Learning Unit 8 Financial Instruments IAS32 IFRS 7 and IFRS 9

Learning Unit 8 Financial Instruments IAS32 IFRS 7 and IFRS 9

You might also like

- Full Download Intermediate Accounting Volume 1 5th Edition Beechy Solutions ManualDocument35 pagesFull Download Intermediate Accounting Volume 1 5th Edition Beechy Solutions Manualwilliammwtc100% (35)

- Ifrs and Us Gaap Juin 2023Document236 pagesIfrs and Us Gaap Juin 2023fluffy fluffNo ratings yet

- Training: January 2012Document54 pagesTraining: January 2012Thulani NdlovuNo ratings yet

- Encounter Series FinalDocument9 pagesEncounter Series FinalThulani Ndlovu100% (1)

- ISO 22301: 2019 - An introduction to a business continuity management system (BCMS)From EverandISO 22301: 2019 - An introduction to a business continuity management system (BCMS)Rating: 4 out of 5 stars4/5 (1)

- CHAPTER-9-Principles of AccountingDocument39 pagesCHAPTER-9-Principles of AccountingNguyễn Ngọc AnhNo ratings yet

- P2 Basic PDFDocument289 pagesP2 Basic PDFPhil Sirius100% (1)

- The Theory and Practice of Investment ManagementDocument17 pagesThe Theory and Practice of Investment ManagementTri RamadhanNo ratings yet

- Ifrs 17 Implementation Guidance RevisedDocument44 pagesIfrs 17 Implementation Guidance RevisedMohammad IslamNo ratings yet

- Financial Accounting IDocument47 pagesFinancial Accounting Inerurkar_tusharNo ratings yet

- Level I Volume 5 2019 IFT NotesDocument258 pagesLevel I Volume 5 2019 IFT NotesNoor QamarNo ratings yet

- ACCT 302 Financial Reporting II Lecture 7Document63 pagesACCT 302 Financial Reporting II Lecture 7Jesse Nelson100% (1)

- Ipsas 5-Borrowing Costs: AcknowledgmentDocument13 pagesIpsas 5-Borrowing Costs: Acknowledgmentriska putri utamiNo ratings yet

- G10489 EC - Advanced Financial Accounting Primer PDFDocument65 pagesG10489 EC - Advanced Financial Accounting Primer PDFCassandra LynnNo ratings yet

- GRANT THORNTON - 2016.09 - Comparison Between U.S. GAAP and IFRSDocument228 pagesGRANT THORNTON - 2016.09 - Comparison Between U.S. GAAP and IFRSricardo.j.cruzNo ratings yet

- A34 Ipsas - 25 - 0Document81 pagesA34 Ipsas - 25 - 0Marius SteffyNo ratings yet

- Handbook Derivatives Hedging AccountingDocument1,228 pagesHandbook Derivatives Hedging AccountingVinayak SatheeshNo ratings yet

- Ey frdbb1793 08 12 2020 v2Document361 pagesEy frdbb1793 08 12 2020 v2Duyên Phạm KỳNo ratings yet

- Ias 32 J Ifrs 9 0 Ifric 7Document134 pagesIas 32 J Ifrs 9 0 Ifric 7ncubetalent1997No ratings yet

- Financial Statement Preparation and AnalysisDocument40 pagesFinancial Statement Preparation and AnalysisMD SAIFUL ISLAMNo ratings yet

- Dimas Trio Fauzan 1042 Ipsas-19-Provisions-cDocument45 pagesDimas Trio Fauzan 1042 Ipsas-19-Provisions-cDimas TrioNo ratings yet

- Mudarabah-A New Guideline of Bank NegaraDocument67 pagesMudarabah-A New Guideline of Bank NegaraolooaNo ratings yet

- G10489 EC Advanced Financial Accounting PrimerDocument64 pagesG10489 EC Advanced Financial Accounting PrimerAlmira ReyesNo ratings yet

