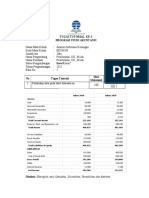

Finance Assignment GP

Finance Assignment GP

You might also like

- Entrepreneurial Finance, Fourth Edition: Finance and Business Strategies for the Serious EntrepreneurFrom EverandEntrepreneurial Finance, Fourth Edition: Finance and Business Strategies for the Serious EntrepreneurNo ratings yet

- Test Bank For Economics Private and Public Choice 16th Edition William A MceachernDocument13 pagesTest Bank For Economics Private and Public Choice 16th Edition William A Mceachernlindapalmeropagfbxsnr100% (27)

- (Gaming) Merchant Services AgreementDocument36 pages(Gaming) Merchant Services AgreementAdarsh SonkarNo ratings yet

- Bachelor of Business Management (Hons) Finance: Universiti Teknologi MARA, Melaka City CampusDocument34 pagesBachelor of Business Management (Hons) Finance: Universiti Teknologi MARA, Melaka City CampusPuteri Nina100% (1)

- PFN1223 - Set A - MSDocument8 pagesPFN1223 - Set A - MSalya farhanaNo ratings yet

- FIN4284 ALTERNATIVE ASSESSMENT-FinalDocument11 pagesFIN4284 ALTERNATIVE ASSESSMENT-FinalAtif QureshiNo ratings yet

- Schaum's Outline of Basic Business Mathematics, 2edFrom EverandSchaum's Outline of Basic Business Mathematics, 2edRating: 5 out of 5 stars5/5 (2)

- 5.1 Seatwork Quiz Receivable FinancingDocument2 pages5.1 Seatwork Quiz Receivable FinancingSean Aaron Segucio0% (1)

- Charles GreerDocument109 pagesCharles GreerVicky GuleriaNo ratings yet

- Liquidity Ratio Industr Y: Company 2.26 0.77Document2 pagesLiquidity Ratio Industr Y: Company 2.26 0.77MasTer PanDaNo ratings yet

- SBL PBA4807 Assignment 1Document11 pagesSBL PBA4807 Assignment 1Charmaine Tshamaano MasuvheNo ratings yet

- Fraser & Neave Holdings BHDDocument10 pagesFraser & Neave Holdings BHDKirthiga NathanNo ratings yet

- MGMT AccDocument15 pagesMGMT Accbollab654No ratings yet

- Sample Assignment UiTM Student PDFDocument319 pagesSample Assignment UiTM Student PDFZul HashimNo ratings yet

- Acc466 - Group G - Project 1Document28 pagesAcc466 - Group G - Project 1Nur SyafiqahNo ratings yet

- Tugas 2 Eksi 4204 - Dini Nur Lathifah - 030995277Document4 pagesTugas 2 Eksi 4204 - Dini Nur Lathifah - 030995277Doni Jogja0% (1)

- AccuduDocument23 pagesAccuduFeilix BennyNo ratings yet

- Ratio Formula Computation Result InterpretationDocument2 pagesRatio Formula Computation Result InterpretationAleya MonteverdeNo ratings yet

- AFM Assignment 2 - Accounting RatiosDocument7 pagesAFM Assignment 2 - Accounting RatiosMunna ShettyNo ratings yet

- Financial Statement Analysis of Beximco Pharmaceuticals LimitedDocument6 pagesFinancial Statement Analysis of Beximco Pharmaceuticals LimitedMaisha AnzumNo ratings yet

- Tugas 2 - Analisis Informasi Keuangan - AisyahdenyDocument3 pagesTugas 2 - Analisis Informasi Keuangan - AisyahdenyJosh SaktiNo ratings yet

- BAC1644 Principles of Finance AssignmentDocument33 pagesBAC1644 Principles of Finance Assignmentyuyin.gohyyNo ratings yet

- Tata Analysis ProjectDocument60 pagesTata Analysis ProjectSeema YadavNo ratings yet

- Nurul Aina Tasha (2020894854) - Individual Report Fin242Document11 pagesNurul Aina Tasha (2020894854) - Individual Report Fin242Aina AsgaliNo ratings yet

