0522 Financial Investments UNIT 7

0522 Financial Investments UNIT 7

You might also like

- Portfolio Construction Using Fundamental AnalysisDocument97 pagesPortfolio Construction Using Fundamental Analysisefreggg100% (2)

- Portfolio Risk and ReturnDocument7 pagesPortfolio Risk and ReturnNga NguyễnNo ratings yet

- Smaliraza - 3622 - 18945 - 1 - Lecture 9 - Investement Ana & Portfolio ManagementDocument13 pagesSmaliraza - 3622 - 18945 - 1 - Lecture 9 - Investement Ana & Portfolio ManagementSadia AbidNo ratings yet

- Business School: Risk and Actuarial StudiesDocument37 pagesBusiness School: Risk and Actuarial StudiesBobNo ratings yet

- CH 6 Fundamental Analysis - 2Document39 pagesCH 6 Fundamental Analysis - 2Amit PandeyNo ratings yet

- 2023 03 23 1142 - UL No Notes No Coms - Capital Asset Pricing Model - Part 1 - Lec 1Document46 pages2023 03 23 1142 - UL No Notes No Coms - Capital Asset Pricing Model - Part 1 - Lec 1詹博智No ratings yet

- Risk and Return: Estimating Cost of Capital: R R E R R EDocument14 pagesRisk and Return: Estimating Cost of Capital: R R E R R EKavya posanNo ratings yet

- Asset PricingDocument23 pagesAsset PricingBrian DhliwayoNo ratings yet

- 98 Sapm-01Document7 pages98 Sapm-01KetakiNo ratings yet

- Unit 02 The Financial Environment-2Document9 pagesUnit 02 The Financial Environment-2Ruthira Nair AB KrishenanNo ratings yet

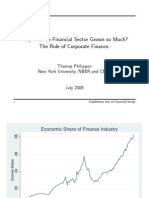

- Why Has The Financial Sector Grown So Much? The Role of Corporate FinanceDocument43 pagesWhy Has The Financial Sector Grown So Much? The Role of Corporate FinanceParul MahajanNo ratings yet

- Private Equity Real Estate: NorthfieldDocument26 pagesPrivate Equity Real Estate: NorthfieldchrisjohnlopezNo ratings yet

- Active Portfolio Management: NoteDocument31 pagesActive Portfolio Management: NoteNitiNo ratings yet

- Analysis of Systematic and Unsystematic Risks in CapitalDocument18 pagesAnalysis of Systematic and Unsystematic Risks in CapitalNishant Edwin PaschalNo ratings yet

- Perf Assignment 1Document7 pagesPerf Assignment 1Blessed NyamaNo ratings yet

- 5 - Asset Pricing ModelsDocument56 pages5 - Asset Pricing ModelsCrimson OwlNo ratings yet

- Group:-Neeraj Kumar Saurabh Jain Prestege Varghese John Raj Kishore Rahul PariharDocument25 pagesGroup:-Neeraj Kumar Saurabh Jain Prestege Varghese John Raj Kishore Rahul PariharAmit Kumar JhaNo ratings yet

- Por To FolioDocument27 pagesPor To Folioharsh_k619No ratings yet

- CPA Core 2Document35 pagesCPA Core 2obamadexNo ratings yet

- Synopsis Taxfghfh Saving Mutual FundsDocument8 pagesSynopsis Taxfghfh Saving Mutual FundsSaidi ReddyNo ratings yet

- Investment ManagementDocument38 pagesInvestment ManagementPranjit BhuyanNo ratings yet

- Basic Concepts: Mba Iii SemesterDocument11 pagesBasic Concepts: Mba Iii SemesterDrDhananjhay GangineniNo ratings yet

- Active Portfolio ManagementDocument31 pagesActive Portfolio ManagementkwongNo ratings yet

- Capital Asset Pricing ModelDocument10 pagesCapital Asset Pricing ModelLiezel AgloboNo ratings yet

- trắc nghiệmDocument6 pagestrắc nghiệmuyenvtt2002No ratings yet

- Unit 5Document32 pagesUnit 5Wgt ChampNo ratings yet

- Financial Management Ca2Document10 pagesFinancial Management Ca2saptadeep.saha26baNo ratings yet

- Single Index ModelDocument14 pagesSingle Index ModelBikram MaharjanNo ratings yet

- The Investment CAPM: Author: Lu Zhang Journal: European Financial Management (2017)Document23 pagesThe Investment CAPM: Author: Lu Zhang Journal: European Financial Management (2017)Nikhil VidhaniNo ratings yet