- If Rs X Consolidation Staff Draft CombinedDocument80 pagesIf Rs X Consolidation Staff Draft Combinedpjnaidu100% (1)

- FR NotesDocument371 pagesFR Notessharrie0004No ratings yet

- Ey frd02856 161us 05 27 2020 PDFDocument538 pagesEy frd02856 161us 05 27 2020 PDFSarwar GolamNo ratings yet

- Chapter 8 RevenueDocument47 pagesChapter 8 RevenueRanjith CLNo ratings yet

- SSRN Id2394622Document19 pagesSSRN Id2394622Rahul DasNo ratings yet

- SHS - Fundamentals of Accounting 2Document122 pagesSHS - Fundamentals of Accounting 2Carmina CarganillaNo ratings yet

- 5-Borrowing-costs-IPSAS 5 - 091901Document12 pages5-Borrowing-costs-IPSAS 5 - 091901Hastings KapalaNo ratings yet

- Unit 1 - Foundations of Financial and Non-Financial Acct PDFDocument102 pagesUnit 1 - Foundations of Financial and Non-Financial Acct PDFZebib HusseinNo ratings yet

- Classification of Contracts Under International Financial Reporting StandardsDocument21 pagesClassification of Contracts Under International Financial Reporting StandardsWubneh AlemuNo ratings yet

- IPSASB IPSAS 38 Disclosure of Interests in Other EntitiesDocument30 pagesIPSASB IPSAS 38 Disclosure of Interests in Other EntitieskajaleNo ratings yet

- Iaasb Isa 810 RevisedDocument31 pagesIaasb Isa 810 RevisedGlenn TaduranNo ratings yet

- Financial Reporting DevelopmentsDocument139 pagesFinancial Reporting DevelopmentsgligorjanNo ratings yet

- Ifrs 9 Implementation GuidanceDocument48 pagesIfrs 9 Implementation GuidanceMohammad IslamNo ratings yet

- Dwnload Full Intermediate Accounting Volume 1 5th Edition Beechy Solutions Manual PDFDocument35 pagesDwnload Full Intermediate Accounting Volume 1 5th Edition Beechy Solutions Manual PDFvaginulegrandly.51163100% (11)

- Effect Study Ifric12 enDocument40 pagesEffect Study Ifric12 enLevoshkina KseniaNo ratings yet

- HTTPSWWW - Icpau.co - UgsitesdefaultfilesResourcesIFRS201620 20LEASES PDFDocument74 pagesHTTPSWWW - Icpau.co - UgsitesdefaultfilesResourcesIFRS201620 20LEASES PDFazharmansoor2002No ratings yet

- PWC Derivative Hedge AccountingDocument441 pagesPWC Derivative Hedge Accountingmariani100% (2)

- A14 Ipsas - 05Document13 pagesA14 Ipsas - 05Marius SteffyNo ratings yet

- FinancialReportingDevelopments BB1946 SoftwareRevenueRecognition 31may2018 PDFDocument470 pagesFinancialReportingDevelopments BB1946 SoftwareRevenueRecognition 31may2018 PDFNathalie LeeNo ratings yet

- Finance For Decision MakersDocument17 pagesFinance For Decision MakersZamzam AbdelazimNo ratings yet

- Financial Accounting IIDocument33 pagesFinancial Accounting IInerurkar_tusharNo ratings yet

- Ifrs 1Document140 pagesIfrs 1Ditya Parameta100% (1)

- IAS - IFRS - Summary (HH)Document237 pagesIAS - IFRS - Summary (HH)Zakariya Zuberi100% (4)

- Notes To and Forming Part of The Financial Statements: For The Year Ended June 30, 2009Document26 pagesNotes To and Forming Part of The Financial Statements: For The Year Ended June 30, 2009Sohail Humayun KhanNo ratings yet

