Download as docx, pdf, or txt

You might also like

- SN325 Cal Ipr BLRDocument380 pagesSN325 Cal Ipr BLRLic-Carlos MoretaNo ratings yet

- AC7000 Nadcap Audit Criteria - Baseline Requirements, For Use On or After 19-Apr-2021Document6 pagesAC7000 Nadcap Audit Criteria - Baseline Requirements, For Use On or After 19-Apr-2021Vijay Yadav100% (2)

- Chapter 10-Understanding A Firm's Financial Statements: True/FalseDocument23 pagesChapter 10-Understanding A Firm's Financial Statements: True/FalseKhang ToNo ratings yet

- Sample Risk RegisterDocument19 pagesSample Risk RegisterRich De GuzmanNo ratings yet

- Student No. Full Name Campus Course: Pending CaseDocument66 pagesStudent No. Full Name Campus Course: Pending Casekapitannwel50% (2)

- Chemistry Investigatory Project On Bio-Diesel Made by Kamal/KishanDocument15 pagesChemistry Investigatory Project On Bio-Diesel Made by Kamal/KishanKishan Saluja76% (84)

- Appendix E1 - Internal Control Review 2023 (Ok)Document7 pagesAppendix E1 - Internal Control Review 2023 (Ok)Younes Abou El MakarimNo ratings yet

- Audit PlanDocument6 pagesAudit Plansyedumarahmed52No ratings yet

- Introduction and Learning Area 1Document31 pagesIntroduction and Learning Area 1w5q9brfkttNo ratings yet

- BJMQ 3113 Quality Management System FIRST SEMESTER 2020/2021 (A201) Individual Assignment Quality Management System Audit Group ADocument12 pagesBJMQ 3113 Quality Management System FIRST SEMESTER 2020/2021 (A201) Individual Assignment Quality Management System Audit Group AainaNo ratings yet

- Guide To Completing A SMETA CAPR 6.1Document29 pagesGuide To Completing A SMETA CAPR 6.1Alexchandar AnbalaganNo ratings yet

- Approved: Change Addition New Instruction Complete RevisionDocument5 pagesApproved: Change Addition New Instruction Complete RevisionDipuNo ratings yet

- Team Lead Core Banking and Other Ancillary Applications - Job Description UFUADocument3 pagesTeam Lead Core Banking and Other Ancillary Applications - Job Description UFUATanisha GargNo ratings yet

- Ip-04 Internal AuditDocument6 pagesIp-04 Internal AuditScha AffinNo ratings yet

- AUDIT 2 New Question PaperDocument9 pagesAUDIT 2 New Question Paperneha manglaniNo ratings yet

- SYS Procedure - Internal Quality Audit P1Document1 pageSYS Procedure - Internal Quality Audit P1sumanNo ratings yet

- Audit Report General & TechnicalDocument23 pagesAudit Report General & TechnicalNamra NaveedNo ratings yet

- ActionDocument4 pagesActionethan tardieuNo ratings yet

- Professional Standards: Chapter Welcome To Econ 132-AuditDocument4 pagesProfessional Standards: Chapter Welcome To Econ 132-Audityea okayNo ratings yet

- 9.2 Procedure For Internal AuditDocument5 pages9.2 Procedure For Internal AuditValantina JamilNo ratings yet

- Control of Non-Conforming Products & ServicesDocument6 pagesControl of Non-Conforming Products & ServicesJoshua ZapateroNo ratings yet

- Total Combined File-1Document36 pagesTotal Combined File-1Shefali TailorNo ratings yet

- BCTA2018 S1 AUE3701 Lecture-Notes Day-1 03032018-1-1Document35 pagesBCTA2018 S1 AUE3701 Lecture-Notes Day-1 03032018-1-1Tazlyn MarillierNo ratings yet

- 2019 Inspection Cohen & Company, LTD.: (Headquartered in Cleveland, Ohio)Document14 pages2019 Inspection Cohen & Company, LTD.: (Headquartered in Cleveland, Ohio)Jason BramwellNo ratings yet