- 2830203-Security Analysis and Portfolio ManagementDocument2 pages2830203-Security Analysis and Portfolio ManagementbhumikajasaniNo ratings yet

- APT-What Is It? Estimating and Testing APT Apt and Capm ConclusionDocument19 pagesAPT-What Is It? Estimating and Testing APT Apt and Capm ConclusionMariya FilimonovaNo ratings yet

- Unit 2 (Fundamental Analysis)Document19 pagesUnit 2 (Fundamental Analysis)Ramya RamamurthyNo ratings yet

- Arbitrage Pricing TheoryDocument21 pagesArbitrage Pricing TheoryVaidyanathan RavichandranNo ratings yet

- A Course On Finance of Insurance Vol 1Document84 pagesA Course On Finance of Insurance Vol 1ulfa dianitaNo ratings yet

- SIngle Index MethodDocument17 pagesSIngle Index Methodamericus_smile7474No ratings yet

- Index Models.Document26 pagesIndex Models.Ishtiaq Hasnat Chowdhury RatulNo ratings yet

- Econf412 Finf313 Mids SDocument11 pagesEconf412 Finf313 Mids SArchita SrivastavaNo ratings yet

- Financial Risk Management 1Document103 pagesFinancial Risk Management 1Mugdha PatilNo ratings yet

- Portfolio Choice: Factor Models and Arbitrage Pricing TheoryDocument23 pagesPortfolio Choice: Factor Models and Arbitrage Pricing TheoryDarrell PassigueNo ratings yet

- 2023 JA - FM Suggested AnswersDocument12 pages2023 JA - FM Suggested Answersmiradvance studyNo ratings yet

- Chapter 5 Economic AnalysisDocument15 pagesChapter 5 Economic Analysisabera assefaNo ratings yet

- SAPM Assignment-Ayush GoyalDocument10 pagesSAPM Assignment-Ayush Goyalkartikay GulaniNo ratings yet

- Resume CH 7 - 0098 - 0326Document5 pagesResume CH 7 - 0098 - 0326nur eka ayu danaNo ratings yet

- Single Index ModelDocument1 pageSingle Index ModelIshtiaq Hasnat Chowdhury RatulNo ratings yet

- Cost of Capital, WACC and BetaDocument3 pagesCost of Capital, WACC and BetaSenith111No ratings yet

- Economics Definitions: Chapter 1: Goals of The FirmDocument12 pagesEconomics Definitions: Chapter 1: Goals of The FirmNoel FitzgeraldNo ratings yet

- Econf412 Finf313 Comp QDocument6 pagesEconf412 Finf313 Comp Qbits.goa2027No ratings yet

- Observed Dividend Policy PatternsDocument1 pageObserved Dividend Policy PatternsIrfan U ShahNo ratings yet

- FAR Notes-DoneDocument122 pagesFAR Notes-DoneJovylyn Balbines LictagNo ratings yet

- IPM - Written Report - TinioDocument8 pagesIPM - Written Report - Tiniogilbertson tinioNo ratings yet

- FM QP KeyDocument19 pagesFM QP KeyporseenaNo ratings yet

- Diversification of RisksDocument14 pagesDiversification of RisksManisha MehtaNo ratings yet

- Security Analysis Bba-Iv (Elective Finance)Document21 pagesSecurity Analysis Bba-Iv (Elective Finance)Bahawal Khan JamaliNo ratings yet

- 9 Week of Lectures: Financial Management - MGT201Document13 pages9 Week of Lectures: Financial Management - MGT201Syed Abdul Mussaver ShahNo ratings yet

- Topic 2.2 Portfolio Theory 2Document29 pagesTopic 2.2 Portfolio Theory 2caroNo ratings yet

- Single Index ModelDocument17 pagesSingle Index ModelWawan Goendoel100% (3)

- MINGGU 13 & 14: Manajemen Keuangan IiDocument24 pagesMINGGU 13 & 14: Manajemen Keuangan IiHadi TheoNo ratings yet

- CFA III-Asset Allocation关键词清单Document27 pagesCFA III-Asset Allocation关键词清单Lê Chấn PhongNo ratings yet

- Questions 1 - 6 Pertain To The Case Study Each Question Should Be Answered IndependentlyDocument22 pagesQuestions 1 - 6 Pertain To The Case Study Each Question Should Be Answered IndependentlyNoura ShamseddineNo ratings yet

- Investments Profitability, Time Value & Risk Analysis: Guidelines for Individuals and CorporationsFrom EverandInvestments Profitability, Time Value & Risk Analysis: Guidelines for Individuals and CorporationsNo ratings yet

