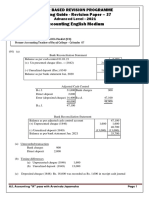

BRS

BRS

You might also like

- Bank Reconciliations PROBLEMS With Solutions PDFDocument5 pagesBank Reconciliations PROBLEMS With Solutions PDFlei vera80% (5)

- FAR - 02 LOANS AND RECEIVABLES With AnswerDocument17 pagesFAR - 02 LOANS AND RECEIVABLES With AnswerAndrei Nicole Mendoza Rivera91% (11)

- Reviewer Intacc 1n2Document58 pagesReviewer Intacc 1n2John100% (1)

- Audit of Cash PDFDocument3 pagesAudit of Cash PDFVincent SampianoNo ratings yet

- Astm E2352 - 1 (En) PDFDocument14 pagesAstm E2352 - 1 (En) PDFSainath AmudaNo ratings yet

- Chapter 9 - Bank Reconciliation StatementDocument15 pagesChapter 9 - Bank Reconciliation StatementSaurabh GohanNo ratings yet

- Additional Illustrations-14Document8 pagesAdditional Illustrations-14Gulneer LambaNo ratings yet

- Adobe Scan 05 Jan 2024Document2 pagesAdobe Scan 05 Jan 2024Harshit GargNo ratings yet

- Bank Reconciliation QuestionsDocument14 pagesBank Reconciliation Questionsanga100% (1)

- (03B) Cash SPECIAL Quiz ANSWER KEYDocument6 pages(03B) Cash SPECIAL Quiz ANSWER KEYGabriel Adrian ObungenNo ratings yet

- BANK RECONCILIATION 2Document4 pagesBANK RECONCILIATION 2Cornelius Chiko MwansaNo ratings yet

- Sessional 2 Solved Sample 3Document4 pagesSessional 2 Solved Sample 3Fami FamzNo ratings yet

- RKG Accounts (XI) CH 9 To 16 SolDocument3 pagesRKG Accounts (XI) CH 9 To 16 SolJohn WickNo ratings yet

- Finac Nov 2017Document5 pagesFinac Nov 2017Amanda Hove HoveNo ratings yet

- P6Document15 pagesP6lakshmananrm2005No ratings yet

- Assignment Pmis 115 Accounting Fundamnental 2 2023Document3 pagesAssignment Pmis 115 Accounting Fundamnental 2 2023stayinmyhome0828No ratings yet

- Fa07 Student Q&ADocument26 pagesFa07 Student Q&AtimothyNo ratings yet

- Cashew ProblemDocument2 pagesCashew ProblemJoyNo ratings yet

- Bank Reconcilaition Statement Problems PDF 1 4 PDFDocument4 pagesBank Reconcilaition Statement Problems PDF 1 4 PDFHakim JanNo ratings yet

- Chapter 9Document7 pagesChapter 9Saharin Islam ShakibNo ratings yet

- HuhnunjnDocument2 pagesHuhnunjnAnne VinuyaNo ratings yet

- MTP-1 (Solutions (QR Code) )Document13 pagesMTP-1 (Solutions (QR Code) )ajay.007.sngNo ratings yet

- Chapter 7 Correction of Errors (II) TestDocument6 pagesChapter 7 Correction of Errors (II) Test陳韋佳No ratings yet

- FAR - CASH ProbDocument2 pagesFAR - CASH Prob2216391No ratings yet

- LB301 2017 08Document4 pagesLB301 2017 08Clayton MutsenekiNo ratings yet

- Bank ReconciliationDocument6 pagesBank ReconciliationXienaNo ratings yet

- Accounts Sample Paper 03 0253b13dc89ddDocument25 pagesAccounts Sample Paper 03 0253b13dc89ddPalashNo ratings yet

- Paper2 Set1 SolutionDocument5 pagesPaper2 Set1 Solutionadityatiwari122006No ratings yet

- Jagjeet NotesDocument12 pagesJagjeet NotesPawan TalrejaNo ratings yet

- Bank Reconciliation Statement: Gravity 4 CaDocument13 pagesBank Reconciliation Statement: Gravity 4 CaAmit ChaudhryNo ratings yet

- Mudio Islamic Examination Board (Mieb)Document5 pagesMudio Islamic Examination Board (Mieb)MmaryNo ratings yet