- Operational Guidelines For FPIs, DDPs and EFIs Revised - PDocument71 pagesOperational Guidelines For FPIs, DDPs and EFIs Revised - PMaharshi BharaliNo ratings yet

- Operational Guidelines For FPIs, DDPs and Eligible Foreign InvestorsDocument60 pagesOperational Guidelines For FPIs, DDPs and Eligible Foreign Investorssaurabh240386No ratings yet

- 07 Revenue 30 Sept 2021 Final For PublishingDocument36 pages07 Revenue 30 Sept 2021 Final For PublishingDineo NongNo ratings yet

- Unit 6: Property, Plant and Equipment: Bachelor of Commerce in AccountingDocument103 pagesUnit 6: Property, Plant and Equipment: Bachelor of Commerce in AccountingAmithNo ratings yet

- IND ASyear-end-consideration-tl - EYDocument56 pagesIND ASyear-end-consideration-tl - EYDilip ChoudharyNo ratings yet

- Ipsas 5 Borrowing Costs 4Document13 pagesIpsas 5 Borrowing Costs 4Lutfia Nur AfifahNo ratings yet

- ED-CON 8-Conceptual Framework For Financial Reporting-Chap 4Document48 pagesED-CON 8-Conceptual Framework For Financial Reporting-Chap 4Jairo Mendez MoraNo ratings yet

- Society of Actuaries: Economic Capital For Life Insurance CompaniesDocument63 pagesSociety of Actuaries: Economic Capital For Life Insurance Companiesjoe malorNo ratings yet

- 11 Capital Assets 30 Sept 21 Final For PublishingDocument80 pages11 Capital Assets 30 Sept 21 Final For PublishingDineo NongNo ratings yet

- Ey Ifrs Us Gaap Rap 2014 EngDocument52 pagesEy Ifrs Us Gaap Rap 2014 EngNasir AliyevNo ratings yet

- 2017 03 IFRS 9 Impairment GuideDocument55 pages2017 03 IFRS 9 Impairment Guideshank nNo ratings yet

- Ap Faisal 001Document19 pagesAp Faisal 001Jashim UddinNo ratings yet

- PWC Guide To Accounting For Derivative Instruments and Hedging ActivitiesDocument594 pagesPWC Guide To Accounting For Derivative Instruments and Hedging Activitieshui7411100% (2)

- Handbook of Asset and Liability Management: From Models to Optimal Return StrategiesFrom EverandHandbook of Asset and Liability Management: From Models to Optimal Return StrategiesNo ratings yet

- Financial Steering: Valuation, KPI Management and the Interaction with IFRSFrom EverandFinancial Steering: Valuation, KPI Management and the Interaction with IFRSNo ratings yet

- Frequently Asked Questions in International Standards on AuditingFrom EverandFrequently Asked Questions in International Standards on AuditingRating: 1 out of 5 stars1/5 (1)

- FAC3764_2024_Study pack 2Document33 pagesFAC3764_2024_Study pack 2Thulani NdlovuNo ratings yet

- Learning Unit 10 - Statement of Cash FlowsDocument31 pagesLearning Unit 10 - Statement of Cash FlowsThulani NdlovuNo ratings yet

- Assessories Business FinalDocument3 pagesAssessories Business FinalThulani NdlovuNo ratings yet

- Cost and Management AccountingDocument38 pagesCost and Management AccountingThulani NdlovuNo ratings yet

- Assessories BusinessDocument5 pagesAssessories BusinessThulani NdlovuNo ratings yet

- A) Calculation of Return On Investment Controllable Profit CalculationDocument12 pagesA) Calculation of Return On Investment Controllable Profit CalculationThulani NdlovuNo ratings yet

- Training: (Texte)Document22 pagesTraining: (Texte)Thulani NdlovuNo ratings yet

- Job Profile - Programme Accountant ZimbabweDocument4 pagesJob Profile - Programme Accountant ZimbabweThulani NdlovuNo ratings yet

