Acn 5

Acn 5

You might also like

- Operational Excellence RoadmapDocument1 pageOperational Excellence RoadmapWilson Perumal & Company67% (3)

- Group 8Document20 pagesGroup 8nirajNo ratings yet

- Problem in Activity Based CostingDocument3 pagesProblem in Activity Based CostingLee Thomas Arvey FernandoNo ratings yet

- ABC CostingDocument17 pagesABC CostingHameed Ullah KhanNo ratings yet

- Afar 1Document34 pagesAfar 1Patricia MandiNo ratings yet

- Case: XY Pvt. LTD: Management Accounting & Control AssignmentDocument5 pagesCase: XY Pvt. LTD: Management Accounting & Control AssignmentSwati DasNo ratings yet

- Activity Based Cost Accounting ProblemsDocument3 pagesActivity Based Cost Accounting ProblemsVicky VigneshNo ratings yet

- Chapter 10 Activity Based CostingDocument10 pagesChapter 10 Activity Based CostingRuby P. MadejaNo ratings yet

- Overhead HWDocument2 pagesOverhead HWTheint Myat KyalsinNo ratings yet

- Fineclad Apparel - Rani Treasa - 2009209Document7 pagesFineclad Apparel - Rani Treasa - 2009209RaniNo ratings yet

- As - CostingDocument9 pagesAs - CostingMUSTHARI KHANNo ratings yet

- Activity Based Costing Review QuestionsDocument3 pagesActivity Based Costing Review Questionshome labNo ratings yet

- S Iv CC 402 ScmaDocument60 pagesS Iv CC 402 ScmaRajnish DubeyNo ratings yet

- Handout Activity Based Costing 2020Document2 pagesHandout Activity Based Costing 2020Nicah AcojonNo ratings yet

- ABC and CashFlow QuestionDocument11 pagesABC and CashFlow QuestionTerryDemetrioCesar100% (1)

- CMA - FOH (Quiz)Document1 pageCMA - FOH (Quiz)Ahmed TahirNo ratings yet

- 05 Handout 1Document6 pages05 Handout 1Reanne Mae BilogNo ratings yet

- Overheads - IBADocument6 pagesOverheads - IBAZehra HussainNo ratings yet

- Managerial Accounting - Mid Term Exam PDFDocument4 pagesManagerial Accounting - Mid Term Exam PDFNavya AgrawalNo ratings yet

- Paper 3 Chapter 4 PractiseDocument11 pagesPaper 3 Chapter 4 PractiseAryan GuptaNo ratings yet

- Accounting For FOH Part 11Document16 pagesAccounting For FOH Part 11Shania LiwanagNo ratings yet

- Cma CDocument14 pagesCma CNaman agrawalNo ratings yet

- Midterm Assignment 3 On Cost Accounting and Control - Manufacturing Overhead - Departmentalization 2024Document1 pageMidterm Assignment 3 On Cost Accounting and Control - Manufacturing Overhead - Departmentalization 2024John karlo TarigaNo ratings yet

- Audit of Property, Plant and Equipment: Auditing ProblemsDocument5 pagesAudit of Property, Plant and Equipment: Auditing ProblemsLei PangilinanNo ratings yet

- 12914sugg Pe2 gp2 1Document33 pages12914sugg Pe2 gp2 1harshrathore17579No ratings yet

- Kuis Paralel AML - UTSDocument4 pagesKuis Paralel AML - UTSGrace EsterMNo ratings yet

- Zegu Cac 414 Practice QuestionsDocument9 pagesZegu Cac 414 Practice Questionsloise zvizvaiNo ratings yet

- Management Development Institute Gurgaon: InstructionsDocument2 pagesManagement Development Institute Gurgaon: Instructionspgpm20 SANCHIT GARGNo ratings yet

- 102.COAP - .L I Question CMA JUNE 2020 ExamDocument3 pages102.COAP - .L I Question CMA JUNE 2020 Examrumelrashid_seuNo ratings yet