- Course Code: Acc117: Declaration Form of Group AssignmentDocument6 pagesCourse Code: Acc117: Declaration Form of Group AssignmentMASTURINA NURNo ratings yet

- Assignment 1 - Fin430 (Hup Seng Berhad)Document10 pagesAssignment 1 - Fin430 (Hup Seng Berhad)Qairunisa Mochsein100% (1)

- Accounting Assessment Report - Hup Seng Berhad & Hwa Tai IndustriesDocument16 pagesAccounting Assessment Report - Hup Seng Berhad & Hwa Tai IndustriesYoga ManiNo ratings yet

- Ashish Black BookDocument57 pagesAshish Black BookHamza FangariNo ratings yet

- Universal Robina Corporation: Prepared By: Garcia, Leriz Peñalosa, Rena Daniel Pescasio, LeonardDocument15 pagesUniversal Robina Corporation: Prepared By: Garcia, Leriz Peñalosa, Rena Daniel Pescasio, LeonardLeriz GarciaNo ratings yet

- Rasio Lancar: Nama:Intania Nim: A1C118086 Kelas: E Akuntansi Reguler Sore MK: Akt. Keuangan 1Document4 pagesRasio Lancar: Nama:Intania Nim: A1C118086 Kelas: E Akuntansi Reguler Sore MK: Akt. Keuangan 1Reza HijjulbaetNo ratings yet

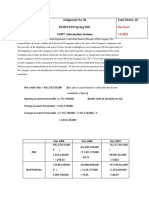

- Assignment No. 02 SEMESTER Spring 2021 CS507-Information Systems Total Marks: 20Document5 pagesAssignment No. 02 SEMESTER Spring 2021 CS507-Information Systems Total Marks: 20UmairAfzalNo ratings yet

- 23090167@student Iumw Edu MyDocument18 pages23090167@student Iumw Edu MyShazryl Rifqi Shamsul NizamNo ratings yet

- GTC BS 22Document76 pagesGTC BS 22Ashwin NaveenNo ratings yet

- BTL tài chính doanh nghiệp mớiDocument19 pagesBTL tài chính doanh nghiệp mớiDo Hoang LanNo ratings yet

- COURSE CODE: ACC117/106/100 Declaration Form of Group AssignmentDocument9 pagesCOURSE CODE: ACC117/106/100 Declaration Form of Group AssignmentMARLINDAH RAHIMNo ratings yet

- Tugas Manajemen Keuangan Ayu Wulan Agustiyanti P32.2021.00805Document1 pageTugas Manajemen Keuangan Ayu Wulan Agustiyanti P32.2021.00805AYU WULAN AGUSTIYANTINo ratings yet

- ACCOUNTING Simulation Exercise DR RIMA - Coop Bank PertamaDocument9 pagesACCOUNTING Simulation Exercise DR RIMA - Coop Bank PertamaericdeskkuNo ratings yet

- 3-Ifn3 031210073 Assignment2Document9 pages3-Ifn3 031210073 Assignment2May MsNo ratings yet

- Profits and Gains of Business or ProfessionDocument2 pagesProfits and Gains of Business or ProfessionDaMoNNo ratings yet

- BC0150010 FM ProjectDocument12 pagesBC0150010 FM ProjectKrishnaNo ratings yet

- Fin242 Group AssignmentDocument14 pagesFin242 Group AssignmentNurul AzlinNo ratings yet

- Dutch Lady - Financial Ratio Analysis - Kba2431aDocument15 pagesDutch Lady - Financial Ratio Analysis - Kba2431aMOHAMAD IZZANI OTHMANNo ratings yet

- Ratio AnalysisDocument2 pagesRatio AnalysisShalehNo ratings yet

- Group Assignment Acc116Document9 pagesGroup Assignment Acc116Nurul AzlinNo ratings yet

- Accounting 2020 P1 MemoDocument11 pagesAccounting 2020 P1 MemoodiantumbaNo ratings yet

- Acc Proj PandaDocument23 pagesAcc Proj PandaFeilix BennyNo ratings yet

- Mineral Processing Engineers Seminars 2023 1671089455Document4 pagesMineral Processing Engineers Seminars 2023 1671089455SalomeyQuarshieNo ratings yet