- Learning Unit 7 - Leases - IFRS 16Document57 pagesLearning Unit 7 - Leases - IFRS 16Thulani NdlovuNo ratings yet

- Per 01Document1 pagePer 01Thulani NdlovuNo ratings yet

- Training: March 2011Document7 pagesTraining: March 2011Thulani NdlovuNo ratings yet

- Marathons 2018Document1 pageMarathons 2018Thulani NdlovuNo ratings yet

- IN101: Inventory Fundamentals Sage ERP X3Document98 pagesIN101: Inventory Fundamentals Sage ERP X3Thulani NdlovuNo ratings yet

- Training: March 2011Document13 pagesTraining: March 2011Thulani NdlovuNo ratings yet

- Kiong 20407Document5 pagesKiong 20407Thulani NdlovuNo ratings yet

- Training: March 2011Document12 pagesTraining: March 2011Thulani NdlovuNo ratings yet

- Financepart 1Document2 pagesFinancepart 1Thulani NdlovuNo ratings yet

- FIN201 Fundamentals Finance Part 3 BookletDocument10 pagesFIN201 Fundamentals Finance Part 3 BookletThulani NdlovuNo ratings yet

- Purchasing Foundation - BookletDocument60 pagesPurchasing Foundation - BookletThulani NdlovuNo ratings yet

- Training: April 2011Document15 pagesTraining: April 2011Thulani NdlovuNo ratings yet

- Presentation of Financial Statements: IASB Documents Published To Accompany International Accounting Standard 1Document50 pagesPresentation of Financial Statements: IASB Documents Published To Accompany International Accounting Standard 1Thulani NdlovuNo ratings yet

- 28 Fundamental BeliefsDocument29 pages28 Fundamental BeliefsThulani Ndlovu100% (1)

- bv2010 - Ias02 - Part BDocument6 pagesbv2010 - Ias02 - Part BThulani NdlovuNo ratings yet

- Encounter Series Final September 2017Document4 pagesEncounter Series Final September 2017Thulani NdlovuNo ratings yet

- Encounter Series Final June 2017Document3 pagesEncounter Series Final June 2017Thulani Ndlovu100% (1)

- FIN201 Fundamentals Finance Part 4 - ExercisesDocument13 pagesFIN201 Fundamentals Finance Part 4 - ExercisesThulani NdlovuNo ratings yet

- Encounter Series Final July 2017Document4 pagesEncounter Series Final July 2017Thulani NdlovuNo ratings yet

- Department of Accountancy Accounting 3A: Suggested SolutionDocument11 pagesDepartment of Accountancy Accounting 3A: Suggested SolutionThulani NdlovuNo ratings yet

- Financial Statement AnalysisDocument62 pagesFinancial Statement AnalysisCECILLE ALBAO100% (1)

- Financial AssumptionsDocument29 pagesFinancial AssumptionsHưng Đặng QuốcNo ratings yet

- FAR PRB Finals Dec 2017Document25 pagesFAR PRB Finals Dec 2017Dale Ponce100% (2)

- Final Term Papers MGT201 - Solved Master FileDocument129 pagesFinal Term Papers MGT201 - Solved Master Filezahidwahla150% (2)

- Mahesh Project (1) Copy-1Document53 pagesMahesh Project (1) Copy-1MohmmedKhayyumNo ratings yet

- Oil and Gas BudgetDocument32 pagesOil and Gas BudgetHarinesh PandyaNo ratings yet

- Taxation Case DigestDocument23 pagesTaxation Case DigestAnonymous vUC7HI2BNo ratings yet

- Crim2017 CampanillaDocument60 pagesCrim2017 CampanillaKing KingNo ratings yet

- D Taxation Updates For Coops by Dean Estelita C. AguirreDocument69 pagesD Taxation Updates For Coops by Dean Estelita C. AguirreDon CamuaNo ratings yet

