Download as pdf or txt

You might also like

- Solution - North Village Capital Private EquityDocument9 pagesSolution - North Village Capital Private Equitykeerthana100% (1)

- Notes Payable, Long-Term Debt, and Interest NarrativeDocument3 pagesNotes Payable, Long-Term Debt, and Interest NarrativeCaterina De Luca100% (3)

- SMART MONEY ORDE BLOC EditedDocument9 pagesSMART MONEY ORDE BLOC Editedtawhid anam88% (8)

- Annexa Prime Trading CoursesDocument11 pagesAnnexa Prime Trading CoursesFatima FX100% (1)

- Intermediate Accounting 1: a QuickStudy Digital Reference GuideFrom EverandIntermediate Accounting 1: a QuickStudy Digital Reference GuideNo ratings yet

- MFRS 119 Employee BenefitsDocument38 pagesMFRS 119 Employee BenefitsAin YanieNo ratings yet

- Chapter 6 Emplooyee Benefit Part 2Document8 pagesChapter 6 Emplooyee Benefit Part 2maria isabellaNo ratings yet

- Employee Benefits 03Document11 pagesEmployee Benefits 03Nelva Quinio33% (3)

- JANBI Model Questions - Principles & Practices of Banking - 0Document8 pagesJANBI Model Questions - Principles & Practices of Banking - 0Biswajit Das0% (1)

- Ias 19Document9 pagesIas 19Hammad SarwarNo ratings yet

- MODULE Midterm FAR 3 EmpBenefitsDocument15 pagesMODULE Midterm FAR 3 EmpBenefitsKezNo ratings yet

- MODULE Midterm FAR 3 EmpBenefitsDocument15 pagesMODULE Midterm FAR 3 EmpBenefitsJohn Mark FernandoNo ratings yet

- IAS 19 Employee BenefitsDocument32 pagesIAS 19 Employee BenefitsTamirat Eshetu WoldeNo ratings yet

- SBR - Chapter 5Document6 pagesSBR - Chapter 5Jason KumarNo ratings yet

- Frs 119 Employee BenefitDocument54 pagesFrs 119 Employee BenefitNahar SabirahNo ratings yet

- CFAP 1Document10 pagesCFAP 1Sohaib AhmedNo ratings yet

- Pas 19Document5 pagesPas 19elle friasNo ratings yet

- Module 1 - Employee BenefitsDocument38 pagesModule 1 - Employee BenefitsMitchie Faustino100% (1)

- 104 Accounting QuizDocument3 pages104 Accounting Quizhyunsuk fhebieNo ratings yet

- Employee Benefit PlanDocument8 pagesEmployee Benefit PlantinydmpNo ratings yet

- Unit 7 E-Tutor PresentationDocument18 pagesUnit 7 E-Tutor PresentationKatrina EustaceNo ratings yet

- Analysis of Finanacing ActivitiesDocument48 pagesAnalysis of Finanacing ActivitiesPrateek SinglaNo ratings yet

- Employee Benefits: Cruz, Jerica May A. CBET-01-501EDocument21 pagesEmployee Benefits: Cruz, Jerica May A. CBET-01-501Eclara san miguelNo ratings yet

- Ias 19 Employee BenefitsDocument43 pagesIas 19 Employee BenefitsHasan Ali BokhariNo ratings yet

- Post Employment BenefitsDocument31 pagesPost Employment BenefitsSky SoronoiNo ratings yet

- Esmerah Lika B. Ilatan BSA-3: Assignment Postemployment BenefitsDocument3 pagesEsmerah Lika B. Ilatan BSA-3: Assignment Postemployment BenefitsKakay AccireNo ratings yet

- Quizlet 6Document3 pagesQuizlet 6Abdul Rahim RattaniNo ratings yet

- April 7 - CH 20 Part IDocument21 pagesApril 7 - CH 20 Part IMichael NguyenNo ratings yet

- LKAS 19 2021 UploadDocument31 pagesLKAS 19 2021 Uploadpriyantha dasanayake100% (2)

- FARAP-4513 (Post-Employment Benefits)Document5 pagesFARAP-4513 (Post-Employment Benefits)Rinoah Mae OlorosoNo ratings yet

- IAS 19 NotesDocument15 pagesIAS 19 NotesArsalan AliNo ratings yet

- Financial Statement Analysis: K R Subramanyam John J WildDocument35 pagesFinancial Statement Analysis: K R Subramanyam John J WildnadiaNo ratings yet