- BhupiDocument251 pagesBhupiRaju PrasadNo ratings yet

- Smith and CPDocument3 pagesSmith and CPFirdausNo ratings yet

- Ratio Calculation - Financial ManagementDocument16 pagesRatio Calculation - Financial ManagementAinul MardhiahNo ratings yet

- Xyz Profitability Analysis: Creating A Profitable Direct Marketing Promotion Using CHAID SegmentationDocument6 pagesXyz Profitability Analysis: Creating A Profitable Direct Marketing Promotion Using CHAID SegmentationAlex TalloNo ratings yet

- Individual AssignmentDocument9 pagesIndividual AssignmentSITI NUR AISYAH MD ROSTANNo ratings yet

- 680-Twinkle Industry Balance Sheet 2021Document4 pages680-Twinkle Industry Balance Sheet 2021twinklesindNo ratings yet

- Accounting NSC P1 Memo Nov 2022 EngDocument12 pagesAccounting NSC P1 Memo Nov 2022 EngItumeleng MogoleNo ratings yet

- Kamre Aalam Balance Sheet - March-2022Document4 pagesKamre Aalam Balance Sheet - March-2022Parth KachhiyaNo ratings yet

- 2021-22 Accountancy Class Xii Sample ProjectDocument19 pages2021-22 Accountancy Class Xii Sample ProjectfarhaanNo ratings yet

- Rescued DocumentDocument9 pagesRescued Documentalihanaveed9No ratings yet

- TUGAS Analisis Laporan Keuangan KAI 2020Document8 pagesTUGAS Analisis Laporan Keuangan KAI 2020Rahma AgustinaNo ratings yet

- Project GuidelinesDocument19 pagesProject GuidelinesShown Shaji JosephNo ratings yet

- Worksheet DagangDocument10 pagesWorksheet DagangSetiandi RiswantoNo ratings yet

- Basic of FinanceDocument5 pagesBasic of FinanceKanitha MuniandyNo ratings yet

- Universiti Teknologi Mara - Examination ResultDocument1 pageUniversiti Teknologi Mara - Examination ResultShuhaina NizamNo ratings yet

- Afrin Shibu SB20CCM003 ProjectDocument79 pagesAfrin Shibu SB20CCM003 Projectabhishek628980No ratings yet

- Pensonic AsignmentDocument12 pagesPensonic AsignmentFaris HanisNo ratings yet

- An Introduction To ESG Reporting FrameworksDocument6 pagesAn Introduction To ESG Reporting FrameworksAblekkNo ratings yet

- Balancing Act: Managing The Public PurseDocument64 pagesBalancing Act: Managing The Public PurseGamers LKONo ratings yet

- A Study On Profitability AnalysisDocument48 pagesA Study On Profitability AnalysisDilip singhNo ratings yet

- Hul Annual Report 2018 19 - tcm1255 538867 - 1 - en PDFDocument228 pagesHul Annual Report 2018 19 - tcm1255 538867 - 1 - en PDFAkankshaNo ratings yet

- Company Profile: Company Name: Coal Bharat LimitedDocument34 pagesCompany Profile: Company Name: Coal Bharat Limitedshya1480No ratings yet

- ECO121 - Test 01 - Individual Assignment 01Document9 pagesECO121 - Test 01 - Individual Assignment 01Tran Binh Minh QP3195No ratings yet

- Double Question EssayDocument4 pagesDouble Question EssayLeyla MammadovaNo ratings yet

- Chapter 1 Introduction To Social EntrepreneurshipDocument11 pagesChapter 1 Introduction To Social EntrepreneurshipRamona Isabel UrsaisNo ratings yet

- BLM Gnf-Tc-Form-990-2020-2021-01Document63 pagesBLM Gnf-Tc-Form-990-2020-2021-01Jim HoftNo ratings yet

- Brand Audit - Final CaseDocument2 pagesBrand Audit - Final CaseDương Thị Tường VyNo ratings yet

- Marketing Research Fall 2022Document15 pagesMarketing Research Fall 2022ZUMARRAGA SAN MIGUEL AmaiaNo ratings yet

- Satisfaction Is Sure, Quality Is PureDocument18 pagesSatisfaction Is Sure, Quality Is PureSheryl BorromeoNo ratings yet

