2 Implications For Report - Nidge Company

2 Implications For Report - Nidge Company

You might also like

- Payroll (HR) RCM 2022-2023Document1 pagePayroll (HR) RCM 2022-2023Aman ParchaniNo ratings yet

- Implementing-Grc-Lines-Of-DefenseDocument1 pageImplementing-Grc-Lines-Of-DefensekeizersNo ratings yet

- 95051060-BRC-Food6-Checklist GDFGDocument27 pages95051060-BRC-Food6-Checklist GDFGAsep RNo ratings yet

- Change Management Routemap at ONE SLIDE PDFDocument1 pageChange Management Routemap at ONE SLIDE PDFAndrey PritulyukNo ratings yet

- QMS Process Interaction Diagram (WHOLE)Document1 pageQMS Process Interaction Diagram (WHOLE)Adil Abdulkhader100% (2)

- FSMS Process Interaction Diagram (WHOLE)Document1 pageFSMS Process Interaction Diagram (WHOLE)Adil AbdulkhaderNo ratings yet

- Audit ProcedureDocument1 pageAudit Procedurejay thakkarNo ratings yet

- MCQDocument36 pagesMCQMike AntolinoNo ratings yet

- CP 0n SLO in The Workplace-Lifting Plan - 6 Slides Per Page - R2Document6 pagesCP 0n SLO in The Workplace-Lifting Plan - 6 Slides Per Page - R2s_bharathkumarNo ratings yet

- SMETA Guidance Workflow AuditorsDocument1 pageSMETA Guidance Workflow AuditorsSam SmithNo ratings yet

- 5 Critical Appraisal - Kilminister, Taylo - SnipeDocument7 pages5 Critical Appraisal - Kilminister, Taylo - Snipesbracca1No ratings yet

- Enterprise Architecture As Capabilities ArchDocument24 pagesEnterprise Architecture As Capabilities ArchOsmo TechNo ratings yet

- DroneAcharya Financial Statements 2022 2023Document8 pagesDroneAcharya Financial Statements 2022 2023pradeep kumar pradeep kumarNo ratings yet

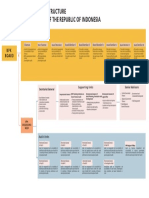

- Organizational Structure The Audit Board of The Republic of IndonesiaDocument1 pageOrganizational Structure The Audit Board of The Republic of IndonesiaFranz rumapeaNo ratings yet

- Revolve Project Audit: No. System Element Compliance Understanding Usage Action by WhenDocument16 pagesRevolve Project Audit: No. System Element Compliance Understanding Usage Action by WhenPatria ArdianNo ratings yet

- Year Clientcode A6 Time BudgetDocument1 pageYear Clientcode A6 Time BudgetReinnalyn UlandayNo ratings yet

- 03A Ic PartDocument19 pages03A Ic Partraghuraghu1490003No ratings yet

- Huye Branch - Risk Assessment - Fy 2022-2023 InspectionsDocument119 pagesHuye Branch - Risk Assessment - Fy 2022-2023 Inspectionsseth uwitonzeNo ratings yet

- Handle Handover Project To End UserDocument41 pagesHandle Handover Project To End UserSALAH HELLARANo ratings yet

- QMS Process Interaction To EditDocument1 pageQMS Process Interaction To EditAdil AbdulkhaderNo ratings yet

- HR Wheel PDCADocument1 pageHR Wheel PDCAMaria PatchinNo ratings yet

- Standalone Financial StatementsDocument39 pagesStandalone Financial StatementsLogan ThakurNo ratings yet

- Payables Work FlowDocument1 pagePayables Work FlowTruc ThanhNo ratings yet

- Topic 5Document1 pageTopic 5sofianasery28No ratings yet

- Nse Iar March 24Document42 pagesNse Iar March 24raju1204No ratings yet

- Audit Notes - 01Document19 pagesAudit Notes - 01JakeSiglerNo ratings yet

- Peer Recognition Program UpdatedDocument1 pagePeer Recognition Program UpdatedAudrey AyosoNo ratings yet

- SRS Brahmastra Notes_240505_193646Document9 pagesSRS Brahmastra Notes_240505_193646Sanjay AryalNo ratings yet

- BPM - TD Bank-3Document1 pageBPM - TD Bank-3frostbitexysNo ratings yet

- Chapter 24Document41 pagesChapter 24balibrea2011No ratings yet

- Close Customer PortfolioDocument1 pageClose Customer PortfolioRam Mohan MishraNo ratings yet

