Download as docx, pdf, or txt

You might also like

- Complete Freedom: Statement of AccountDocument5 pagesComplete Freedom: Statement of AccountWenjie6567% (3)

- Cost Sheet ProblemsDocument18 pagesCost Sheet ProblemsMariam Mathen77% (57)

- Cost Accounting and Control by Sir ChuaDocument92 pagesCost Accounting and Control by Sir ChuaAnalyn Lafradez100% (3)

- Cost Accounting Matz & Usry 7 EditionDocument24 pagesCost Accounting Matz & Usry 7 Editionsaira22pafNo ratings yet

- Accounting For Manufacturing BusinessDocument56 pagesAccounting For Manufacturing Businessrajahmati_2890% (20)

- RusselJ. Fuller and Chi-Cheng Hsia A Simplified Common Stock Valuation ModelDocument9 pagesRusselJ. Fuller and Chi-Cheng Hsia A Simplified Common Stock Valuation ModelShivani RahejaNo ratings yet

- P2 Manufacturing Learning MaterialDocument5 pagesP2 Manufacturing Learning Materialchen.abellar.swuNo ratings yet

- Cost Accounting RefresherDocument15 pagesCost Accounting Refresherfat31udm100% (1)

- Jewish Wisdom For BusinessDocument11 pagesJewish Wisdom For Businessvanvic93No ratings yet

- Three Rules For Safety From Covid: Prepared By:-Ms Tinu AnandDocument21 pagesThree Rules For Safety From Covid: Prepared By:-Ms Tinu AnandPriyanshu singhNo ratings yet

- Cost AccountingDocument21 pagesCost Accountingabdullah_0o0No ratings yet

- 201 NotesDocument18 pages201 NotesSky SoronoiNo ratings yet

- Unit Costing: Notebook: Costing Created: 24-12-20 07:20 PM Updated: 04-01-21 12:57 PM Author: Tags: Unit CostingDocument7 pagesUnit Costing: Notebook: Costing Created: 24-12-20 07:20 PM Updated: 04-01-21 12:57 PM Author: Tags: Unit CostingNaman JainNo ratings yet

- Chapter 2 - Cost Accounting CycleDocument16 pagesChapter 2 - Cost Accounting CycleJoey Lazarte100% (1)

- The Fundamentals of CostingDocument13 pagesThe Fundamentals of Costingmy tràNo ratings yet

- Cost Systems and AccumulationDocument12 pagesCost Systems and Accumulations.gallur.gwynethNo ratings yet

- These Are The Key Points You Should Know For Chapter 1Document7 pagesThese Are The Key Points You Should Know For Chapter 1Jane VillanuevaNo ratings yet

- UNIT 1 Management AccountingDocument30 pagesUNIT 1 Management Accountingrehan husainNo ratings yet

- Cost Accaunting 2Document12 pagesCost Accaunting 2ዝምታ ተሻለNo ratings yet

- FIN600 Module 3 Topic 2Document25 pagesFIN600 Module 3 Topic 2Inés Tetuá TralleroNo ratings yet

- Cost Sheet: Definition, Elements of Cost and CalculationsDocument22 pagesCost Sheet: Definition, Elements of Cost and CalculationsOmkar JadhavNo ratings yet

- ACC212 Final Exam ReviewDocument5 pagesACC212 Final Exam ReviewVictoria PecicNo ratings yet

- Ac040 NoteDocument54 pagesAc040 NoteAdam OngNo ratings yet

- Just-In-Time and Backflush AccountingDocument3 pagesJust-In-Time and Backflush AccountingElla Mae VergaraNo ratings yet

- Notes On Week 13 - ManufacturingDocument2 pagesNotes On Week 13 - ManufacturingChristy CaneteNo ratings yet

- Classify The Following As Direct (D) or Indirect (I) MaterialsDocument7 pagesClassify The Following As Direct (D) or Indirect (I) MaterialsDaryll SallanNo ratings yet

