Download as pdf or txt

You might also like

- Case Assignment 8 - Diamond Energy Resources PDFDocument3 pagesCase Assignment 8 - Diamond Energy Resources PDFAudrey Ang100% (1)

- The Impact of Forward and Backward Integration On Microsoft S Performance and Sustainability in AmericaDocument32 pagesThe Impact of Forward and Backward Integration On Microsoft S Performance and Sustainability in Americakariuki josephNo ratings yet

- Bantay KorapsyonDocument18 pagesBantay KorapsyonRheinhart PahilaNo ratings yet

- 2021-09-01 Elle UKDocument224 pages2021-09-01 Elle UKLilith100% (2)

- SANAR Investment Proposition 260421Document18 pagesSANAR Investment Proposition 260421swopnilrNo ratings yet

- Ethical Expectations: Employers & EmployeesDocument16 pagesEthical Expectations: Employers & EmployeesArpita Dhar TamaNo ratings yet

- Workday Interviews Q & ADocument155 pagesWorkday Interviews Q & AMahesh Chikoti56% (9)

- APREIT 2015 03 Investor PresentationDocument55 pagesAPREIT 2015 03 Investor PresentationRobin van ReFyNo ratings yet

- Pay Rates & Allowances Motion Picture Production Collective AgreementDocument8 pagesPay Rates & Allowances Motion Picture Production Collective AgreementKyle WatsonNo ratings yet

- Solar Tornado International LLC - Feasibility Report - ExecutiveDocument5 pagesSolar Tornado International LLC - Feasibility Report - ExecutivedprosenjitNo ratings yet

- TanishqDocument49 pagesTanishqAditya Chaturvedi0% (2)

- Vineta PriyaDocument10 pagesVineta PriyaPriya SahniNo ratings yet

- Annual Report2018 PDFDocument282 pagesAnnual Report2018 PDFadnanNo ratings yet

- MFM-Annual Report (53-204) PDFDocument153 pagesMFM-Annual Report (53-204) PDFZikri ZainuddinNo ratings yet

- Hikkaduwa Beach Resorts PLC and Waskaduwa Beach Resorts PLCDocument17 pagesHikkaduwa Beach Resorts PLC and Waskaduwa Beach Resorts PLCreshadNo ratings yet

- Checklist - Roto Pumps Limited FY 18-19Document6 pagesChecklist - Roto Pumps Limited FY 18-19Shubham SinuNo ratings yet

- CRDB Bank Annual Report-2009Document138 pagesCRDB Bank Annual Report-2009John SekaNo ratings yet

- Equity Tips Recommendation and Analysis For The 04 JuneDocument7 pagesEquity Tips Recommendation and Analysis For The 04 JuneTheequicom AdvisoryNo ratings yet

- WEB Smart House Presntetion 2Document28 pagesWEB Smart House Presntetion 2Mehari GebreyohannesNo ratings yet

- Comprofile2 PDFDocument41 pagesComprofile2 PDFAkeem AlteranNo ratings yet

- MarineDocument33 pagesMarineAnonymous Feglbx5No ratings yet

- Section 2 0 Current Carrying Capacity of BusbarsDocument13 pagesSection 2 0 Current Carrying Capacity of BusbarsCarlos ChalcoNo ratings yet

- Project Assignment For Lean Six Sigma Class of 2017 Industrial and Systems Engineering & Business ManagementDocument7 pagesProject Assignment For Lean Six Sigma Class of 2017 Industrial and Systems Engineering & Business ManagementAparjeet KaushalNo ratings yet

- Trading Index Dividends: Junhua Lu, Phd. CFADocument19 pagesTrading Index Dividends: Junhua Lu, Phd. CFAMatthew BurkeNo ratings yet

- Ezz Steel Report.eDocument14 pagesEzz Steel Report.eIsrael Sodium JobNo ratings yet

- Article Portfolio ManagementDocument5 pagesArticle Portfolio ManagementadityaNo ratings yet

- 6 Business Risk SampleDocument3 pages6 Business Risk SampleMushtaq AhmadNo ratings yet

- PTS Morning Call 12-14-09Document4 pagesPTS Morning Call 12-14-09PrismtradingschoolNo ratings yet

- Coworking Preview FDocument129 pagesCoworking Preview FNicolas JaramilloNo ratings yet

- TEMPLATE DCF Made Simple by Kefas EvanderDocument32 pagesTEMPLATE DCF Made Simple by Kefas EvanderMuhammad RizaldiNo ratings yet

