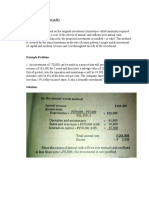

Super Project Slides

Super Project Slides

You might also like

- 2024 Becker CPA Financial (FAR) NotesDocument51 pages2024 Becker CPA Financial (FAR) Notescraigsappletree100% (4)

- Capital Budgeting Sums-Doc For PDF (Encrypted)Document7 pagesCapital Budgeting Sums-Doc For PDF (Encrypted)Prasad GharatNo ratings yet

- SuperDocument30 pagesSuperAbhishek TiwariNo ratings yet

- BUAD 839 ASSIGNMENT (Group F)Document4 pagesBUAD 839 ASSIGNMENT (Group F)Yemi Jonathan OlusholaNo ratings yet

- Tire City SlidesDocument8 pagesTire City Slidesp23ayushsNo ratings yet

- The Basics of Capital Budgeting: Evaluating Cash Flows: Should We Build This Plant?Document41 pagesThe Basics of Capital Budgeting: Evaluating Cash Flows: Should We Build This Plant?Vaishali GuptaNo ratings yet

- Capital BudgetingDocument108 pagesCapital Budgetingdhanraj_aartiNo ratings yet

- FM L6 7 Investment RevDocument27 pagesFM L6 7 Investment RevANJALI SHARMANo ratings yet

- Capital BudgetingDocument18 pagesCapital BudgetingNilesh SondigalaNo ratings yet

- Capital Budgeting Techniques: Prof. Nidhi BandaruDocument28 pagesCapital Budgeting Techniques: Prof. Nidhi Bandaruhashmi4a4No ratings yet

- MBA Finance FAQsDocument2 pagesMBA Finance FAQsTosin GeorgeNo ratings yet

- Unit 5 Capital Budgeting TechniquesDocument37 pagesUnit 5 Capital Budgeting Techniquesayaankhan2307sreNo ratings yet

- Evaluating Business and Engineering Assets II: The Annual Worth Method and The Rate-of-ReturnDocument25 pagesEvaluating Business and Engineering Assets II: The Annual Worth Method and The Rate-of-ReturnJane Erestain BuenaobraNo ratings yet

- The AW Method and IRR Method (Week 9)Document4 pagesThe AW Method and IRR Method (Week 9)raymond moscosoNo ratings yet

- Capital Budgeting: Should We Build This Plant?Document33 pagesCapital Budgeting: Should We Build This Plant?Bhuvan SemwalNo ratings yet

- Economic Analysis For RoboticsDocument15 pagesEconomic Analysis For RoboticsAman SharmaNo ratings yet

- Chapter 9 Profitability Part 1Document13 pagesChapter 9 Profitability Part 1Subhadeep ChakrabartiNo ratings yet

- ITC CaseDocument5 pagesITC CaseAbhijeet GangulyNo ratings yet

- Internal Rate of ReturnDocument28 pagesInternal Rate of ReturnVaidyanathan Ravichandran100% (1)

- Techniques of Capital Budgeting: Investment Evaluation CriteriaDocument29 pagesTechniques of Capital Budgeting: Investment Evaluation CriteriaNaitik ModiNo ratings yet

- Assignment On FaseelDocument6 pagesAssignment On FaseelAbdul KhanNo ratings yet

- 03 - 20th Aug Capital Budgeting, 2019Document37 pages03 - 20th Aug Capital Budgeting, 2019anujNo ratings yet

- Incremental AnalysisDocument25 pagesIncremental AnalysisAngel MallariNo ratings yet

- Project Appraisal - Investment Appraisal - 2023Document40 pagesProject Appraisal - Investment Appraisal - 2023ThaboNo ratings yet

- Accounting 9th Edition Horngren Solution ManualDocument19 pagesAccounting 9th Edition Horngren Solution ManualAsa100% (1)

- Risk in Capital BudgetingDocument18 pagesRisk in Capital BudgetingHaresh VermaNo ratings yet

- Methods of Project AppraisalDocument28 pagesMethods of Project AppraisalMîñåk ŞhïïNo ratings yet

- Appraisal Criteria - Capital BudgetingDocument50 pagesAppraisal Criteria - Capital BudgetingNitesh NagdevNo ratings yet