- The Complete Beginners Trading Guide - Trader's - SpotDocument73 pagesThe Complete Beginners Trading Guide - Trader's - Spothari100% (1)

- How A 16 YEAR OLD GIRL READINGDocument2 pagesHow A 16 YEAR OLD GIRL READINGMIREIA RIPOLL SOLERNo ratings yet

- Ims Operation Manual Purchase Department: Ivrcl Limited, HyderabadDocument14 pagesIms Operation Manual Purchase Department: Ivrcl Limited, HyderabadAkd DeshmukhNo ratings yet

- Easy Shop Plus Kick Off Tour - Werner - PH - Basic VersionDocument90 pagesEasy Shop Plus Kick Off Tour - Werner - PH - Basic VersionHazel L. ansulaNo ratings yet

- Mid Term Assignment k60 2021 1Document2 pagesMid Term Assignment k60 2021 1Thành Đạt NguyễnNo ratings yet

- Black & White Modern Design Project Proposal Document - 20240604 - 114746 - 0000Document4 pagesBlack & White Modern Design Project Proposal Document - 20240604 - 114746 - 0000Mr.H4No ratings yet

- Report On The Job TrainingDocument19 pagesReport On The Job TrainingRaisa RaisaNo ratings yet

- Execution Stage ActivitiesDocument1 pageExecution Stage ActivitieskapsarcNo ratings yet

- Business Chapter 2 BUSINESS STRUCTUREDocument7 pagesBusiness Chapter 2 BUSINESS STRUCTUREJosue MushagalusaNo ratings yet

- MGT 657: Strategic Management Individual Assignment ReportDocument6 pagesMGT 657: Strategic Management Individual Assignment Reportaisyah fadlyNo ratings yet

- Dilli Haat: Reviving Lost Glory: Submitted byDocument7 pagesDilli Haat: Reviving Lost Glory: Submitted byDaniyalNo ratings yet

- Industrial Policy Resolution 2022Document6 pagesIndustrial Policy Resolution 2022Pritam Umar K DasNo ratings yet

- Week 1 Introduction To Entrepreneurial CapitalDocument42 pagesWeek 1 Introduction To Entrepreneurial CapitalMichael AurynnNo ratings yet

- CapacityDocument19 pagesCapacityNitin KarnkaleNo ratings yet

Download as pdf or txt

You might also like

- Entrepreneurial Finance, Fourth Edition: Finance and Business Strategies for the Serious EntrepreneurFrom EverandEntrepreneurial Finance, Fourth Edition: Finance and Business Strategies for the Serious EntrepreneurNo ratings yet

- Test Bank For Economics Private and Public Choice 16th Edition William A MceachernDocument13 pagesTest Bank For Economics Private and Public Choice 16th Edition William A Mceachernlindapalmeropagfbxsnr100% (27)

- (Gaming) Merchant Services AgreementDocument36 pages(Gaming) Merchant Services AgreementAdarsh SonkarNo ratings yet

- Bachelor of Business Management (Hons) Finance: Universiti Teknologi MARA, Melaka City CampusDocument34 pagesBachelor of Business Management (Hons) Finance: Universiti Teknologi MARA, Melaka City CampusPuteri Nina100% (1)

- PFN1223 - Set A - MSDocument8 pagesPFN1223 - Set A - MSalya farhanaNo ratings yet

- FIN4284 ALTERNATIVE ASSESSMENT-FinalDocument11 pagesFIN4284 ALTERNATIVE ASSESSMENT-FinalAtif QureshiNo ratings yet

- Schaum's Outline of Basic Business Mathematics, 2edFrom EverandSchaum's Outline of Basic Business Mathematics, 2edRating: 5 out of 5 stars5/5 (2)

- 5.1 Seatwork Quiz Receivable FinancingDocument2 pages5.1 Seatwork Quiz Receivable FinancingSean Aaron Segucio0% (1)

- Charles GreerDocument109 pagesCharles GreerVicky GuleriaNo ratings yet

- Liquidity Ratio Industr Y: Company 2.26 0.77Document2 pagesLiquidity Ratio Industr Y: Company 2.26 0.77MasTer PanDaNo ratings yet

- SBL PBA4807 Assignment 1Document11 pagesSBL PBA4807 Assignment 1Charmaine Tshamaano MasuvheNo ratings yet