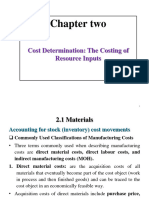

- Chapter TwoDocument33 pagesChapter TwoTerefe DubeNo ratings yet

- Systems Designs - Job and Process CostingDocument49 pagesSystems Designs - Job and Process Costingjoe6hodagameNo ratings yet

- JOB ORDER COSTING-notes and IllustrationDocument25 pagesJOB ORDER COSTING-notes and IllustrationKristienalyn De AsisNo ratings yet

- LESSON 1: Introduction To Cost AccountingDocument4 pagesLESSON 1: Introduction To Cost AccountingChriselda CabangonNo ratings yet

- Cost Accounting With More Illustrations-2Document21 pagesCost Accounting With More Illustrations-2Rohit KashyapNo ratings yet

- ACT3110 - Accounting For Manufacturing (S)Document39 pagesACT3110 - Accounting For Manufacturing (S)amirah1999No ratings yet

- Cost Accounting RefresherDocument16 pagesCost Accounting RefresherDemi PardilloNo ratings yet

- Presentation 12Document20 pagesPresentation 12MAHATMADANONo ratings yet

- Financial Tools Week 5 Block BDocument9 pagesFinancial Tools Week 5 Block BBelen González BouzaNo ratings yet

- COST I Chapter - 3&4Document30 pagesCOST I Chapter - 3&4alemuayalew01No ratings yet

- LP4 - Accounting For Job Order Costing-2Document4 pagesLP4 - Accounting For Job Order Costing-2Ciana SacdalanNo ratings yet

- 1Document2 pages1El - loolNo ratings yet

- Accounting For Manufacturing Cost Accounting Is Defined As A Systematic Set of Procedures For Recording and ReportingDocument5 pagesAccounting For Manufacturing Cost Accounting Is Defined As A Systematic Set of Procedures For Recording and ReportingEdgardo TangalinNo ratings yet

- Ankita ProjectDocument17 pagesAnkita ProjectRaman NehraNo ratings yet

- Product CostDocument22 pagesProduct CostJINKY TOLENTINONo ratings yet

- Management Accounting:: Balance Sheet: Income StatementDocument12 pagesManagement Accounting:: Balance Sheet: Income StatementTân NguyênNo ratings yet

- ACCCOB3Document87 pagesACCCOB3Lexy SungaNo ratings yet

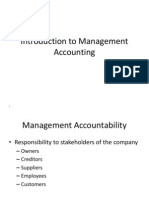

- Introduction To Management AccountingDocument34 pagesIntroduction To Management AccountingriyakalpetaNo ratings yet

- CH 01 - Basic Concepts and Job Order Cost CycleDocument22 pagesCH 01 - Basic Concepts and Job Order Cost CycleJi Baltazar100% (1)

- Mrac211 Midterm Concepts For ReviewDocument3 pagesMrac211 Midterm Concepts For Reviewlunamae evangelistaNo ratings yet

- Reviewer: Accounting For Manufacturing OperationsDocument16 pagesReviewer: Accounting For Manufacturing Operationsgab mNo ratings yet

- Basic Cost Management ConceptsDocument15 pagesBasic Cost Management ConceptsKatCaldwell100% (1)

- 4672 4986 - Rajasekaran Cost Accounting Supplements Important FormulaeDocument16 pages4672 4986 - Rajasekaran Cost Accounting Supplements Important FormulaeKunal SharmaNo ratings yet

- Chapter 1-Basic-Concepts-and-Job-Order-Cost-CycleDocument21 pagesChapter 1-Basic-Concepts-and-Job-Order-Cost-CycleRhodoraNo ratings yet