- Chapter - 8: Capital Budgeting DecisionsDocument45 pagesChapter - 8: Capital Budgeting DecisionsNirmal ThomasNo ratings yet

- Financial Analysis: Alka Assistant Director Power System Training Institute BangaloreDocument40 pagesFinancial Analysis: Alka Assistant Director Power System Training Institute Bangaloregaurang1111No ratings yet

- Capital Budgeting A Nice Finance Topic Helpful For Mba and Bba StudentsDocument39 pagesCapital Budgeting A Nice Finance Topic Helpful For Mba and Bba StudentsNimish KumarNo ratings yet

- Investment Appraisal and NPV AnalysisDocument4 pagesInvestment Appraisal and NPV Analysistran thanhNo ratings yet

- Economic PrinciplesDocument9 pagesEconomic PrinciplesLindsay BakerNo ratings yet

- Capital BudgetingDocument49 pagesCapital Budgetingthkrarun100No ratings yet

- Net Present Value and Other Investment CriteriaDocument23 pagesNet Present Value and Other Investment CriteriaHanniel Madramootoo100% (1)

- Profitability AnalysisDocument43 pagesProfitability AnalysisAvinash Iyer100% (1)

- 29th Aug 2023 Final Complex Investment DecisionsDocument15 pages29th Aug 2023 Final Complex Investment DecisionsKunal KadamNo ratings yet

- CIMA Paper P1: NotesDocument3 pagesCIMA Paper P1: NotesSajid AliNo ratings yet

- Profitabilty. AnalysisDocument35 pagesProfitabilty. AnalysisSidharth RazdanNo ratings yet

- Unwinding of DiscountDocument5 pagesUnwinding of Discountlavanya sNo ratings yet

- Capital Budgeting: Kiran ThapaDocument34 pagesCapital Budgeting: Kiran ThapaRajesh ShresthaNo ratings yet

- CH - 08 Cap BudgetingDocument54 pagesCH - 08 Cap BudgetingfoglaabhishekNo ratings yet

- Incremental AnalysisDocument25 pagesIncremental AnalysisMobin NasimNo ratings yet

- Rate of Return CalculationsDocument37 pagesRate of Return CalculationsSrushti MNo ratings yet

- Capital Budgeting - Adv IssuesDocument21 pagesCapital Budgeting - Adv IssuesdixitBhavak DixitNo ratings yet

- Capital Budgeting: BA 217: Financial ManagementDocument46 pagesCapital Budgeting: BA 217: Financial ManagementyanaNo ratings yet

- Incremental AnalysisDocument25 pagesIncremental AnalysisDejene HailuNo ratings yet

- Financial StatementDocument54 pagesFinancial StatementAlvin FelicianoNo ratings yet

- Capital BudgetingDocument30 pagesCapital BudgetingUmesh ChandraNo ratings yet

- Efa-Unit 5Document45 pagesEfa-Unit 5mandavillinagavenkatasriNo ratings yet

- Capital Budgeting - I: Gourav Vallabh Xlri JamshedpurDocument64 pagesCapital Budgeting - I: Gourav Vallabh Xlri JamshedpurSimran JainNo ratings yet

- Measuring Investment Returns: Stern School of BusinessDocument139 pagesMeasuring Investment Returns: Stern School of Businesssuhasshinde88No ratings yet

- Capital Budgeting 30032010Document18 pagesCapital Budgeting 30032010kkv_phani_varma5396No ratings yet

- FM Mod II-2Document10 pagesFM Mod II-2Irfanu NisaNo ratings yet

- Capitall Budgeting Unit 2Document70 pagesCapitall Budgeting Unit 2kdxpro22No ratings yet

- Capital BudgetingDocument6 pagesCapital BudgetingHannahbea LindoNo ratings yet

- Capital BudgetingDocument42 pagesCapital BudgetingPiyush ChitlangiaNo ratings yet

- 9 Capital BudgetingDocument6 pages9 Capital BudgetingRavichandran SeenivasanNo ratings yet

- Applied Corporate Finance. What is a Company worth?From EverandApplied Corporate Finance. What is a Company worth?Rating: 3 out of 5 stars3/5 (2)

