limited Pay Slip: Gross Pay 12,083 Net Pay 11,333Tech-savvy GirishaNo ratings yet

- Continuous Quality Improvement (CQI)Document15 pagesContinuous Quality Improvement (CQI)Kayla Suzanne GuanellaNo ratings yet

- Accounts Cec 1year Test PaparDocument2 pagesAccounts Cec 1year Test PaparMohammad MoinuddinNo ratings yet

- Lecture : Day 1: Adjusting Entries & Chart of Accounts (Periodic & Perpetual)Document7 pagesLecture : Day 1: Adjusting Entries & Chart of Accounts (Periodic & Perpetual)khrysna ayra villanuevaNo ratings yet

- Medical Transcription (Medical Records)Document32 pagesMedical Transcription (Medical Records)Rana Abd Almugeeth100% (5)

- BANKINGDocument14 pagesBANKINGpinky NathNo ratings yet

- WVCH Health Plan ContractDocument185 pagesWVCH Health Plan ContractStatesman JournalNo ratings yet

- Signal CommunicationDocument44 pagesSignal CommunicationIan PolancosNo ratings yet

- HZV1P3 Finisar Optics Reference Guide 1Document2 pagesHZV1P3 Finisar Optics Reference Guide 1Diy DoeNo ratings yet

- Last Mile LogisticsDocument7 pagesLast Mile LogisticsBoyce DigitalNo ratings yet

- Punjab State Cooperative BankDocument58 pagesPunjab State Cooperative BankRavneet Singh75% (4)

- Working Backward To Cash Receipts and DisbursementsDocument8 pagesWorking Backward To Cash Receipts and DisbursementsHarsha ThejaNo ratings yet

- Macroeconomic Assignment 1mba059 Ma Pann Myat PhyuDocument2 pagesMacroeconomic Assignment 1mba059 Ma Pann Myat PhyuCWHNo ratings yet

- RS Sharma CV 12032020Document3 pagesRS Sharma CV 12032020Sourav kachhawahaNo ratings yet

- Plkk-F-Hse-50 Daily - Report - Safety OfficerDocument1 pagePlkk-F-Hse-50 Daily - Report - Safety OfficerandriNo ratings yet

- Cash - Management and Fraud PreventionDocument21 pagesCash - Management and Fraud PreventionnathanielNo ratings yet

- Cash Managment (Q)Document7 pagesCash Managment (Q)amna zamanNo ratings yet

- Employee BenefitDocument37 pagesEmployee BenefitNinjo senpaiNo ratings yet

Download as xlsx, pdf, or txt

You might also like

- Manduleli Victor Bikitsha Nsualwhk ArchivedDocument10 pagesManduleli Victor Bikitsha Nsualwhk ArchivedManduleli BikitshaNo ratings yet

- Tugas Pengantar Akuntansi-1Document23 pagesTugas Pengantar Akuntansi-1Wiedya fitrianaNo ratings yet

- Gold Business Account 82Document1 pageGold Business Account 82nicole.philippsNo ratings yet

- Sample Small Law Firm Chart of AccountsDocument3 pagesSample Small Law Firm Chart of AccountsYasmin ZainuzzamanNo ratings yet

- This Study Resource Was: Problem 1Document5 pagesThis Study Resource Was: Problem 1xicoyiNo ratings yet

- Ais Draft TaskDocument21 pagesAis Draft TaskHazel DimaanoNo ratings yet

- Bookkeeping FinalExam - Answers2022 - GG1712Document8 pagesBookkeeping FinalExam - Answers2022 - GG1712Karan KhannaNo ratings yet

- 27 Mar 2020 - (Free) ..Chqmwuilbna - Fawfawn - Ehqjeqx - B31yax1ycmcgaadwdnf3ag8jbnjyc3eiaakgcnj1cw8idgf7dxvycqDocument2 pages27 Mar 2020 - (Free) ..Chqmwuilbna - Fawfawn - Ehqjeqx - B31yax1ycmcgaadwdnf3ag8jbnjyc3eiaakgcnj1cw8idgf7dxvycqkhuthadzoNo ratings yet

- Exercise 7-9 Credit Card and Debit Card Transactions LO5Document2 pagesExercise 7-9 Credit Card and Debit Card Transactions LO5Jehiel Mathew100% (1)

- Rie March2018Document1 pageRie March2018Zairo MosesNo ratings yet

- Demo Problem #1 Bank Rec Solution (White)Document2 pagesDemo Problem #1 Bank Rec Solution (White)Anu kahtterNo ratings yet

