Download as docx, pdf, or txt

You might also like

- Internal Audit Checklist of Real EstateDocument41 pagesInternal Audit Checklist of Real Estatemaahi782% (45)

- Cash NarrativeDocument4 pagesCash NarrativeCaterina De LucaNo ratings yet

- Zoom Case StudyDocument16 pagesZoom Case StudyParve SharmaNo ratings yet

- Audit of Inventory and Production Cycle Part 2Document10 pagesAudit of Inventory and Production Cycle Part 2AJ Cresmundo100% (1)

- Addressing The Gaps: The Philippines As An Emerging Health Tourism DestinationDocument9 pagesAddressing The Gaps: The Philippines As An Emerging Health Tourism DestinationN.a. M. TandayagNo ratings yet

- Auditing - Vouching of Cash TransactionsDocument8 pagesAuditing - Vouching of Cash Transactionsaditya.singhup112001No ratings yet

- Vouching of Trading Transactions: Unit 2Document6 pagesVouching of Trading Transactions: Unit 2Muskan TyagiNo ratings yet

- 4774 - Vouching - Joan MamDocument34 pages4774 - Vouching - Joan Mamnaikveerendra17No ratings yet

- Audit of General Insurance CompaniesDocument16 pagesAudit of General Insurance CompaniesTACS & CO.No ratings yet

- Chapter No.03Document11 pagesChapter No.03Masood khanNo ratings yet

- Murabah ProfitDocument15 pagesMurabah ProfitMuhammad ZulkifulNo ratings yet

- CHAPTER4Document28 pagesCHAPTER4ggukieolshopNo ratings yet

- Chapter 4 - Reveneus and Other ReceiptsDocument57 pagesChapter 4 - Reveneus and Other ReceiptsBENITEZ, DIANNE ASHLEY G.100% (1)

- Auditing Notes PadmasunDocument11 pagesAuditing Notes PadmasunPadmasunNo ratings yet

- W6 Module 10 Cash and Cash Equivalents Part 2Document8 pagesW6 Module 10 Cash and Cash Equivalents Part 2leare ruazaNo ratings yet

- Nkosenhle Ncube Report For The First QuarterDocument11 pagesNkosenhle Ncube Report For The First Quartermqondisi nkabindeNo ratings yet

- Accounts Receivable System For TPITDocument6 pagesAccounts Receivable System For TPITFokso FutekoNo ratings yet

- AuditingDocument34 pagesAuditingaditya.singhup112001No ratings yet

- 9 Expenses & Other IncomesDocument22 pages9 Expenses & Other IncomesZindgiKiKhatirNo ratings yet

- VouchingDocument61 pagesVouchingTeja Ravi67% (3)

- DYBSAAgn313 - Accounting For Government & Non-Profit Organizations (SEMI-FINAL MODULE)Document14 pagesDYBSAAgn313 - Accounting For Government & Non-Profit Organizations (SEMI-FINAL MODULE)Jonnafe Almendralejo IntanoNo ratings yet

- Check List For The AuditDocument14 pagesCheck List For The AuditushaNo ratings yet

- Financial Accounting and ReportingDocument31 pagesFinancial Accounting and ReportingBer SchoolNo ratings yet

- Unit: 3 - Vouching: by Mahitha VasanthiDocument15 pagesUnit: 3 - Vouching: by Mahitha VasanthianuragNo ratings yet

- Revenue Recognition 23-25Document23 pagesRevenue Recognition 23-25Yashveer SinghNo ratings yet

- Receivables (Handouts)Document6 pagesReceivables (Handouts)Crystal Padilla100% (1)

- Accounting For Revenue and Other Receipts: Instructor: Rey C. Ramonal, CPADocument13 pagesAccounting For Revenue and Other Receipts: Instructor: Rey C. Ramonal, CPACarlo manejaNo ratings yet

- RECEIVABLESDocument31 pagesRECEIVABLESAcads PurpsNo ratings yet

- Unit 1 Vouching - 1 - FinalDocument12 pagesUnit 1 Vouching - 1 - Finalshoaib shaikhNo ratings yet

- Receivable Financing: Pledge, Assignment and FactoringDocument35 pagesReceivable Financing: Pledge, Assignment and FactoringMARY GRACE VARGASNo ratings yet

- Explain What Type of Information Should Be Included in The Schedule For The Permanent File in Respect of The MortgageDocument5 pagesExplain What Type of Information Should Be Included in The Schedule For The Permanent File in Respect of The MortgageBeyonce SmithNo ratings yet