- BRS PDFDocument8 pagesBRS PDFAnshumanNo ratings yet

- Bank Reconciliation StatementDocument9 pagesBank Reconciliation StatementMarvin tvNo ratings yet

- Chap 3 PDFDocument8 pagesChap 3 PDFJohanna VidadNo ratings yet

- Examination Question and Answers, Set C (Problem Solving), Chapter 2 - Analyzing TransactionsDocument3 pagesExamination Question and Answers, Set C (Problem Solving), Chapter 2 - Analyzing TransactionsJohn Carlos DoringoNo ratings yet

- AIS Prelim ExamDocument4 pagesAIS Prelim Examsharielles /No ratings yet

- AP - Quiz 01 (UCP)Document8 pagesAP - Quiz 01 (UCP)CrestinaNo ratings yet

- Samplepractice Exam 15 October 2020 Questions and AnswersDocument6 pagesSamplepractice Exam 15 October 2020 Questions and AnswersMartha Nicole MaristelaNo ratings yet

- Quiz 1Document3 pagesQuiz 1Van MateoNo ratings yet

- Particulars: Rs. RsDocument7 pagesParticulars: Rs. RsAnmol ChawlaNo ratings yet

- Examination Question and Answers, Set B (Problem Solving), Chapter 2 - Analyzing TransactionsDocument4 pagesExamination Question and Answers, Set B (Problem Solving), Chapter 2 - Analyzing TransactionsJohn Carlos DoringoNo ratings yet

- Accounting English Medium: Paper Based Revision Programme Marking Guide - Revision Paper - 37Document6 pagesAccounting English Medium: Paper Based Revision Programme Marking Guide - Revision Paper - 37Malar SrirengarajahNo ratings yet

- CA Foundation Accounts A MTP 2 June 2023Document12 pagesCA Foundation Accounts A MTP 2 June 2023Vranda RastogiNo ratings yet

- Cash Book (Bank Column)Document6 pagesCash Book (Bank Column)batmam7589No ratings yet

- Answer Key To Bank Reconciliation Statement 14-12-2021Document53 pagesAnswer Key To Bank Reconciliation Statement 14-12-2021Abdelkadr NurhisenNo ratings yet

- RTP Accounting CA Foundation May 18Document35 pagesRTP Accounting CA Foundation May 18kanishk bahetiNo ratings yet

- Unit 8 Bank Reconciliation StatementDocument7 pagesUnit 8 Bank Reconciliation StatementUrja JoshiNo ratings yet

- BoardPaper 2019 SolutionsDocument7 pagesBoardPaper 2019 Solutionskartik 011No ratings yet

- Paper - 2 - Answer - E - NormalDocument191 pagesPaper - 2 - Answer - E - NormalJhianne Mae AlbagNo ratings yet

- Accounts Class 12Document167 pagesAccounts Class 12Utkarsh Navandar100% (1)

- Frank AccDocument6 pagesFrank AccJoseph NjovuNo ratings yet

- SolutionDocument23 pagesSolutionKavita WadhwaNo ratings yet

- Applied Auditing-Prelim FinalDocument3 pagesApplied Auditing-Prelim FinalDominic E. BoticarioNo ratings yet

- DBM 611 Financial AccountingDocument3 pagesDBM 611 Financial AccountingCollins AbereNo ratings yet

- 4.CA Foundation Test 4Document6 pages4.CA Foundation Test 4Nived Narayan PNo ratings yet

- Bos 28432 CP 10Document45 pagesBos 28432 CP 10hiral dattaniNo ratings yet

- 07 Correction of Errors (II)Document16 pages07 Correction of Errors (II)Babamu Kalmoni JaatoNo ratings yet

- BRS SCANNER by Nahta PDFDocument24 pagesBRS SCANNER by Nahta PDFVaidika JainNo ratings yet

- Suggested Answers PSPM AA015 2021Document9 pagesSuggested Answers PSPM AA015 2021Shiela shiniNo ratings yet

- Admission_of_a_PartnerDocument21 pagesAdmission_of_a_Partnerrenu bhattNo ratings yet

- Icest2030 AzureDocument4 pagesIcest2030 AzureJorge RoblesNo ratings yet

- E W Hildick - (McGurk Mystery 05) - The Case of The Invisible Dog (siPDF) PDFDocument132 pagesE W Hildick - (McGurk Mystery 05) - The Case of The Invisible Dog (siPDF) PDFTheAsh2No ratings yet