- Employee BenefitsDocument9 pagesEmployee BenefitstinydmpNo ratings yet

- FARAP-4413 (Post-Employment Benefits)Document5 pagesFARAP-4413 (Post-Employment Benefits)Dizon Ropalito P.No ratings yet

- Objectives: Chapter 5 - Employee Benefits - Ias 19Document82 pagesObjectives: Chapter 5 - Employee Benefits - Ias 19Tram NguyenNo ratings yet

- Employee BenefitsDocument9 pagesEmployee BenefitstinydmpNo ratings yet

- REVISED EMPLOYEES BENIFITS IAS 19 and IFRS 2Document8 pagesREVISED EMPLOYEES BENIFITS IAS 19 and IFRS 2It'z Pragmatic IbrahimNo ratings yet

- IAS 19 Employee Benefits StudentDocument40 pagesIAS 19 Employee Benefits StudentYI WEI CHANGNo ratings yet

- Chapter 4 - Accounting For Other Liabilities: A. Post Employment BenefitsDocument50 pagesChapter 4 - Accounting For Other Liabilities: A. Post Employment BenefitsLovely AbadianoNo ratings yet

- Topic 3.2 Employee BenefitsDocument15 pagesTopic 3.2 Employee BenefitsJayson KlineNo ratings yet

- Chapter 17Document54 pagesChapter 17wennstyleNo ratings yet

- Lecture Notes Employee Benefits: Page 1 of 16Document16 pagesLecture Notes Employee Benefits: Page 1 of 16fastslowerNo ratings yet

- Unit 03Document9 pagesUnit 03bobo tangaNo ratings yet

- Slide Chapter 3 Analyzing Financing ActivitiesDocument40 pagesSlide Chapter 3 Analyzing Financing ActivitiesardhikasatriaNo ratings yet

- Chapter 03 Analyzing Financing ActivitiesDocument40 pagesChapter 03 Analyzing Financing Activitiesshabrina rNo ratings yet

- IAS 19 Employee BenefitsDocument22 pagesIAS 19 Employee Benefitsanon_419651076No ratings yet

- IAS 19 NotesDocument16 pagesIAS 19 NotesArsalan AliNo ratings yet

- Contributions TDocument6 pagesContributions TRena Jocelle NalzaroNo ratings yet

- IAS 19 Employee Benefits (2021)Document6 pagesIAS 19 Employee Benefits (2021)Tawanda Tatenda Herbert100% (1)

- Accounting For Employment BenefitsDocument5 pagesAccounting For Employment BenefitsiamacrusaderNo ratings yet

- Employer Benefit - Part 2Document9 pagesEmployer Benefit - Part 2Julian Adam PagalNo ratings yet

- Accounting For Employment Benefits PDF FreeDocument5 pagesAccounting For Employment Benefits PDF FreeTrisha Mae BujalanceNo ratings yet

- CH20 PDFDocument81 pagesCH20 PDFelaine aureliaNo ratings yet

- Employee BenefitsDocument31 pagesEmployee BenefitsHazel PachecoNo ratings yet

- Module 3 Packet: College of CommerceDocument21 pagesModule 3 Packet: College of CommerceDexie Jane MayoNo ratings yet

- Postemployment BenefitsDocument22 pagesPostemployment BenefitsChoco ButternutNo ratings yet

- EmployeebenefitsreportDocument172 pagesEmployeebenefitsreportMikaela LacabaNo ratings yet

- Employee Benefits Ias19Document42 pagesEmployee Benefits Ias19krishnaguptaNo ratings yet

- SBR Assigment-Liam'sDocument7 pagesSBR Assigment-Liam'sbuls eyeNo ratings yet

- Cfas Pas 19Document4 pagesCfas Pas 19Zyribelle Anne JAPSONNo ratings yet

- Accounting For PensionsDocument15 pagesAccounting For PensionsOnwuchekwa Chidi CalebNo ratings yet

- Ias 19Document43 pagesIas 19Reever RiverNo ratings yet

- Contributory, Funded (Managed by A Trustee) or Unfunded (Managed by The Employer), and Defined Contribution Plan or Defined Benefit PlanDocument5 pagesContributory, Funded (Managed by A Trustee) or Unfunded (Managed by The Employer), and Defined Contribution Plan or Defined Benefit PlanJustine VeralloNo ratings yet

