Download as pdf or txt

You might also like

- The Basics of Public Budgeting and Financial Management: A Handbook for Academics and PractitionersFrom EverandThe Basics of Public Budgeting and Financial Management: A Handbook for Academics and PractitionersNo ratings yet

- Interview Questions and TipsDocument45 pagesInterview Questions and TipsSoumava BasuNo ratings yet

- Activity 1 Employee Benefits AKDocument7 pagesActivity 1 Employee Benefits AKRalph Rivera SantosNo ratings yet

- Employee Benefit 1 PDFDocument34 pagesEmployee Benefit 1 PDFbobo kaNo ratings yet

- The Following Information Relates To Questions 1-7: Components of Periodic Benefit CostDocument6 pagesThe Following Information Relates To Questions 1-7: Components of Periodic Benefit CostGHINA NURRAMDHANNo ratings yet

- (Use The Below Problem To Answers The Succeeding Four (4) Questions.)Document3 pages(Use The Below Problem To Answers The Succeeding Four (4) Questions.)admiral spongebobNo ratings yet

- Chapter 19 Assignment IAF410 Excel SheetDocument14 pagesChapter 19 Assignment IAF410 Excel SheetTati AnaNo ratings yet

- Homework Chapter 4Document17 pagesHomework Chapter 4Trung Kiên Nguyễn100% (1)

- Benefits AccountingDocument4 pagesBenefits AccountingJulian Christopher Torcuator50% (2)

- Group 1 (ODD) - Question 1.editedDocument5 pagesGroup 1 (ODD) - Question 1.editedPatricia Byun100% (1)

- CH 20Document8 pagesCH 20Saleh RaoufNo ratings yet

- Employee BenefitsDocument20 pagesEmployee BenefitsKezNo ratings yet

- Chapter 19 in Class ExercisesDocument14 pagesChapter 19 in Class ExercisesByul ProductionsNo ratings yet

- Tutor Accounting For Pensions PlanDocument16 pagesTutor Accounting For Pensions PlanAngel Valentine Tirayo100% (1)

- Compilation of ProblemsDocument10 pagesCompilation of ProblemsjojNo ratings yet

- SM01 EmployeeBenefitsDocument1 pageSM01 EmployeeBenefitsJoan Rachel CalansinginNo ratings yet

- Employees BenefitsDocument2 pagesEmployees BenefitsorillosachristoperjohnNo ratings yet

- Grup - Task 4Document6 pagesGrup - Task 4DemastaufiqNo ratings yet

- Assignment No. 2 - Pension - Cunanan & ManlangitDocument3 pagesAssignment No. 2 - Pension - Cunanan & ManlangitCunanan, Malakhai JeuNo ratings yet

- Colegio de San Juan de Letran: Employee BenefitsDocument4 pagesColegio de San Juan de Letran: Employee BenefitsRed YuNo ratings yet

- Far Module 21 27Document61 pagesFar Module 21 27ryanNo ratings yet

- Balances or Values at December 31, 2019Document6 pagesBalances or Values at December 31, 2019KATHERINEMARIE DIMAUNAHANNo ratings yet

- Chapter 18 Ia2Document18 pagesChapter 18 Ia2JM Valonda Villena, CPA, MBANo ratings yet

- 1231231231231231Document11 pages1231231231231231JV De VeraNo ratings yet

- Q2 Employee Benefits Pt.2Document4 pagesQ2 Employee Benefits Pt.2francine del rosarioNo ratings yet

- Compiled By: Wenston Del Rosario ACCTGREV1 - 010: Employee BenefitsDocument2 pagesCompiled By: Wenston Del Rosario ACCTGREV1 - 010: Employee BenefitsJeremiah DavidNo ratings yet

- Auxtero - Assignment No. 2 - Pension AccountingDocument3 pagesAuxtero - Assignment No. 2 - Pension AccountingCunanan, Malakhai JeuNo ratings yet

- FA2-T10-AB-DB Pensions-DATA-rev 10-Nov-2018Document1 pageFA2-T10-AB-DB Pensions-DATA-rev 10-Nov-2018Ghai BilElNo ratings yet

- Retirement BenefitsDocument4 pagesRetirement BenefitsJona FranciscoNo ratings yet

- ACC221Document5 pagesACC221Hilarie JeanNo ratings yet

- Adjusting Entries: Asistensi Pengantar Akuntansi IDocument4 pagesAdjusting Entries: Asistensi Pengantar Akuntansi Isinta agnes100% (1)

- Chapter 19 SolutionsDocument34 pagesChapter 19 SolutionsRachel Rajanayagam100% (1)