- Accounting Cycle ReviewerDocument20 pagesAccounting Cycle ReviewerKriezl Labay CalditoNo ratings yet

- Cash Additional ProblemsDocument2 pagesCash Additional ProblemsRed TigerNo ratings yet

- Tugas 3 (Revisi) - Proses Posting-Ricky Andrian K. RumereDocument23 pagesTugas 3 (Revisi) - Proses Posting-Ricky Andrian K. RumererickyNo ratings yet

- Cash On Hand Cash in BankDocument2 pagesCash On Hand Cash in BankCristina Melloria100% (1)

- Exercise 7.1: S.O. Heater Installations: Bank Reconciliation Statement As at 31 July 2015Document12 pagesExercise 7.1: S.O. Heater Installations: Bank Reconciliation Statement As at 31 July 2015Doan Chan PhongNo ratings yet

- AFA241Document5 pagesAFA241sarah josephNo ratings yet

- Accounting ExercisesDocument41 pagesAccounting ExercisesKayla MirandaNo ratings yet

- Nissan Renault Financial Services India Private Limited: Loan Account Statement For DBAN136091Document4 pagesNissan Renault Financial Services India Private Limited: Loan Account Statement For DBAN136091shashiNo ratings yet

- Topic 7: Cash Management and Control, Preparation Bank Reconciliations and Maintaining A Petty Cash System Solutions To Tutorial QuestionsDocument3 pagesTopic 7: Cash Management and Control, Preparation Bank Reconciliations and Maintaining A Petty Cash System Solutions To Tutorial QuestionsMitchell BylartNo ratings yet

- Accn June Memo 2015Document18 pagesAccn June Memo 2015Abrar DhoratNo ratings yet

- 18 Apr 2020 - (Free) ..cg11NTQKdgU - FXpwFhZhdQVyA3wCGXwCdhwEBxp-CHEOcw0DfBkIdgdzBQR1dgh2B3MDBn11DnECcgwHcQDocument1 page18 Apr 2020 - (Free) ..cg11NTQKdgU - FXpwFhZhdQVyA3wCGXwCdhwEBxp-CHEOcw0DfBkIdgdzBQR1dgh2B3MDBn11DnECcgwHcQLovemore Mutyambizi MuchenjeNo ratings yet

- Manduleli Victor Bikitsha Nsualwjh ArchivedDocument10 pagesManduleli Victor Bikitsha Nsualwjh ArchivedManduleli BikitshaNo ratings yet

- Acc Chapter 09Document39 pagesAcc Chapter 09Nicholas J W LeeNo ratings yet

- Further Information: Schedule of Accounts Receivable MayDocument6 pagesFurther Information: Schedule of Accounts Receivable MaySaifullah WaqarNo ratings yet

- BTVN Chapter 6 New 1Document21 pagesBTVN Chapter 6 New 1hangptt214051No ratings yet

- 2018 April Resource Booklet L2Document8 pages2018 April Resource Booklet L2Ronald YeeNo ratings yet

- Acc 2018 MemoDocument12 pagesAcc 2018 Memokyle.govender2004No ratings yet

- Unit 2. Audit of Cash and Cash Transactions - Handout - T21920 (Final)Document6 pagesUnit 2. Audit of Cash and Cash Transactions - Handout - T21920 (Final)Alyna JNo ratings yet

- San Andres Branch SOA 02-17-24 Bill DateDocument4 pagesSan Andres Branch SOA 02-17-24 Bill DateAnonymous gV9BmXXHNo ratings yet

- Business Supersave 36Document1 pageBusiness Supersave 36majodinaabegailNo ratings yet

- SWAZI+ONE Accounting ExerciseDocument2 pagesSWAZI+ONE Accounting Exercisekj98mcqc5zNo ratings yet

- Omaha Bank Statement (Card)Document3 pagesOmaha Bank Statement (Card)ВасилийNo ratings yet

- Nama: Melvina Puhut Siregar Nim: 1932150049 E7-23 (Petty Cash) Mcmann, Inc. Decided To Establish A Petty Cash Fund To Help Ensure InternalDocument6 pagesNama: Melvina Puhut Siregar Nim: 1932150049 E7-23 (Petty Cash) Mcmann, Inc. Decided To Establish A Petty Cash Fund To Help Ensure Internalmelvina siregarNo ratings yet

- GR11 Accounting Practice Exam November Paper 1 PDFDocument7 pagesGR11 Accounting Practice Exam November Paper 1 PDFGood LifeNo ratings yet

