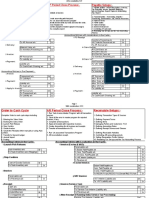

IAS 20 Chart

IAS 20 Chart

You might also like

- Fce 2015 Complete Tests 1 e 2 AnswersDocument4 pagesFce 2015 Complete Tests 1 e 2 AnswersMárcia Bonfim83% (23)

- UndergroundG StyleHandgunMainManual PDFDocument46 pagesUndergroundG StyleHandgunMainManual PDFRick Gaines100% (2)

- Mathematics of InvestmentsDocument2 pagesMathematics of InvestmentsShiera Saletrero SimbajonNo ratings yet

- Notes For L2Document9 pagesNotes For L2yuyin.gohyyNo ratings yet

- MyacccheatDocument5 pagesMyacccheatraygains23No ratings yet

- Company Accounts - Issue of DebenturesDocument11 pagesCompany Accounts - Issue of DebenturesHarsh MishraNo ratings yet

- Final Accounts With AdjustmentsDocument4 pagesFinal Accounts With AdjustmentsDivyaman RamawatNo ratings yet

- O2C P2P Accounting Entries With India Localization PDFDocument2 pagesO2C P2P Accounting Entries With India Localization PDFAvijit BanerjeeNo ratings yet

- Final Account Adjusment Entry - 2Document3 pagesFinal Account Adjusment Entry - 2khanpur88822No ratings yet

- Governmental Fund Financial StatementsDocument5 pagesGovernmental Fund Financial StatementsGift ChaliNo ratings yet

- Pensions Practice QuizDocument10 pagesPensions Practice QuizJyNo ratings yet

- AS 12 - Governemnt GrantsDocument5 pagesAS 12 - Governemnt GrantsaslngNo ratings yet

- IA - Receivables Addtl ConceptsDocument3 pagesIA - Receivables Addtl ConceptsDiana AcostaNo ratings yet

- CH - 02 Issue and Redemption of DebenturesDocument7 pagesCH - 02 Issue and Redemption of DebenturesMahathi AmudhanNo ratings yet

- Accounting - AP, FA, ARDocument4 pagesAccounting - AP, FA, ARVinoth Kumar KNo ratings yet

- Issue of DebenturesDocument12 pagesIssue of Debenturessiva883100% (1)

- ACT112-Module 2-Receivables-Part 3Document39 pagesACT112-Module 2-Receivables-Part 3Charish Ann SimbajonNo ratings yet

- IAS 20 Accounting For Government Grants and Disclosure of Government AssistanceDocument1 pageIAS 20 Accounting For Government Grants and Disclosure of Government Assistanceamanda kNo ratings yet

- Admission of A Parnter - Work Sheet No - 2Document7 pagesAdmission of A Parnter - Work Sheet No - 2BLUE SKY GAMINGNo ratings yet

- ACC3606Document3 pagesACC3606Anan ShaoNo ratings yet

- 4 - Test 4 SolutionDocument7 pages4 - Test 4 SolutionAashika SamaiyaNo ratings yet

- As 12Document11 pagesAs 12Dipak UgaleNo ratings yet

- Afgnpo MidtermDocument12 pagesAfgnpo Midtermjr centenoNo ratings yet

- Accounting EntriesDocument7 pagesAccounting EntriesVikram Thodupunoori100% (1)

- 3 FinalAccounts - AFB - Module CDocument23 pages3 FinalAccounts - AFB - Module Cwaste mailNo ratings yet

- Addendum (30.8.2022)Document4 pagesAddendum (30.8.2022)Arjita DubeyNo ratings yet

- Provision For DepreciationDocument10 pagesProvision For DepreciationAsh InuNo ratings yet

- Chap 12 NotesDocument3 pagesChap 12 NotesrbarronsolutionsNo ratings yet

- Redemption of Debentures FA - III1644399049Document48 pagesRedemption of Debentures FA - III1644399049Shaista SultanaNo ratings yet

- IAS 20 Government GrantsDocument16 pagesIAS 20 Government GrantsmekuleileNo ratings yet

- Accounting Statement For Issue of Debentures For The Consideration of Cash.Document8 pagesAccounting Statement For Issue of Debentures For The Consideration of Cash.Vinamra MathurNo ratings yet