- FAR-2202 (Employee Benefits)Document2 pagesFAR-2202 (Employee Benefits)Sam FranciscoNo ratings yet

- INTACT. Post Employment BenefitsDocument13 pagesINTACT. Post Employment BenefitsKii-anne FernandezNo ratings yet

- Iac 11 Employee BenefitsDocument5 pagesIac 11 Employee BenefitsNacelleNo ratings yet

- Computation of Prior Service Cost Amortization Pension PDFDocument1 pageComputation of Prior Service Cost Amortization Pension PDFAnbu jaromiaNo ratings yet

- Defined Benefit Plan Accounting ProceduresDocument46 pagesDefined Benefit Plan Accounting ProceduresEJ EduqueNo ratings yet

- Activity #2-Employee BenefitsDocument5 pagesActivity #2-Employee BenefitsJamaica DavidNo ratings yet

- Employee Benefits: Defined Benefit PlansDocument4 pagesEmployee Benefits: Defined Benefit PlansMHARTIN DAENNIELLE ORSALNo ratings yet

- (Use The Below Problem To Answers The Succeeding Four (4) Questions.)Document3 pages(Use The Below Problem To Answers The Succeeding Four (4) Questions.)Janine LerumNo ratings yet

- (Use The Below Problem To Answers The Succeeding Four (4) Questions.)Document3 pages(Use The Below Problem To Answers The Succeeding Four (4) Questions.)Sitti Ayesha HasimanNo ratings yet

- CH03Document3 pagesCH03Fuyiko Kaneshiro HosanaNo ratings yet

- Employee Benefits Part 2 pROBLEM 3-8Document2 pagesEmployee Benefits Part 2 pROBLEM 3-8Christian QuidipNo ratings yet

- Be Advised, The Template Workbooks and Worksheets Are Not Protected. Overtyping Any Data May Remove ItDocument6 pagesBe Advised, The Template Workbooks and Worksheets Are Not Protected. Overtyping Any Data May Remove ItSalman KhalidNo ratings yet

- Sept. 1, 2020 Topic 1 - Employee Benefits (Closure Questions)Document4 pagesSept. 1, 2020 Topic 1 - Employee Benefits (Closure Questions)Lj Diane TuazonNo ratings yet

- Learning Objective: Daftar Komponen Biaya PensiunDocument3 pagesLearning Objective: Daftar Komponen Biaya Pensiuntes doangNo ratings yet

- Activity 1.6.2Document1 pageActivity 1.6.2Stephen JohnNo ratings yet

- Example Exercise - Postemployment BenefitsDocument5 pagesExample Exercise - Postemployment BenefitsYhana SarmientoNo ratings yet

- FAR PROBLEMS - 1 FinalDocument9 pagesFAR PROBLEMS - 1 FinalLouise GazaNo ratings yet

- LM-24 Intermediate AccountingDocument7 pagesLM-24 Intermediate AccountingMary Jane TalanNo ratings yet

- Ch20 PensionDocument17 pagesCh20 PensionEmma Mariz Garcia100% (1)

- Quiz Employee BenefitsDocument4 pagesQuiz Employee Benefitscrispin leanoNo ratings yet

- Employee Benefits 1Document4 pagesEmployee Benefits 1CAI50% (2)

- Mohammed - Moinuddin Sutherland SalaryDocument2 pagesMohammed - Moinuddin Sutherland SalaryShoaib Khan -Vlog'sNo ratings yet

- Employee Benefits Exercises - Pensions and LT BenefitsDocument3 pagesEmployee Benefits Exercises - Pensions and LT BenefitsAcads LangNo ratings yet

- Karthik PanditDocument2 pagesKarthik PanditprincemjNo ratings yet

- Soal Latihan DDADocument1 pageSoal Latihan DDAMutia AzzahraNo ratings yet

- Tugas Penyelesaian 14 AIK - 0119101024 - Muhamad Adam Palmaleo - Kelas BDocument23 pagesTugas Penyelesaian 14 AIK - 0119101024 - Muhamad Adam Palmaleo - Kelas BAdam PalmaleoNo ratings yet

- Module 31 Employee Benefits ProblemDocument2 pagesModule 31 Employee Benefits ProblemThalia UyNo ratings yet

- Exam2 Acct414 F07Document16 pagesExam2 Acct414 F07ElvinNo ratings yet

- Henning Company Sponsors A Defined Benefit Pension Plan For PDFDocument1 pageHenning Company Sponsors A Defined Benefit Pension Plan For PDFAnbu jaromiaNo ratings yet