- San Andres Branch SOA 01-12-24Document4 pagesSan Andres Branch SOA 01-12-24Anonymous gV9BmXXHNo ratings yet

- Bank Reconciliation NotesDocument25 pagesBank Reconciliation NotesJohn Sue HanNo ratings yet

- TRƯƠNG THỊ QUỲNH NHƯ - ESSAY TEST - - ACC101 - IB17CDocument15 pagesTRƯƠNG THỊ QUỲNH NHƯ - ESSAY TEST - - ACC101 - IB17CTrương Thị Quỳnh NhưNo ratings yet

- General DescriptionDocument7 pagesGeneral Description11A Ol MonorothNo ratings yet

- College Accounting 12th Edition Slater Solutions Manual DownloadDocument35 pagesCollege Accounting 12th Edition Slater Solutions Manual DownloadRicardo Rivera100% (27)

- Perilla Geriqjoedn 1Document20 pagesPerilla Geriqjoedn 1Geriq Joeden PerillaNo ratings yet

- FA Assignment 5: Ishani Sathish (PGP/25/331)Document7 pagesFA Assignment 5: Ishani Sathish (PGP/25/331)ishaniNo ratings yet

- LawDocument3 pagesLawKhenett Ramirez PuertoNo ratings yet

- WDC202440Document1 pageWDC202440kennethmwangi2024No ratings yet

- Exercise Chap 2 NLKTDocument10 pagesExercise Chap 2 NLKTalexnguyen21007No ratings yet

- Topic No. 1 - Statement of Financial Position PDFDocument4 pagesTopic No. 1 - Statement of Financial Position PDFSARAH ANDREA TORRESNo ratings yet

- V1620034 - Dzaky FarhansyahDocument11 pagesV1620034 - Dzaky FarhansyahDzaky FarhansyahNo ratings yet

- Philippine Politics and Governance DLPDocument6 pagesPhilippine Politics and Governance DLPDMarrie Abao Boniao-LabadanNo ratings yet

- Trade IncDocument2 pagesTrade IncAnne Angelie Gomez SebialNo ratings yet

- 2022-03-10 Item 6aDocument4 pages2022-03-10 Item 6a视频精选全球No ratings yet

- Financial Accounting Assignment - 1Document17 pagesFinancial Accounting Assignment - 1Yosef MitikuNo ratings yet

- 2018-10-27 PDFDocument2 pages2018-10-27 PDFKhathutshelo KharivheNo ratings yet

- C02 Financial Accounting Fundamentals - Control AccountsDocument7 pagesC02 Financial Accounting Fundamentals - Control AccountsAlfred MakonaNo ratings yet

- 2018-10-27 PDFDocument2 pages2018-10-27 PDFKhathutshelo KharivheNo ratings yet

- Quiz Review CH 5 6 7Document8 pagesQuiz Review CH 5 6 7yanto ismailNo ratings yet

- RTM 2 Pa 1Document3 pagesRTM 2 Pa 1Mega UrjuwanNo ratings yet

- Financial Accounting and Reporting 1Document18 pagesFinancial Accounting and Reporting 1cruzdelica18No ratings yet

- Solutions To More SAC 1 Revision 2021Document5 pagesSolutions To More SAC 1 Revision 2021anshsinghsoniNo ratings yet

- BHN Ajar Samone Equipment Repair Inc - PreparationDocument29 pagesBHN Ajar Samone Equipment Repair Inc - PreparationfghhjjjnjjnNo ratings yet

- PL BS of MD ShafikDocument12 pagesPL BS of MD ShafikanupNo ratings yet

- Seminar Activity (10) - Managing Human ResourcesDocument7 pagesSeminar Activity (10) - Managing Human Resourcesbhattfenil29No ratings yet

- Grit Activity Week 1Document2 pagesGrit Activity Week 1bhattfenil29No ratings yet

- Excel Class FileDocument3 pagesExcel Class Filebhattfenil29No ratings yet

- Grit Activity Week 1Document2 pagesGrit Activity Week 1bhattfenil29No ratings yet

- Week12 SeminarAssignmentDocument13 pagesWeek12 SeminarAssignmentbhattfenil29No ratings yet

- Final Group Project - Opportunity AssessmentDocument7 pagesFinal Group Project - Opportunity Assessmentbhattfenil29No ratings yet

- Week10 SeminarAssignmentDocument7 pagesWeek10 SeminarAssignmentbhattfenil29No ratings yet

- Week11 CH5 SeminarAssignmentDocument10 pagesWeek11 CH5 SeminarAssignmentbhattfenil29No ratings yet