- Sip ReportDocument52 pagesSip ReportRavi JoshiNo ratings yet

- 2024 GIO - APAC Report - Final - CompressedDocument24 pages2024 GIO - APAC Report - Final - Compressedbotoy26No ratings yet

- Komal SharmaDocument34 pagesKomal SharmaVini Balot0% (1)

- Financial Risk ND ProfitabilityDocument22 pagesFinancial Risk ND Profitabilitytungeena waseemNo ratings yet

- 18.functions of Commercial BanksDocument15 pages18.functions of Commercial BanksPraneeth KumarNo ratings yet

- This Study Resource Was: FinanceDocument4 pagesThis Study Resource Was: FinanceSIDDHARTH SETHI-DM 21DM198No ratings yet

- Transcript Orsted Q3 2023Document25 pagesTranscript Orsted Q3 2023shen.wangNo ratings yet

- Construction Sector Update - 141013Document32 pagesConstruction Sector Update - 141013Pinaki RoychowdhuryNo ratings yet

- Performance of Indian IPOs Listed in 2021Document11 pagesPerformance of Indian IPOs Listed in 2021REGI MEMANA VARUGHESENo ratings yet

- IsleX - Global Digital Liquidity (Presentation - Deck)Document26 pagesIsleX - Global Digital Liquidity (Presentation - Deck)Brian NiessenNo ratings yet

- Quotation: Syarikat Takaful Malaysia Keluarga Berhad (Head OfficeDocument5 pagesQuotation: Syarikat Takaful Malaysia Keluarga Berhad (Head OfficeakmabushNo ratings yet

- Lesson 3A. Investment On Securities - Please PrintDocument13 pagesLesson 3A. Investment On Securities - Please PrintHail DeityNo ratings yet

- Plumbing Arithmetic EconomyDocument9 pagesPlumbing Arithmetic EconomyAngelo Lirio InsigneNo ratings yet

- NPV and IRRDocument2 pagesNPV and IRRsaadhashmi97No ratings yet

- HW2 QDocument6 pagesHW2 Qtranthithanhhuong25110211No ratings yet

- Working CapitalDocument107 pagesWorking CapitalGanesh Nikhil100% (1)

- DK Goel Solutions Class 11 Accountancy Chapter 23 - Accounts From Incomplete RecordsDocument67 pagesDK Goel Solutions Class 11 Accountancy Chapter 23 - Accounts From Incomplete RecordsPython The SnakeNo ratings yet

- CapitalGain Summary Report - 1658151067650 - 11Document1 pageCapitalGain Summary Report - 1658151067650 - 11honey mittalNo ratings yet

- Dr. Ashfak ShikalgarDocument4 pagesDr. Ashfak Shikalgarravikiran1955No ratings yet

- TMFB TSC 2012 Prospectus PDFDocument83 pagesTMFB TSC 2012 Prospectus PDFMehboobElaheiNo ratings yet

- BUSANA1 Chapter 1: Simple Interest & Simple DiscountDocument28 pagesBUSANA1 Chapter 1: Simple Interest & Simple Discount7 bit88% (16)

- Inclusive Digital Financial Services A Reference Guide For RegulatorsDocument262 pagesInclusive Digital Financial Services A Reference Guide For Regulatorsunknown4080No ratings yet

- VXV DY23 LCD 47 C QGDocument2 pagesVXV DY23 LCD 47 C QGhp34thNo ratings yet

- AFM476 - Risk and Real OptionsDocument4 pagesAFM476 - Risk and Real OptionsJonah HuNo ratings yet

- Financial Manager: Typical Work ActivitiesDocument5 pagesFinancial Manager: Typical Work ActivitiesMansi ChughNo ratings yet

- 108A W23++Homework+8Document8 pages108A W23++Homework+8Julius SuhermanNo ratings yet

- Steen Stress IndicatorsDocument13 pagesSteen Stress IndicatorsZerohedgeNo ratings yet

- Terms and Conditions Person CustomerDocument40 pagesTerms and Conditions Person CustomerFotos LibresNo ratings yet

- Accounting Standards: Sub: Financial Reporting & AnalysisDocument13 pagesAccounting Standards: Sub: Financial Reporting & AnalysisDevasaya MitraNo ratings yet