- COST I CH 2Document58 pagesCOST I CH 2YemaneNo ratings yet

- CH 3-Job CostingDocument54 pagesCH 3-Job CostingFasiko AsmaroNo ratings yet

- Chapter 1 ACCOUNTING FOR MANUFACTURING OPERATIONDocument36 pagesChapter 1 ACCOUNTING FOR MANUFACTURING OPERATIONMaimoona AsadNo ratings yet

- CA - 06 Job Order CostingDocument6 pagesCA - 06 Job Order CostingRonalyn ManuelNo ratings yet

- CH 6 Process Costing - Usman GabaDocument17 pagesCH 6 Process Costing - Usman GabaAmmad ShamiNo ratings yet

- Midterm 1 Cheat SheetDocument2 pagesMidterm 1 Cheat SheetPeter DenNo ratings yet

- Cost Accounting - Guerrerro Notes: Chapter 1-Cost Accounting - Basic Concepts and Job Order Cost CycleDocument6 pagesCost Accounting - Guerrerro Notes: Chapter 1-Cost Accounting - Basic Concepts and Job Order Cost CycleAyraaahNo ratings yet

- Managerial Accounting and CostDocument19 pagesManagerial Accounting and CostIqra MughalNo ratings yet

- MAC 2 - Strategic Cost Management Set of ProblemsDocument10 pagesMAC 2 - Strategic Cost Management Set of ProblemsC/PVT DAET, SHAINA JOYNo ratings yet

- Chapter 16 - FinalDocument24 pagesChapter 16 - FinalMuhammad Saad UmarNo ratings yet

- Practical Guide To Production Planning & Control [Revised Edition]From EverandPractical Guide To Production Planning & Control [Revised Edition]Rating: 1 out of 5 stars1/5 (1)

- Financial MarketsDocument16 pagesFinancial MarketsCharlotte AvalonNo ratings yet

- The BeatitudesDocument1 pageThe BeatitudesCharlotte AvalonNo ratings yet

- EconomicDevelopment 2Document15 pagesEconomicDevelopment 2Charlotte AvalonNo ratings yet

- MC Midterm NotesDocument25 pagesMC Midterm NotesCharlotte AvalonNo ratings yet

- Module 2Document10 pagesModule 2Charlotte AvalonNo ratings yet

- MC Midterm NotesDocument25 pagesMC Midterm NotesCharlotte AvalonNo ratings yet

- Reviewersa MclifeandowrkdsDocument12 pagesReviewersa MclifeandowrkdsCharlotte AvalonNo ratings yet

- GEC 5 PREFINAL HandoutsDocument4 pagesGEC 5 PREFINAL HandoutsCharlotte AvalonNo ratings yet

- UMITEN BLUE TERNATE 4 1 420 EmailedDocument5 pagesUMITEN BLUE TERNATE 4 1 420 EmailedCharlotte AvalonNo ratings yet

- Reviewersa TheologyDocument15 pagesReviewersa TheologyCharlotte AvalonNo ratings yet

- GEC 5 Prefinal SpeechDocument1 pageGEC 5 Prefinal SpeechCharlotte AvalonNo ratings yet

- Learners' Study Habits During The Covid-19 PandemicDocument10 pagesLearners' Study Habits During The Covid-19 PandemicCharlotte AvalonNo ratings yet

- Group 5 Research QuestionnaireDocument4 pagesGroup 5 Research QuestionnaireCharlotte AvalonNo ratings yet

- What Are The Changes Routines of The Learners Before and After Pandemic Has Occurred?Document2 pagesWhat Are The Changes Routines of The Learners Before and After Pandemic Has Occurred?Charlotte AvalonNo ratings yet

- Learner'S Study Habits During The Covid-19 PandemicDocument34 pagesLearner'S Study Habits During The Covid-19 PandemicCharlotte AvalonNo ratings yet

- Procedures of Mergers and Acquisition in IndiaDocument10 pagesProcedures of Mergers and Acquisition in IndiaVignesh KymalNo ratings yet

- Chapter 14 Test Bank Part 2Document21 pagesChapter 14 Test Bank Part 2Rachel GreenNo ratings yet