- Bansal Roofing ProductsDocument15 pagesBansal Roofing ProductsChirag SharmaNo ratings yet

- Cambridge International AS & A Level: Business 9609/41Document16 pagesCambridge International AS & A Level: Business 9609/41Arnold VasheNo ratings yet

- Answer Key Fa RemDocument4 pagesAnswer Key Fa RemMac b IBANEZNo ratings yet

- Acct201 g1 Banyan Tree ReportDocument18 pagesAcct201 g1 Banyan Tree ReportdfghfiNo ratings yet

- Ch15 UpdatedDocument94 pagesCh15 Updatedkokmunwai717No ratings yet

- Auditing BitsDocument48 pagesAuditing BitskalyanikamineniNo ratings yet

- NCM and Dividend Payments - An Appraisal 060412Document4 pagesNCM and Dividend Payments - An Appraisal 060412ProshareNo ratings yet

- Instruction: 1. Email AddressDocument26 pagesInstruction: 1. Email AddressYeji BabeNo ratings yet

- 2010 - 05 ProspectusDocument293 pages2010 - 05 ProspectusPak DefanceNo ratings yet

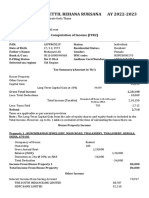

- AY2022-23 KALLA PUTHIYAVEETTIL REHANA RUKSANA-ASFPR0552F-ComputationDocument3 pagesAY2022-23 KALLA PUTHIYAVEETTIL REHANA RUKSANA-ASFPR0552F-ComputationSourabh PunshiNo ratings yet

- Payment of Bonus Act Quick RevisionDocument9 pagesPayment of Bonus Act Quick Revisionshanky631No ratings yet

- UCBL Intern ReportDocument89 pagesUCBL Intern Reportziko777100% (1)

- Getting Started: Principles of FinanceDocument16 pagesGetting Started: Principles of Finance방탄트와이스 짱No ratings yet

- Impact of Corporate Social Responsibility On Profitability of Islamic and Conventional Financial InstitutionsDocument12 pagesImpact of Corporate Social Responsibility On Profitability of Islamic and Conventional Financial Institutionsnauman yunusNo ratings yet

- Marketing of Financial Services V Q IotvvzDocument12 pagesMarketing of Financial Services V Q IotvvzNageshwar SinghNo ratings yet

- Unit 3 Hindi Corporate TaxDocument44 pagesUnit 3 Hindi Corporate Taxsankiworld3No ratings yet

- Financial Management RatiosDocument6 pagesFinancial Management RatiosCharlotte PalmaNo ratings yet

- Mergers, Lbos, Divestitures, and Business FailureDocument69 pagesMergers, Lbos, Divestitures, and Business FailureRendy FranataNo ratings yet

- Audit Fot Liability Problem #2Document3 pagesAudit Fot Liability Problem #2Ma Teresa B. CerezoNo ratings yet

Download as pdf or txt

You might also like

- Full Download Intermediate Accounting Volume 1 5th Edition Beechy Solutions ManualDocument35 pagesFull Download Intermediate Accounting Volume 1 5th Edition Beechy Solutions Manualwilliammwtc100% (35)

- Ifrs and Us Gaap Juin 2023Document236 pagesIfrs and Us Gaap Juin 2023fluffy fluffNo ratings yet

- Training: January 2012Document54 pagesTraining: January 2012Thulani NdlovuNo ratings yet

- Encounter Series FinalDocument9 pagesEncounter Series FinalThulani Ndlovu100% (1)

- ISO 22301: 2019 - An introduction to a business continuity management system (BCMS)From EverandISO 22301: 2019 - An introduction to a business continuity management system (BCMS)Rating: 4 out of 5 stars4/5 (1)

- CHAPTER-9-Principles of AccountingDocument39 pagesCHAPTER-9-Principles of AccountingNguyễn Ngọc AnhNo ratings yet