- Accounts Intro 3Document1 pageAccounts Intro 3manishchd81No ratings yet

- Performance Management BrokenDocument32 pagesPerformance Management BrokenJackNo ratings yet

- Audit Plan2020Document1 pageAudit Plan2020rebin azizNo ratings yet

- 25 - BC - AssetSMART-2.0-A-Tool-to-Assess-Your-Communitys-Asset-Management-PracticesDocument10 pages25 - BC - AssetSMART-2.0-A-Tool-to-Assess-Your-Communitys-Asset-Management-PracticesGuy YgalNo ratings yet

- AP 9502 - LiabilitiesDocument12 pagesAP 9502 - Liabilitiesrandel10caneteNo ratings yet

- Adobe Scan 26-Apr-2024Document6 pagesAdobe Scan 26-Apr-2024Nishi GuptaNo ratings yet

- App-A - Acme-Process-Map-1Document1 pageApp-A - Acme-Process-Map-1adamNo ratings yet

- Risk Treatment ProcessDocument1 pageRisk Treatment Processcybertank378No ratings yet

- Module 4 ACCTDocument11 pagesModule 4 ACCTFathimath NoohaNo ratings yet

- Labrador Petro ManagementDocument3 pagesLabrador Petro ManagementTuanson PhamNo ratings yet

- ReportingDocument62 pagesReportingElvis RumintsNo ratings yet

- Agile Devops Planning Transition TransformationDocument1 pageAgile Devops Planning Transition TransformationAdrian des RotoursNo ratings yet

- 431705996.xls List of Findings (Current)Document2 pages431705996.xls List of Findings (Current)RamppraSath MgrsNo ratings yet

- Behavior Life CycleDocument1 pageBehavior Life CycleSubash VenkataNo ratings yet

- Flexi Cap Fund - Leaflet 1 0Document2 pagesFlexi Cap Fund - Leaflet 1 0shubhamchavan8411No ratings yet

- Acc Mind Map PDFDocument1 pageAcc Mind Map PDFSIDDHARTH MALIKNo ratings yet

- RP2-ISO9001 2015 ADocument50 pagesRP2-ISO9001 2015 AMasrawana Mohd Masran100% (1)

- Notebook - Principle of AccountingDocument33 pagesNotebook - Principle of AccountingNguyễn Quỳnh AnhNo ratings yet

- Pa 2Document8 pagesPa 2Trần Ngọc NhưNo ratings yet

- Add Defect / Deviation: Processing of Notification Need To Be Delayed/ Defects Analysis Not CompletedDocument1 pageAdd Defect / Deviation: Processing of Notification Need To Be Delayed/ Defects Analysis Not CompletedkdgkamlakarNo ratings yet

- Grade 12 Notes 3Document1 pageGrade 12 Notes 3RainbowNo ratings yet

- Limits Delegation of AuthorityDocument13 pagesLimits Delegation of AuthoritySheikh Ahmer HameedNo ratings yet

- Bus200 Chapter 17 Notes Naif Alqahtani-2Document6 pagesBus200 Chapter 17 Notes Naif Alqahtani-2Ammar YasserNo ratings yet

- Related Parties ISA 550 Audit CAF 9 (ARM+AMK)Document11 pagesRelated Parties ISA 550 Audit CAF 9 (ARM+AMK)Abdul WahabNo ratings yet

- Account & Deposit Processes (Corporate)Document1 pageAccount & Deposit Processes (Corporate)Ram Mohan MishraNo ratings yet

- GMRs 2021 EnglishDocument90 pagesGMRs 2021 EnglishMuhammad Ashraf AhmadNo ratings yet

- Audit PlanningDocument2 pagesAudit Planninglied27106No ratings yet

- In-N-Out Burger, Inc. vs. Sehwani, Incorporated, 575 SCRA 535, G.R. No. 179127 December 24, 2008Document10 pagesIn-N-Out Burger, Inc. vs. Sehwani, Incorporated, 575 SCRA 535, G.R. No. 179127 December 24, 2008Lyka Angelique CisnerosNo ratings yet

- ONGC Cash FlowDocument4 pagesONGC Cash FlowSreehari K.SNo ratings yet

- Concert: Certified Installer Plus - Enterprise Solutions Partner (Cip-Esp)Document2 pagesConcert: Certified Installer Plus - Enterprise Solutions Partner (Cip-Esp)AndresNo ratings yet

