Download as pdf or txt

You might also like

- Afar Mock Board 2022Document16 pagesAfar Mock Board 2022Reynaldo corpuz0% (1)

- Cost Accounting Summary NotesDocument10 pagesCost Accounting Summary NotesCarlene Ugay100% (1)

- Ind As 2: Inventories: (I) MeaningDocument6 pagesInd As 2: Inventories: (I) MeaningDinesh KumarNo ratings yet

- FR Shield - Ind As 2 - InventoriesDocument4 pagesFR Shield - Ind As 2 - InventoriesTanvi jain100% (1)

- As 2Document7 pagesAs 2sanjay sNo ratings yet

- As - 2: Valuation of InventoriesDocument18 pagesAs - 2: Valuation of InventoriesrajuNo ratings yet

- 08 Ias 2Document3 pages08 Ias 2Irtiza AbbasNo ratings yet

- Ias2 SNDocument7 pagesIas2 SNEmaan QaiserNo ratings yet

- 04 InventoriesDocument52 pages04 InventoriesKhalid MahmoodNo ratings yet

- 13.3 As 2 Valuation of Inventories Revision Notes by Nitin Goel Sir PDFDocument6 pages13.3 As 2 Valuation of Inventories Revision Notes by Nitin Goel Sir PDFSrinishaNo ratings yet

- AS 2 - Valuation of Inventories: Paper 1: Financial Reporting Chapter 1 Unit 3Document32 pagesAS 2 - Valuation of Inventories: Paper 1: Financial Reporting Chapter 1 Unit 3arvindNo ratings yet

- (Finished Goods/stock in Trade) (Work - In-Progress) (Raw Material, Stores and Spares, Etc.)Document20 pages(Finished Goods/stock in Trade) (Work - In-Progress) (Raw Material, Stores and Spares, Etc.)razorNo ratings yet

- AS 2 Valuation of InventoriesDocument18 pagesAS 2 Valuation of InventoriesRENU PALINo ratings yet

- AS 2 Valuation of InventoriesDocument11 pagesAS 2 Valuation of InventoriesBharatbhusan RoutNo ratings yet

- Aaca Chap 12Document3 pagesAaca Chap 12Eidel PantaleonNo ratings yet

- Chapter 18 IAS 2 InventoriesDocument6 pagesChapter 18 IAS 2 InventoriesKelvin Chu JYNo ratings yet

- Scope: Allocation of Fixed Production OverheadsDocument8 pagesScope: Allocation of Fixed Production OverheadsjayveeNo ratings yet

- CA IPCC As - 2,7,9,10 Accounts As by Rohan SirDocument38 pagesCA IPCC As - 2,7,9,10 Accounts As by Rohan SirJoya AhasanNo ratings yet

- LKAS 2 / IAS 2 - InventoriesDocument29 pagesLKAS 2 / IAS 2 - InventoriesShihan Haniff100% (9)

- Review Session 01 MA Topics 1-6 AfterDocument32 pagesReview Session 01 MA Topics 1-6 AftermisalNo ratings yet

- Review Session 01 MA Topics 1-6 BeforeDocument32 pagesReview Session 01 MA Topics 1-6 BeforemisalNo ratings yet

- Ind As-2 SummaryDocument7 pagesInd As-2 Summarysagarsingla1234509876No ratings yet

- Inventories NotesDocument2 pagesInventories NotesMikaela LacabaNo ratings yet

- Chapter 5 InventoriesDocument12 pagesChapter 5 InventoriesMelvin OngNo ratings yet

- 4 - Pages From 294214181 IFRS Explained Study Text 2014Document5 pages4 - Pages From 294214181 IFRS Explained Study Text 2014Wedi TassewNo ratings yet

- BookDocument1,240 pagesBookAmitNo ratings yet

- Ojas FR Module 1Document280 pagesOjas FR Module 1AnupNo ratings yet

- Ias 2Document47 pagesIas 2waqas ahmadNo ratings yet

- ea2e5ecc-fa8e-46c7-891a-a70d7ab7fc6fDocument13 pagesea2e5ecc-fa8e-46c7-891a-a70d7ab7fc6fKajal SharmaNo ratings yet

- Inventory ValuationDocument16 pagesInventory ValuationKillari PadmasriNo ratings yet

- Inventories: Initial RecognitionDocument5 pagesInventories: Initial RecognitionMary Grace NaragNo ratings yet

- SIM - Variable and Absorption Costing - 0Document5 pagesSIM - Variable and Absorption Costing - 0lilienesieraNo ratings yet

- Farap 4503Document12 pagesFarap 4503Marya Nvlz100% (1)

- Absorption and Variable Costing ReviewDocument13 pagesAbsorption and Variable Costing ReviewRodelLabor100% (1)