- P2 Basic PDFDocument289 pagesP2 Basic PDFPhil Sirius100% (1)

- The Theory and Practice of Investment ManagementDocument17 pagesThe Theory and Practice of Investment ManagementTri RamadhanNo ratings yet

- Ifrs 17 Implementation Guidance RevisedDocument44 pagesIfrs 17 Implementation Guidance RevisedMohammad IslamNo ratings yet

- Financial Accounting IDocument47 pagesFinancial Accounting Inerurkar_tusharNo ratings yet

- Level I Volume 5 2019 IFT NotesDocument258 pagesLevel I Volume 5 2019 IFT NotesNoor QamarNo ratings yet

- ACCT 302 Financial Reporting II Lecture 7Document63 pagesACCT 302 Financial Reporting II Lecture 7Jesse Nelson100% (1)

- Ipsas 5-Borrowing Costs: AcknowledgmentDocument13 pagesIpsas 5-Borrowing Costs: Acknowledgmentriska putri utamiNo ratings yet

- G10489 EC - Advanced Financial Accounting Primer PDFDocument65 pagesG10489 EC - Advanced Financial Accounting Primer PDFCassandra LynnNo ratings yet

- GRANT THORNTON - 2016.09 - Comparison Between U.S. GAAP and IFRSDocument228 pagesGRANT THORNTON - 2016.09 - Comparison Between U.S. GAAP and IFRSricardo.j.cruzNo ratings yet

- A34 Ipsas - 25 - 0Document81 pagesA34 Ipsas - 25 - 0Marius SteffyNo ratings yet

- Handbook Derivatives Hedging AccountingDocument1,228 pagesHandbook Derivatives Hedging AccountingVinayak SatheeshNo ratings yet

- Ey frdbb1793 08 12 2020 v2Document361 pagesEy frdbb1793 08 12 2020 v2Duyên Phạm KỳNo ratings yet

- Ias 32 J Ifrs 9 0 Ifric 7Document134 pagesIas 32 J Ifrs 9 0 Ifric 7ncubetalent1997No ratings yet

- Financial Statement Preparation and AnalysisDocument40 pagesFinancial Statement Preparation and AnalysisMD SAIFUL ISLAMNo ratings yet

- Dimas Trio Fauzan 1042 Ipsas-19-Provisions-cDocument45 pagesDimas Trio Fauzan 1042 Ipsas-19-Provisions-cDimas TrioNo ratings yet

- Mudarabah-A New Guideline of Bank NegaraDocument67 pagesMudarabah-A New Guideline of Bank NegaraolooaNo ratings yet

- G10489 EC Advanced Financial Accounting PrimerDocument64 pagesG10489 EC Advanced Financial Accounting PrimerAlmira ReyesNo ratings yet

- If Rs X Consolidation Staff Draft CombinedDocument80 pagesIf Rs X Consolidation Staff Draft Combinedpjnaidu100% (1)

- FR NotesDocument371 pagesFR Notessharrie0004No ratings yet

- Ey frd02856 161us 05 27 2020 PDFDocument538 pagesEy frd02856 161us 05 27 2020 PDFSarwar GolamNo ratings yet

- Chapter 8 RevenueDocument47 pagesChapter 8 RevenueRanjith CLNo ratings yet

- SSRN Id2394622Document19 pagesSSRN Id2394622Rahul DasNo ratings yet

- SHS - Fundamentals of Accounting 2Document122 pagesSHS - Fundamentals of Accounting 2Carmina CarganillaNo ratings yet

- 5-Borrowing-costs-IPSAS 5 - 091901Document12 pages5-Borrowing-costs-IPSAS 5 - 091901Hastings KapalaNo ratings yet

- Unit 1 - Foundations of Financial and Non-Financial Acct PDFDocument102 pagesUnit 1 - Foundations of Financial and Non-Financial Acct PDFZebib HusseinNo ratings yet