- Milling Machine EMCOMAT FB 450L 600L enDocument12 pagesMilling Machine EMCOMAT FB 450L 600L enŽan PjerNo ratings yet

- Arun 41Document4 pagesArun 41k.g.thri moorthyNo ratings yet

- MSDS of Asi-CalphosDocument4 pagesMSDS of Asi-Calphosthiensuty74No ratings yet

- List Sponsorship 2021Document6 pagesList Sponsorship 2021chotto matte100% (1)

- Chapter 02 Financial Statements AnalysisDocument15 pagesChapter 02 Financial Statements AnalysisAliceJohnNo ratings yet

- Log FileDocument51 pagesLog FileGopalakrishna Devulapalli100% (1)

- Abstract On Honey PotsDocument18 pagesAbstract On Honey PotsBen Garcia100% (3)

- Owner's Manual EM3000 - EM4000: ©1994 American Honda Motor Co., Inc. - All Rights ReservedDocument41 pagesOwner's Manual EM3000 - EM4000: ©1994 American Honda Motor Co., Inc. - All Rights ReservedTrần Hoàng LâmNo ratings yet

- CEASIOM An Open Source Multi Module ConcDocument7 pagesCEASIOM An Open Source Multi Module ConcSab-Win DamadNo ratings yet

- Report On FINANCIAL PERFORMANCE ANALYSIS OF CEMENT INDUSTRY AND COMPARISON WITH LAFARGE-HOLCIM BANGLADESH CEMENT LTDDocument34 pagesReport On FINANCIAL PERFORMANCE ANALYSIS OF CEMENT INDUSTRY AND COMPARISON WITH LAFARGE-HOLCIM BANGLADESH CEMENT LTDavishek karmakerNo ratings yet

- Apparel ManufacturingDocument13 pagesApparel ManufacturingBoier Sesh Pata100% (1)

- FM1 (4th) May2019Document2 pagesFM1 (4th) May2019fdwkqjNo ratings yet

- Vortex Bladeless Wind TurbineDocument3 pagesVortex Bladeless Wind TurbineLokesh Kumar GuptaNo ratings yet

- Eutech Con2700Document3 pagesEutech Con2700neda ahadiNo ratings yet

- v12 Engine Manual x300 - v12 - Service PDFDocument43 pagesv12 Engine Manual x300 - v12 - Service PDFfrankfmv50% (2)

- Module 1 Long Term Financing DecisionsDocument9 pagesModule 1 Long Term Financing Decisionscha11100% (1)

- CSR Business Ethics in IBDocument10 pagesCSR Business Ethics in IBBhavya NagdaNo ratings yet

- VMware Overview of L1 Terminal Fault' (L1TF) Speculative-Execution Vulnerabilities in Intel Processors - CVE-2018-3646, CVE-2018-3620, and CVE-2018-3615 (55636)Document2 pagesVMware Overview of L1 Terminal Fault' (L1TF) Speculative-Execution Vulnerabilities in Intel Processors - CVE-2018-3646, CVE-2018-3620, and CVE-2018-3615 (55636)Priyank RajNo ratings yet

- Optimization of The Setup Position of A Workpiece For Five-Axis Machining To Reduce Machining TimeDocument13 pagesOptimization of The Setup Position of A Workpiece For Five-Axis Machining To Reduce Machining TimeHungTranNo ratings yet

- Review Part1IA2.Docx 1Document73 pagesReview Part1IA2.Docx 1HAZELMAE JEMINEZNo ratings yet

- Incident Record FormDocument2 pagesIncident Record FormMark Joel AguilaNo ratings yet

- Prove That If XN Is BoundedDocument2 pagesProve That If XN Is BoundedPallav Jyoti PalNo ratings yet

- Dissertation: Amal P Azeez 171110027Document66 pagesDissertation: Amal P Azeez 171110027Amal azeezNo ratings yet

- Realworld Upgrade ISRroutersDocument2 pagesRealworld Upgrade ISRroutersFarman ATeeqNo ratings yet

- Baker DX 71-030 Ug en v10Document156 pagesBaker DX 71-030 Ug en v10Joel Parra ZambranoNo ratings yet

- OOP Week 2Document34 pagesOOP Week 2鄭力愷No ratings yet

- GE Oil & Gas Nuovo Pignone: Title: Part List: Drawing: Gear BoxDocument1 pageGE Oil & Gas Nuovo Pignone: Title: Part List: Drawing: Gear BoxMohammed ElarbedNo ratings yet