- Computational Intelligence and Financial Markets - A Survey and Future DirectionsDocument18 pagesComputational Intelligence and Financial Markets - A Survey and Future DirectionsMarcus ViniciusNo ratings yet

- Bahasa Inggris Lawang SewuDocument12 pagesBahasa Inggris Lawang Sewuaisyah100% (1)

- Common Service Data Model (CSDM) 3.0 White PaperDocument31 pagesCommon Service Data Model (CSDM) 3.0 White PaperЕвгения МазинаNo ratings yet

- शरीर में सन्निहित शक्ति-केंद्र या चक्र Inner Powers Center or Chakra in BodyDocument33 pagesशरीर में सन्निहित शक्ति-केंद्र या चक्र Inner Powers Center or Chakra in BodygujjuNo ratings yet

- Brainy kl7 Unit Test 7 CDocument5 pagesBrainy kl7 Unit Test 7 CMateusz NochNo ratings yet

- Nokia: Management of SmesDocument32 pagesNokia: Management of SmesSimone SantosNo ratings yet

- Diy Direct Drive WheelDocument10 pagesDiy Direct Drive WheelBrad PortelliNo ratings yet

- Anh Văn Chuyên NgànhDocument7 pagesAnh Văn Chuyên Ngành19150004No ratings yet

- It Is Better For Children To Grow Up in The Countryside Than in A Big City. To What Extend Do You Agree or Disagree?Document2 pagesIt Is Better For Children To Grow Up in The Countryside Than in A Big City. To What Extend Do You Agree or Disagree?Lê Hữu ĐạtNo ratings yet

- NY B32 Fire Tape 2A FDR - Entire Contents - Transcript - 911 Calls 381Document82 pagesNY B32 Fire Tape 2A FDR - Entire Contents - Transcript - 911 Calls 3819/11 Document Archive100% (3)

- Views, Synonyms, and SequencesDocument46 pagesViews, Synonyms, and Sequencesprad15No ratings yet

- Midas - NFX - 2022R1 - Release NoteDocument10 pagesMidas - NFX - 2022R1 - Release NoteCristian Camilo Londoño PiedrahítaNo ratings yet

- Metro Starter Unit 5 Test A One StarDocument3 pagesMetro Starter Unit 5 Test A One StarTarik Kourad100% (1)

- SDocument8 pagesSdebate ddNo ratings yet

- Karens A-MDocument21 pagesKarens A-Mapi-291270075No ratings yet

- SSC Gr10 ICT Q4 Module 2 WK 2 - v.01-CC-released-7June2021Document16 pagesSSC Gr10 ICT Q4 Module 2 WK 2 - v.01-CC-released-7June2021Vj AleserNo ratings yet

- The Silt Verses - Chapter 21 TranscriptDocument32 pagesThe Silt Verses - Chapter 21 TranscriptVictória MoraesNo ratings yet

- PFW - Vol. 23, Issue 08 (August 18, 2008) Escape To New YorkDocument0 pagesPFW - Vol. 23, Issue 08 (August 18, 2008) Escape To New YorkskanzeniNo ratings yet

- Note On Geneva ConventionDocument12 pagesNote On Geneva ConventionRajesh JosephNo ratings yet

- ĐỀ 2Document4 pagesĐỀ 2Khôi Nguyên PhạmNo ratings yet

- Character Analysis of Lyubov Andreyevna RanevskayaDocument4 pagesCharacter Analysis of Lyubov Andreyevna RanevskayaAnnapurna V GNo ratings yet

- Group 1 Intro To TechnopreneurshipDocument22 pagesGroup 1 Intro To TechnopreneurshipMarshall james G. RamirezNo ratings yet

- Classification of Common Musical InstrumentsDocument3 pagesClassification of Common Musical InstrumentsFabian FebianoNo ratings yet

- Multiple Choice Questions:: SAARC Head QuarterDocument35 pagesMultiple Choice Questions:: SAARC Head QuarterQazi Sajjad Ul HassanNo ratings yet

- 0809 KarlsenDocument5 pages0809 KarlsenprateekbaldwaNo ratings yet

- Besmed Indonesia - Google SearchDocument1 pageBesmed Indonesia - Google SearchPelayanan ResusitasiNo ratings yet