- CDC LIQUIDATION PLAN FORMAT - SBA CompleteDocument6 pagesCDC LIQUIDATION PLAN FORMAT - SBA CompleteMoureen MosotiNo ratings yet

- Accounting Entries For Payables and ReceivablesDocument2 pagesAccounting Entries For Payables and Receivableskotesh kumNo ratings yet

- GH002204 - SANRU - Y2Continuation - TR PDFDocument13 pagesGH002204 - SANRU - Y2Continuation - TR PDFDenis MatshifiNo ratings yet

- Solution Ultimate Sample Paper 2Document7 pagesSolution Ultimate Sample Paper 2Nitin KumarNo ratings yet

- CCP402Document15 pagesCCP402api-3849444No ratings yet

- Ac Entries ARDocument2 pagesAc Entries ARMahendar Naidu ANo ratings yet

- Partnership: AdmissionDocument7 pagesPartnership: AdmissionSweta SinghNo ratings yet

- A3. Year End AdjustmentsDocument9 pagesA3. Year End AdjustmentsFrankNo ratings yet

- Non-Current Liabilities (Bonds Payable) Issuing BondsDocument11 pagesNon-Current Liabilities (Bonds Payable) Issuing BondsDiahNo ratings yet

- Subsidy From NG and Other NGAsDocument4 pagesSubsidy From NG and Other NGAsWawex DavisNo ratings yet

- IND AS 20 - Bhavik Chokshi - FR ShieldDocument7 pagesIND AS 20 - Bhavik Chokshi - FR ShieldSoham Upadhyay100% (1)

- Basics of Accounting - QBDocument7 pagesBasics of Accounting - QBsujanthqatarNo ratings yet

- Accountancy 2008Document23 pagesAccountancy 2008Piyush SrivastavaNo ratings yet

- Solution of Chapter 5Document3 pagesSolution of Chapter 5Minh Do Ky0% (1)

- Worksheet On Issue of Debenture - Board QuestionsDocument12 pagesWorksheet On Issue of Debenture - Board QuestionsCfa Deepti BindalNo ratings yet

- Final Reviewer GovaccDocument7 pagesFinal Reviewer GovaccShane TorrieNo ratings yet

- AP0004.02 Loan Receivable and ECL ModelDocument4 pagesAP0004.02 Loan Receivable and ECL ModelKatrina Peralta FabianNo ratings yet

- Notes On Chapter 19 Financial Statements - With AdjustmentsDocument10 pagesNotes On Chapter 19 Financial Statements - With Adjustmentspvaghasiya7535No ratings yet

- ACT B861F - Tutorial Questions and SolutionDocument13 pagesACT B861F - Tutorial Questions and SolutionCalvin MaNo ratings yet

- CA-Foundation June 2023 Free Test - SUGGESTED ANSWERSDocument17 pagesCA-Foundation June 2023 Free Test - SUGGESTED ANSWERSAastha ShrivastavaNo ratings yet

- Internal Reconstruction - HomeworkDocument25 pagesInternal Reconstruction - HomeworkYash ShewaleNo ratings yet

- Causes of DepreciationDocument6 pagesCauses of DepreciationSHEKHAR SHUKLANo ratings yet

- TEMPORARY ADVANCEGPF-2023-24-15006 - Thu Oct 12 15 - 37 - 15 IST 2023Document2 pagesTEMPORARY ADVANCEGPF-2023-24-15006 - Thu Oct 12 15 - 37 - 15 IST 2023hemantaduttaghy1No ratings yet

- Gov. Note No.3-Investment Expenditures (External)Document7 pagesGov. Note No.3-Investment Expenditures (External)Eman AbasiryNo ratings yet

- Xi See Acc 2021 Set 2 MsDocument5 pagesXi See Acc 2021 Set 2 Mss1672snehil6353No ratings yet

- MTP 23 54 Answers 1717828857Document15 pagesMTP 23 54 Answers 1717828857himanirajora4452No ratings yet

- Ty Baf Q 17 SolutionDocument1 pageTy Baf Q 17 SolutionGANESHNo ratings yet

- P2P & O2C (Entries)Document9 pagesP2P & O2C (Entries)hari koppalaNo ratings yet