- Accounting StandardsDocument56 pagesAccounting StandardsAkshay KumarNo ratings yet

- Inventories Lkas 2Document12 pagesInventories Lkas 2kavindyatharaki2002No ratings yet

- G Ias 2Document19 pagesG Ias 2Daniel MNo ratings yet

- Management Accounting NotesDocument212 pagesManagement Accounting NotesFrank Chinguwo100% (1)

- 1 Inventories and ShortDocument6 pages1 Inventories and ShortHussein FokeerNo ratings yet

- Acc 203 RevDocument6 pagesAcc 203 RevHazel DimaanoNo ratings yet

- MAS 9204 Product Costing Activity-Based Costing (ABC)Document19 pagesMAS 9204 Product Costing Activity-Based Costing (ABC)Mila Casandra CastañedaNo ratings yet

- NOTE CHAPTER 9 - Absorption Costing & Marginal CostingDocument18 pagesNOTE CHAPTER 9 - Absorption Costing & Marginal CostingNUR ANIS SYAMIMI BINTI MUSTAFA / UPMNo ratings yet

- Assignment 1571213755 SmsDocument15 pagesAssignment 1571213755 SmsRahul Kumar Sharma 17No ratings yet

- Variable and Absorption CostingDocument4 pagesVariable and Absorption CostingFranz CampuedNo ratings yet

- Ias 2 - InventoriesDocument2 pagesIas 2 - Inventoriesangelinamaye99No ratings yet

- Presentation4.1 - Audit of Inventories, Cost of Sales and Other Related AccountsDocument37 pagesPresentation4.1 - Audit of Inventories, Cost of Sales and Other Related AccountsRoseanne Dela CruzNo ratings yet

- Absorption and Marginal CostingDocument19 pagesAbsorption and Marginal CostingsadikzeenatNo ratings yet

- ACT121 - Topic 5Document5 pagesACT121 - Topic 5Juan FrivaldoNo ratings yet

- Cagayan - Batch 2Document22 pagesCagayan - Batch 2Sarah BalisacanNo ratings yet

- Chapter 3 - IND AS 2 InventoriesDocument18 pagesChapter 3 - IND AS 2 InventoriesAmbati Madhava ReddyNo ratings yet

- TOPIC3 InventoriesDocument17 pagesTOPIC3 InventoriesNhlosenhle MthiyaneNo ratings yet

- D - Absorption and Variable CostingDocument5 pagesD - Absorption and Variable Costingian dizonNo ratings yet

- Costman Variable CostingDocument2 pagesCostman Variable CostingJeremi BernardoNo ratings yet

- معايير Ch 2 InventoriesDocument11 pagesمعايير Ch 2 InventoriesHamza MahmoudNo ratings yet

- T10 - NoteDocument7 pagesT10 - NoterbnbalachandranNo ratings yet

- Chapter 7Document12 pagesChapter 7Camille GarciaNo ratings yet

- Cost NotesDocument49 pagesCost NotesHarriniNo ratings yet

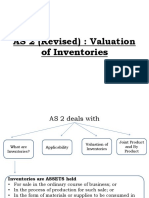

- AS 2 (Revised) : Valuation of InventoriesDocument13 pagesAS 2 (Revised) : Valuation of InventoriesAkshay PatilNo ratings yet

- Review Materials: Prepared By: Junior Philippine Institute of Accountants UC-Banilad Chapter F.Y. 2019-2020Document22 pagesReview Materials: Prepared By: Junior Philippine Institute of Accountants UC-Banilad Chapter F.Y. 2019-2020AB CloydNo ratings yet

- 74695bos60485 Inter p1 cp5 U1Document20 pages74695bos60485 Inter p1 cp5 U1Just KiddingNo ratings yet

- Management Accounting: Decision-Making by Numbers: Business Strategy & Competitive AdvantageFrom EverandManagement Accounting: Decision-Making by Numbers: Business Strategy & Competitive AdvantageRating: 5 out of 5 stars5/5 (1)

- Taxation Sec B May 2024 1703584298Document6 pagesTaxation Sec B May 2024 1703584298abhishekkapse654No ratings yet

- Taxation Sec B May 2024 1703584210Document6 pagesTaxation Sec B May 2024 1703584210abhishekkapse654No ratings yet

- Taxation Sec B May 2024 1703584499Document8 pagesTaxation Sec B May 2024 1703584499abhishekkapse654No ratings yet

- Taxation Sec B May 2024 1703583896Document15 pagesTaxation Sec B May 2024 1703583896abhishekkapse654No ratings yet