Download as pdf or txt

You might also like

- Payroll (HR) RCM 2022-2023Document1 pagePayroll (HR) RCM 2022-2023Aman ParchaniNo ratings yet

- Implementing-Grc-Lines-Of-DefenseDocument1 pageImplementing-Grc-Lines-Of-DefensekeizersNo ratings yet

- 95051060-BRC-Food6-Checklist GDFGDocument27 pages95051060-BRC-Food6-Checklist GDFGAsep RNo ratings yet

- Change Management Routemap at ONE SLIDE PDFDocument1 pageChange Management Routemap at ONE SLIDE PDFAndrey PritulyukNo ratings yet

- QMS Process Interaction Diagram (WHOLE)Document1 pageQMS Process Interaction Diagram (WHOLE)Adil Abdulkhader100% (2)

- FSMS Process Interaction Diagram (WHOLE)Document1 pageFSMS Process Interaction Diagram (WHOLE)Adil AbdulkhaderNo ratings yet

- Audit ProcedureDocument1 pageAudit Procedurejay thakkarNo ratings yet

- MCQDocument36 pagesMCQMike AntolinoNo ratings yet

- CP 0n SLO in The Workplace-Lifting Plan - 6 Slides Per Page - R2Document6 pagesCP 0n SLO in The Workplace-Lifting Plan - 6 Slides Per Page - R2s_bharathkumarNo ratings yet

- SMETA Guidance Workflow AuditorsDocument1 pageSMETA Guidance Workflow AuditorsSam SmithNo ratings yet

- 5 Critical Appraisal - Kilminister, Taylo - SnipeDocument7 pages5 Critical Appraisal - Kilminister, Taylo - Snipesbracca1No ratings yet

- Enterprise Architecture As Capabilities ArchDocument24 pagesEnterprise Architecture As Capabilities ArchOsmo TechNo ratings yet

- DroneAcharya Financial Statements 2022 2023Document8 pagesDroneAcharya Financial Statements 2022 2023pradeep kumar pradeep kumarNo ratings yet

- Organizational Structure The Audit Board of The Republic of IndonesiaDocument1 pageOrganizational Structure The Audit Board of The Republic of IndonesiaFranz rumapeaNo ratings yet

- Revolve Project Audit: No. System Element Compliance Understanding Usage Action by WhenDocument16 pagesRevolve Project Audit: No. System Element Compliance Understanding Usage Action by WhenPatria ArdianNo ratings yet

- Year Clientcode A6 Time BudgetDocument1 pageYear Clientcode A6 Time BudgetReinnalyn UlandayNo ratings yet

- 03A Ic PartDocument19 pages03A Ic Partraghuraghu1490003No ratings yet

- Huye Branch - Risk Assessment - Fy 2022-2023 InspectionsDocument119 pagesHuye Branch - Risk Assessment - Fy 2022-2023 Inspectionsseth uwitonzeNo ratings yet

- Handle Handover Project To End UserDocument41 pagesHandle Handover Project To End UserSALAH HELLARANo ratings yet

- QMS Process Interaction To EditDocument1 pageQMS Process Interaction To EditAdil AbdulkhaderNo ratings yet

- HR Wheel PDCADocument1 pageHR Wheel PDCAMaria PatchinNo ratings yet

- Standalone Financial StatementsDocument39 pagesStandalone Financial StatementsLogan ThakurNo ratings yet

- Payables Work FlowDocument1 pagePayables Work FlowTruc ThanhNo ratings yet

- Topic 5Document1 pageTopic 5sofianasery28No ratings yet

- Nse Iar March 24Document42 pagesNse Iar March 24raju1204No ratings yet

- Audit Notes - 01Document19 pagesAudit Notes - 01JakeSiglerNo ratings yet

- Peer Recognition Program UpdatedDocument1 pagePeer Recognition Program UpdatedAudrey AyosoNo ratings yet

- SRS Brahmastra Notes_240505_193646Document9 pagesSRS Brahmastra Notes_240505_193646Sanjay AryalNo ratings yet

- BPM - TD Bank-3Document1 pageBPM - TD Bank-3frostbitexysNo ratings yet

- Chapter 24Document41 pagesChapter 24balibrea2011No ratings yet

- Close Customer PortfolioDocument1 pageClose Customer PortfolioRam Mohan MishraNo ratings yet