- W6400 PC PDFDocument34 pagesW6400 PC PDFHùng TàiNo ratings yet

Download as docx, pdf, or txt

You might also like

- Bank Reconciliations PROBLEMS With Solutions PDFDocument5 pagesBank Reconciliations PROBLEMS With Solutions PDFlei vera80% (5)

- FAR - 02 LOANS AND RECEIVABLES With AnswerDocument17 pagesFAR - 02 LOANS AND RECEIVABLES With AnswerAndrei Nicole Mendoza Rivera91% (11)

- Reviewer Intacc 1n2Document58 pagesReviewer Intacc 1n2John100% (1)

- Audit of Cash PDFDocument3 pagesAudit of Cash PDFVincent SampianoNo ratings yet

- Astm E2352 - 1 (En) PDFDocument14 pagesAstm E2352 - 1 (En) PDFSainath AmudaNo ratings yet

- Chapter 9 - Bank Reconciliation StatementDocument15 pagesChapter 9 - Bank Reconciliation StatementSaurabh GohanNo ratings yet

- Additional Illustrations-14Document8 pagesAdditional Illustrations-14Gulneer LambaNo ratings yet

- Adobe Scan 05 Jan 2024Document2 pagesAdobe Scan 05 Jan 2024Harshit GargNo ratings yet

- Bank Reconciliation QuestionsDocument14 pagesBank Reconciliation Questionsanga100% (1)

- (03B) Cash SPECIAL Quiz ANSWER KEYDocument6 pages(03B) Cash SPECIAL Quiz ANSWER KEYGabriel Adrian ObungenNo ratings yet

- BANK RECONCILIATION 2Document4 pagesBANK RECONCILIATION 2Cornelius Chiko MwansaNo ratings yet

- Sessional 2 Solved Sample 3Document4 pagesSessional 2 Solved Sample 3Fami FamzNo ratings yet

- RKG Accounts (XI) CH 9 To 16 SolDocument3 pagesRKG Accounts (XI) CH 9 To 16 SolJohn WickNo ratings yet

- Finac Nov 2017Document5 pagesFinac Nov 2017Amanda Hove HoveNo ratings yet

- P6Document15 pagesP6lakshmananrm2005No ratings yet

- Assignment Pmis 115 Accounting Fundamnental 2 2023Document3 pagesAssignment Pmis 115 Accounting Fundamnental 2 2023stayinmyhome0828No ratings yet

- Fa07 Student Q&ADocument26 pagesFa07 Student Q&AtimothyNo ratings yet

- Cashew ProblemDocument2 pagesCashew ProblemJoyNo ratings yet

- Bank Reconcilaition Statement Problems PDF 1 4 PDFDocument4 pagesBank Reconcilaition Statement Problems PDF 1 4 PDFHakim JanNo ratings yet

- Chapter 9Document7 pagesChapter 9Saharin Islam ShakibNo ratings yet

- HuhnunjnDocument2 pagesHuhnunjnAnne VinuyaNo ratings yet

- MTP-1 (Solutions (QR Code) )Document13 pagesMTP-1 (Solutions (QR Code) )ajay.007.sngNo ratings yet

- Chapter 7 Correction of Errors (II) TestDocument6 pagesChapter 7 Correction of Errors (II) Test陳韋佳No ratings yet

- FAR - CASH ProbDocument2 pagesFAR - CASH Prob2216391No ratings yet

- LB301 2017 08Document4 pagesLB301 2017 08Clayton MutsenekiNo ratings yet

- Bank ReconciliationDocument6 pagesBank ReconciliationXienaNo ratings yet

- Accounts Sample Paper 03 0253b13dc89ddDocument25 pagesAccounts Sample Paper 03 0253b13dc89ddPalashNo ratings yet

- Paper2 Set1 SolutionDocument5 pagesPaper2 Set1 Solutionadityatiwari122006No ratings yet

- Jagjeet NotesDocument12 pagesJagjeet NotesPawan TalrejaNo ratings yet

- Bank Reconciliation Statement: Gravity 4 CaDocument13 pagesBank Reconciliation Statement: Gravity 4 CaAmit ChaudhryNo ratings yet

- Mudio Islamic Examination Board (Mieb)Document5 pagesMudio Islamic Examination Board (Mieb)MmaryNo ratings yet