- Fraser & Neave Holdings BHDDocument10 pagesFraser & Neave Holdings BHDKirthiga NathanNo ratings yet

- MGMT AccDocument15 pagesMGMT Accbollab654No ratings yet

- Sample Assignment UiTM Student PDFDocument319 pagesSample Assignment UiTM Student PDFZul HashimNo ratings yet

- Acc466 - Group G - Project 1Document28 pagesAcc466 - Group G - Project 1Nur SyafiqahNo ratings yet

- Tugas 2 Eksi 4204 - Dini Nur Lathifah - 030995277Document4 pagesTugas 2 Eksi 4204 - Dini Nur Lathifah - 030995277Doni Jogja0% (1)

- AccuduDocument23 pagesAccuduFeilix BennyNo ratings yet

- Ratio Formula Computation Result InterpretationDocument2 pagesRatio Formula Computation Result InterpretationAleya MonteverdeNo ratings yet

- AFM Assignment 2 - Accounting RatiosDocument7 pagesAFM Assignment 2 - Accounting RatiosMunna ShettyNo ratings yet

- Financial Statement Analysis of Beximco Pharmaceuticals LimitedDocument6 pagesFinancial Statement Analysis of Beximco Pharmaceuticals LimitedMaisha AnzumNo ratings yet

- Tugas 2 - Analisis Informasi Keuangan - AisyahdenyDocument3 pagesTugas 2 - Analisis Informasi Keuangan - AisyahdenyJosh SaktiNo ratings yet

- BAC1644 Principles of Finance AssignmentDocument33 pagesBAC1644 Principles of Finance Assignmentyuyin.gohyyNo ratings yet

- Tata Analysis ProjectDocument60 pagesTata Analysis ProjectSeema YadavNo ratings yet

- Nurul Aina Tasha (2020894854) - Individual Report Fin242Document11 pagesNurul Aina Tasha (2020894854) - Individual Report Fin242Aina AsgaliNo ratings yet

- Course Code: Acc117: Declaration Form of Group AssignmentDocument6 pagesCourse Code: Acc117: Declaration Form of Group AssignmentMASTURINA NURNo ratings yet

- Assignment 1 - Fin430 (Hup Seng Berhad)Document10 pagesAssignment 1 - Fin430 (Hup Seng Berhad)Qairunisa Mochsein100% (1)

- Accounting Assessment Report - Hup Seng Berhad & Hwa Tai IndustriesDocument16 pagesAccounting Assessment Report - Hup Seng Berhad & Hwa Tai IndustriesYoga ManiNo ratings yet

- Ashish Black BookDocument57 pagesAshish Black BookHamza FangariNo ratings yet

- Universal Robina Corporation: Prepared By: Garcia, Leriz Peñalosa, Rena Daniel Pescasio, LeonardDocument15 pagesUniversal Robina Corporation: Prepared By: Garcia, Leriz Peñalosa, Rena Daniel Pescasio, LeonardLeriz GarciaNo ratings yet

- Rasio Lancar: Nama:Intania Nim: A1C118086 Kelas: E Akuntansi Reguler Sore MK: Akt. Keuangan 1Document4 pagesRasio Lancar: Nama:Intania Nim: A1C118086 Kelas: E Akuntansi Reguler Sore MK: Akt. Keuangan 1Reza HijjulbaetNo ratings yet

- Assignment No. 02 SEMESTER Spring 2021 CS507-Information Systems Total Marks: 20Document5 pagesAssignment No. 02 SEMESTER Spring 2021 CS507-Information Systems Total Marks: 20UmairAfzalNo ratings yet

- 23090167@student Iumw Edu MyDocument18 pages23090167@student Iumw Edu MyShazryl Rifqi Shamsul NizamNo ratings yet

- GTC BS 22Document76 pagesGTC BS 22Ashwin NaveenNo ratings yet

- BTL tài chính doanh nghiệp mớiDocument19 pagesBTL tài chính doanh nghiệp mớiDo Hoang LanNo ratings yet

- COURSE CODE: ACC117/106/100 Declaration Form of Group AssignmentDocument9 pagesCOURSE CODE: ACC117/106/100 Declaration Form of Group AssignmentMARLINDAH RAHIMNo ratings yet