- Sesi 5&6 PraktikDocument6 pagesSesi 5&6 PraktikDian Permata SariNo ratings yet

- Abc RemedialDocument6 pagesAbc RemedialMinie KimNo ratings yet

- Arcadia and Enterprise Co. Worked ExamplesDocument22 pagesArcadia and Enterprise Co. Worked ExamplesIvy TulesiNo ratings yet

- Chapter 12 AssignmentDocument7 pagesChapter 12 AssignmentAngelica AnonoyNo ratings yet

- Overhead Cost: Warunika N. HettiarachchiDocument52 pagesOverhead Cost: Warunika N. HettiarachchiAnuruddha RajasuriyaNo ratings yet

- Skans School of Accountancy Cost & Management Accounting - Caf 08 Class Test # 1Document4 pagesSkans School of Accountancy Cost & Management Accounting - Caf 08 Class Test # 1maryNo ratings yet

- Homework For ABCDocument6 pagesHomework For ABCLikey CruzNo ratings yet

- ABC - Sem-IV - 10 MarksDocument5 pagesABC - Sem-IV - 10 MarksTechboy RahulNo ratings yet

- WK4 Abc Ii HMWRK QDocument1 pageWK4 Abc Ii HMWRK QFungaiNo ratings yet

- ABC Sample Problems 1Document13 pagesABC Sample Problems 1Mary Grace PagalanNo ratings yet

- Chapter - 05 - Activity - Based - Costing - ABC - .Doc - Filename UTF-8''Chapter 05 Activity Based Costing (ABC)Document8 pagesChapter - 05 - Activity - Based - Costing - ABC - .Doc - Filename UTF-8''Chapter 05 Activity Based Costing (ABC)NasrinTonni AhmedNo ratings yet

- Additional Problems in ABCDocument3 pagesAdditional Problems in ABCMaviel SuaverdezNo ratings yet

- Extra Questions For Chapter 3 Cost Assignment: 3.1 Intermediate: Job Cost CalculationDocument72 pagesExtra Questions For Chapter 3 Cost Assignment: 3.1 Intermediate: Job Cost Calculationjessica_joaquinNo ratings yet

- Pricing Decisions and Cost ManagementDocument18 pagesPricing Decisions and Cost ManagementAmrit PrasadNo ratings yet

- Activity Based Costing SystemDocument18 pagesActivity Based Costing SystemMAXA FASHIONNo ratings yet

- 7e Extra QDocument72 pages7e Extra QNur AimyNo ratings yet

- W7 Handout 1 For StudentDocument15 pagesW7 Handout 1 For StudentDo Tue MinhNo ratings yet

- Publishing Company Question: Service Department Operating Department A B C 1 2 TotalDocument3 pagesPublishing Company Question: Service Department Operating Department A B C 1 2 Totalisrael adesanyaNo ratings yet

- Midterm Quiz 3 On Cost Accounting and Control - Manufacturing Overhead - Departmentalization 2024Document1 pageMidterm Quiz 3 On Cost Accounting and Control - Manufacturing Overhead - Departmentalization 2024John karlo TarigaNo ratings yet

- Hassan Exame 21 AugustrDocument4 pagesHassan Exame 21 Augustrsardar hussainNo ratings yet

- Overheads & ABC - Questions Test 1Document4 pagesOverheads & ABC - Questions Test 1jj4223062003No ratings yet

- ABC Model For A UniversityDocument20 pagesABC Model For A UniversityrahulNo ratings yet

- FIFODocument5 pagesFIFOYanna YahNo ratings yet

- (w8) ABC Class ExerciseDocument6 pages(w8) ABC Class ExerciseDarya KoroviyNo ratings yet

- Tugas Sesi 3 - AML PDFDocument2 pagesTugas Sesi 3 - AML PDFcatharina arnitaNo ratings yet

