Download as pdf or txt

You might also like

- Step Smart FitnessDocument5 pagesStep Smart Fitnessamit sah83% (6)

- Mario y DragónDocument23 pagesMario y DragónJenny Astrid Velandia Castillo100% (3)

- Luffy Inu WhitepaperDocument11 pagesLuffy Inu WhitepaperAlexter de Gala100% (1)

- Tax Invoice/Bill of Supply/Cash Memo: (Original For Recipient)Document1 pageTax Invoice/Bill of Supply/Cash Memo: (Original For Recipient)Shriharsh KatageriNo ratings yet

- Project Management Group Work 8: The Bathtub PeriodDocument3 pagesProject Management Group Work 8: The Bathtub Periodpalak mohodNo ratings yet

- Circular No.45Document5 pagesCircular No.45Hr legaladviserNo ratings yet

- "Last Date For Availing Itc For 2017-2018 IS 31 AUGUST, 2019": Gujarat High CourtDocument2 pages"Last Date For Availing Itc For 2017-2018 IS 31 AUGUST, 2019": Gujarat High Courtsukantabera215No ratings yet

- Circular CGST 193Document4 pagesCircular CGST 193Jaipur-B Gr-2No ratings yet

- 03 WP GST - Ipsum - v2Document47 pages03 WP GST - Ipsum - v2noorensaba01100% (1)

- Mamatha Traders Adjuducation Order Us 73 - CompressedDocument31 pagesMamatha Traders Adjuducation Order Us 73 - Compressedurmilachoudhary1999No ratings yet

- Circular Refund 137 7 2020Document3 pagesCircular Refund 137 7 2020Shirish JainNo ratings yet

- June 2020 SP 2Document27 pagesJune 2020 SP 2Avinash ShettyNo ratings yet

- Ref: GSTN: Sub: Reply To Your Notice For Payment of Interest Period: July'2017 To Nov'2018Document4 pagesRef: GSTN: Sub: Reply To Your Notice For Payment of Interest Period: July'2017 To Nov'2018Nikhil JainNo ratings yet

- 1 Latest GSTR 9 and 9C TaxbykkDocument73 pages1 Latest GSTR 9 and 9C TaxbykkjitendraktNo ratings yet

- Page 1 of 8Document8 pagesPage 1 of 8Faiqa HamidNo ratings yet

- Circular No.59Document6 pagesCircular No.59Hr legaladviserNo ratings yet

- Asmt 10 1920Document69 pagesAsmt 10 1920Prashant ZawareNo ratings yet

- DRC 03 Letters-1Document2 pagesDRC 03 Letters-1anjani deviNo ratings yet

- Cir 174 06 2022 CGSTDocument5 pagesCir 174 06 2022 CGSTNM JHANWAR & ASSOCIATESNo ratings yet

- Tax Laws Ns Ep June 2020Document29 pagesTax Laws Ns Ep June 2020sarvaniNo ratings yet

- Recommendations of GST Council Related To Law &procedureDocument2 pagesRecommendations of GST Council Related To Law &procedurePunit AroraNo ratings yet

- Relief For ITC Claimed For Unmatched Invoices in GSTR 2A For FYs 2017-18Document3 pagesRelief For ITC Claimed For Unmatched Invoices in GSTR 2A For FYs 2017-18sanket lunkadNo ratings yet

- J 2020 SCC OnLine Tri 598 2021 87 GSTR 170 2021 52 G Rameshananda Gmailcom 20231212 121104 1 27Document27 pagesJ 2020 SCC OnLine Tri 598 2021 87 GSTR 170 2021 52 G Rameshananda Gmailcom 20231212 121104 1 27r.preethimanasaug22No ratings yet

- Instruction No 022022 GST Dated 22032022Document13 pagesInstruction No 022022 GST Dated 22032022GroupA PreventiveNo ratings yet

- 5254 - Tax Regime - 2024 - 240408 - 212256Document3 pages5254 - Tax Regime - 2024 - 240408 - 212256sunil78No ratings yet

- Circular CGST 95Document3 pagesCircular CGST 95Venkataramana NippaniNo ratings yet

- SOP For ScrutinyDocument5 pagesSOP For Scrutinyacgstdiv4No ratings yet

- AAR - ITC On Capital Goods in Case of Taxable + Exepmt SupplyDocument3 pagesAAR - ITC On Capital Goods in Case of Taxable + Exepmt SupplyJigar MakwanaNo ratings yet

- OIO AarkeyTrad 57 13Document20 pagesOIO AarkeyTrad 57 13jitendraktNo ratings yet

- Circular No 16 2023 - Refund-AbstactDocument14 pagesCircular No 16 2023 - Refund-AbstactsakthijackNo ratings yet

- Unit 5 GSTDocument3 pagesUnit 5 GSTNishu KatiyarNo ratings yet

- Reportable: 1 For Short, "Impugned Circular" 2 For Short, "Commissioner (GST) "Document52 pagesReportable: 1 For Short, "Impugned Circular" 2 For Short, "Commissioner (GST) "AMAR GUPTANo ratings yet