- TEMPORARY ADVANCEGPF-2023-24-15006 - Mon Oct 30 22 - 58 - 41 IST 2023Document2 pagesTEMPORARY ADVANCEGPF-2023-24-15006 - Mon Oct 30 22 - 58 - 41 IST 2023hemantaduttaghy1No ratings yet

- Government Accounting QuizDocument2 pagesGovernment Accounting QuizKate Fernandez100% (2)

- Accounting For Capital Projects and Debt ServiceDocument38 pagesAccounting For Capital Projects and Debt ServiceAroel VaganzhaNo ratings yet

- How To File Your Own Bankruptcy: The Step-by-Step Handbook to Filing Your Own Bankruptcy PetitionFrom EverandHow To File Your Own Bankruptcy: The Step-by-Step Handbook to Filing Your Own Bankruptcy PetitionNo ratings yet

- Understanding The Recent Monetary Policy and What It Entails For The Nigerian Economy - Ugochukwu AnthonyDocument10 pagesUnderstanding The Recent Monetary Policy and What It Entails For The Nigerian Economy - Ugochukwu Anthonyabdulbasitabdulazeez30No ratings yet

- Chapter 7 PowerPointDocument37 pagesChapter 7 PowerPointabdulbasitabdulazeez30No ratings yet

- Decision MakingDocument21 pagesDecision Makingabdulbasitabdulazeez30No ratings yet

- IAS 10 - EVENTS AFTER Q OnlyDocument5 pagesIAS 10 - EVENTS AFTER Q Onlyabdulbasitabdulazeez30No ratings yet

- Risk ManagementDocument18 pagesRisk Managementabdulbasitabdulazeez30No ratings yet

- Corporate GovernanceDocument42 pagesCorporate Governanceabdulbasitabdulazeez30No ratings yet

- Chords Like Jeff BuckleyDocument5 pagesChords Like Jeff BuckleyTDROCKNo ratings yet

- Bsl6 Qual Spec 11-12 FinalDocument35 pagesBsl6 Qual Spec 11-12 FinalBSLcourses.co.ukNo ratings yet

- Répit Transit (English Version)Document5 pagesRépit Transit (English Version)CTREQ école-famille-communautéNo ratings yet

- Testi I Pare YlberiDocument6 pagesTesti I Pare YlberiAhmetNo ratings yet

- LP in MusicDocument10 pagesLP in MusicContagious Joy VillapandoNo ratings yet

- Redeemable Preference SharesDocument2 pagesRedeemable Preference Sharestanvia KNo ratings yet

- Precis WritingDocument37 pagesPrecis WritingLetlie SemblanteNo ratings yet

- Ahad NaamahDocument2 pagesAhad NaamahedoolawNo ratings yet

- Break Even AnalysisDocument18 pagesBreak Even AnalysisSMHE100% (10)

- Full Download Art of Leadership 5th Edition Manning Test Bank PDF Full ChapterDocument36 pagesFull Download Art of Leadership 5th Edition Manning Test Bank PDF Full Chaptermasqueedenized8a43l100% (19)

- Birds: Prof. AN. Subramanian and Dr. A. SethuramanDocument8 pagesBirds: Prof. AN. Subramanian and Dr. A. SethuramanMuh SaifullahNo ratings yet

- Unit 8 Our World Heritage Sites Lesson 3 ReadingDocument41 pagesUnit 8 Our World Heritage Sites Lesson 3 ReadingThái HoàngNo ratings yet

- SHW8Z - Shiraplas 85PDocument9 pagesSHW8Z - Shiraplas 85PfrankieNo ratings yet

- SWM Notes IIDocument8 pagesSWM Notes IIBeast gaming liveNo ratings yet

- Practical Work 1 EventDocument19 pagesPractical Work 1 EventNur ShakirinNo ratings yet

- KELOMPOK 04 PPT AUDIT Siklus Perolehan Dan Pembayaran EditDocument39 pagesKELOMPOK 04 PPT AUDIT Siklus Perolehan Dan Pembayaran EditAkuntansi 6511No ratings yet

- Quotation - ABS 2020-21 - E203 - Mr. K Ramesh ReddyDocument1 pageQuotation - ABS 2020-21 - E203 - Mr. K Ramesh ReddyairblisssolutionsNo ratings yet