- Tugas Manajemen Keuangan Ayu Wulan Agustiyanti P32.2021.00805Document1 pageTugas Manajemen Keuangan Ayu Wulan Agustiyanti P32.2021.00805AYU WULAN AGUSTIYANTINo ratings yet

- ACCOUNTING Simulation Exercise DR RIMA - Coop Bank PertamaDocument9 pagesACCOUNTING Simulation Exercise DR RIMA - Coop Bank PertamaericdeskkuNo ratings yet

- 3-Ifn3 031210073 Assignment2Document9 pages3-Ifn3 031210073 Assignment2May MsNo ratings yet

- Profits and Gains of Business or ProfessionDocument2 pagesProfits and Gains of Business or ProfessionDaMoNNo ratings yet

- BC0150010 FM ProjectDocument12 pagesBC0150010 FM ProjectKrishnaNo ratings yet

- Fin242 Group AssignmentDocument14 pagesFin242 Group AssignmentNurul AzlinNo ratings yet

- Dutch Lady - Financial Ratio Analysis - Kba2431aDocument15 pagesDutch Lady - Financial Ratio Analysis - Kba2431aMOHAMAD IZZANI OTHMANNo ratings yet

- Ratio AnalysisDocument2 pagesRatio AnalysisShalehNo ratings yet

- Group Assignment Acc116Document9 pagesGroup Assignment Acc116Nurul AzlinNo ratings yet

- Accounting 2020 P1 MemoDocument11 pagesAccounting 2020 P1 MemoodiantumbaNo ratings yet

- Acc Proj PandaDocument23 pagesAcc Proj PandaFeilix BennyNo ratings yet

- Mineral Processing Engineers Seminars 2023 1671089455Document4 pagesMineral Processing Engineers Seminars 2023 1671089455SalomeyQuarshieNo ratings yet

- BhupiDocument251 pagesBhupiRaju PrasadNo ratings yet

- Smith and CPDocument3 pagesSmith and CPFirdausNo ratings yet

- Ratio Calculation - Financial ManagementDocument16 pagesRatio Calculation - Financial ManagementAinul MardhiahNo ratings yet

- Xyz Profitability Analysis: Creating A Profitable Direct Marketing Promotion Using CHAID SegmentationDocument6 pagesXyz Profitability Analysis: Creating A Profitable Direct Marketing Promotion Using CHAID SegmentationAlex TalloNo ratings yet

- Individual AssignmentDocument9 pagesIndividual AssignmentSITI NUR AISYAH MD ROSTANNo ratings yet

- 680-Twinkle Industry Balance Sheet 2021Document4 pages680-Twinkle Industry Balance Sheet 2021twinklesindNo ratings yet

- Accounting NSC P1 Memo Nov 2022 EngDocument12 pagesAccounting NSC P1 Memo Nov 2022 EngItumeleng MogoleNo ratings yet

- Kamre Aalam Balance Sheet - March-2022Document4 pagesKamre Aalam Balance Sheet - March-2022Parth KachhiyaNo ratings yet

- 2021-22 Accountancy Class Xii Sample ProjectDocument19 pages2021-22 Accountancy Class Xii Sample ProjectfarhaanNo ratings yet

- Rescued DocumentDocument9 pagesRescued Documentalihanaveed9No ratings yet

- TUGAS Analisis Laporan Keuangan KAI 2020Document8 pagesTUGAS Analisis Laporan Keuangan KAI 2020Rahma AgustinaNo ratings yet

- Project GuidelinesDocument19 pagesProject GuidelinesShown Shaji JosephNo ratings yet

- Worksheet DagangDocument10 pagesWorksheet DagangSetiandi RiswantoNo ratings yet

- Basic of FinanceDocument5 pagesBasic of FinanceKanitha MuniandyNo ratings yet

- Universiti Teknologi Mara - Examination ResultDocument1 pageUniversiti Teknologi Mara - Examination ResultShuhaina NizamNo ratings yet

- Afrin Shibu SB20CCM003 ProjectDocument79 pagesAfrin Shibu SB20CCM003 Projectabhishek628980No ratings yet