Download as pdf or txt

You might also like

- 2024 Becker CPA Financial (FAR) NotesDocument51 pages2024 Becker CPA Financial (FAR) Notescraigsappletree100% (4)

- Capital Budgeting Sums-Doc For PDF (Encrypted)Document7 pagesCapital Budgeting Sums-Doc For PDF (Encrypted)Prasad GharatNo ratings yet

- SuperDocument30 pagesSuperAbhishek TiwariNo ratings yet

- BUAD 839 ASSIGNMENT (Group F)Document4 pagesBUAD 839 ASSIGNMENT (Group F)Yemi Jonathan OlusholaNo ratings yet

- Tire City SlidesDocument8 pagesTire City Slidesp23ayushsNo ratings yet

- The Basics of Capital Budgeting: Evaluating Cash Flows: Should We Build This Plant?Document41 pagesThe Basics of Capital Budgeting: Evaluating Cash Flows: Should We Build This Plant?Vaishali GuptaNo ratings yet

- Capital BudgetingDocument108 pagesCapital Budgetingdhanraj_aartiNo ratings yet

- FM L6 7 Investment RevDocument27 pagesFM L6 7 Investment RevANJALI SHARMANo ratings yet

- Capital BudgetingDocument18 pagesCapital BudgetingNilesh SondigalaNo ratings yet

- Capital Budgeting Techniques: Prof. Nidhi BandaruDocument28 pagesCapital Budgeting Techniques: Prof. Nidhi Bandaruhashmi4a4No ratings yet

- MBA Finance FAQsDocument2 pagesMBA Finance FAQsTosin GeorgeNo ratings yet

- Unit 5 Capital Budgeting TechniquesDocument37 pagesUnit 5 Capital Budgeting Techniquesayaankhan2307sreNo ratings yet

- Evaluating Business and Engineering Assets II: The Annual Worth Method and The Rate-of-ReturnDocument25 pagesEvaluating Business and Engineering Assets II: The Annual Worth Method and The Rate-of-ReturnJane Erestain BuenaobraNo ratings yet

- The AW Method and IRR Method (Week 9)Document4 pagesThe AW Method and IRR Method (Week 9)raymond moscosoNo ratings yet

- Capital Budgeting: Should We Build This Plant?Document33 pagesCapital Budgeting: Should We Build This Plant?Bhuvan SemwalNo ratings yet

- Economic Analysis For RoboticsDocument15 pagesEconomic Analysis For RoboticsAman SharmaNo ratings yet

- Chapter 9 Profitability Part 1Document13 pagesChapter 9 Profitability Part 1Subhadeep ChakrabartiNo ratings yet

- ITC CaseDocument5 pagesITC CaseAbhijeet GangulyNo ratings yet

- Internal Rate of ReturnDocument28 pagesInternal Rate of ReturnVaidyanathan Ravichandran100% (1)

- Techniques of Capital Budgeting: Investment Evaluation CriteriaDocument29 pagesTechniques of Capital Budgeting: Investment Evaluation CriteriaNaitik ModiNo ratings yet

- Assignment On FaseelDocument6 pagesAssignment On FaseelAbdul KhanNo ratings yet

- 03 - 20th Aug Capital Budgeting, 2019Document37 pages03 - 20th Aug Capital Budgeting, 2019anujNo ratings yet

- Incremental AnalysisDocument25 pagesIncremental AnalysisAngel MallariNo ratings yet

- Project Appraisal - Investment Appraisal - 2023Document40 pagesProject Appraisal - Investment Appraisal - 2023ThaboNo ratings yet

- Accounting 9th Edition Horngren Solution ManualDocument19 pagesAccounting 9th Edition Horngren Solution ManualAsa100% (1)

- Risk in Capital BudgetingDocument18 pagesRisk in Capital BudgetingHaresh VermaNo ratings yet

- Methods of Project AppraisalDocument28 pagesMethods of Project AppraisalMîñåk ŞhïïNo ratings yet

- Appraisal Criteria - Capital BudgetingDocument50 pagesAppraisal Criteria - Capital BudgetingNitesh NagdevNo ratings yet