- Construction Contract: Contract For Construction of Apco Hyundai Car Showroom at Uppala, Kasaragod, KeralaDocument2 pagesConstruction Contract: Contract For Construction of Apco Hyundai Car Showroom at Uppala, Kasaragod, KeralakrishnanunniNo ratings yet

- HDPR Cluster Resolution No. 1, S. 2012 - RH Bill - FinalDocument2 pagesHDPR Cluster Resolution No. 1, S. 2012 - RH Bill - FinalMaria Amparo WarrenNo ratings yet

- General: Specific: Leading Statement:: TITLE: A Healthy LifestyleDocument2 pagesGeneral: Specific: Leading Statement:: TITLE: A Healthy LifestyleM Arshad M AmirNo ratings yet

- Mauro Giuliani: Etudes Instructives, Op. 100Document35 pagesMauro Giuliani: Etudes Instructives, Op. 100Thiago Camargo Juvito de Souza100% (1)

- PHIN101 HandoutDocument7 pagesPHIN101 HandoutVeronica ShaneNo ratings yet

- Justin Bieber Is - Famous Singer.: (You Must Read Out The Whole Sentence.)Document2 pagesJustin Bieber Is - Famous Singer.: (You Must Read Out The Whole Sentence.)Irene De la FuenteNo ratings yet

- 1st Year Chemistry Pairing Scheme 2021 - 11th Class - Ratta - PKDocument2 pages1st Year Chemistry Pairing Scheme 2021 - 11th Class - Ratta - PKazeemNo ratings yet

- The DJ Test: Personalised Report and Recommendations For Alex YachevskiDocument34 pagesThe DJ Test: Personalised Report and Recommendations For Alex YachevskiSashadanceNo ratings yet

- Communication MatrixDocument1 pageCommunication Matrixrohini kadamNo ratings yet

- History of The Negro Race in America From 1619 To 1880. Vol. 2 (Of 2) Negroes As Slaves, As Soldiers, and As Citizens by Williams, George WashingtonDocument476 pagesHistory of The Negro Race in America From 1619 To 1880. Vol. 2 (Of 2) Negroes As Slaves, As Soldiers, and As Citizens by Williams, George WashingtonGutenberg.org100% (2)

Download as pdf or txt

You might also like

- Fce 2015 Complete Tests 1 e 2 AnswersDocument4 pagesFce 2015 Complete Tests 1 e 2 AnswersMárcia Bonfim83% (23)

- UndergroundG StyleHandgunMainManual PDFDocument46 pagesUndergroundG StyleHandgunMainManual PDFRick Gaines100% (2)

- Mathematics of InvestmentsDocument2 pagesMathematics of InvestmentsShiera Saletrero SimbajonNo ratings yet

- Notes For L2Document9 pagesNotes For L2yuyin.gohyyNo ratings yet

- MyacccheatDocument5 pagesMyacccheatraygains23No ratings yet

- Company Accounts - Issue of DebenturesDocument11 pagesCompany Accounts - Issue of DebenturesHarsh MishraNo ratings yet

- Final Accounts With AdjustmentsDocument4 pagesFinal Accounts With AdjustmentsDivyaman RamawatNo ratings yet

- O2C P2P Accounting Entries With India Localization PDFDocument2 pagesO2C P2P Accounting Entries With India Localization PDFAvijit BanerjeeNo ratings yet

- Final Account Adjusment Entry - 2Document3 pagesFinal Account Adjusment Entry - 2khanpur88822No ratings yet

- Governmental Fund Financial StatementsDocument5 pagesGovernmental Fund Financial StatementsGift ChaliNo ratings yet

- Pensions Practice QuizDocument10 pagesPensions Practice QuizJyNo ratings yet

- AS 12 - Governemnt GrantsDocument5 pagesAS 12 - Governemnt GrantsaslngNo ratings yet

- IA - Receivables Addtl ConceptsDocument3 pagesIA - Receivables Addtl ConceptsDiana AcostaNo ratings yet

- CH - 02 Issue and Redemption of DebenturesDocument7 pagesCH - 02 Issue and Redemption of DebenturesMahathi AmudhanNo ratings yet

- Accounting - AP, FA, ARDocument4 pagesAccounting - AP, FA, ARVinoth Kumar KNo ratings yet