- Acc003 Summary IA3 C01 Small EntitiesDocument8 pagesAcc003 Summary IA3 C01 Small EntitiesMonique VillaNo ratings yet

- Accounts ReceivableDocument41 pagesAccounts ReceivableTenshi ChanNo ratings yet

- (ACCT 317) Chapter 8 - Reporting and Analyzing ReceivablesDocument1 page(ACCT 317) Chapter 8 - Reporting and Analyzing Receivablesp.a.No ratings yet

- 2020 Int Acc 1 - ReceivablesDocument45 pages2020 Int Acc 1 - ReceivablesNICOLE HIPOLITONo ratings yet

- Lecture On Nature of ReceivablesDocument3 pagesLecture On Nature of ReceivablesSara AlbinaNo ratings yet

- Glossary of AccountingDocument8 pagesGlossary of AccountingSarbuland Khan LodhiNo ratings yet

- 160_16CCCCM15-16CCCBM15-16CCCAC15_2020052605363635Document25 pages160_16CCCCM15-16CCCBM15-16CCCAC15_2020052605363635sandeepattigeri65No ratings yet

- Lecture 15 Vouching of Income and ExpensesDocument26 pagesLecture 15 Vouching of Income and ExpensesHarjot SinghNo ratings yet

- AC414 - Audit and Investigations II - Audit of Payables, Capital and Reserves IIDocument18 pagesAC414 - Audit and Investigations II - Audit of Payables, Capital and Reserves IITsitsi AbigailNo ratings yet

- Auditing 2&3 Theories Reviewer CompilationDocument9 pagesAuditing 2&3 Theories Reviewer CompilationPaupauNo ratings yet

- Finnancial AccountingDocument10 pagesFinnancial AccountingNaveenNo ratings yet

- Business Audit - MVATDocument10 pagesBusiness Audit - MVATNeha SharmaNo ratings yet

- Untitled Document 1Document4 pagesUntitled Document 1GESPEJO, JC SHEEN O.No ratings yet

- Lecture Notes On Trade and Other ReceivablesDocument5 pagesLecture Notes On Trade and Other Receivablesjudel ArielNo ratings yet

- Lecture Notes On Trade and Other Receivables PDFDocument5 pagesLecture Notes On Trade and Other Receivables PDFjudel ArielNo ratings yet

- ACCCOB2-Chapter 3 - RECEIVABLESDocument43 pagesACCCOB2-Chapter 3 - RECEIVABLESVan TisbeNo ratings yet

- Current Liabilities, Provisions and Contingencies UPDATEDDocument82 pagesCurrent Liabilities, Provisions and Contingencies UPDATEDPaolo Perandos100% (2)

- 12 - ReceivablesDocument18 pages12 - ReceivablesNMCartNo ratings yet

- Notes To Fs - SeDocument8 pagesNotes To Fs - SeMilds LadaoNo ratings yet

- Chapter 1 - Current LiabilitiesDocument7 pagesChapter 1 - Current LiabilitiesAnton LauretaNo ratings yet

- Accounting Standard 9Document8 pagesAccounting Standard 9GAURAV JAINNo ratings yet

- SCF - 3rd YrDocument27 pagesSCF - 3rd YrA.J. Chua100% (1)

- Debit and Credit PrinciplesDocument29 pagesDebit and Credit PrinciplesHarry100% (1)

- VouchersDocument9 pagesVouchersRaviSankar100% (2)

- Revenue and Other Receipts: Revenue From Exchange TransactionsDocument6 pagesRevenue and Other Receipts: Revenue From Exchange TransactionsMaria Cecilia ReyesNo ratings yet

- Cash and Cash EquivalentsDocument27 pagesCash and Cash EquivalentsPatOcampoNo ratings yet

- Gov't Acctg Chap 6 Financial Asset 2Document4 pagesGov't Acctg Chap 6 Financial Asset 2marvinsoy.geronaNo ratings yet

- Chapter 3 ReceivablesDocument22 pagesChapter 3 ReceivablesCale Robert RascoNo ratings yet

- Audititing: Verification and Valuation OF Current AssetDocument35 pagesAudititing: Verification and Valuation OF Current AssetkunaltylNo ratings yet

- Glossary of Accounting TermsDocument16 pagesGlossary of Accounting TermsSamarpan RoyNo ratings yet

- 1040 Exam Prep Module III: Items Excluded from Gross IncomeFrom Everand1040 Exam Prep Module III: Items Excluded from Gross IncomeRating: 1 out of 5 stars1/5 (1)