- Finance Business Analyst JD J MandaDocument6 pagesFinance Business Analyst JD J MandaBenard ChimhondoNo ratings yet

- Running Head: Factors Which Influence Project SuccessDocument19 pagesRunning Head: Factors Which Influence Project Successbushra_faruq5377No ratings yet

- Audit of AdvancesDocument41 pagesAudit of AdvancesRupali GuptaNo ratings yet

- Planning Kaplan Chapter 6: Acca Paper F8 Int Audit and AssuranceDocument38 pagesPlanning Kaplan Chapter 6: Acca Paper F8 Int Audit and Assurancehaddad2020No ratings yet

- B PNP DRD CA2 Audit ReportDocument3 pagesB PNP DRD CA2 Audit ReportRaymond SmithNo ratings yet

- Follow Up of Internal Cost Recoveries Internal Audit Report 202021Document21 pagesFollow Up of Internal Cost Recoveries Internal Audit Report 202021christinahNo ratings yet

- Sample Win-Win Performance Review (Position Agreement)Document7 pagesSample Win-Win Performance Review (Position Agreement)JohnNo ratings yet

- AARS Practice QuestionsDocument211 pagesAARS Practice QuestionsChaudhury Ahmed HabibNo ratings yet

- (QSP-QMS-03) Process For Internal AuditDocument4 pages(QSP-QMS-03) Process For Internal AuditTanveer AhmadNo ratings yet

- Emirates Integrated Telecommunications Company PJSC and Its Subsidiaries Consolidated Financial Statements For The Year Ended 31 December 2020Document70 pagesEmirates Integrated Telecommunications Company PJSC and Its Subsidiaries Consolidated Financial Statements For The Year Ended 31 December 2020Vanshita SharmaNo ratings yet

- RBI Readiness ChecklistDocument2 pagesRBI Readiness ChecklistPeter IyereNo ratings yet

- Big Data - Work Program - 03 - Data Warehousing (10 24 2013)Document5 pagesBig Data - Work Program - 03 - Data Warehousing (10 24 2013)DefaultUsrNo ratings yet

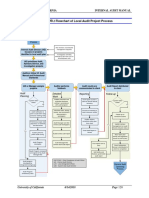

- 6000 Appendix 6000.: 2 Flowchart of Local Audit Project ProcessDocument1 page6000 Appendix 6000.: 2 Flowchart of Local Audit Project ProcessNiken RindasariNo ratings yet

- BIA Methodology - Sample Executive Summary - CDocument21 pagesBIA Methodology - Sample Executive Summary - CMondher GamNo ratings yet

- Template ProjectplanDocument33 pagesTemplate ProjectplanĐạt Vũ0% (1)

- CO - Internal OrdersDocument7 pagesCO - Internal OrdersVishal YadavNo ratings yet

- 2017 IAWebinarSeries Course-2 ReducingTheBurdenOfSOXCompliance 042517Document19 pages2017 IAWebinarSeries Course-2 ReducingTheBurdenOfSOXCompliance 042517Sergio VinsennauNo ratings yet

- Audit and Assurance Answers: Professional Level Examination JUNE 2016 Mock Exam 1Document20 pagesAudit and Assurance Answers: Professional Level Examination JUNE 2016 Mock Exam 1Madalitso MbeweNo ratings yet

- Introduction and Background 2023 - SunlearnDocument34 pagesIntroduction and Background 2023 - Sunlearnwww.lekgaumosa7No ratings yet

- Account and Finance Departmental ObjectiveDocument7 pagesAccount and Finance Departmental ObjectiveVICTORNo ratings yet

- Emirates Integrated Telecommunications Company PJSC and Its Subsidiaries Consolidated Financial Statements For The Year Ended 31 December 2021Document73 pagesEmirates Integrated Telecommunications Company PJSC and Its Subsidiaries Consolidated Financial Statements For The Year Ended 31 December 2021Vanshita SharmaNo ratings yet