- Classification of Contracts Under International Financial Reporting StandardsDocument21 pagesClassification of Contracts Under International Financial Reporting StandardsWubneh AlemuNo ratings yet

- IPSASB IPSAS 38 Disclosure of Interests in Other EntitiesDocument30 pagesIPSASB IPSAS 38 Disclosure of Interests in Other EntitieskajaleNo ratings yet

- Iaasb Isa 810 RevisedDocument31 pagesIaasb Isa 810 RevisedGlenn TaduranNo ratings yet

- Financial Reporting DevelopmentsDocument139 pagesFinancial Reporting DevelopmentsgligorjanNo ratings yet

- Ifrs 9 Implementation GuidanceDocument48 pagesIfrs 9 Implementation GuidanceMohammad IslamNo ratings yet

- Dwnload Full Intermediate Accounting Volume 1 5th Edition Beechy Solutions Manual PDFDocument35 pagesDwnload Full Intermediate Accounting Volume 1 5th Edition Beechy Solutions Manual PDFvaginulegrandly.51163100% (11)

- Effect Study Ifric12 enDocument40 pagesEffect Study Ifric12 enLevoshkina KseniaNo ratings yet

- HTTPSWWW - Icpau.co - UgsitesdefaultfilesResourcesIFRS201620 20LEASES PDFDocument74 pagesHTTPSWWW - Icpau.co - UgsitesdefaultfilesResourcesIFRS201620 20LEASES PDFazharmansoor2002No ratings yet

- PWC Derivative Hedge AccountingDocument441 pagesPWC Derivative Hedge Accountingmariani100% (2)

- A14 Ipsas - 05Document13 pagesA14 Ipsas - 05Marius SteffyNo ratings yet

- FinancialReportingDevelopments BB1946 SoftwareRevenueRecognition 31may2018 PDFDocument470 pagesFinancialReportingDevelopments BB1946 SoftwareRevenueRecognition 31may2018 PDFNathalie LeeNo ratings yet

- Finance For Decision MakersDocument17 pagesFinance For Decision MakersZamzam AbdelazimNo ratings yet

- Financial Accounting IIDocument33 pagesFinancial Accounting IInerurkar_tusharNo ratings yet

- Ifrs 1Document140 pagesIfrs 1Ditya Parameta100% (1)

- IAS - IFRS - Summary (HH)Document237 pagesIAS - IFRS - Summary (HH)Zakariya Zuberi100% (4)

- Notes To and Forming Part of The Financial Statements: For The Year Ended June 30, 2009Document26 pagesNotes To and Forming Part of The Financial Statements: For The Year Ended June 30, 2009Sohail Humayun KhanNo ratings yet

- Operational Guidelines For FPIs, DDPs and EFIs Revised - PDocument71 pagesOperational Guidelines For FPIs, DDPs and EFIs Revised - PMaharshi BharaliNo ratings yet

- Operational Guidelines For FPIs, DDPs and Eligible Foreign InvestorsDocument60 pagesOperational Guidelines For FPIs, DDPs and Eligible Foreign Investorssaurabh240386No ratings yet

- 07 Revenue 30 Sept 2021 Final For PublishingDocument36 pages07 Revenue 30 Sept 2021 Final For PublishingDineo NongNo ratings yet

- Unit 6: Property, Plant and Equipment: Bachelor of Commerce in AccountingDocument103 pagesUnit 6: Property, Plant and Equipment: Bachelor of Commerce in AccountingAmithNo ratings yet

- IND ASyear-end-consideration-tl - EYDocument56 pagesIND ASyear-end-consideration-tl - EYDilip ChoudharyNo ratings yet

- Ipsas 5 Borrowing Costs 4Document13 pagesIpsas 5 Borrowing Costs 4Lutfia Nur AfifahNo ratings yet