- Chapter - 2Document34 pagesChapter - 2NishobithaNo ratings yet

- Mark Newman, Chief Analyst Justin Funnell, Contributing Analyst Dawn Bushaus, Managing EditorDocument42 pagesMark Newman, Chief Analyst Justin Funnell, Contributing Analyst Dawn Bushaus, Managing EditorPNG networksNo ratings yet

- Modulo Di Rimborso Spese Mediche ClaimForm-EnglishDocument2 pagesModulo Di Rimborso Spese Mediche ClaimForm-EnglishCarlo_Sturlese_4203No ratings yet

- Penerapan Telenursing Dalam Pelayanan Kesehatan: Literature ReviewDocument8 pagesPenerapan Telenursing Dalam Pelayanan Kesehatan: Literature ReviewAdi RiskiNo ratings yet

- Chapter 17Document54 pagesChapter 17Shivom YadavNo ratings yet

- Double-Entry Book-Keeping Slides For Handout - Session 4Document10 pagesDouble-Entry Book-Keeping Slides For Handout - Session 4Dilfaraz KalawatNo ratings yet

- ISO 9001-2015 Certificate 2021 - Daikin MalaysiaDocument2 pagesISO 9001-2015 Certificate 2021 - Daikin Malaysiachengkk100% (1)

- Lcci Examination Timetable 2022Document10 pagesLcci Examination Timetable 2022ShweHein 2002No ratings yet

- American English File 1. Workbook, 2nd Edition - Oxford - RemovedDocument2 pagesAmerican English File 1. Workbook, 2nd Edition - Oxford - RemovedestefaniNo ratings yet

- Worked Example-Profit Testing For UnitDocument2 pagesWorked Example-Profit Testing For UnitPatrick MugoNo ratings yet

- Digital Fundraising - Pandemic Situation - SAIDocument17 pagesDigital Fundraising - Pandemic Situation - SAIHelmi SonhajiNo ratings yet

- 3.10 AnswerDocument4 pages3.10 AnswerIlovejjcNo ratings yet

- Si 2Document4 pagesSi 2seraNo ratings yet

- Q2 MODULE3 CSS-NCII G12 Luciano-MillanDocument8 pagesQ2 MODULE3 CSS-NCII G12 Luciano-MillanRoland RodriguezNo ratings yet

- Differrence Between Primary and Secondary CostDocument3 pagesDifferrence Between Primary and Secondary CostKauam Santos100% (1)

- New Microsoft Office Excel WorksheetDocument7 pagesNew Microsoft Office Excel WorksheetKamal DasNo ratings yet

- Vikram - QA Enginner - LTE-IMS-Testing PDFDocument5 pagesVikram - QA Enginner - LTE-IMS-Testing PDFYATENDRA TRIPATHINo ratings yet

- A Guide To Digital Marketing (Social Media)Document63 pagesA Guide To Digital Marketing (Social Media)dogiparthy100% (1)

- Health Financing MechanismsDocument11 pagesHealth Financing MechanismsMayom MabuongNo ratings yet

- 2013 Jan AS MSDocument21 pages2013 Jan AS MSAfrida AnanNo ratings yet

- Cpe 08312021Document51 pagesCpe 08312021Orbenson TanNo ratings yet

- List of Grocery Importers in Austria Europe PDF FreeDocument11 pagesList of Grocery Importers in Austria Europe PDF FreeEmpy SumardiNo ratings yet

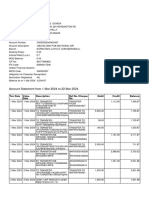

- Account Statement From 1 Mar 2024 To 22 Mar 2024: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocument13 pagesAccount Statement From 1 Mar 2024 To 22 Mar 2024: TXN Date Value Date Description Ref No./Cheque No. Debit Credit Balancerohit8324007No ratings yet

- Chapter 12 SummaryDocument19 pagesChapter 12 SummaryHamza AlBulushiNo ratings yet

- 0c0701670000000800075 ESTATEMENT 052023 0c07016700000008Document8 pages0c0701670000000800075 ESTATEMENT 052023 0c07016700000008shiripalsingh0167No ratings yet

- Theoritical Framework &literature ReviewDocument27 pagesTheoritical Framework &literature ReviewGelani PradipNo ratings yet

- Chapter3 Part1Document26 pagesChapter3 Part1Sarah AlJaberNo ratings yet