- Discount Factor TemplateDocument5 pagesDiscount Factor TemplateRashan Jida Reshan100% (1)

- Opportunity Stages Forecasting: What Is Sales Forecasting?Document6 pagesOpportunity Stages Forecasting: What Is Sales Forecasting?Aleema KhanNo ratings yet

- Today's Equity Market Report and Equity Tips 15 MayDocument7 pagesToday's Equity Market Report and Equity Tips 15 MayTheequicom AdvisoryNo ratings yet

- Amtek Ratios 1Document18 pagesAmtek Ratios 1Dr Sakshi SharmaNo ratings yet

- Valuation For Nestlé Lanka PLCDocument20 pagesValuation For Nestlé Lanka PLCErandika Lakmali GamageNo ratings yet

- The ANZ 2012 Asia Investor TourDocument118 pagesThe ANZ 2012 Asia Investor Tourkarlng167No ratings yet

- Final ProposalDocument24 pagesFinal ProposalFalfa PacinoNo ratings yet

- My Current Portfolio SahamDocument1 pageMy Current Portfolio Sahamshahfiq95 1210No ratings yet

- Fluxo de Investidores Estrangeiro - 2.5.2024Document3 pagesFluxo de Investidores Estrangeiro - 2.5.2024Daniel LimaNo ratings yet

- TYDFL Marketing ProfileDocument1 pageTYDFL Marketing ProfileSoyeb HassanNo ratings yet

- Annual Report - 2020 - Linde Bangladesh BOCDocument90 pagesAnnual Report - 2020 - Linde Bangladesh BOCAtiqul islamNo ratings yet

- DRM - Handouts (1) 2Document54 pagesDRM - Handouts (1) 2tanshlinkedinNo ratings yet

- Segment & Interim ReportDocument12 pagesSegment & Interim ReportMuhammad ZulhisyamNo ratings yet

- Your Policy No. 144808 / 53-IPDocument2 pagesYour Policy No. 144808 / 53-IPtanveer.randhawa25No ratings yet

- Revised Alfalah Solar Financing - Mr. JahanzaibDocument3 pagesRevised Alfalah Solar Financing - Mr. JahanzaibChaudhary Muhammad Suban TasirNo ratings yet

- Irp Adani FinalDocument4 pagesIrp Adani Finalharsh kaushikNo ratings yet

- Production of Pearl Caustic Soda-653343 PDFDocument62 pagesProduction of Pearl Caustic Soda-653343 PDFhardajhbfNo ratings yet

- R DJ Raymond James 32 Annual Institutional Investors Conference Orlando Florida Orlando, Florida March 7, 2011Document38 pagesR DJ Raymond James 32 Annual Institutional Investors Conference Orlando Florida Orlando, Florida March 7, 2011nrao123No ratings yet

- Pharmaceutical Industry: Krithika SubramaniamDocument4 pagesPharmaceutical Industry: Krithika Subramaniamkrithika_tataNo ratings yet

- Formulae and Discount Tables: Professional Level Examination Financial ManagementDocument2 pagesFormulae and Discount Tables: Professional Level Examination Financial ManagementClaudine CjNo ratings yet

- 2015 Garage EquipementDocument35 pages2015 Garage EquipementSolomon WaldemariamNo ratings yet

- Aisha Final Enterpreneurship ReportDocument6 pagesAisha Final Enterpreneurship Reportaisha malikNo ratings yet

- Dawood Bank June 2005Document98 pagesDawood Bank June 2005mukarram123No ratings yet

- Prism Morning Call 11-17-2009Document4 pagesPrism Morning Call 11-17-2009PrismtradingschoolNo ratings yet

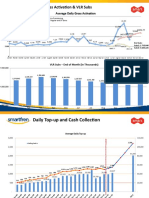

- Daily Gross Activation & VLR SubsDocument3 pagesDaily Gross Activation & VLR Subsdarwin.saragihNo ratings yet

- AMTEXDocument87 pagesAMTEXBilal Ahmed KhanNo ratings yet

- Company Information: Board of DirectorsDocument12 pagesCompany Information: Board of Directors03004523983No ratings yet

- Depreciation Drilling Rigs Esv2008Document108 pagesDepreciation Drilling Rigs Esv2008corsini999No ratings yet