Download as pdf or txt

You might also like

- Portfolio Construction Using Fundamental AnalysisDocument97 pagesPortfolio Construction Using Fundamental Analysisefreggg100% (2)

- Portfolio Risk and ReturnDocument7 pagesPortfolio Risk and ReturnNga NguyễnNo ratings yet

- Smaliraza - 3622 - 18945 - 1 - Lecture 9 - Investement Ana & Portfolio ManagementDocument13 pagesSmaliraza - 3622 - 18945 - 1 - Lecture 9 - Investement Ana & Portfolio ManagementSadia AbidNo ratings yet

- Business School: Risk and Actuarial StudiesDocument37 pagesBusiness School: Risk and Actuarial StudiesBobNo ratings yet

- CH 6 Fundamental Analysis - 2Document39 pagesCH 6 Fundamental Analysis - 2Amit PandeyNo ratings yet

- 2023 03 23 1142 - UL No Notes No Coms - Capital Asset Pricing Model - Part 1 - Lec 1Document46 pages2023 03 23 1142 - UL No Notes No Coms - Capital Asset Pricing Model - Part 1 - Lec 1詹博智No ratings yet

- Risk and Return: Estimating Cost of Capital: R R E R R EDocument14 pagesRisk and Return: Estimating Cost of Capital: R R E R R EKavya posanNo ratings yet

- Asset PricingDocument23 pagesAsset PricingBrian DhliwayoNo ratings yet

- 98 Sapm-01Document7 pages98 Sapm-01KetakiNo ratings yet

- Unit 02 The Financial Environment-2Document9 pagesUnit 02 The Financial Environment-2Ruthira Nair AB KrishenanNo ratings yet

- Why Has The Financial Sector Grown So Much? The Role of Corporate FinanceDocument43 pagesWhy Has The Financial Sector Grown So Much? The Role of Corporate FinanceParul MahajanNo ratings yet

- Private Equity Real Estate: NorthfieldDocument26 pagesPrivate Equity Real Estate: NorthfieldchrisjohnlopezNo ratings yet

- Active Portfolio Management: NoteDocument31 pagesActive Portfolio Management: NoteNitiNo ratings yet

- Analysis of Systematic and Unsystematic Risks in CapitalDocument18 pagesAnalysis of Systematic and Unsystematic Risks in CapitalNishant Edwin PaschalNo ratings yet

- Perf Assignment 1Document7 pagesPerf Assignment 1Blessed NyamaNo ratings yet

- 5 - Asset Pricing ModelsDocument56 pages5 - Asset Pricing ModelsCrimson OwlNo ratings yet

- Group:-Neeraj Kumar Saurabh Jain Prestege Varghese John Raj Kishore Rahul PariharDocument25 pagesGroup:-Neeraj Kumar Saurabh Jain Prestege Varghese John Raj Kishore Rahul PariharAmit Kumar JhaNo ratings yet

- Por To FolioDocument27 pagesPor To Folioharsh_k619No ratings yet

- CPA Core 2Document35 pagesCPA Core 2obamadexNo ratings yet

- Synopsis Taxfghfh Saving Mutual FundsDocument8 pagesSynopsis Taxfghfh Saving Mutual FundsSaidi ReddyNo ratings yet

- Investment ManagementDocument38 pagesInvestment ManagementPranjit BhuyanNo ratings yet

- Basic Concepts: Mba Iii SemesterDocument11 pagesBasic Concepts: Mba Iii SemesterDrDhananjhay GangineniNo ratings yet

- Active Portfolio ManagementDocument31 pagesActive Portfolio ManagementkwongNo ratings yet

- Capital Asset Pricing ModelDocument10 pagesCapital Asset Pricing ModelLiezel AgloboNo ratings yet

- trắc nghiệmDocument6 pagestrắc nghiệmuyenvtt2002No ratings yet

- Unit 5Document32 pagesUnit 5Wgt ChampNo ratings yet

- Financial Management Ca2Document10 pagesFinancial Management Ca2saptadeep.saha26baNo ratings yet

- Single Index ModelDocument14 pagesSingle Index ModelBikram MaharjanNo ratings yet

- The Investment CAPM: Author: Lu Zhang Journal: European Financial Management (2017)Document23 pagesThe Investment CAPM: Author: Lu Zhang Journal: European Financial Management (2017)Nikhil VidhaniNo ratings yet