- Activity Based Costing Notes and ExerciseDocument6 pagesActivity Based Costing Notes and Exercisefrancis MagobaNo ratings yet

- Job and Batch CostingDocument3 pagesJob and Batch CostingbhngbjNo ratings yet

- Group 10 - Chapter 12 - Group Assignment No. 10 Exercises 1 & 2 Pages 331 - 334Document31 pagesGroup 10 - Chapter 12 - Group Assignment No. 10 Exercises 1 & 2 Pages 331 - 334Carla TalanganNo ratings yet

- Cma ProblemsDocument25 pagesCma ProblemsPridhvi Raj ReddyNo ratings yet

- Creating a One-Piece Flow and Production Cell: Just-in-time Production with Toyota’s Single Piece FlowFrom EverandCreating a One-Piece Flow and Production Cell: Just-in-time Production with Toyota’s Single Piece FlowRating: 4 out of 5 stars4/5 (1)

- Chapter 2-Culture in IHRMDocument22 pagesChapter 2-Culture in IHRMNavidul IslamNo ratings yet

- Acn202 AssignmentDocument6 pagesAcn202 AssignmentNavidul IslamNo ratings yet

- Acn 3Document5 pagesAcn 3Navidul IslamNo ratings yet

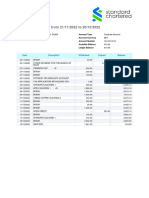

- Account StatmentDocument1 pageAccount StatmentNavidul IslamNo ratings yet

- What Is The Difference Between SCM and Logistics?Document3 pagesWhat Is The Difference Between SCM and Logistics?Atiqah Ismail67% (3)

- Answer Key PTDocument42 pagesAnswer Key PTMJ ArboledaNo ratings yet

- Handout 3 Cost ManagementDocument10 pagesHandout 3 Cost ManagementNikki San GabrielNo ratings yet

- IC Kanban Board Spreadsheet 11578 0Document12 pagesIC Kanban Board Spreadsheet 11578 0toilalongNo ratings yet

- Operational Guidance: Inspection Procedure (June 2018) : Enforcement Policy Statement Enforcement Management ModelDocument8 pagesOperational Guidance: Inspection Procedure (June 2018) : Enforcement Policy Statement Enforcement Management ModelRinaldi ArazaquNo ratings yet

- Project Plan: Group Case Study 4 OctoberDocument15 pagesProject Plan: Group Case Study 4 OctobernileshvpNo ratings yet

- CAT Reman: Reman Generator Product Line ExpandedDocument4 pagesCAT Reman: Reman Generator Product Line ExpandedssinokrotNo ratings yet

- Total Quality Management in Banking SectorDocument8 pagesTotal Quality Management in Banking SectorAadil KakarNo ratings yet

- Radiomuseum Grundig Konzertschrank Ks490we Export 456917Document2 pagesRadiomuseum Grundig Konzertschrank Ks490we Export 456917brenodesenneNo ratings yet

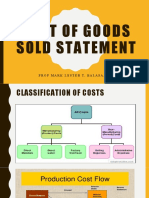

- Cost of Goods Sold StatementDocument18 pagesCost of Goods Sold StatementCherrylane EdicaNo ratings yet

- UK Communications Industry Architecture Summit: 30 September 2015 LondonDocument35 pagesUK Communications Industry Architecture Summit: 30 September 2015 Londontranhieu5959No ratings yet

- Job Safety Analysis Worksheet: JSA JSA Participants PPE Required Tools And/or EquipmentDocument5 pagesJob Safety Analysis Worksheet: JSA JSA Participants PPE Required Tools And/or EquipmentVigieNo ratings yet

- 303 Production and Operation Management Ajay PDFDocument10 pages303 Production and Operation Management Ajay PDFAnkita Dash100% (1)

- Topic 10 Dividend Policy FinalDocument13 pagesTopic 10 Dividend Policy Finalshivani dholeNo ratings yet