- SodapdfDocument13 pagesSodapdfvithacitra engineeringNo ratings yet

- Annual Report2017Document278 pagesAnnual Report2017Jafar IqbalNo ratings yet

- Liquid Urea-Formaldehyde Resin Manufacturing Industry-217599 - 4Document65 pagesLiquid Urea-Formaldehyde Resin Manufacturing Industry-217599 - 4Sanzar Rahman 1621555030No ratings yet

- Satish Kumar Chelladurai: Ugro Capital LimitedDocument8 pagesSatish Kumar Chelladurai: Ugro Capital LimitedBrojo Gopal GhoshNo ratings yet

- Illustration ApaDocument1 pageIllustration ApaShub KumarNo ratings yet

- GAY DEL: TICKET - ConfirmedDocument3 pagesGAY DEL: TICKET - ConfirmedRajat RanjanNo ratings yet

- Duplicate Result Card Application FormDocument4 pagesDuplicate Result Card Application FormShoaib akhterNo ratings yet

- Lloyd Industries Manufactures Electrical Equipment From Specifications Received From CustomersDocument2 pagesLloyd Industries Manufactures Electrical Equipment From Specifications Received From CustomersAmit PandeyNo ratings yet

- An Overview of Footwear Industry in BangladeshDocument11 pagesAn Overview of Footwear Industry in BangladeshSyed M IslamNo ratings yet

- SM Presentation On Garment IndustryDocument14 pagesSM Presentation On Garment IndustrytariqueshadabNo ratings yet

- Board Gender Diversity and Firm-Level Climate Change ExposureDocument9 pagesBoard Gender Diversity and Firm-Level Climate Change ExposureAbby LiNo ratings yet

- Global Village-OBassignmentDocument10 pagesGlobal Village-OBassignmentMOJAHID HASAN Fall 19No ratings yet

- GO (P) No 106-16-Fin DateDocument2 pagesGO (P) No 106-16-Fin Datesunil777tvpmNo ratings yet

- JRC 92241Document110 pagesJRC 92241felipedulinskiNo ratings yet

- DN500 Mounting Flange Installation ManualDocument12 pagesDN500 Mounting Flange Installation ManualSreekanthNo ratings yet

- Lien Form PDFDocument2 pagesLien Form PDFDanielleNo ratings yet

- Methodology of Installation of FencingDocument3 pagesMethodology of Installation of FencingA MakkiNo ratings yet

- Gonzales Cannon Oct 18 IssueDocument42 pagesGonzales Cannon Oct 18 IssueGonzales CannonNo ratings yet

- MBA102 - Case # 2Document5 pagesMBA102 - Case # 2Maricres arzagonNo ratings yet

- Itu Publications For Vessels Operating in Port LimitDocument6 pagesItu Publications For Vessels Operating in Port LimitVM ExportNo ratings yet

- Pearson Edexcel A-Level Economics A Guided WalkthroughDocument69 pagesPearson Edexcel A-Level Economics A Guided Walkthroughtim bryceNo ratings yet

- Main Aur Mera Vyakaran-07 TB 5 ChaptersDocument68 pagesMain Aur Mera Vyakaran-07 TB 5 ChaptersRAVI SHANKARNo ratings yet

- USSEC 2021 Global Soy Foods Market OverviewDocument73 pagesUSSEC 2021 Global Soy Foods Market OverviewgiangNo ratings yet

- Azure Sentinel Deployment and Migration ServicesDocument2 pagesAzure Sentinel Deployment and Migration ServicesGerman MarinoNo ratings yet

- Simon-Kucher SPI LCE SC2 DraftDocument68 pagesSimon-Kucher SPI LCE SC2 DraftHugo CaviedesNo ratings yet

- To Be Prepared by The Recipient Institution. This Proposal Will Be Submitted To The Steering Committee/Project Board For ApprovalDocument4 pagesTo Be Prepared by The Recipient Institution. This Proposal Will Be Submitted To The Steering Committee/Project Board For ApprovalЭ. ЦэлмэгNo ratings yet

- Fastmig Ms Om en PDFDocument22 pagesFastmig Ms Om en PDFmariustudoracheNo ratings yet

- Current Trends in PMSDocument4 pagesCurrent Trends in PMSSofia SebastianNo ratings yet

- Terex Digger Derrick Operators Manual 1Document20 pagesTerex Digger Derrick Operators Manual 1Israel SotoNo ratings yet

- Blackblot PMTK Gap AnalysisDocument7 pagesBlackblot PMTK Gap AnalysisVasilica BobNo ratings yet