- BRS PDFDocument8 pagesBRS PDFAnshumanNo ratings yet

- Bank Reconciliation StatementDocument9 pagesBank Reconciliation StatementMarvin tvNo ratings yet

- Chap 3 PDFDocument8 pagesChap 3 PDFJohanna VidadNo ratings yet

- Examination Question and Answers, Set C (Problem Solving), Chapter 2 - Analyzing TransactionsDocument3 pagesExamination Question and Answers, Set C (Problem Solving), Chapter 2 - Analyzing TransactionsJohn Carlos DoringoNo ratings yet

- AIS Prelim ExamDocument4 pagesAIS Prelim Examsharielles /No ratings yet

- AP - Quiz 01 (UCP)Document8 pagesAP - Quiz 01 (UCP)CrestinaNo ratings yet

- Samplepractice Exam 15 October 2020 Questions and AnswersDocument6 pagesSamplepractice Exam 15 October 2020 Questions and AnswersMartha Nicole MaristelaNo ratings yet

- Quiz 1Document3 pagesQuiz 1Van MateoNo ratings yet

- Particulars: Rs. RsDocument7 pagesParticulars: Rs. RsAnmol ChawlaNo ratings yet

- Examination Question and Answers, Set B (Problem Solving), Chapter 2 - Analyzing TransactionsDocument4 pagesExamination Question and Answers, Set B (Problem Solving), Chapter 2 - Analyzing TransactionsJohn Carlos DoringoNo ratings yet

- Accounting English Medium: Paper Based Revision Programme Marking Guide - Revision Paper - 37Document6 pagesAccounting English Medium: Paper Based Revision Programme Marking Guide - Revision Paper - 37Malar SrirengarajahNo ratings yet

- CA Foundation Accounts A MTP 2 June 2023Document12 pagesCA Foundation Accounts A MTP 2 June 2023Vranda RastogiNo ratings yet

- Cash Book (Bank Column)Document6 pagesCash Book (Bank Column)batmam7589No ratings yet

- Answer Key To Bank Reconciliation Statement 14-12-2021Document53 pagesAnswer Key To Bank Reconciliation Statement 14-12-2021Abdelkadr NurhisenNo ratings yet

- RTP Accounting CA Foundation May 18Document35 pagesRTP Accounting CA Foundation May 18kanishk bahetiNo ratings yet

- Unit 8 Bank Reconciliation StatementDocument7 pagesUnit 8 Bank Reconciliation StatementUrja JoshiNo ratings yet

- BoardPaper 2019 SolutionsDocument7 pagesBoardPaper 2019 Solutionskartik 011No ratings yet

- Paper - 2 - Answer - E - NormalDocument191 pagesPaper - 2 - Answer - E - NormalJhianne Mae AlbagNo ratings yet

- Accounts Class 12Document167 pagesAccounts Class 12Utkarsh Navandar100% (1)

- Frank AccDocument6 pagesFrank AccJoseph NjovuNo ratings yet

- SolutionDocument23 pagesSolutionKavita WadhwaNo ratings yet

- Applied Auditing-Prelim FinalDocument3 pagesApplied Auditing-Prelim FinalDominic E. BoticarioNo ratings yet

- DBM 611 Financial AccountingDocument3 pagesDBM 611 Financial AccountingCollins AbereNo ratings yet

- 4.CA Foundation Test 4Document6 pages4.CA Foundation Test 4Nived Narayan PNo ratings yet

- Bos 28432 CP 10Document45 pagesBos 28432 CP 10hiral dattaniNo ratings yet

- 07 Correction of Errors (II)Document16 pages07 Correction of Errors (II)Babamu Kalmoni JaatoNo ratings yet

- BRS SCANNER by Nahta PDFDocument24 pagesBRS SCANNER by Nahta PDFVaidika JainNo ratings yet

- Suggested Answers PSPM AA015 2021Document9 pagesSuggested Answers PSPM AA015 2021Shiela shiniNo ratings yet

- Admission_of_a_PartnerDocument21 pagesAdmission_of_a_Partnerrenu bhattNo ratings yet

- Icest2030 AzureDocument4 pagesIcest2030 AzureJorge RoblesNo ratings yet

- E W Hildick - (McGurk Mystery 05) - The Case of The Invisible Dog (siPDF) PDFDocument132 pagesE W Hildick - (McGurk Mystery 05) - The Case of The Invisible Dog (siPDF) PDFTheAsh2No ratings yet