- Resume MJDocument3 pagesResume MJAnuradha SriramNo ratings yet

- ZAA424631821 - Indesore Sweater LTD - Periodic - SMETA 4 Pillars - 26 Jul 23 - CAPRDocument14 pagesZAA424631821 - Indesore Sweater LTD - Periodic - SMETA 4 Pillars - 26 Jul 23 - CAPRmd.kajalbdNo ratings yet

- Business Continuity and Information Security - An Excellent Fit - Ramesh Ramani - LRQADocument22 pagesBusiness Continuity and Information Security - An Excellent Fit - Ramesh Ramani - LRQAchanchal100% (1)

- l20 To l21 - ControllingDocument68 pagesl20 To l21 - ControllinganvipotnisNo ratings yet

- General Instruction ManualDocument7 pagesGeneral Instruction ManualAkash K NairNo ratings yet

- Appraisal Form 2019-2020Document4 pagesAppraisal Form 2019-2020manishNo ratings yet

- Aui3701 Exam 2020Document6 pagesAui3701 Exam 2020tinyikodiscussNo ratings yet

- AP BizPlan - 1 Table of Content & RequirementsDocument24 pagesAP BizPlan - 1 Table of Content & RequirementsHakeem AdesanyaNo ratings yet

- STL PAF Guidelines For Performance Based Bonus FY 2022 0Document8 pagesSTL PAF Guidelines For Performance Based Bonus FY 2022 0HEALTH SERVICE CENTER - CENTRALNo ratings yet

- Financial StatementsDocument81 pagesFinancial StatementsArjun S KumarNo ratings yet

- Resume of M.a.yousufDocument4 pagesResume of M.a.yousufRobal MiahNo ratings yet

- Capr Zaa600007132Document12 pagesCapr Zaa600007132alexis bustinza castilloNo ratings yet

- Accelerated Zero Based Budgeting: Identify and Implement Quickly Up To 25% of AgilityDocument7 pagesAccelerated Zero Based Budgeting: Identify and Implement Quickly Up To 25% of AgilityInácio CogeNo ratings yet

- General Instruction Manual: Accounting For The Costs of Computer Software Developed or Obtained For Internal Use ContentDocument9 pagesGeneral Instruction Manual: Accounting For The Costs of Computer Software Developed or Obtained For Internal Use ContentDipuNo ratings yet

- Supplier Audits and SurveysDocument13 pagesSupplier Audits and SurveysBighneswar PatraNo ratings yet

- Greater Male WTE ADBDocument15 pagesGreater Male WTE ADBTamara RachimNo ratings yet

- C11 Audit Question BankDocument20 pagesC11 Audit Question BankYash SharmaNo ratings yet

- Information Systems Auditing: The IS Audit Planning ProcessFrom EverandInformation Systems Auditing: The IS Audit Planning ProcessRating: 3.5 out of 5 stars3.5/5 (2)

- IFRS 16: Lessor & Lessee Accounting Treatment in The Finance LeaseDocument2 pagesIFRS 16: Lessor & Lessee Accounting Treatment in The Finance LeaseboygarfanNo ratings yet

- Data Integrity TemplateDocument4 pagesData Integrity TemplateboygarfanNo ratings yet

- GCC Ia Ia Rev.00.24Document3 pagesGCC Ia Ia Rev.00.24boygarfanNo ratings yet

- 1122 482 2019-02-14 15-47-38 enDocument17 pages1122 482 2019-02-14 15-47-38 enboygarfanNo ratings yet

- Mss-Netherlands enDocument16 pagesMss-Netherlands enboygarfanNo ratings yet

- Green Concrete Company ProfileDocument79 pagesGreen Concrete Company ProfileboygarfanNo ratings yet

- 10 DifferencesDocument1 page10 DifferencesboygarfanNo ratings yet

- 1122 482 2019-02-14 15-47-38 enDocument16 pages1122 482 2019-02-14 15-47-38 enboygarfanNo ratings yet

