Download as pdf or txt

You might also like

- Chapter 3 Homework Template 7.6 21Document27 pagesChapter 3 Homework Template 7.6 21Ahmed Mahmoud100% (1)

- Ramya Mba ProjectDocument103 pagesRamya Mba ProjectSudha Swetha100% (1)

- La Opala RG LimitedDocument5 pagesLa Opala RG LimitedAshwani KesharwaniNo ratings yet

- Myra Hygiene Products Private LimitedDocument7 pagesMyra Hygiene Products Private Limitedanuj7729No ratings yet

- Press Release Tab India Granites Private LimitedDocument6 pagesPress Release Tab India Granites Private LimitedRavi BabuNo ratings yet

- Shilchar Technologies LimitedDocument5 pagesShilchar Technologies Limitedjaikumar608jainNo ratings yet

- Amarth Ifestyle RetailingDocument5 pagesAmarth Ifestyle Retailingheera lal thakurNo ratings yet

- Gujarat Themis Biosyn LimitedDocument5 pagesGujarat Themis Biosyn LimitedAshwani KesharwaniNo ratings yet

- Best Finance Corporation Limited: Facilities/Instruments Amount (Rs. Crore) Rating Rating ActionDocument5 pagesBest Finance Corporation Limited: Facilities/Instruments Amount (Rs. Crore) Rating Rating ActionKarthikeyan RK SwamyNo ratings yet

- SVR Drugsprivate LimitedDocument4 pagesSVR Drugsprivate Limitedlalit rawatNo ratings yet

- Tarsons Products LimitedDocument5 pagesTarsons Products LimitedujjwalgoldNo ratings yet

- Divis Laboratories LimitedDocument7 pagesDivis Laboratories Limiteddivygupta198No ratings yet

- 3F Industries LimitedDocument5 pages3F Industries LimitedData CentrumNo ratings yet

- Coral AssociatesDocument5 pagesCoral AssociatesFunny CloudsNo ratings yet

- SMFG India Credit Company LimitedDocument9 pagesSMFG India Credit Company Limitedvatsal sinhaNo ratings yet

- Wockhardt LimitedDocument8 pagesWockhardt LimitedKumar SatyakamNo ratings yet

- Technico Industries LimitedDocument4 pagesTechnico Industries Limitedshankarravi8975No ratings yet

- Indotech Transformers LimitedDocument7 pagesIndotech Transformers Limitedpiyush.kundraNo ratings yet

- Shapoorji Pallonji and Company Private LimitedDocument5 pagesShapoorji Pallonji and Company Private LimitedPrabhakar DubeyNo ratings yet

- Microfinance Private LimitedDocument5 pagesMicrofinance Private LimitedsantoshbsantuNo ratings yet

- Bhuwalka and Sons Private LimitedDocument4 pagesBhuwalka and Sons Private LimiteddoctorsabeehNo ratings yet

- Sunlex Fabrics Private Limited - Care RatingsDocument6 pagesSunlex Fabrics Private Limited - Care RatingsManeet GoyalNo ratings yet

- Keventer Agro LimitedDocument4 pagesKeventer Agro LimitedYasser SayedNo ratings yet

- PR ARCL Organics 31jan22Document7 pagesPR ARCL Organics 31jan22anady135344No ratings yet

- Jay Ushin Limited: Rationale-Press ReleaseDocument4 pagesJay Ushin Limited: Rationale-Press Releaseravi.youNo ratings yet

- Press Release Deccan Industries: Positive FactorsDocument4 pagesPress Release Deccan Industries: Positive FactorsHARI HARANNo ratings yet

- Press Release RACL Geartech LTDDocument4 pagesPress Release RACL Geartech LTDSourav DuttaNo ratings yet

- Devyani Food Industries LimitedDocument7 pagesDevyani Food Industries LimitedRahulNo ratings yet

- Ganga Rasayanie Private Limited-R-10102019Document7 pagesGanga Rasayanie Private Limited-R-10102019DarshanNo ratings yet

- Mega Steel IndustriesDocument4 pagesMega Steel IndustrieshseckalpeshNo ratings yet

- CRD Foods 8apr2020Document6 pagesCRD Foods 8apr2020samudragupta05No ratings yet

- Document Service V2Document8 pagesDocument Service V2ritika.choudharyNo ratings yet

- Poddar Diamonds Limited-09-29-2017Document4 pagesPoddar Diamonds Limited-09-29-2017tridev kant tripathiNo ratings yet