- Issue of DebenturesDocument12 pagesIssue of Debenturessiva883100% (1)

- ACT112-Module 2-Receivables-Part 3Document39 pagesACT112-Module 2-Receivables-Part 3Charish Ann SimbajonNo ratings yet

- IAS 20 Accounting For Government Grants and Disclosure of Government AssistanceDocument1 pageIAS 20 Accounting For Government Grants and Disclosure of Government Assistanceamanda kNo ratings yet

- Admission of A Parnter - Work Sheet No - 2Document7 pagesAdmission of A Parnter - Work Sheet No - 2BLUE SKY GAMINGNo ratings yet

- ACC3606Document3 pagesACC3606Anan ShaoNo ratings yet

- 4 - Test 4 SolutionDocument7 pages4 - Test 4 SolutionAashika SamaiyaNo ratings yet

- As 12Document11 pagesAs 12Dipak UgaleNo ratings yet

- Afgnpo MidtermDocument12 pagesAfgnpo Midtermjr centenoNo ratings yet

- Accounting EntriesDocument7 pagesAccounting EntriesVikram Thodupunoori100% (1)

- 3 FinalAccounts - AFB - Module CDocument23 pages3 FinalAccounts - AFB - Module Cwaste mailNo ratings yet

- Addendum (30.8.2022)Document4 pagesAddendum (30.8.2022)Arjita DubeyNo ratings yet

- Provision For DepreciationDocument10 pagesProvision For DepreciationAsh InuNo ratings yet

- Chap 12 NotesDocument3 pagesChap 12 NotesrbarronsolutionsNo ratings yet

- Redemption of Debentures FA - III1644399049Document48 pagesRedemption of Debentures FA - III1644399049Shaista SultanaNo ratings yet

- IAS 20 Government GrantsDocument16 pagesIAS 20 Government GrantsmekuleileNo ratings yet

- Accounting Statement For Issue of Debentures For The Consideration of Cash.Document8 pagesAccounting Statement For Issue of Debentures For The Consideration of Cash.Vinamra MathurNo ratings yet

- CDC LIQUIDATION PLAN FORMAT - SBA CompleteDocument6 pagesCDC LIQUIDATION PLAN FORMAT - SBA CompleteMoureen MosotiNo ratings yet

- Accounting Entries For Payables and ReceivablesDocument2 pagesAccounting Entries For Payables and Receivableskotesh kumNo ratings yet

- GH002204 - SANRU - Y2Continuation - TR PDFDocument13 pagesGH002204 - SANRU - Y2Continuation - TR PDFDenis MatshifiNo ratings yet

- Solution Ultimate Sample Paper 2Document7 pagesSolution Ultimate Sample Paper 2Nitin KumarNo ratings yet

- CCP402Document15 pagesCCP402api-3849444No ratings yet

- Ac Entries ARDocument2 pagesAc Entries ARMahendar Naidu ANo ratings yet

- Partnership: AdmissionDocument7 pagesPartnership: AdmissionSweta SinghNo ratings yet

- A3. Year End AdjustmentsDocument9 pagesA3. Year End AdjustmentsFrankNo ratings yet

- Non-Current Liabilities (Bonds Payable) Issuing BondsDocument11 pagesNon-Current Liabilities (Bonds Payable) Issuing BondsDiahNo ratings yet

- Subsidy From NG and Other NGAsDocument4 pagesSubsidy From NG and Other NGAsWawex DavisNo ratings yet

- IND AS 20 - Bhavik Chokshi - FR ShieldDocument7 pagesIND AS 20 - Bhavik Chokshi - FR ShieldSoham Upadhyay100% (1)

- Basics of Accounting - QBDocument7 pagesBasics of Accounting - QBsujanthqatarNo ratings yet

- Accountancy 2008Document23 pagesAccountancy 2008Piyush SrivastavaNo ratings yet

- Solution of Chapter 5Document3 pagesSolution of Chapter 5Minh Do Ky0% (1)

- Worksheet On Issue of Debenture - Board QuestionsDocument12 pagesWorksheet On Issue of Debenture - Board QuestionsCfa Deepti BindalNo ratings yet

- Final Reviewer GovaccDocument7 pagesFinal Reviewer GovaccShane TorrieNo ratings yet