- Pensonic AsignmentDocument12 pagesPensonic AsignmentFaris HanisNo ratings yet

- An Introduction To ESG Reporting FrameworksDocument6 pagesAn Introduction To ESG Reporting FrameworksAblekkNo ratings yet

- Balancing Act: Managing The Public PurseDocument64 pagesBalancing Act: Managing The Public PurseGamers LKONo ratings yet

- A Study On Profitability AnalysisDocument48 pagesA Study On Profitability AnalysisDilip singhNo ratings yet

- Hul Annual Report 2018 19 - tcm1255 538867 - 1 - en PDFDocument228 pagesHul Annual Report 2018 19 - tcm1255 538867 - 1 - en PDFAkankshaNo ratings yet

- Company Profile: Company Name: Coal Bharat LimitedDocument34 pagesCompany Profile: Company Name: Coal Bharat Limitedshya1480No ratings yet

- ECO121 - Test 01 - Individual Assignment 01Document9 pagesECO121 - Test 01 - Individual Assignment 01Tran Binh Minh QP3195No ratings yet

- Double Question EssayDocument4 pagesDouble Question EssayLeyla MammadovaNo ratings yet

- Chapter 1 Introduction To Social EntrepreneurshipDocument11 pagesChapter 1 Introduction To Social EntrepreneurshipRamona Isabel UrsaisNo ratings yet

- BLM Gnf-Tc-Form-990-2020-2021-01Document63 pagesBLM Gnf-Tc-Form-990-2020-2021-01Jim HoftNo ratings yet

- Brand Audit - Final CaseDocument2 pagesBrand Audit - Final CaseDương Thị Tường VyNo ratings yet

- Marketing Research Fall 2022Document15 pagesMarketing Research Fall 2022ZUMARRAGA SAN MIGUEL AmaiaNo ratings yet

- Satisfaction Is Sure, Quality Is PureDocument18 pagesSatisfaction Is Sure, Quality Is PureSheryl BorromeoNo ratings yet

- The Complete Beginners Trading Guide - Trader's - SpotDocument73 pagesThe Complete Beginners Trading Guide - Trader's - Spothari100% (1)

- How A 16 YEAR OLD GIRL READINGDocument2 pagesHow A 16 YEAR OLD GIRL READINGMIREIA RIPOLL SOLERNo ratings yet

- Ims Operation Manual Purchase Department: Ivrcl Limited, HyderabadDocument14 pagesIms Operation Manual Purchase Department: Ivrcl Limited, HyderabadAkd DeshmukhNo ratings yet

- Easy Shop Plus Kick Off Tour - Werner - PH - Basic VersionDocument90 pagesEasy Shop Plus Kick Off Tour - Werner - PH - Basic VersionHazel L. ansulaNo ratings yet

- Mid Term Assignment k60 2021 1Document2 pagesMid Term Assignment k60 2021 1Thành Đạt NguyễnNo ratings yet

- Black & White Modern Design Project Proposal Document - 20240604 - 114746 - 0000Document4 pagesBlack & White Modern Design Project Proposal Document - 20240604 - 114746 - 0000Mr.H4No ratings yet

- Report On The Job TrainingDocument19 pagesReport On The Job TrainingRaisa RaisaNo ratings yet

- Execution Stage ActivitiesDocument1 pageExecution Stage ActivitieskapsarcNo ratings yet

- Business Chapter 2 BUSINESS STRUCTUREDocument7 pagesBusiness Chapter 2 BUSINESS STRUCTUREJosue MushagalusaNo ratings yet

- MGT 657: Strategic Management Individual Assignment ReportDocument6 pagesMGT 657: Strategic Management Individual Assignment Reportaisyah fadlyNo ratings yet

- Dilli Haat: Reviving Lost Glory: Submitted byDocument7 pagesDilli Haat: Reviving Lost Glory: Submitted byDaniyalNo ratings yet

- Industrial Policy Resolution 2022Document6 pagesIndustrial Policy Resolution 2022Pritam Umar K DasNo ratings yet

- Week 1 Introduction To Entrepreneurial CapitalDocument42 pagesWeek 1 Introduction To Entrepreneurial CapitalMichael AurynnNo ratings yet

- CapacityDocument19 pagesCapacityNitin KarnkaleNo ratings yet