- As 19Document8 pagesAs 19abhishekkapse654No ratings yet

- Day 5Document7 pagesDay 5abhishekkapse654No ratings yet

- PDF 167984100250523Document1 pagePDF 167984100250523abhishekkapse654No ratings yet

- FM Chart BookDocument36 pagesFM Chart Bookabhishekkapse654No ratings yet

- Audit Chap-6 Short NotesDocument1 pageAudit Chap-6 Short Notesabhishekkapse654No ratings yet

- Economics Important QuestionsDocument4 pagesEconomics Important Questionsabhishekkapse654No ratings yet

- EIS Mentor N23Document308 pagesEIS Mentor N23abhishekkapse654No ratings yet

- Law120230912 13.6.41Document5 pagesLaw120230912 13.6.41abhishekkapse654No ratings yet

- Dividend Short NotesDocument1 pageDividend Short Notesabhishekkapse654No ratings yet

- Unit 4 Quotation and OfferDocument37 pagesUnit 4 Quotation and OfferthuhienNo ratings yet

- Pte ORNDocument9 pagesPte ORNamandeep9895No ratings yet

- ODC Otis ElevatorzDocument6 pagesODC Otis Elevatorzarnab sanyal100% (1)

- Microeconomics Course SyllabusDocument5 pagesMicroeconomics Course SyllabusSamira AlhashimiNo ratings yet

- Week 14: Game Theory and Pricing Strategies Game TheoryDocument3 pagesWeek 14: Game Theory and Pricing Strategies Game Theorysherryl caoNo ratings yet

- M607 L06 SolutionDocument5 pagesM607 L06 SolutionRonak PatelNo ratings yet

- Bid SheetDocument6 pagesBid SheetVi KraNo ratings yet

- 20140811Document28 pages20140811កំពូលបុរសឯកាNo ratings yet

- Markets For Factor Inputs, Labour Market Economic Rent: Chapter 10 & 11Document24 pagesMarkets For Factor Inputs, Labour Market Economic Rent: Chapter 10 & 11Sapna RohitNo ratings yet

- Chap 002 SDocument8 pagesChap 002 SAashima GroverNo ratings yet

- HUL CasestudyDocument15 pagesHUL CasestudyBecky PaulNo ratings yet

- Customer Ordering Guide and Price List: Transit Chassis CabDocument18 pagesCustomer Ordering Guide and Price List: Transit Chassis CabZoraydaNo ratings yet

- Semira - Kuku - Mba 502-3-2 Final Project.Document3 pagesSemira - Kuku - Mba 502-3-2 Final Project.Eric WogbeNo ratings yet

- Comparative AdvertisingDocument3 pagesComparative Advertisingdnrwn0% (1)

- Office Stationery Manufacturing in The US Industry ReportDocument40 pagesOffice Stationery Manufacturing in The US Industry Reportdr_digital100% (1)

- Ch08 - Principles of Capital InvestmentDocument7 pagesCh08 - Principles of Capital InvestmentStevin GeorgeNo ratings yet

- Chapter11 Stock Valuation and RiskDocument39 pagesChapter11 Stock Valuation and RiskRaghav MadaanNo ratings yet

- 12 Accountancy sp04Document45 pages12 Accountancy sp04Priyansh AryaNo ratings yet

- CH 5 Process CostingDocument13 pagesCH 5 Process CostingAmit SawantNo ratings yet

- CMR Institute of Technology: A Project ReportDocument73 pagesCMR Institute of Technology: A Project ReportKishor KumarNo ratings yet

- BAFI1018 International FinanceDocument109 pagesBAFI1018 International FinanceSteven NgNo ratings yet

- Mohd. Faid Khan: ObjectiveDocument4 pagesMohd. Faid Khan: Objectiveanon_948045789No ratings yet

- ICTSD White Paper - James Bacchus - Triggering The Trade Transition - G20 Role in Rules For Trade and Climate Change - Feb 2018Document40 pagesICTSD White Paper - James Bacchus - Triggering The Trade Transition - G20 Role in Rules For Trade and Climate Change - Feb 2018Seni NabouNo ratings yet

- Tax Review Part 1Document29 pagesTax Review Part 1JImlan Sahipa IsmaelNo ratings yet

- Club of Mozambique InfoDocument9 pagesClub of Mozambique Infojt4fds100% (1)

- The Foundation of EconomicsDocument11 pagesThe Foundation of EconomicstychrNo ratings yet

- Business Economics - Session 1 (LMS)Document28 pagesBusiness Economics - Session 1 (LMS)Abhimanyu AnejaNo ratings yet

- Allocative and Productive EfficiencyDocument6 pagesAllocative and Productive Efficiencysgt_invictus100% (1)

- Sap Fico TutorialDocument7 pagesSap Fico TutorialgirirajNo ratings yet