- 55908551177Document3 pages55908551177junaidi 9No ratings yet

- Case 1 - CCSDocument3 pagesCase 1 - CCSShashi RanjanNo ratings yet

- Entrepreneurship Assignment No 1 M.Com 2 (Evening)Document3 pagesEntrepreneurship Assignment No 1 M.Com 2 (Evening)Aftab AlamNo ratings yet

- Tutorial Relevant Costs For StudentsDocument3 pagesTutorial Relevant Costs For StudentsJihan RafiqaNo ratings yet

- Digitally Signed by DS Reliance Retail Limited Date: 2022.09.27 05:05:23 ISTDocument1 pageDigitally Signed by DS Reliance Retail Limited Date: 2022.09.27 05:05:23 ISTsairaj utekarNo ratings yet

- Case Study Presentation ON Rendell Company: Presented ByDocument14 pagesCase Study Presentation ON Rendell Company: Presented Bynimmisaxena2005No ratings yet

- Managing RiskDocument12 pagesManaging RiskMARGANE MONTERONA-GALLETONo ratings yet

- 01 x01 Basic ConceptsDocument9 pages01 x01 Basic ConceptsNorfaidah IbrahimNo ratings yet

- The Essentials Off Procure-To-Pay: EbookDocument10 pagesThe Essentials Off Procure-To-Pay: EbookSurendra PNo ratings yet

- EXAMPLE 20.1: Hotel Reservations: Inventory ManagementDocument2 pagesEXAMPLE 20.1: Hotel Reservations: Inventory Managementkael invokerNo ratings yet

- Audit Sampling.2024Document48 pagesAudit Sampling.2024najiath mzeeNo ratings yet

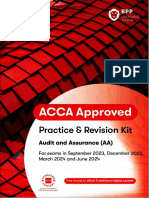

- Aa BPP Kit J24Document519 pagesAa BPP Kit J24Myo NaingNo ratings yet

- QuizDocument2 pagesQuizGilang LestariNo ratings yet

- CH 18 20 AKMDocument121 pagesCH 18 20 AKMDewanto Kusumo100% (1)

- BR100 INV Inventory Application SetupDocument51 pagesBR100 INV Inventory Application SetupAbdelaziz Abada100% (2)

Download as pdf or txt

You might also like

- Operational Excellence RoadmapDocument1 pageOperational Excellence RoadmapWilson Perumal & Company67% (3)

- Group 8Document20 pagesGroup 8nirajNo ratings yet

- Problem in Activity Based CostingDocument3 pagesProblem in Activity Based CostingLee Thomas Arvey FernandoNo ratings yet

- ABC CostingDocument17 pagesABC CostingHameed Ullah KhanNo ratings yet

- Afar 1Document34 pagesAfar 1Patricia MandiNo ratings yet

- Case: XY Pvt. LTD: Management Accounting & Control AssignmentDocument5 pagesCase: XY Pvt. LTD: Management Accounting & Control AssignmentSwati DasNo ratings yet

- Activity Based Cost Accounting ProblemsDocument3 pagesActivity Based Cost Accounting ProblemsVicky VigneshNo ratings yet

- Chapter 10 Activity Based CostingDocument10 pagesChapter 10 Activity Based CostingRuby P. MadejaNo ratings yet

- Overhead HWDocument2 pagesOverhead HWTheint Myat KyalsinNo ratings yet

- Fineclad Apparel - Rani Treasa - 2009209Document7 pagesFineclad Apparel - Rani Treasa - 2009209RaniNo ratings yet

- As - CostingDocument9 pagesAs - CostingMUSTHARI KHANNo ratings yet

- Activity Based Costing Review QuestionsDocument3 pagesActivity Based Costing Review Questionshome labNo ratings yet

- S Iv CC 402 ScmaDocument60 pagesS Iv CC 402 ScmaRajnish DubeyNo ratings yet

- Handout Activity Based Costing 2020Document2 pagesHandout Activity Based Costing 2020Nicah AcojonNo ratings yet