- Chapter - 8: Capital Budgeting DecisionsDocument45 pagesChapter - 8: Capital Budgeting DecisionsNirmal ThomasNo ratings yet

- Financial Analysis: Alka Assistant Director Power System Training Institute BangaloreDocument40 pagesFinancial Analysis: Alka Assistant Director Power System Training Institute Bangaloregaurang1111No ratings yet

- Capital Budgeting A Nice Finance Topic Helpful For Mba and Bba StudentsDocument39 pagesCapital Budgeting A Nice Finance Topic Helpful For Mba and Bba StudentsNimish KumarNo ratings yet

- Investment Appraisal and NPV AnalysisDocument4 pagesInvestment Appraisal and NPV Analysistran thanhNo ratings yet

- Economic PrinciplesDocument9 pagesEconomic PrinciplesLindsay BakerNo ratings yet

- Capital BudgetingDocument49 pagesCapital Budgetingthkrarun100No ratings yet

- Net Present Value and Other Investment CriteriaDocument23 pagesNet Present Value and Other Investment CriteriaHanniel Madramootoo100% (1)

- Profitability AnalysisDocument43 pagesProfitability AnalysisAvinash Iyer100% (1)

- 29th Aug 2023 Final Complex Investment DecisionsDocument15 pages29th Aug 2023 Final Complex Investment DecisionsKunal KadamNo ratings yet

- CIMA Paper P1: NotesDocument3 pagesCIMA Paper P1: NotesSajid AliNo ratings yet

- Profitabilty. AnalysisDocument35 pagesProfitabilty. AnalysisSidharth RazdanNo ratings yet

- Unwinding of DiscountDocument5 pagesUnwinding of Discountlavanya sNo ratings yet

- Capital Budgeting: Kiran ThapaDocument34 pagesCapital Budgeting: Kiran ThapaRajesh ShresthaNo ratings yet

- CH - 08 Cap BudgetingDocument54 pagesCH - 08 Cap BudgetingfoglaabhishekNo ratings yet

- Incremental AnalysisDocument25 pagesIncremental AnalysisMobin NasimNo ratings yet

- Rate of Return CalculationsDocument37 pagesRate of Return CalculationsSrushti MNo ratings yet

- Capital Budgeting - Adv IssuesDocument21 pagesCapital Budgeting - Adv IssuesdixitBhavak DixitNo ratings yet

- Capital Budgeting: BA 217: Financial ManagementDocument46 pagesCapital Budgeting: BA 217: Financial ManagementyanaNo ratings yet

- Incremental AnalysisDocument25 pagesIncremental AnalysisDejene HailuNo ratings yet

- Financial StatementDocument54 pagesFinancial StatementAlvin FelicianoNo ratings yet

- Capital BudgetingDocument30 pagesCapital BudgetingUmesh ChandraNo ratings yet

- Efa-Unit 5Document45 pagesEfa-Unit 5mandavillinagavenkatasriNo ratings yet

- Capital Budgeting - I: Gourav Vallabh Xlri JamshedpurDocument64 pagesCapital Budgeting - I: Gourav Vallabh Xlri JamshedpurSimran JainNo ratings yet

- Measuring Investment Returns: Stern School of BusinessDocument139 pagesMeasuring Investment Returns: Stern School of Businesssuhasshinde88No ratings yet

- Capital Budgeting 30032010Document18 pagesCapital Budgeting 30032010kkv_phani_varma5396No ratings yet

- FM Mod II-2Document10 pagesFM Mod II-2Irfanu NisaNo ratings yet

- Capitall Budgeting Unit 2Document70 pagesCapitall Budgeting Unit 2kdxpro22No ratings yet

- Capital BudgetingDocument6 pagesCapital BudgetingHannahbea LindoNo ratings yet

- Capital BudgetingDocument42 pagesCapital BudgetingPiyush ChitlangiaNo ratings yet

- 9 Capital BudgetingDocument6 pages9 Capital BudgetingRavichandran SeenivasanNo ratings yet

- Applied Corporate Finance. What is a Company worth?From EverandApplied Corporate Finance. What is a Company worth?Rating: 3 out of 5 stars3/5 (2)

