Download as pdf or txt

You might also like

- CH - 02 - Cost Terms, Concepts and Classifications With Mixed Cost AnalysisDocument84 pagesCH - 02 - Cost Terms, Concepts and Classifications With Mixed Cost AnalysisankonmahmudNo ratings yet

- Cost Accounting 1 8 PDFDocument110 pagesCost Accounting 1 8 PDFHashim Mahmood KhanNo ratings yet

- Cost Concepts HandoutsDocument13 pagesCost Concepts HandoutsTushar DuaNo ratings yet

- Cost Concept and ClassificationDocument45 pagesCost Concept and ClassificationMountaha0% (1)

- Unit 3Document258 pagesUnit 3Raunak Maheshwari100% (1)

- CMA - 1-Introduction To CMADocument35 pagesCMA - 1-Introduction To CMAIrtaza AhsanNo ratings yet

- Costs in Managerial AccountingDocument9 pagesCosts in Managerial AccountingVerily DomingoNo ratings yet

- Managerial Accounting (1-3) - Fall 2022Document60 pagesManagerial Accounting (1-3) - Fall 2022Saahil KarnikNo ratings yet

- Chapter 3 Cost IDocument64 pagesChapter 3 Cost IBikila MalasaNo ratings yet

- Presentation 04 (1slide-Pg)Document33 pagesPresentation 04 (1slide-Pg)araika.maksutNo ratings yet

- Introduction Cost Concepts Terms and BehaviorDocument43 pagesIntroduction Cost Concepts Terms and BehaviorZACARIAS, Marc Nickson DG.No ratings yet

- 10632m Lecture 6 - Full Costing I (Full Version)Document53 pages10632m Lecture 6 - Full Costing I (Full Version)kammiefan215No ratings yet

- Chapter-4: Manufacturing Cost Elements and Cost Estimation For Various ProcessDocument21 pagesChapter-4: Manufacturing Cost Elements and Cost Estimation For Various ProcessTerefa FeyisaNo ratings yet

- Module 7 Activity Based Management and Activity Based SystemDocument23 pagesModule 7 Activity Based Management and Activity Based SystemCharity ZamoraNo ratings yet

- Chapter-2 Answer KeyDocument18 pagesChapter-2 Answer KeyKylie sheena MendezNo ratings yet

- CH 2 Cost Concepts and BehaviorDocument36 pagesCH 2 Cost Concepts and BehaviorYunita LalaNo ratings yet

- Introduction To Cost Accounting: 15.501/516 Spring 2004Document23 pagesIntroduction To Cost Accounting: 15.501/516 Spring 2004scribddmailNo ratings yet

- Chapter 2 Cost IDocument50 pagesChapter 2 Cost IBikila MalasaNo ratings yet

- CH 2 Cost Concepts and BehaviorDocument37 pagesCH 2 Cost Concepts and BehaviorRexmar Christian BernardoNo ratings yet

- Topic 2 - Cost and Cost SystemDocument28 pagesTopic 2 - Cost and Cost SystemTân Nguyên100% (1)

- Garrison Lecture Chapter 2Document61 pagesGarrison Lecture Chapter 2Ahmad Tawfiq Darabseh100% (2)

- Chapter 2 Cost IDocument51 pagesChapter 2 Cost IheysemNo ratings yet

- I. Answers To Questions: Cost Accounting and Control - Solutions Manual Cost Terms, Concepts and ClassificationsDocument18 pagesI. Answers To Questions: Cost Accounting and Control - Solutions Manual Cost Terms, Concepts and ClassificationsYannah HidalgoNo ratings yet

- Part III-Managerial AccountingDocument91 pagesPart III-Managerial AccountingGebreNo ratings yet

- Session 2 - Cost Concept and Classification RevisedDocument48 pagesSession 2 - Cost Concept and Classification Revisedsakshi upadhyayNo ratings yet

- CH 2Document62 pagesCH 2MUHAMMAD WAJID SHAHZADNo ratings yet

- Classification of CostDocument23 pagesClassification of CostShohidul Islam SaykatNo ratings yet

- Chapter-2-Answer Cost AccountingDocument18 pagesChapter-2-Answer Cost AccountingJuline Ashley A Carballo100% (1)

- Chapter 2 UpdatedDocument58 pagesChapter 2 Updatedbing bongNo ratings yet

- Chapter 2 Answer PDFDocument19 pagesChapter 2 Answer PDFCris VillarNo ratings yet

- 110-W2-3-Cost concept-chp02-STDocument85 pages110-W2-3-Cost concept-chp02-STmargaret mariaNo ratings yet

- Session 2 An Introduction To Cost Terms and PurposesDocument57 pagesSession 2 An Introduction To Cost Terms and Purposeschloe lamxdNo ratings yet

- Basic Management Accounting ConceptsDocument28 pagesBasic Management Accounting Conceptsgenidia giselaNo ratings yet

- ACCT2105 - Lecture 2Document60 pagesACCT2105 - Lecture 2DS ENo ratings yet

- Module 2 Basic Cost Management ConceptDocument12 pagesModule 2 Basic Cost Management ConceptWendryNo ratings yet