- Accounts Intro 3Document1 pageAccounts Intro 3manishchd81No ratings yet

- Performance Management BrokenDocument32 pagesPerformance Management BrokenJackNo ratings yet

- Audit Plan2020Document1 pageAudit Plan2020rebin azizNo ratings yet

- 25 - BC - AssetSMART-2.0-A-Tool-to-Assess-Your-Communitys-Asset-Management-PracticesDocument10 pages25 - BC - AssetSMART-2.0-A-Tool-to-Assess-Your-Communitys-Asset-Management-PracticesGuy YgalNo ratings yet

- AP 9502 - LiabilitiesDocument12 pagesAP 9502 - Liabilitiesrandel10caneteNo ratings yet

- Adobe Scan 26-Apr-2024Document6 pagesAdobe Scan 26-Apr-2024Nishi GuptaNo ratings yet

- App-A - Acme-Process-Map-1Document1 pageApp-A - Acme-Process-Map-1adamNo ratings yet

- Risk Treatment ProcessDocument1 pageRisk Treatment Processcybertank378No ratings yet

- Module 4 ACCTDocument11 pagesModule 4 ACCTFathimath NoohaNo ratings yet

- Labrador Petro ManagementDocument3 pagesLabrador Petro ManagementTuanson PhamNo ratings yet

- ReportingDocument62 pagesReportingElvis RumintsNo ratings yet

- Agile Devops Planning Transition TransformationDocument1 pageAgile Devops Planning Transition TransformationAdrian des RotoursNo ratings yet

- 431705996.xls List of Findings (Current)Document2 pages431705996.xls List of Findings (Current)RamppraSath MgrsNo ratings yet

- Behavior Life CycleDocument1 pageBehavior Life CycleSubash VenkataNo ratings yet

- Flexi Cap Fund - Leaflet 1 0Document2 pagesFlexi Cap Fund - Leaflet 1 0shubhamchavan8411No ratings yet

- Acc Mind Map PDFDocument1 pageAcc Mind Map PDFSIDDHARTH MALIKNo ratings yet

- RP2-ISO9001 2015 ADocument50 pagesRP2-ISO9001 2015 AMasrawana Mohd Masran100% (1)

- Notebook - Principle of AccountingDocument33 pagesNotebook - Principle of AccountingNguyễn Quỳnh AnhNo ratings yet

- Pa 2Document8 pagesPa 2Trần Ngọc NhưNo ratings yet

- Add Defect / Deviation: Processing of Notification Need To Be Delayed/ Defects Analysis Not CompletedDocument1 pageAdd Defect / Deviation: Processing of Notification Need To Be Delayed/ Defects Analysis Not CompletedkdgkamlakarNo ratings yet

- Grade 12 Notes 3Document1 pageGrade 12 Notes 3RainbowNo ratings yet

- Limits Delegation of AuthorityDocument13 pagesLimits Delegation of AuthoritySheikh Ahmer HameedNo ratings yet

- Bus200 Chapter 17 Notes Naif Alqahtani-2Document6 pagesBus200 Chapter 17 Notes Naif Alqahtani-2Ammar YasserNo ratings yet

- Related Parties ISA 550 Audit CAF 9 (ARM+AMK)Document11 pagesRelated Parties ISA 550 Audit CAF 9 (ARM+AMK)Abdul WahabNo ratings yet

- Account & Deposit Processes (Corporate)Document1 pageAccount & Deposit Processes (Corporate)Ram Mohan MishraNo ratings yet

- GMRs 2021 EnglishDocument90 pagesGMRs 2021 EnglishMuhammad Ashraf AhmadNo ratings yet

- Audit PlanningDocument2 pagesAudit Planninglied27106No ratings yet

- In-N-Out Burger, Inc. vs. Sehwani, Incorporated, 575 SCRA 535, G.R. No. 179127 December 24, 2008Document10 pagesIn-N-Out Burger, Inc. vs. Sehwani, Incorporated, 575 SCRA 535, G.R. No. 179127 December 24, 2008Lyka Angelique CisnerosNo ratings yet

- ONGC Cash FlowDocument4 pagesONGC Cash FlowSreehari K.SNo ratings yet

- Concert: Certified Installer Plus - Enterprise Solutions Partner (Cip-Esp)Document2 pagesConcert: Certified Installer Plus - Enterprise Solutions Partner (Cip-Esp)AndresNo ratings yet