- Chapter 11 GST ReturnsDocument18 pagesChapter 11 GST ReturnsDR. PREETI JINDALNo ratings yet

- Paper-18 Supplementary 180221Document109 pagesPaper-18 Supplementary 180221Srihari SrinivasNo ratings yet

- Action For Difference in ITC Between 3B and 2ADocument46 pagesAction For Difference in ITC Between 3B and 2Aphani raja kumarNo ratings yet

- Circular Refund 142 11 2020Document3 pagesCircular Refund 142 11 2020Gulrana AlamNo ratings yet

- Annexure-X - Waiver of SCN & PenaltyDocument3 pagesAnnexure-X - Waiver of SCN & Penaltyvishnuprakash1990No ratings yet

- Skyline Pipes para WiseDocument4 pagesSkyline Pipes para WiseAjay SinghNo ratings yet

- MB ComDocument2 pagesMB Comsatyanand guptaNo ratings yet

- Tax HDocument15 pagesTax HDeepesh SinghNo ratings yet

- Circular Refund 147-1.5 Times RefundDocument5 pagesCircular Refund 147-1.5 Times Refundbanerjeeankita13No ratings yet

- Circular No.63Document10 pagesCircular No.63Shrikant KulkarniNo ratings yet

- Moot ProblemDocument2 pagesMoot ProblemSachin Anand Roll No. 48No ratings yet

- GST - Notification No. Order No. 02 - 2018 - Dated 31-12-2018 - Central GST (CGST)Document2 pagesGST - Notification No. Order No. 02 - 2018 - Dated 31-12-2018 - Central GST (CGST)ARJUN ATHREYANNo ratings yet

- Article On Assessment and AuditDocument33 pagesArticle On Assessment and Auditmks895525No ratings yet

- E InvoiceDocument1 pageE Invoicegurdyal672No ratings yet

- 784 Settlement of Arrears of Tax Interest Penalty or Late Fee For The Period Ending On or Before 30.06.2017Document38 pages784 Settlement of Arrears of Tax Interest Penalty or Late Fee For The Period Ending On or Before 30.06.2017santosh pandeyNo ratings yet

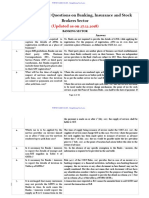

- 27122018-UPDATED - FAQs ON BANKING, INSURANCE AND STOCK BROKERSDocument34 pages27122018-UPDATED - FAQs ON BANKING, INSURANCE AND STOCK BROKERSHimanshu PanchpalNo ratings yet

- Cir 180 08 2022 CGSTDocument8 pagesCir 180 08 2022 CGSTveer_bcaNo ratings yet

- SYNOPSISDocument2 pagesSYNOPSISnoorensaba01No ratings yet

- Faqs On Banking, Insurance and Stock Brokers CbicDocument34 pagesFaqs On Banking, Insurance and Stock Brokers CbicVenkataramana NippaniNo ratings yet

- All About GSTR 3B With Latest AmendmentsDocument7 pagesAll About GSTR 3B With Latest AmendmentsDINESH CHANCHALANINo ratings yet

- Circular CGST 197Document5 pagesCircular CGST 197Jaipur-B Gr-2No ratings yet

- 30.07.2020 - CGST Rules, 2017 - (Part-A - Rules)Document164 pages30.07.2020 - CGST Rules, 2017 - (Part-A - Rules)Dost BhawanaNo ratings yet

- Basic GST - AmitDocument34 pagesBasic GST - AmitRohit MuleyNo ratings yet

- Circular CGST 123Document4 pagesCircular CGST 123AKSHATANo ratings yet

- ST ND: 1 - Ca Shubham Khaitan S.Khaitan and AssociatesDocument9 pagesST ND: 1 - Ca Shubham Khaitan S.Khaitan and AssociatesTaruna BajajNo ratings yet

- Section: A MCQ 20X1 20 Marks: A. B. C. DDocument12 pagesSection: A MCQ 20X1 20 Marks: A. B. C. DSarath KumarNo ratings yet

- 147 147 Circular12072021144813Document5 pages147 147 Circular12072021144813sumit71sharmaNo ratings yet

- 37th GSTC Meeting - 02Document2 pages37th GSTC Meeting - 02Sahil ShahNo ratings yet

- Before The Madurai Bench of Madras High Court W.P. (MD) .Nos.7173 and 7174 of 2023 andDocument8 pagesBefore The Madurai Bench of Madras High Court W.P. (MD) .Nos.7173 and 7174 of 2023 andHARIDWARNA CHARITABLE TRUSTNo ratings yet

- PRADIPDocument7 pagesPRADIPGovindNo ratings yet

- Exports - Furnishing of Bond/Letter of Undertaking For Exports - ClarificationDocument11 pagesExports - Furnishing of Bond/Letter of Undertaking For Exports - ClarificationRohan KulkarniNo ratings yet