- ABC and CashFlow QuestionDocument11 pagesABC and CashFlow QuestionTerryDemetrioCesar100% (1)

- CMA - FOH (Quiz)Document1 pageCMA - FOH (Quiz)Ahmed TahirNo ratings yet

- 05 Handout 1Document6 pages05 Handout 1Reanne Mae BilogNo ratings yet

- Overheads - IBADocument6 pagesOverheads - IBAZehra HussainNo ratings yet

- Managerial Accounting - Mid Term Exam PDFDocument4 pagesManagerial Accounting - Mid Term Exam PDFNavya AgrawalNo ratings yet

- Paper 3 Chapter 4 PractiseDocument11 pagesPaper 3 Chapter 4 PractiseAryan GuptaNo ratings yet

- Accounting For FOH Part 11Document16 pagesAccounting For FOH Part 11Shania LiwanagNo ratings yet

- Cma CDocument14 pagesCma CNaman agrawalNo ratings yet

- Midterm Assignment 3 On Cost Accounting and Control - Manufacturing Overhead - Departmentalization 2024Document1 pageMidterm Assignment 3 On Cost Accounting and Control - Manufacturing Overhead - Departmentalization 2024John karlo TarigaNo ratings yet

- Audit of Property, Plant and Equipment: Auditing ProblemsDocument5 pagesAudit of Property, Plant and Equipment: Auditing ProblemsLei PangilinanNo ratings yet

- 12914sugg Pe2 gp2 1Document33 pages12914sugg Pe2 gp2 1harshrathore17579No ratings yet

- Kuis Paralel AML - UTSDocument4 pagesKuis Paralel AML - UTSGrace EsterMNo ratings yet

- Zegu Cac 414 Practice QuestionsDocument9 pagesZegu Cac 414 Practice Questionsloise zvizvaiNo ratings yet

- Management Development Institute Gurgaon: InstructionsDocument2 pagesManagement Development Institute Gurgaon: Instructionspgpm20 SANCHIT GARGNo ratings yet

- 102.COAP - .L I Question CMA JUNE 2020 ExamDocument3 pages102.COAP - .L I Question CMA JUNE 2020 Examrumelrashid_seuNo ratings yet

- Sesi 5&6 PraktikDocument6 pagesSesi 5&6 PraktikDian Permata SariNo ratings yet

- Abc RemedialDocument6 pagesAbc RemedialMinie KimNo ratings yet

- Arcadia and Enterprise Co. Worked ExamplesDocument22 pagesArcadia and Enterprise Co. Worked ExamplesIvy TulesiNo ratings yet

- Chapter 12 AssignmentDocument7 pagesChapter 12 AssignmentAngelica AnonoyNo ratings yet

- Overhead Cost: Warunika N. HettiarachchiDocument52 pagesOverhead Cost: Warunika N. HettiarachchiAnuruddha RajasuriyaNo ratings yet

- Skans School of Accountancy Cost & Management Accounting - Caf 08 Class Test # 1Document4 pagesSkans School of Accountancy Cost & Management Accounting - Caf 08 Class Test # 1maryNo ratings yet

- Homework For ABCDocument6 pagesHomework For ABCLikey CruzNo ratings yet

- ABC - Sem-IV - 10 MarksDocument5 pagesABC - Sem-IV - 10 MarksTechboy RahulNo ratings yet

- WK4 Abc Ii HMWRK QDocument1 pageWK4 Abc Ii HMWRK QFungaiNo ratings yet

- ABC Sample Problems 1Document13 pagesABC Sample Problems 1Mary Grace PagalanNo ratings yet

- Chapter - 05 - Activity - Based - Costing - ABC - .Doc - Filename UTF-8''Chapter 05 Activity Based Costing (ABC)Document8 pagesChapter - 05 - Activity - Based - Costing - ABC - .Doc - Filename UTF-8''Chapter 05 Activity Based Costing (ABC)NasrinTonni AhmedNo ratings yet