- Sip ReportDocument52 pagesSip ReportRavi JoshiNo ratings yet

- 2024 GIO - APAC Report - Final - CompressedDocument24 pages2024 GIO - APAC Report - Final - Compressedbotoy26No ratings yet

- Komal SharmaDocument34 pagesKomal SharmaVini Balot0% (1)

- Financial Risk ND ProfitabilityDocument22 pagesFinancial Risk ND Profitabilitytungeena waseemNo ratings yet

- 18.functions of Commercial BanksDocument15 pages18.functions of Commercial BanksPraneeth KumarNo ratings yet

- This Study Resource Was: FinanceDocument4 pagesThis Study Resource Was: FinanceSIDDHARTH SETHI-DM 21DM198No ratings yet

- Transcript Orsted Q3 2023Document25 pagesTranscript Orsted Q3 2023shen.wangNo ratings yet

- Construction Sector Update - 141013Document32 pagesConstruction Sector Update - 141013Pinaki RoychowdhuryNo ratings yet

- Performance of Indian IPOs Listed in 2021Document11 pagesPerformance of Indian IPOs Listed in 2021REGI MEMANA VARUGHESENo ratings yet

- IsleX - Global Digital Liquidity (Presentation - Deck)Document26 pagesIsleX - Global Digital Liquidity (Presentation - Deck)Brian NiessenNo ratings yet

- Quotation: Syarikat Takaful Malaysia Keluarga Berhad (Head OfficeDocument5 pagesQuotation: Syarikat Takaful Malaysia Keluarga Berhad (Head OfficeakmabushNo ratings yet

- Lesson 3A. Investment On Securities - Please PrintDocument13 pagesLesson 3A. Investment On Securities - Please PrintHail DeityNo ratings yet

- Plumbing Arithmetic EconomyDocument9 pagesPlumbing Arithmetic EconomyAngelo Lirio InsigneNo ratings yet

- NPV and IRRDocument2 pagesNPV and IRRsaadhashmi97No ratings yet

- HW2 QDocument6 pagesHW2 Qtranthithanhhuong25110211No ratings yet

- Working CapitalDocument107 pagesWorking CapitalGanesh Nikhil100% (1)

- DK Goel Solutions Class 11 Accountancy Chapter 23 - Accounts From Incomplete RecordsDocument67 pagesDK Goel Solutions Class 11 Accountancy Chapter 23 - Accounts From Incomplete RecordsPython The SnakeNo ratings yet

- CapitalGain Summary Report - 1658151067650 - 11Document1 pageCapitalGain Summary Report - 1658151067650 - 11honey mittalNo ratings yet

- Dr. Ashfak ShikalgarDocument4 pagesDr. Ashfak Shikalgarravikiran1955No ratings yet

- TMFB TSC 2012 Prospectus PDFDocument83 pagesTMFB TSC 2012 Prospectus PDFMehboobElaheiNo ratings yet

- BUSANA1 Chapter 1: Simple Interest & Simple DiscountDocument28 pagesBUSANA1 Chapter 1: Simple Interest & Simple Discount7 bit88% (16)

- Inclusive Digital Financial Services A Reference Guide For RegulatorsDocument262 pagesInclusive Digital Financial Services A Reference Guide For Regulatorsunknown4080No ratings yet

- VXV DY23 LCD 47 C QGDocument2 pagesVXV DY23 LCD 47 C QGhp34thNo ratings yet

- AFM476 - Risk and Real OptionsDocument4 pagesAFM476 - Risk and Real OptionsJonah HuNo ratings yet

- Financial Manager: Typical Work ActivitiesDocument5 pagesFinancial Manager: Typical Work ActivitiesMansi ChughNo ratings yet

- 108A W23++Homework+8Document8 pages108A W23++Homework+8Julius SuhermanNo ratings yet

- Steen Stress IndicatorsDocument13 pagesSteen Stress IndicatorsZerohedgeNo ratings yet

- Terms and Conditions Person CustomerDocument40 pagesTerms and Conditions Person CustomerFotos LibresNo ratings yet

- Accounting Standards: Sub: Financial Reporting & AnalysisDocument13 pagesAccounting Standards: Sub: Financial Reporting & AnalysisDevasaya MitraNo ratings yet