- Input Tax Credit Cannot Be Denied To Purchaser Merely Because Seller Didnt Record Transaction in GSTR-2A Form - Kerala High CourtDocument9 pagesInput Tax Credit Cannot Be Denied To Purchaser Merely Because Seller Didnt Record Transaction in GSTR-2A Form - Kerala High CourtdeepakasopaNo ratings yet

- A Comparative Analysis of Tax Administration in Asia and the Pacific: Fifth EditionFrom EverandA Comparative Analysis of Tax Administration in Asia and the Pacific: Fifth EditionNo ratings yet

- Invoice 127433138Document1 pageInvoice 127433138ADARSH TIWARINo ratings yet

- GST 2016346532Document1 pageGST 2016346532ADARSH TIWARINo ratings yet

- GST 2016406656Document1 pageGST 2016406656ADARSH TIWARINo ratings yet

- GST ChallanDocument2 pagesGST ChallanADARSH TIWARINo ratings yet

- The Theories of International BusinessDocument13 pagesThe Theories of International BusinessHasnour MoyoNo ratings yet

- Shipment Schedule PT. Super Supply ChainDocument2 pagesShipment Schedule PT. Super Supply Chainreza arrachmanNo ratings yet

- Anneaux Levage CATDocument13 pagesAnneaux Levage CATA100% (1)

- Steel Infographic July 2022Document1 pageSteel Infographic July 2022revathykchettyNo ratings yet

- Deutsche Edelstahlwerke GMBH, Plant Witten: This Is To CertifyDocument3 pagesDeutsche Edelstahlwerke GMBH, Plant Witten: This Is To CertifyardeshirNo ratings yet

- Tutorial ElasticityDocument7 pagesTutorial ElasticityLena LeezNo ratings yet

- Jurnal Akuntansi AKTIVA, Vol. 2, No. 1, April 2021: Astuti Anggraini Yulita Zanaria Sri Retnaning RahayuDocument11 pagesJurnal Akuntansi AKTIVA, Vol. 2, No. 1, April 2021: Astuti Anggraini Yulita Zanaria Sri Retnaning RahayuRamadhini WNo ratings yet

- Compensating Variation, Equivalent Variation, Consumer Surplus, Revealed PreferenceDocument10 pagesCompensating Variation, Equivalent Variation, Consumer Surplus, Revealed Preferencehishamsauk100% (1)

- 2-11 Process Constraint Identification (ABBE-R031104)Document37 pages2-11 Process Constraint Identification (ABBE-R031104)lrff1950No ratings yet

- J.D Bank Alfalah Operation ManagerDocument3 pagesJ.D Bank Alfalah Operation ManagerMehwish RasheedNo ratings yet

- TaxAcc 2 - Assignment #3 Posadas Sec-CDocument5 pagesTaxAcc 2 - Assignment #3 Posadas Sec-CCendimee PosadasNo ratings yet

- Deed of Donation & Certificate of AcceptanceDocument2 pagesDeed of Donation & Certificate of AcceptanceByron DizonNo ratings yet

- Sample SPA - Sale (Shares)Document1 pageSample SPA - Sale (Shares)Anonymous RNdYSJNo ratings yet

- Collaboration AgreementDocument6 pagesCollaboration AgreementDurairaj SampathkumarNo ratings yet

- Running Event Waiver Form: (Signature Required)Document1 pageRunning Event Waiver Form: (Signature Required)Rizza Angela MangallenoNo ratings yet

- PlanDocument10 pagesPlanHanny ValenciaNo ratings yet

- Managers and The Legal Environment 9th Edition Bagley Test BankDocument25 pagesManagers and The Legal Environment 9th Edition Bagley Test BankDrRubenMartinezMDspcg100% (59)

- Political Theory Volume 22 Issue 4 1994 (Doi 10.2307/192041) Nancy Fraser - After The Family Wage - Gender Equity and The Welfare StateDocument29 pagesPolitical Theory Volume 22 Issue 4 1994 (Doi 10.2307/192041) Nancy Fraser - After The Family Wage - Gender Equity and The Welfare StateJürgen PortschyNo ratings yet

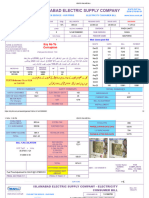

- IESCO BillDocument2 pagesIESCO Billtehreem tanveerNo ratings yet

- Roll Me A Ruler - by Assassin NPCDocument7 pagesRoll Me A Ruler - by Assassin NPCAntônioNo ratings yet

- Px2K Globally Approved, Explosive Atmosphere Barrier Cable Gland For All Types of Armoured CablesDocument1 pagePx2K Globally Approved, Explosive Atmosphere Barrier Cable Gland For All Types of Armoured Cablescahyo sNo ratings yet

- Managing Infrastructure For Next GenerationDocument15 pagesManaging Infrastructure For Next GenerationNathalie Hernández Rodríguez0% (1)

- Tax Invoice / Bill of SupplyDocument1 pageTax Invoice / Bill of SupplyabhimanyuNo ratings yet

- International StrategyDocument26 pagesInternational StrategyQuân Đoàn MinhNo ratings yet

- Ratio and ProportionDocument11 pagesRatio and ProportionCharmaine Joy UntalanNo ratings yet