- AP0004.02 Loan Receivable and ECL ModelDocument4 pagesAP0004.02 Loan Receivable and ECL ModelKatrina Peralta FabianNo ratings yet

- Notes On Chapter 19 Financial Statements - With AdjustmentsDocument10 pagesNotes On Chapter 19 Financial Statements - With Adjustmentspvaghasiya7535No ratings yet

- ACT B861F - Tutorial Questions and SolutionDocument13 pagesACT B861F - Tutorial Questions and SolutionCalvin MaNo ratings yet

- CA-Foundation June 2023 Free Test - SUGGESTED ANSWERSDocument17 pagesCA-Foundation June 2023 Free Test - SUGGESTED ANSWERSAastha ShrivastavaNo ratings yet

- Internal Reconstruction - HomeworkDocument25 pagesInternal Reconstruction - HomeworkYash ShewaleNo ratings yet

- Causes of DepreciationDocument6 pagesCauses of DepreciationSHEKHAR SHUKLANo ratings yet

- TEMPORARY ADVANCEGPF-2023-24-15006 - Thu Oct 12 15 - 37 - 15 IST 2023Document2 pagesTEMPORARY ADVANCEGPF-2023-24-15006 - Thu Oct 12 15 - 37 - 15 IST 2023hemantaduttaghy1No ratings yet

- Gov. Note No.3-Investment Expenditures (External)Document7 pagesGov. Note No.3-Investment Expenditures (External)Eman AbasiryNo ratings yet

- Xi See Acc 2021 Set 2 MsDocument5 pagesXi See Acc 2021 Set 2 Mss1672snehil6353No ratings yet

- MTP 23 54 Answers 1717828857Document15 pagesMTP 23 54 Answers 1717828857himanirajora4452No ratings yet

- Ty Baf Q 17 SolutionDocument1 pageTy Baf Q 17 SolutionGANESHNo ratings yet

- P2P & O2C (Entries)Document9 pagesP2P & O2C (Entries)hari koppalaNo ratings yet

- TEMPORARY ADVANCEGPF-2023-24-15006 - Mon Oct 30 22 - 58 - 41 IST 2023Document2 pagesTEMPORARY ADVANCEGPF-2023-24-15006 - Mon Oct 30 22 - 58 - 41 IST 2023hemantaduttaghy1No ratings yet

- Government Accounting QuizDocument2 pagesGovernment Accounting QuizKate Fernandez100% (2)

- Accounting For Capital Projects and Debt ServiceDocument38 pagesAccounting For Capital Projects and Debt ServiceAroel VaganzhaNo ratings yet

- How To File Your Own Bankruptcy: The Step-by-Step Handbook to Filing Your Own Bankruptcy PetitionFrom EverandHow To File Your Own Bankruptcy: The Step-by-Step Handbook to Filing Your Own Bankruptcy PetitionNo ratings yet

- Understanding The Recent Monetary Policy and What It Entails For The Nigerian Economy - Ugochukwu AnthonyDocument10 pagesUnderstanding The Recent Monetary Policy and What It Entails For The Nigerian Economy - Ugochukwu Anthonyabdulbasitabdulazeez30No ratings yet

- Chapter 7 PowerPointDocument37 pagesChapter 7 PowerPointabdulbasitabdulazeez30No ratings yet

- Decision MakingDocument21 pagesDecision Makingabdulbasitabdulazeez30No ratings yet

- IAS 10 - EVENTS AFTER Q OnlyDocument5 pagesIAS 10 - EVENTS AFTER Q Onlyabdulbasitabdulazeez30No ratings yet

- Risk ManagementDocument18 pagesRisk Managementabdulbasitabdulazeez30No ratings yet

- Corporate GovernanceDocument42 pagesCorporate Governanceabdulbasitabdulazeez30No ratings yet

- Chords Like Jeff BuckleyDocument5 pagesChords Like Jeff BuckleyTDROCKNo ratings yet

- Bsl6 Qual Spec 11-12 FinalDocument35 pagesBsl6 Qual Spec 11-12 FinalBSLcourses.co.ukNo ratings yet

- Répit Transit (English Version)Document5 pagesRépit Transit (English Version)CTREQ école-famille-communautéNo ratings yet