- This Study Resource Was: Identify The Letter of The Choice That Best Completes The Statement or Answers The QuestionDocument8 pagesThis Study Resource Was: Identify The Letter of The Choice That Best Completes The Statement or Answers The Questionfufu pandaNo ratings yet

- Project Report Mandap DecorationDocument17 pagesProject Report Mandap Decorationkushal chopda100% (1)

- Methods of Payment For DFTDocument31 pagesMethods of Payment For DFTPalak MehraNo ratings yet

- T AccountDocument2 pagesT AccountSophia RamirezNo ratings yet

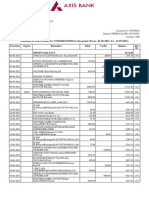

- Statement of Axis Account No:917010066315582 For The Period (From: 01-06-2021 To: 12-09-2021)Document6 pagesStatement of Axis Account No:917010066315582 For The Period (From: 01-06-2021 To: 12-09-2021)Anirban DebNo ratings yet

- Accounting Cycle WorksheetDocument11 pagesAccounting Cycle Worksheettarikuabdisa0No ratings yet

- Bank of Maharashtra PDFDocument76 pagesBank of Maharashtra PDFPRATIK BhosaleNo ratings yet

- Principles of Accounting RevisionDocument99 pagesPrinciples of Accounting RevisionHoang Khanh Linh NguyenNo ratings yet

- Mas-03: Absorption & Variable CostingDocument4 pagesMas-03: Absorption & Variable CostingClint AbenojaNo ratings yet

- Cash FlowDocument35 pagesCash FlowsiriusNo ratings yet

- How To Start A Lending BusinessDocument4 pagesHow To Start A Lending BusinessJerome BundaNo ratings yet

- FT Partners Research - The Rise of Challenger BanksDocument217 pagesFT Partners Research - The Rise of Challenger BanksnguoinhenvnNo ratings yet

- SqoopDocument575 pagesSqoopAnonymous vzc5LdnaLNo ratings yet

- B1 Features of Financial InstitutionsDocument19 pagesB1 Features of Financial InstitutionsKanna MathikaranNo ratings yet

- Cash 1. List The Five Primary Activities Involved in The Acquisition and Payment CycleDocument3 pagesCash 1. List The Five Primary Activities Involved in The Acquisition and Payment CycleJomer Fernandez100% (3)

- AF205 Assignment 2 - Navneet Nischal Chand - S11157889Document3 pagesAF205 Assignment 2 - Navneet Nischal Chand - S11157889Shayal ChandNo ratings yet

- UCO - GROUP CARE 360 APPLICATION FORM (Scheme For Customers of UCO Bank) (JULY-5th) - CompressedDocument2 pagesUCO - GROUP CARE 360 APPLICATION FORM (Scheme For Customers of UCO Bank) (JULY-5th) - CompressedRahulSinghNo ratings yet

- Sbi 6Document8 pagesSbi 6Chouhan Akshay SinghNo ratings yet

- Mod Sub Inspector Challan FormDocument1 pageMod Sub Inspector Challan FormMuhammad Rɘʜʌŋ BakhshNo ratings yet

- CH 9Document27 pagesCH 9eng.hfk06No ratings yet

- Modern Portfolio Theory and Investment Analysis 9th Edition Elton Test Bank 1Document27 pagesModern Portfolio Theory and Investment Analysis 9th Edition Elton Test Bank 1george100% (45)

- प्रबन्धकीय लेखाविधि Management AccountingDocument21 pagesप्रबन्धकीय लेखाविधि Management AccountingNeeraj Singh RainaNo ratings yet

- MAS 2nd Summative TestDocument16 pagesMAS 2nd Summative TestNovie Abel BolivarNo ratings yet

- Accounts Receivable Flashcards - 2Document6 pagesAccounts Receivable Flashcards - 2SeanNo ratings yet

- In The Books of Virat Simple Cash Book DR. 2021Document13 pagesIn The Books of Virat Simple Cash Book DR. 2021S1626No ratings yet

- Capital Budgeting MalaysiaDocument12 pagesCapital Budgeting MalaysiaFarandi AngestiNo ratings yet

- Uban Ashab Ali Proposal 3Document17 pagesUban Ashab Ali Proposal 3Utban AshabNo ratings yet

- Motor Policy With Reference To New India Assurance Company LTDDocument70 pagesMotor Policy With Reference To New India Assurance Company LTDkevalcool2500% (1)

- Module III Intrest Rate and Currency SwapDocument21 pagesModule III Intrest Rate and Currency SwapJ BNo ratings yet