- Snatch Theft Prevention TipsDocument1 pageSnatch Theft Prevention TipsDon McleanNo ratings yet

- Handbook - Curtin UniversityDocument12 pagesHandbook - Curtin UniversityJuni KasthakarNo ratings yet

- GCSE Literature SyllabusDocument29 pagesGCSE Literature SyllabusJooby77No ratings yet

- CSMI v. TrinityDocument22 pagesCSMI v. TrinityCTV OttawaNo ratings yet

- R Walters MimiDocument19 pagesR Walters MimiCalWonkNo ratings yet

- EL - 124 Electronic Devices & Circuits: Experiment # 04Document6 pagesEL - 124 Electronic Devices & Circuits: Experiment # 04Jawwad IqbalNo ratings yet

- Yom Ha'atzmaut Missing Letters: Fill in The Missing Letters To Complete The WordsDocument34 pagesYom Ha'atzmaut Missing Letters: Fill in The Missing Letters To Complete The WordsRachel MalagaNo ratings yet

- Evolution of Advertisement and Misleading Advertisement in Indian Context Mr. Ajay Krishna PandeyDocument16 pagesEvolution of Advertisement and Misleading Advertisement in Indian Context Mr. Ajay Krishna PandeyMahender SinghNo ratings yet

- Institute of Cost and Management Accountants of Pakistan Spring (August) 2012 ExaminationsDocument2 pagesInstitute of Cost and Management Accountants of Pakistan Spring (August) 2012 ExaminationsAmmar KashanNo ratings yet

- Airplane Flight Manual Supplement: Gps/Waas Nav ComDocument7 pagesAirplane Flight Manual Supplement: Gps/Waas Nav Comraisul dianaNo ratings yet

- Business Objectives and Stakeholder ObjectivesDocument28 pagesBusiness Objectives and Stakeholder ObjectivesThin Zar Tin WinNo ratings yet

- Reading Comprehension WorksheetDocument10 pagesReading Comprehension WorksheetJherick TacderasNo ratings yet

- Student Tox LectureDocument49 pagesStudent Tox Lecturelenin_villaltaNo ratings yet

- Lecture Notes: A Powerpoint PresentationDocument105 pagesLecture Notes: A Powerpoint PresentationDutchsMoin Mohammad100% (1)

- IMO Shortlist 2010Document72 pagesIMO Shortlist 2010Florina TomaNo ratings yet

- Homonyms PDFDocument34 pagesHomonyms PDFNanaimha50% (2)

- Pee BuddyDocument11 pagesPee Buddychitta4iterNo ratings yet

- Ic 2003Document21 pagesIc 2003Dinesh KumarNo ratings yet

- Second Year Mba Syllabus (Only Electives) Third Semester Functional Area: MarketingDocument21 pagesSecond Year Mba Syllabus (Only Electives) Third Semester Functional Area: MarketingSatya ReddyNo ratings yet

- REFUSE DISPOSAL 2016 EdDocument54 pagesREFUSE DISPOSAL 2016 EdEmmanuel P DubeNo ratings yet

- (Isi) Task1Document22 pages(Isi) Task1hidayatiamminyNo ratings yet

- LP SampleDocument12 pagesLP SampleFayeNo ratings yet

- Seismic Upgrade of Existing Buildings With Fluid Viscous Dampers: Design Methodologies and Case StudyDocument12 pagesSeismic Upgrade of Existing Buildings With Fluid Viscous Dampers: Design Methodologies and Case StudyHimanshu WasterNo ratings yet

- Brad J Hornberger Cystoscopy Indications and Preparation. UAPA CME Conference 2012 (30 Min)Document36 pagesBrad J Hornberger Cystoscopy Indications and Preparation. UAPA CME Conference 2012 (30 Min)Cristian OrozcoNo ratings yet

- C++ Exercises IIDocument4 pagesC++ Exercises IIZaid Al-Ali50% (2)

- BUS Chap 1 PDF 1Document17 pagesBUS Chap 1 PDF 1Tamanna Sharmin ChowdhuryNo ratings yet