- Testi I Pare YlberiDocument6 pagesTesti I Pare YlberiAhmetNo ratings yet

- LP in MusicDocument10 pagesLP in MusicContagious Joy VillapandoNo ratings yet

- Redeemable Preference SharesDocument2 pagesRedeemable Preference Sharestanvia KNo ratings yet

- Precis WritingDocument37 pagesPrecis WritingLetlie SemblanteNo ratings yet

- Ahad NaamahDocument2 pagesAhad NaamahedoolawNo ratings yet

- Break Even AnalysisDocument18 pagesBreak Even AnalysisSMHE100% (10)

- Full Download Art of Leadership 5th Edition Manning Test Bank PDF Full ChapterDocument36 pagesFull Download Art of Leadership 5th Edition Manning Test Bank PDF Full Chaptermasqueedenized8a43l100% (19)

- Birds: Prof. AN. Subramanian and Dr. A. SethuramanDocument8 pagesBirds: Prof. AN. Subramanian and Dr. A. SethuramanMuh SaifullahNo ratings yet

- Unit 8 Our World Heritage Sites Lesson 3 ReadingDocument41 pagesUnit 8 Our World Heritage Sites Lesson 3 ReadingThái HoàngNo ratings yet

- SHW8Z - Shiraplas 85PDocument9 pagesSHW8Z - Shiraplas 85PfrankieNo ratings yet

- SWM Notes IIDocument8 pagesSWM Notes IIBeast gaming liveNo ratings yet

- Practical Work 1 EventDocument19 pagesPractical Work 1 EventNur ShakirinNo ratings yet

- KELOMPOK 04 PPT AUDIT Siklus Perolehan Dan Pembayaran EditDocument39 pagesKELOMPOK 04 PPT AUDIT Siklus Perolehan Dan Pembayaran EditAkuntansi 6511No ratings yet

- Quotation - ABS 2020-21 - E203 - Mr. K Ramesh ReddyDocument1 pageQuotation - ABS 2020-21 - E203 - Mr. K Ramesh ReddyairblisssolutionsNo ratings yet

- Construction Contract: Contract For Construction of Apco Hyundai Car Showroom at Uppala, Kasaragod, KeralaDocument2 pagesConstruction Contract: Contract For Construction of Apco Hyundai Car Showroom at Uppala, Kasaragod, KeralakrishnanunniNo ratings yet

- HDPR Cluster Resolution No. 1, S. 2012 - RH Bill - FinalDocument2 pagesHDPR Cluster Resolution No. 1, S. 2012 - RH Bill - FinalMaria Amparo WarrenNo ratings yet

- General: Specific: Leading Statement:: TITLE: A Healthy LifestyleDocument2 pagesGeneral: Specific: Leading Statement:: TITLE: A Healthy LifestyleM Arshad M AmirNo ratings yet

- Mauro Giuliani: Etudes Instructives, Op. 100Document35 pagesMauro Giuliani: Etudes Instructives, Op. 100Thiago Camargo Juvito de Souza100% (1)

- PHIN101 HandoutDocument7 pagesPHIN101 HandoutVeronica ShaneNo ratings yet

- Justin Bieber Is - Famous Singer.: (You Must Read Out The Whole Sentence.)Document2 pagesJustin Bieber Is - Famous Singer.: (You Must Read Out The Whole Sentence.)Irene De la FuenteNo ratings yet

- 1st Year Chemistry Pairing Scheme 2021 - 11th Class - Ratta - PKDocument2 pages1st Year Chemistry Pairing Scheme 2021 - 11th Class - Ratta - PKazeemNo ratings yet

- The DJ Test: Personalised Report and Recommendations For Alex YachevskiDocument34 pagesThe DJ Test: Personalised Report and Recommendations For Alex YachevskiSashadanceNo ratings yet

- Communication MatrixDocument1 pageCommunication Matrixrohini kadamNo ratings yet

- History of The Negro Race in America From 1619 To 1880. Vol. 2 (Of 2) Negroes As Slaves, As Soldiers, and As Citizens by Williams, George WashingtonDocument476 pagesHistory of The Negro Race in America From 1619 To 1880. Vol. 2 (Of 2) Negroes As Slaves, As Soldiers, and As Citizens by Williams, George WashingtonGutenberg.org100% (2)