- Week9 - SeminarAssign Ch04Prob4 - 3ADocument12 pagesWeek9 - SeminarAssign Ch04Prob4 - 3Abhattfenil29No ratings yet

- AUDIT PROGRAM For Cash Disbursements 2Document5 pagesAUDIT PROGRAM For Cash Disbursements 2jezreel dela mercedNo ratings yet

- VLAN Setup in MikroTik SwitchOS (SwOS)Document3 pagesVLAN Setup in MikroTik SwitchOS (SwOS)Phạm Đức HạnhNo ratings yet

- SME Company NameDocument12 pagesSME Company NamesahildoraNo ratings yet

- Acct Statement XX8038 12102023Document5 pagesAcct Statement XX8038 12102023middeslifesciencesNo ratings yet

- Updated List of Insurance Entities in Good Standing As at November 20, 2020Document5 pagesUpdated List of Insurance Entities in Good Standing As at November 20, 2020Fuaad DodooNo ratings yet

- CyberSecOp Scoping Questionnaire March2023Document3 pagesCyberSecOp Scoping Questionnaire March2023hemanth_jayaraman100% (1)

- LinkageDocument1 pageLinkagerasool mehrjooNo ratings yet

- SBAA7025Document102 pagesSBAA7025Sharuk HussainNo ratings yet

- Upaya Hukum Otoritas Jasa Keuangan Dalam Mengatasi Layanan Pinjaman Online IlegalDocument12 pagesUpaya Hukum Otoritas Jasa Keuangan Dalam Mengatasi Layanan Pinjaman Online IlegalNursyah RazakNo ratings yet

- Futuristic NursingDocument6 pagesFuturistic NursingAnusha Verghese100% (1)

- Statement (CAD) : Corporate StaysDocument2 pagesStatement (CAD) : Corporate Staysvbt1561No ratings yet

- M/s. Valmind IT Needs Private Limited Pay Slip: Gross Pay 12,083 Net Pay 11,333Document5 pagesM/s. Valmind IT Needs Private Limited Pay Slip: Gross Pay 12,083 Net Pay 11,333Tech-savvy GirishaNo ratings yet

- Continuous Quality Improvement (CQI)Document15 pagesContinuous Quality Improvement (CQI)Kayla Suzanne GuanellaNo ratings yet

- Accounts Cec 1year Test PaparDocument2 pagesAccounts Cec 1year Test PaparMohammad MoinuddinNo ratings yet

- Lecture : Day 1: Adjusting Entries & Chart of Accounts (Periodic & Perpetual)Document7 pagesLecture : Day 1: Adjusting Entries & Chart of Accounts (Periodic & Perpetual)khrysna ayra villanuevaNo ratings yet

- Medical Transcription (Medical Records)Document32 pagesMedical Transcription (Medical Records)Rana Abd Almugeeth100% (5)

- BANKINGDocument14 pagesBANKINGpinky NathNo ratings yet

- WVCH Health Plan ContractDocument185 pagesWVCH Health Plan ContractStatesman JournalNo ratings yet

- Signal CommunicationDocument44 pagesSignal CommunicationIan PolancosNo ratings yet

- HZV1P3 Finisar Optics Reference Guide 1Document2 pagesHZV1P3 Finisar Optics Reference Guide 1Diy DoeNo ratings yet

- Last Mile LogisticsDocument7 pagesLast Mile LogisticsBoyce DigitalNo ratings yet

- Punjab State Cooperative BankDocument58 pagesPunjab State Cooperative BankRavneet Singh75% (4)

- Working Backward To Cash Receipts and DisbursementsDocument8 pagesWorking Backward To Cash Receipts and DisbursementsHarsha ThejaNo ratings yet

- Macroeconomic Assignment 1mba059 Ma Pann Myat PhyuDocument2 pagesMacroeconomic Assignment 1mba059 Ma Pann Myat PhyuCWHNo ratings yet

- RS Sharma CV 12032020Document3 pagesRS Sharma CV 12032020Sourav kachhawahaNo ratings yet

- Plkk-F-Hse-50 Daily - Report - Safety OfficerDocument1 pagePlkk-F-Hse-50 Daily - Report - Safety OfficerandriNo ratings yet

- Cash - Management and Fraud PreventionDocument21 pagesCash - Management and Fraud PreventionnathanielNo ratings yet

- Cash Managment (Q)Document7 pagesCash Managment (Q)amna zamanNo ratings yet

- Employee BenefitDocument37 pagesEmployee BenefitNinjo senpaiNo ratings yet