- Milling Machine EMCOMAT FB 450L 600L enDocument12 pagesMilling Machine EMCOMAT FB 450L 600L enŽan PjerNo ratings yet

- Arun 41Document4 pagesArun 41k.g.thri moorthyNo ratings yet

- MSDS of Asi-CalphosDocument4 pagesMSDS of Asi-Calphosthiensuty74No ratings yet

- List Sponsorship 2021Document6 pagesList Sponsorship 2021chotto matte100% (1)

- Chapter 02 Financial Statements AnalysisDocument15 pagesChapter 02 Financial Statements AnalysisAliceJohnNo ratings yet

- Log FileDocument51 pagesLog FileGopalakrishna Devulapalli100% (1)

- Abstract On Honey PotsDocument18 pagesAbstract On Honey PotsBen Garcia100% (3)

- Owner's Manual EM3000 - EM4000: ©1994 American Honda Motor Co., Inc. - All Rights ReservedDocument41 pagesOwner's Manual EM3000 - EM4000: ©1994 American Honda Motor Co., Inc. - All Rights ReservedTrần Hoàng LâmNo ratings yet

- CEASIOM An Open Source Multi Module ConcDocument7 pagesCEASIOM An Open Source Multi Module ConcSab-Win DamadNo ratings yet

- Report On FINANCIAL PERFORMANCE ANALYSIS OF CEMENT INDUSTRY AND COMPARISON WITH LAFARGE-HOLCIM BANGLADESH CEMENT LTDDocument34 pagesReport On FINANCIAL PERFORMANCE ANALYSIS OF CEMENT INDUSTRY AND COMPARISON WITH LAFARGE-HOLCIM BANGLADESH CEMENT LTDavishek karmakerNo ratings yet

- Apparel ManufacturingDocument13 pagesApparel ManufacturingBoier Sesh Pata100% (1)

- FM1 (4th) May2019Document2 pagesFM1 (4th) May2019fdwkqjNo ratings yet

- Vortex Bladeless Wind TurbineDocument3 pagesVortex Bladeless Wind TurbineLokesh Kumar GuptaNo ratings yet

- Eutech Con2700Document3 pagesEutech Con2700neda ahadiNo ratings yet

- v12 Engine Manual x300 - v12 - Service PDFDocument43 pagesv12 Engine Manual x300 - v12 - Service PDFfrankfmv50% (2)

- Module 1 Long Term Financing DecisionsDocument9 pagesModule 1 Long Term Financing Decisionscha11100% (1)

- CSR Business Ethics in IBDocument10 pagesCSR Business Ethics in IBBhavya NagdaNo ratings yet

- VMware Overview of L1 Terminal Fault' (L1TF) Speculative-Execution Vulnerabilities in Intel Processors - CVE-2018-3646, CVE-2018-3620, and CVE-2018-3615 (55636)Document2 pagesVMware Overview of L1 Terminal Fault' (L1TF) Speculative-Execution Vulnerabilities in Intel Processors - CVE-2018-3646, CVE-2018-3620, and CVE-2018-3615 (55636)Priyank RajNo ratings yet

- Optimization of The Setup Position of A Workpiece For Five-Axis Machining To Reduce Machining TimeDocument13 pagesOptimization of The Setup Position of A Workpiece For Five-Axis Machining To Reduce Machining TimeHungTranNo ratings yet

- Review Part1IA2.Docx 1Document73 pagesReview Part1IA2.Docx 1HAZELMAE JEMINEZNo ratings yet

- Incident Record FormDocument2 pagesIncident Record FormMark Joel AguilaNo ratings yet

- Prove That If XN Is BoundedDocument2 pagesProve That If XN Is BoundedPallav Jyoti PalNo ratings yet

- Dissertation: Amal P Azeez 171110027Document66 pagesDissertation: Amal P Azeez 171110027Amal azeezNo ratings yet

- Realworld Upgrade ISRroutersDocument2 pagesRealworld Upgrade ISRroutersFarman ATeeqNo ratings yet

- Baker DX 71-030 Ug en v10Document156 pagesBaker DX 71-030 Ug en v10Joel Parra ZambranoNo ratings yet

- OOP Week 2Document34 pagesOOP Week 2鄭力愷No ratings yet

- GE Oil & Gas Nuovo Pignone: Title: Part List: Drawing: Gear BoxDocument1 pageGE Oil & Gas Nuovo Pignone: Title: Part List: Drawing: Gear BoxMohammed ElarbedNo ratings yet