- Tab India Granites Private Limited-02-07-2020Document6 pagesTab India Granites Private Limited-02-07-2020Puneet367No ratings yet

- Vinati Organics Limited CARE Rating July 2017Document5 pagesVinati Organics Limited CARE Rating July 2017mgrreddyNo ratings yet

- Save Microfinance Private Limited: RatingsDocument4 pagesSave Microfinance Private Limited: RatingsSubhamNo ratings yet

- Bikanervala Foods - R - 22022019Document7 pagesBikanervala Foods - R - 22022019aman.raj2022No ratings yet

- Team Computers Private - R - 09102020Document8 pagesTeam Computers Private - R - 09102020DarshanNo ratings yet

- Thriveni Earthmovers Private LimitedDocument9 pagesThriveni Earthmovers Private Limitedarc14consultantNo ratings yet

- Filatex India Limited PDFDocument6 pagesFilatex India Limited PDFfatNo ratings yet

- Stove Kraft LimitedDocument7 pagesStove Kraft LimitedSiddharth Rai SuranaNo ratings yet

- Kanchan Oil Industries LimitedDocument4 pagesKanchan Oil Industries LimitedSam FireNo ratings yet

- Sun Home Appliances Private - R - 25082020Document7 pagesSun Home Appliances Private - R - 25082020DarshanNo ratings yet

- Home First Finance Company India LimitedDocument8 pagesHome First Finance Company India LimitedRAROLINKSNo ratings yet

- RR 20190917Document4 pagesRR 20190917omkarambale1No ratings yet

- AETHER Industries LTD - 2020 Credit RatingDocument5 pagesAETHER Industries LTD - 2020 Credit RatingEast West Strategic ConsultingNo ratings yet

- Incred Financial Services Limited Press+ReleaseDocument7 pagesIncred Financial Services Limited Press+ReleaseGautam MehtaNo ratings yet

- Credit Rating Post March 2023Document26 pagesCredit Rating Post March 2023Sumiran BansalNo ratings yet

- Sanghi Jewellers PVT - R - 20102020Document7 pagesSanghi Jewellers PVT - R - 20102020DarshanNo ratings yet

- Thriveni Sainik Mining Private Limited 2023Document8 pagesThriveni Sainik Mining Private Limited 2023Karthikeyan RK SwamyNo ratings yet

- Press Release Gravita India Limited: Ratings Facilities Amount (Rs. Crore) Ratings Rating ActionDocument7 pagesPress Release Gravita India Limited: Ratings Facilities Amount (Rs. Crore) Ratings Rating ActionhamsNo ratings yet

- Derewala Industries 6mar2020Document6 pagesDerewala Industries 6mar2020Mukul SoniNo ratings yet

- A One Steel Alloys 10may2021Document7 pagesA One Steel Alloys 10may2021L KNo ratings yet

- SGS Tekniks Manufacturing PVT LTDDocument7 pagesSGS Tekniks Manufacturing PVT LTDgcgary87No ratings yet

- Super Screws Private Limited: Summary of Rated InstrumentsDocument7 pagesSuper Screws Private Limited: Summary of Rated InstrumentsAnonymous bdUhUNm7JNo ratings yet

- Satya Stone Exports-01!24!2020Document4 pagesSatya Stone Exports-01!24!2020vasfee.7172No ratings yet

- Ramani Cars Private Limited 2023Document6 pagesRamani Cars Private Limited 2023Karthikeyan RK SwamyNo ratings yet

- Samunnati Rating Rationale b764561b41Document8 pagesSamunnati Rating Rationale b764561b41PratyushNo ratings yet

- Press Release Airo Lam Limited: Details of Instruments/facilities in Annexure-1Document4 pagesPress Release Airo Lam Limited: Details of Instruments/facilities in Annexure-1flying400No ratings yet

- Varsha Industries-R-19072018 PDFDocument7 pagesVarsha Industries-R-19072018 PDFKunal DamaniNo ratings yet

- Pon Pure Chemical - R-31082018Document8 pagesPon Pure Chemical - R-31082018Games ZoneNo ratings yet

- ASEAN Corporate Governance Scorecard Country Reports and Assessments 2019From EverandASEAN Corporate Governance Scorecard Country Reports and Assessments 2019No ratings yet

- Bagkiya Constructions Private Limited-RU-01!03!2024Document10 pagesBagkiya Constructions Private Limited-RU-01!03!2024arc14consultantNo ratings yet