- Chapter 3 - Virtual - Classroom-M.Document61 pagesChapter 3 - Virtual - Classroom-M.rebeccahf7No ratings yet

- C&MDocument18 pagesC&MSultanaQuader50% (2)

- c1 - Introduction To Cost AccountingDocument2 pagesc1 - Introduction To Cost AccountingAndrea Camille AquinoNo ratings yet

- Iafm Ch05 Fall 2023 NuDocument31 pagesIafm Ch05 Fall 2023 Nugigih satyaNo ratings yet

- Chapter 2 Cost Accounting ConceptsDocument22 pagesChapter 2 Cost Accounting ConceptsRosliana RazabNo ratings yet

- CH 02Document40 pagesCH 02lyonanh289No ratings yet

- Cost Accounting and ControlDocument14 pagesCost Accounting and Controlkaye SagabaenNo ratings yet

- Chapter 2 Hilton 10th Instructor NotesDocument10 pagesChapter 2 Hilton 10th Instructor NotesKD MV100% (1)

- Managerial Accounting and Cost ConceptsDocument57 pagesManagerial Accounting and Cost ConceptsFrances Monique AlburoNo ratings yet

- Supplementary 1 - Cost ClassificationDocument26 pagesSupplementary 1 - Cost ClassificationNguyen Tuan Anh (BTEC HN)No ratings yet

- Activity BasedDocument50 pagesActivity BasedSandipan DawnNo ratings yet

- Topic 1 Application of Cost Concepts To The Decision Making ProcessDocument68 pagesTopic 1 Application of Cost Concepts To The Decision Making ProcessSaudulla Jameel JameelNo ratings yet

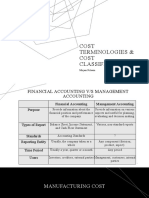

- Cost Terminologies & Cost Classification: Mirjam NilssonDocument13 pagesCost Terminologies & Cost Classification: Mirjam NilssonHitesh JainNo ratings yet

- Chapter 1 IntroductionDocument46 pagesChapter 1 IntroductionIrzam ZairyNo ratings yet

- Introduction To Management AccountingDocument47 pagesIntroduction To Management AccountingMULATNo ratings yet

- Chapter 02 - Cost Term and Concepts FinalDocument60 pagesChapter 02 - Cost Term and Concepts FinalAminaMatinNo ratings yet

- Topic Outline For Topic 4 Variable, Absorption and Throughput CostingDocument28 pagesTopic Outline For Topic 4 Variable, Absorption and Throughput Costinggayel.makipig.21No ratings yet

- An Introduction To Cost Terms and PurposesDocument33 pagesAn Introduction To Cost Terms and PurposesAi LatifahNo ratings yet

- Topic 1 Application of Cost Concepts To The Decision Making ProcessDocument69 pagesTopic 1 Application of Cost Concepts To The Decision Making ProcessMaryam MalieNo ratings yet

- Chapter 4 (Acc)Document25 pagesChapter 4 (Acc)shafNo ratings yet

- Module 9. Cost Accumulation 12.11.2012Document34 pagesModule 9. Cost Accumulation 12.11.2012NajlaNo ratings yet

- Full Download Managerial Accounting For Managers 2nd Edition Noreen Solutions ManualDocument35 pagesFull Download Managerial Accounting For Managers 2nd Edition Noreen Solutions Manuallinderleafeulah97% (38)

- Q.9. Differentiate Direct Cost and Direct Costing?Document10 pagesQ.9. Differentiate Direct Cost and Direct Costing?Hami KhaNNo ratings yet

- CH02Document28 pagesCH02Slalu Terima Apa AdanyaNo ratings yet

- Management Accounting Strategy Study Resource for CIMA Students: CIMA Study ResourcesFrom EverandManagement Accounting Strategy Study Resource for CIMA Students: CIMA Study ResourcesNo ratings yet

- PS5Document2 pagesPS5ebrarrsevimmNo ratings yet

- Right-Skewed Left-Skewed SymmetricDocument3 pagesRight-Skewed Left-Skewed SymmetricebrarrsevimmNo ratings yet

- Continuous Random Variables and Probability DistributionsDocument73 pagesContinuous Random Variables and Probability DistributionsebrarrsevimmNo ratings yet

- Bus 211 - Introduction To Accounting / Handout 2Document2 pagesBus 211 - Introduction To Accounting / Handout 2ebrarrsevimmNo ratings yet

- Adjusting EntriesDocument3 pagesAdjusting EntriesebrarrsevimmNo ratings yet

- Correlation Coefficient PracticeDocument6 pagesCorrelation Coefficient PracticeebrarrsevimmNo ratings yet

- Bus 211 - Introduction To Accounting / Handout 1Document1 pageBus 211 - Introduction To Accounting / Handout 1ebrarrsevimmNo ratings yet

- 6Document2 pages6ebrarrsevimmNo ratings yet

- Right-Skewed Left-Skewed SymmetricDocument2 pagesRight-Skewed Left-Skewed SymmetricebrarrsevimmNo ratings yet

- 2Document4 pages2ebrarrsevimmNo ratings yet

- Slide SolutionsDocument3 pagesSlide SolutionsebrarrsevimmNo ratings yet