- Additional Problems in ABCDocument3 pagesAdditional Problems in ABCMaviel SuaverdezNo ratings yet

- Extra Questions For Chapter 3 Cost Assignment: 3.1 Intermediate: Job Cost CalculationDocument72 pagesExtra Questions For Chapter 3 Cost Assignment: 3.1 Intermediate: Job Cost Calculationjessica_joaquinNo ratings yet

- Pricing Decisions and Cost ManagementDocument18 pagesPricing Decisions and Cost ManagementAmrit PrasadNo ratings yet

- Activity Based Costing SystemDocument18 pagesActivity Based Costing SystemMAXA FASHIONNo ratings yet

- 7e Extra QDocument72 pages7e Extra QNur AimyNo ratings yet

- W7 Handout 1 For StudentDocument15 pagesW7 Handout 1 For StudentDo Tue MinhNo ratings yet

- Publishing Company Question: Service Department Operating Department A B C 1 2 TotalDocument3 pagesPublishing Company Question: Service Department Operating Department A B C 1 2 Totalisrael adesanyaNo ratings yet

- Midterm Quiz 3 On Cost Accounting and Control - Manufacturing Overhead - Departmentalization 2024Document1 pageMidterm Quiz 3 On Cost Accounting and Control - Manufacturing Overhead - Departmentalization 2024John karlo TarigaNo ratings yet

- Hassan Exame 21 AugustrDocument4 pagesHassan Exame 21 Augustrsardar hussainNo ratings yet

- Overheads & ABC - Questions Test 1Document4 pagesOverheads & ABC - Questions Test 1jj4223062003No ratings yet

- ABC Model For A UniversityDocument20 pagesABC Model For A UniversityrahulNo ratings yet

- FIFODocument5 pagesFIFOYanna YahNo ratings yet

- (w8) ABC Class ExerciseDocument6 pages(w8) ABC Class ExerciseDarya KoroviyNo ratings yet

- Tugas Sesi 3 - AML PDFDocument2 pagesTugas Sesi 3 - AML PDFcatharina arnitaNo ratings yet

- Activity Based Costing Notes and ExerciseDocument6 pagesActivity Based Costing Notes and Exercisefrancis MagobaNo ratings yet

- Job and Batch CostingDocument3 pagesJob and Batch CostingbhngbjNo ratings yet

- Group 10 - Chapter 12 - Group Assignment No. 10 Exercises 1 & 2 Pages 331 - 334Document31 pagesGroup 10 - Chapter 12 - Group Assignment No. 10 Exercises 1 & 2 Pages 331 - 334Carla TalanganNo ratings yet

- Cma ProblemsDocument25 pagesCma ProblemsPridhvi Raj ReddyNo ratings yet

- Creating a One-Piece Flow and Production Cell: Just-in-time Production with Toyota’s Single Piece FlowFrom EverandCreating a One-Piece Flow and Production Cell: Just-in-time Production with Toyota’s Single Piece FlowRating: 4 out of 5 stars4/5 (1)

- Chapter 2-Culture in IHRMDocument22 pagesChapter 2-Culture in IHRMNavidul IslamNo ratings yet

- Acn202 AssignmentDocument6 pagesAcn202 AssignmentNavidul IslamNo ratings yet

- Acn 3Document5 pagesAcn 3Navidul IslamNo ratings yet

- Account StatmentDocument1 pageAccount StatmentNavidul IslamNo ratings yet

- What Is The Difference Between SCM and Logistics?Document3 pagesWhat Is The Difference Between SCM and Logistics?Atiqah Ismail67% (3)

- Answer Key PTDocument42 pagesAnswer Key PTMJ ArboledaNo ratings yet

- Handout 3 Cost ManagementDocument10 pagesHandout 3 Cost ManagementNikki San GabrielNo ratings yet

- IC Kanban Board Spreadsheet 11578 0Document12 pagesIC Kanban Board Spreadsheet 11578 0toilalongNo ratings yet