- 2830203-Security Analysis and Portfolio ManagementDocument2 pages2830203-Security Analysis and Portfolio ManagementbhumikajasaniNo ratings yet

- APT-What Is It? Estimating and Testing APT Apt and Capm ConclusionDocument19 pagesAPT-What Is It? Estimating and Testing APT Apt and Capm ConclusionMariya FilimonovaNo ratings yet

- Unit 2 (Fundamental Analysis)Document19 pagesUnit 2 (Fundamental Analysis)Ramya RamamurthyNo ratings yet

- Arbitrage Pricing TheoryDocument21 pagesArbitrage Pricing TheoryVaidyanathan RavichandranNo ratings yet

- A Course On Finance of Insurance Vol 1Document84 pagesA Course On Finance of Insurance Vol 1ulfa dianitaNo ratings yet

- SIngle Index MethodDocument17 pagesSIngle Index Methodamericus_smile7474No ratings yet

- Index Models.Document26 pagesIndex Models.Ishtiaq Hasnat Chowdhury RatulNo ratings yet

- Econf412 Finf313 Mids SDocument11 pagesEconf412 Finf313 Mids SArchita SrivastavaNo ratings yet

- Financial Risk Management 1Document103 pagesFinancial Risk Management 1Mugdha PatilNo ratings yet

- Portfolio Choice: Factor Models and Arbitrage Pricing TheoryDocument23 pagesPortfolio Choice: Factor Models and Arbitrage Pricing TheoryDarrell PassigueNo ratings yet

- 2023 JA - FM Suggested AnswersDocument12 pages2023 JA - FM Suggested Answersmiradvance studyNo ratings yet

- Chapter 5 Economic AnalysisDocument15 pagesChapter 5 Economic Analysisabera assefaNo ratings yet

- SAPM Assignment-Ayush GoyalDocument10 pagesSAPM Assignment-Ayush Goyalkartikay GulaniNo ratings yet

- Resume CH 7 - 0098 - 0326Document5 pagesResume CH 7 - 0098 - 0326nur eka ayu danaNo ratings yet

- Single Index ModelDocument1 pageSingle Index ModelIshtiaq Hasnat Chowdhury RatulNo ratings yet

- Cost of Capital, WACC and BetaDocument3 pagesCost of Capital, WACC and BetaSenith111No ratings yet

- Economics Definitions: Chapter 1: Goals of The FirmDocument12 pagesEconomics Definitions: Chapter 1: Goals of The FirmNoel FitzgeraldNo ratings yet

- Econf412 Finf313 Comp QDocument6 pagesEconf412 Finf313 Comp Qbits.goa2027No ratings yet

- Observed Dividend Policy PatternsDocument1 pageObserved Dividend Policy PatternsIrfan U ShahNo ratings yet

- FAR Notes-DoneDocument122 pagesFAR Notes-DoneJovylyn Balbines LictagNo ratings yet

- IPM - Written Report - TinioDocument8 pagesIPM - Written Report - Tiniogilbertson tinioNo ratings yet

- FM QP KeyDocument19 pagesFM QP KeyporseenaNo ratings yet

- Diversification of RisksDocument14 pagesDiversification of RisksManisha MehtaNo ratings yet

- Security Analysis Bba-Iv (Elective Finance)Document21 pagesSecurity Analysis Bba-Iv (Elective Finance)Bahawal Khan JamaliNo ratings yet

- 9 Week of Lectures: Financial Management - MGT201Document13 pages9 Week of Lectures: Financial Management - MGT201Syed Abdul Mussaver ShahNo ratings yet

- Topic 2.2 Portfolio Theory 2Document29 pagesTopic 2.2 Portfolio Theory 2caroNo ratings yet

- Single Index ModelDocument17 pagesSingle Index ModelWawan Goendoel100% (3)

- MINGGU 13 & 14: Manajemen Keuangan IiDocument24 pagesMINGGU 13 & 14: Manajemen Keuangan IiHadi TheoNo ratings yet

- CFA III-Asset Allocation关键词清单Document27 pagesCFA III-Asset Allocation关键词清单Lê Chấn PhongNo ratings yet

- Questions 1 - 6 Pertain To The Case Study Each Question Should Be Answered IndependentlyDocument22 pagesQuestions 1 - 6 Pertain To The Case Study Each Question Should Be Answered IndependentlyNoura ShamseddineNo ratings yet

- Investments Profitability, Time Value & Risk Analysis: Guidelines for Individuals and CorporationsFrom EverandInvestments Profitability, Time Value & Risk Analysis: Guidelines for Individuals and CorporationsNo ratings yet