- Jagdhatri Papers Private Limited-RU-01-03-2024Document10 pagesJagdhatri Papers Private Limited-RU-01-03-2024arc14consultantNo ratings yet

- Eauction Ludhiana PNB ENGLISH 11042016Document1 pageEauction Ludhiana PNB ENGLISH 11042016arc14consultantNo ratings yet

- Auction Notice 1685951975Document6 pagesAuction Notice 1685951975arc14consultantNo ratings yet

- Accounting Revision Notes 0452Document18 pagesAccounting Revision Notes 0452Hassan AsgharNo ratings yet

- Working Capital Management atDocument29 pagesWorking Capital Management atNavkesh GautamNo ratings yet

- Chapter 10 - Financial PlanningDocument69 pagesChapter 10 - Financial PlanningNgọc Trân Trần NguyễnNo ratings yet

- Bilawal Khan Assignment 2 23386 FCFF and Fcfe DG CementDocument5 pagesBilawal Khan Assignment 2 23386 FCFF and Fcfe DG CementBabar MairajNo ratings yet

- 1 Finance Project Report IMTDocument41 pages1 Finance Project Report IMTqueen8321100% (1)

- AFM Study Guide 2115Document15 pagesAFM Study Guide 2115RENJiiiNo ratings yet

- Problems Faced by Small Scale IndustriesDocument10 pagesProblems Faced by Small Scale IndustriesMd SharikNo ratings yet

- The Home Depot IncDocument12 pagesThe Home Depot IncKhushbooNo ratings yet

- Working Capital: in Small Scale IndustryDocument8 pagesWorking Capital: in Small Scale IndustryIrum KhanNo ratings yet

- Solvency Ratios: Debt-Equity RatioDocument5 pagesSolvency Ratios: Debt-Equity RatioShirsendu MondolNo ratings yet

- Week 8-Financial Analysis-S2 2015Document66 pagesWeek 8-Financial Analysis-S2 2015jp30ptt7No ratings yet

- Debt Free Cash FreeDocument21 pagesDebt Free Cash FreeAhmad BilalNo ratings yet

- ENT600 Blueprint FormatDocument20 pagesENT600 Blueprint FormatMujahid Addin100% (1)

- Assignment-1 Grp-3-3Document8 pagesAssignment-1 Grp-3-3Gaurang GawasNo ratings yet

- Horizontal Analysis United Plantation LatestDocument33 pagesHorizontal Analysis United Plantation Latestwawan100% (1)

- Financial Management Research Paper Financial Ratios of BritanniaDocument15 pagesFinancial Management Research Paper Financial Ratios of BritanniaShaik Noor Mohammed Ali Jinnah 19DBLAW036No ratings yet

- More Illustrative Problems: Illustration 1Document33 pagesMore Illustrative Problems: Illustration 1VEDANT BASNYATNo ratings yet

- Business Finance: Unit III: Financial Planning Tools & ConceptsDocument50 pagesBusiness Finance: Unit III: Financial Planning Tools & ConceptsKristel Anne Roquero BalisiNo ratings yet

- Swisstek (Ceylon) PLC Swisstek (Ceylon) PLCDocument7 pagesSwisstek (Ceylon) PLC Swisstek (Ceylon) PLCkasun witharanaNo ratings yet

- CCASBCP030Document64 pagesCCASBCP030Swati KaleNo ratings yet

- Cadbury India - R1 (Group-6)Document39 pagesCadbury India - R1 (Group-6)Radha ShekharNo ratings yet

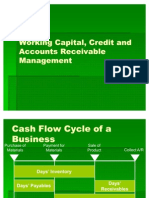

- Working Capital, Credit and Accounts Receivable ManagementDocument31 pagesWorking Capital, Credit and Accounts Receivable ManagementAnkit AgarwalNo ratings yet

- Mercury Athletic FootwareDocument12 pagesMercury Athletic FootwareAnandNo ratings yet

- FRM CompleteDocument28 pagesFRM CompleteZaineb Mora SadikNo ratings yet

- Go Rural FM AssignmentDocument31 pagesGo Rural FM AssignmentHumphrey OsaigbeNo ratings yet

- Working Capital Management: Kiran ThapaDocument18 pagesWorking Capital Management: Kiran ThapaRajesh ShresthaNo ratings yet

- Techniques of Cash ManagementDocument18 pagesTechniques of Cash ManagementKrishna Chandran PallippuramNo ratings yet

- Chap 6 Notes AFMDocument30 pagesChap 6 Notes AFMAngel RubiosNo ratings yet