- Acco 420 Final Coursepack CoursepacAplusDocument51 pagesAcco 420 Final Coursepack CoursepacAplusApril MayNo ratings yet

- Problems - Capital BudgetingDocument5 pagesProblems - Capital BudgetingDianne TorresNo ratings yet

- Final Income TaxDocument27 pagesFinal Income TaxKai Son-MyoiNo ratings yet

- Math Accounting by AtaurDocument28 pagesMath Accounting by AtaurShajib KhanNo ratings yet

- Pas 10 Events After The Balance Sheet DateDocument2 pagesPas 10 Events After The Balance Sheet DaterandyNo ratings yet

- Assignment-2 (New) PDFDocument12 pagesAssignment-2 (New) PDFminnie908No ratings yet

- Chapter 10 MKDocument33 pagesChapter 10 MKzf1370No ratings yet

- SANDISKDocument16 pagesSANDISKAswini Kumar BhuyanNo ratings yet

- Assign 2 WP 2-2 To 2-5b-1Document6 pagesAssign 2 WP 2-2 To 2-5b-1zabraham18No ratings yet

- SFM by CA Pavan Karmele SirDocument2 pagesSFM by CA Pavan Karmele SirPrerak JainNo ratings yet

- 552748Document3 pages552748mohitgaba19No ratings yet

- Cambridge International AS & A Level: ACCOUNTING 9706/22Document16 pagesCambridge International AS & A Level: ACCOUNTING 9706/22Aimen AhmedNo ratings yet

- FAR610 - Test 1-Apr2018-Q PDFDocument3 pagesFAR610 - Test 1-Apr2018-Q PDFIman NadhirahNo ratings yet

- Ias 33 EpsDocument4 pagesIas 33 EpsMd. Mamunur RashidNo ratings yet

- Berkshire Hathway - Conclusions From LettersDocument8 pagesBerkshire Hathway - Conclusions From LettersAnonymous yjwN5VAjNo ratings yet

- Transfer and Business Taxation Accounting Methods and PeriodsDocument5 pagesTransfer and Business Taxation Accounting Methods and PeriodsApril Joy Padua SimonNo ratings yet

- MCQ Cma Inter-P8 CostingDocument58 pagesMCQ Cma Inter-P8 Costingsekhee1011No ratings yet

- Chapter 3 Presentation of Financial StatementsDocument24 pagesChapter 3 Presentation of Financial StatementsLEE WEI LONGNo ratings yet

- Chandu PRJDocument67 pagesChandu PRJAnonymous 22GBLsme1No ratings yet

- Group Presentation FOI 2020-21Document6 pagesGroup Presentation FOI 2020-21Amazon WorldNo ratings yet

- The Following Information Relates To The Shareholders' Equity Accounts of PABEBE CO.Document6 pagesThe Following Information Relates To The Shareholders' Equity Accounts of PABEBE CO.JamesNo ratings yet

- SOCARDocument113 pagesSOCAREl ShanNo ratings yet

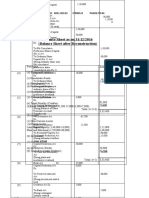

- Balance Sheet As On 31/12/2016 (Balance Sheet After Reconstruction)Document8 pagesBalance Sheet As On 31/12/2016 (Balance Sheet After Reconstruction)GauravNo ratings yet

- Audit of LedgersDocument28 pagesAudit of LedgersShahbaz NoorNo ratings yet

- Disbursement Voucher SKDocument13 pagesDisbursement Voucher SKCharlyn MoyonNo ratings yet

- TCI Altaba PresentationDocument13 pagesTCI Altaba Presentationmarketfolly.comNo ratings yet

![Practical Guide To Production Planning & Control [Revised Edition]](https://imgv2-1-f.scribdassets.com/img/word_document/235162742/149x198/2a816df8c8/1709920378?v=1)