- Partnership Corp. Chapter3Document17 pagesPartnership Corp. Chapter3deniseanne clementeNo ratings yet

- Saunders CH08 AccessibleDocument33 pagesSaunders CH08 AccessibleindriawardhaniNo ratings yet

- Financial Analysis of Britannia and DaburDocument8 pagesFinancial Analysis of Britannia and DaburBiplab MondalNo ratings yet

- Ifrs 13: Fair Value MeasurementDocument35 pagesIfrs 13: Fair Value MeasurementXXXXXXXXXXXXXXXXXXNo ratings yet

- Intaudp - Mem02Document2 pagesIntaudp - Mem02Cal PedreroNo ratings yet

- Phillips, Hager & North Global Equity Fund F: Growth of 10,000 10-09-2009 - 10-09-2019 Morningstar Risk MeasuresDocument3 pagesPhillips, Hager & North Global Equity Fund F: Growth of 10,000 10-09-2009 - 10-09-2019 Morningstar Risk MeasuresRoger SongNo ratings yet

- Finals - Com 505 ReviewerDocument29 pagesFinals - Com 505 ReviewerPAULYNE BONGALOSNo ratings yet

- Chapter 02 - How To Calculate Present ValuesDocument18 pagesChapter 02 - How To Calculate Present ValuesTrinh VũNo ratings yet

- What Is Masala Bond - QuoraDocument6 pagesWhat Is Masala Bond - QuoraSriramPrasannabalajiNo ratings yet

- VFV Vs VSPDocument2 pagesVFV Vs VSPAnonymous P73cUg73LNo ratings yet

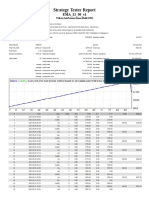

- StrategyTesterEMA21 EMA 50 1 Tahun - ResultDocument6 pagesStrategyTesterEMA21 EMA 50 1 Tahun - ResultHadiyatno HalibNo ratings yet

- Chapter 7 Prospective Analysis: Valuation Theory and ConceptsDocument9 pagesChapter 7 Prospective Analysis: Valuation Theory and ConceptsWalm KetyNo ratings yet

- UntitledDocument32 pagesUntitledShine ButconNo ratings yet

- IFRS 1 - For PresDocument27 pagesIFRS 1 - For Presnati67% (3)

- Reaction Paper: Explained - The Stock Market - NetflixDocument2 pagesReaction Paper: Explained - The Stock Market - Netflixmary grace cornelioNo ratings yet

- The Initial Public Offering (IPO) : Presented By: Farzana Sayyed Roll No: 40Document18 pagesThe Initial Public Offering (IPO) : Presented By: Farzana Sayyed Roll No: 40Farzana SayyedNo ratings yet

- Collapse of The LTCMDocument42 pagesCollapse of The LTCMPriya UpadhyayNo ratings yet

- Blue Bill Corp Module 6 Assignment-1cxlc8byxz6r5 - 1euusngisn9vlDocument4 pagesBlue Bill Corp Module 6 Assignment-1cxlc8byxz6r5 - 1euusngisn9vlKimberley WrightNo ratings yet

- Stock Market QuizDocument5 pagesStock Market QuizRavi KiranNo ratings yet

- Kohinoor Chemical Assumptions, ConstrainsDocument6 pagesKohinoor Chemical Assumptions, ConstrainsFYAJ ROHANNo ratings yet

- Assignment Sw#1 Mod3 Return & Risk Multiple Choice ADocument6 pagesAssignment Sw#1 Mod3 Return & Risk Multiple Choice AAra FloresNo ratings yet

- EF3442 Intermediate MicroeconomicsDocument6 pagesEF3442 Intermediate MicroeconomicsAshtar Ali Bangash100% (1)

- Accounts of Holding CompaniesDocument16 pagesAccounts of Holding CompaniesNawab Ali Khan100% (1)

- T04 - Risks Cost of CapitalDocument80 pagesT04 - Risks Cost of CapitalAzureBlazeNo ratings yet

- PT Bank Mandiri (Persero) TBK BMRIDocument3 pagesPT Bank Mandiri (Persero) TBK BMRIDaniel Hanry SitompulNo ratings yet