- Computational Intelligence and Financial Markets - A Survey and Future DirectionsDocument18 pagesComputational Intelligence and Financial Markets - A Survey and Future DirectionsMarcus ViniciusNo ratings yet

- Bahasa Inggris Lawang SewuDocument12 pagesBahasa Inggris Lawang Sewuaisyah100% (1)

- Common Service Data Model (CSDM) 3.0 White PaperDocument31 pagesCommon Service Data Model (CSDM) 3.0 White PaperЕвгения МазинаNo ratings yet

- शरीर में सन्निहित शक्ति-केंद्र या चक्र Inner Powers Center or Chakra in BodyDocument33 pagesशरीर में सन्निहित शक्ति-केंद्र या चक्र Inner Powers Center or Chakra in BodygujjuNo ratings yet

- Brainy kl7 Unit Test 7 CDocument5 pagesBrainy kl7 Unit Test 7 CMateusz NochNo ratings yet

- Nokia: Management of SmesDocument32 pagesNokia: Management of SmesSimone SantosNo ratings yet

- Diy Direct Drive WheelDocument10 pagesDiy Direct Drive WheelBrad PortelliNo ratings yet

- Anh Văn Chuyên NgànhDocument7 pagesAnh Văn Chuyên Ngành19150004No ratings yet

- It Is Better For Children To Grow Up in The Countryside Than in A Big City. To What Extend Do You Agree or Disagree?Document2 pagesIt Is Better For Children To Grow Up in The Countryside Than in A Big City. To What Extend Do You Agree or Disagree?Lê Hữu ĐạtNo ratings yet

- NY B32 Fire Tape 2A FDR - Entire Contents - Transcript - 911 Calls 381Document82 pagesNY B32 Fire Tape 2A FDR - Entire Contents - Transcript - 911 Calls 3819/11 Document Archive100% (3)

- Views, Synonyms, and SequencesDocument46 pagesViews, Synonyms, and Sequencesprad15No ratings yet

- Midas - NFX - 2022R1 - Release NoteDocument10 pagesMidas - NFX - 2022R1 - Release NoteCristian Camilo Londoño PiedrahítaNo ratings yet

- Metro Starter Unit 5 Test A One StarDocument3 pagesMetro Starter Unit 5 Test A One StarTarik Kourad100% (1)

- SDocument8 pagesSdebate ddNo ratings yet

- Karens A-MDocument21 pagesKarens A-Mapi-291270075No ratings yet

- SSC Gr10 ICT Q4 Module 2 WK 2 - v.01-CC-released-7June2021Document16 pagesSSC Gr10 ICT Q4 Module 2 WK 2 - v.01-CC-released-7June2021Vj AleserNo ratings yet

- The Silt Verses - Chapter 21 TranscriptDocument32 pagesThe Silt Verses - Chapter 21 TranscriptVictória MoraesNo ratings yet

- PFW - Vol. 23, Issue 08 (August 18, 2008) Escape To New YorkDocument0 pagesPFW - Vol. 23, Issue 08 (August 18, 2008) Escape To New YorkskanzeniNo ratings yet

- Note On Geneva ConventionDocument12 pagesNote On Geneva ConventionRajesh JosephNo ratings yet

- ĐỀ 2Document4 pagesĐỀ 2Khôi Nguyên PhạmNo ratings yet

- Character Analysis of Lyubov Andreyevna RanevskayaDocument4 pagesCharacter Analysis of Lyubov Andreyevna RanevskayaAnnapurna V GNo ratings yet

- Group 1 Intro To TechnopreneurshipDocument22 pagesGroup 1 Intro To TechnopreneurshipMarshall james G. RamirezNo ratings yet

- Classification of Common Musical InstrumentsDocument3 pagesClassification of Common Musical InstrumentsFabian FebianoNo ratings yet

- Multiple Choice Questions:: SAARC Head QuarterDocument35 pagesMultiple Choice Questions:: SAARC Head QuarterQazi Sajjad Ul HassanNo ratings yet

- 0809 KarlsenDocument5 pages0809 KarlsenprateekbaldwaNo ratings yet

- Besmed Indonesia - Google SearchDocument1 pageBesmed Indonesia - Google SearchPelayanan ResusitasiNo ratings yet

- W6400 PC PDFDocument34 pagesW6400 PC PDFHùng TàiNo ratings yet