- Operational Guidance: Inspection Procedure (June 2018) : Enforcement Policy Statement Enforcement Management ModelDocument8 pagesOperational Guidance: Inspection Procedure (June 2018) : Enforcement Policy Statement Enforcement Management ModelRinaldi ArazaquNo ratings yet

- Project Plan: Group Case Study 4 OctoberDocument15 pagesProject Plan: Group Case Study 4 OctobernileshvpNo ratings yet

- CAT Reman: Reman Generator Product Line ExpandedDocument4 pagesCAT Reman: Reman Generator Product Line ExpandedssinokrotNo ratings yet

- Total Quality Management in Banking SectorDocument8 pagesTotal Quality Management in Banking SectorAadil KakarNo ratings yet

- Radiomuseum Grundig Konzertschrank Ks490we Export 456917Document2 pagesRadiomuseum Grundig Konzertschrank Ks490we Export 456917brenodesenneNo ratings yet

- Cost of Goods Sold StatementDocument18 pagesCost of Goods Sold StatementCherrylane EdicaNo ratings yet

- UK Communications Industry Architecture Summit: 30 September 2015 LondonDocument35 pagesUK Communications Industry Architecture Summit: 30 September 2015 Londontranhieu5959No ratings yet

- Job Safety Analysis Worksheet: JSA JSA Participants PPE Required Tools And/or EquipmentDocument5 pagesJob Safety Analysis Worksheet: JSA JSA Participants PPE Required Tools And/or EquipmentVigieNo ratings yet

- 303 Production and Operation Management Ajay PDFDocument10 pages303 Production and Operation Management Ajay PDFAnkita Dash100% (1)

- Topic 10 Dividend Policy FinalDocument13 pagesTopic 10 Dividend Policy Finalshivani dholeNo ratings yet

- 55908551177Document3 pages55908551177junaidi 9No ratings yet

- Case 1 - CCSDocument3 pagesCase 1 - CCSShashi RanjanNo ratings yet

- Entrepreneurship Assignment No 1 M.Com 2 (Evening)Document3 pagesEntrepreneurship Assignment No 1 M.Com 2 (Evening)Aftab AlamNo ratings yet

- Tutorial Relevant Costs For StudentsDocument3 pagesTutorial Relevant Costs For StudentsJihan RafiqaNo ratings yet

- Digitally Signed by DS Reliance Retail Limited Date: 2022.09.27 05:05:23 ISTDocument1 pageDigitally Signed by DS Reliance Retail Limited Date: 2022.09.27 05:05:23 ISTsairaj utekarNo ratings yet

- Case Study Presentation ON Rendell Company: Presented ByDocument14 pagesCase Study Presentation ON Rendell Company: Presented Bynimmisaxena2005No ratings yet

- Managing RiskDocument12 pagesManaging RiskMARGANE MONTERONA-GALLETONo ratings yet

- 01 x01 Basic ConceptsDocument9 pages01 x01 Basic ConceptsNorfaidah IbrahimNo ratings yet

- The Essentials Off Procure-To-Pay: EbookDocument10 pagesThe Essentials Off Procure-To-Pay: EbookSurendra PNo ratings yet

- EXAMPLE 20.1: Hotel Reservations: Inventory ManagementDocument2 pagesEXAMPLE 20.1: Hotel Reservations: Inventory Managementkael invokerNo ratings yet

- Audit Sampling.2024Document48 pagesAudit Sampling.2024najiath mzeeNo ratings yet

- Aa BPP Kit J24Document519 pagesAa BPP Kit J24Myo NaingNo ratings yet

- QuizDocument2 pagesQuizGilang LestariNo ratings yet

- CH 18 20 AKMDocument121 pagesCH 18 20 AKMDewanto Kusumo100% (1)

- BR100 INV Inventory Application SetupDocument51 pagesBR100 INV Inventory Application SetupAbdelaziz Abada100% (2)