- ED-CON 8-Conceptual Framework For Financial Reporting-Chap 4Document48 pagesED-CON 8-Conceptual Framework For Financial Reporting-Chap 4Jairo Mendez MoraNo ratings yet

- Society of Actuaries: Economic Capital For Life Insurance CompaniesDocument63 pagesSociety of Actuaries: Economic Capital For Life Insurance Companiesjoe malorNo ratings yet

- 11 Capital Assets 30 Sept 21 Final For PublishingDocument80 pages11 Capital Assets 30 Sept 21 Final For PublishingDineo NongNo ratings yet

- Ey Ifrs Us Gaap Rap 2014 EngDocument52 pagesEy Ifrs Us Gaap Rap 2014 EngNasir AliyevNo ratings yet

- 2017 03 IFRS 9 Impairment GuideDocument55 pages2017 03 IFRS 9 Impairment Guideshank nNo ratings yet

- Ap Faisal 001Document19 pagesAp Faisal 001Jashim UddinNo ratings yet

- PWC Guide To Accounting For Derivative Instruments and Hedging ActivitiesDocument594 pagesPWC Guide To Accounting For Derivative Instruments and Hedging Activitieshui7411100% (2)

- Handbook of Asset and Liability Management: From Models to Optimal Return StrategiesFrom EverandHandbook of Asset and Liability Management: From Models to Optimal Return StrategiesNo ratings yet

- Financial Steering: Valuation, KPI Management and the Interaction with IFRSFrom EverandFinancial Steering: Valuation, KPI Management and the Interaction with IFRSNo ratings yet

- Frequently Asked Questions in International Standards on AuditingFrom EverandFrequently Asked Questions in International Standards on AuditingRating: 1 out of 5 stars1/5 (1)

- FAC3764_2024_Study pack 2Document33 pagesFAC3764_2024_Study pack 2Thulani NdlovuNo ratings yet

- Learning Unit 10 - Statement of Cash FlowsDocument31 pagesLearning Unit 10 - Statement of Cash FlowsThulani NdlovuNo ratings yet

- Assessories Business FinalDocument3 pagesAssessories Business FinalThulani NdlovuNo ratings yet

- Cost and Management AccountingDocument38 pagesCost and Management AccountingThulani NdlovuNo ratings yet

- Assessories BusinessDocument5 pagesAssessories BusinessThulani NdlovuNo ratings yet

- A) Calculation of Return On Investment Controllable Profit CalculationDocument12 pagesA) Calculation of Return On Investment Controllable Profit CalculationThulani NdlovuNo ratings yet

- Training: (Texte)Document22 pagesTraining: (Texte)Thulani NdlovuNo ratings yet

- Job Profile - Programme Accountant ZimbabweDocument4 pagesJob Profile - Programme Accountant ZimbabweThulani NdlovuNo ratings yet

- Learning Unit 7 - Leases - IFRS 16Document57 pagesLearning Unit 7 - Leases - IFRS 16Thulani NdlovuNo ratings yet

- Per 01Document1 pagePer 01Thulani NdlovuNo ratings yet

- Training: March 2011Document7 pagesTraining: March 2011Thulani NdlovuNo ratings yet

- Marathons 2018Document1 pageMarathons 2018Thulani NdlovuNo ratings yet

- IN101: Inventory Fundamentals Sage ERP X3Document98 pagesIN101: Inventory Fundamentals Sage ERP X3Thulani NdlovuNo ratings yet

- Training: March 2011Document13 pagesTraining: March 2011Thulani NdlovuNo ratings yet

- Kiong 20407Document5 pagesKiong 20407Thulani NdlovuNo ratings yet

- Training: March 2011Document12 pagesTraining: March 2011Thulani NdlovuNo ratings yet

- Financepart 1Document2 pagesFinancepart 1Thulani NdlovuNo ratings yet

- FIN201 Fundamentals Finance Part 3 BookletDocument10 pagesFIN201 Fundamentals Finance Part 3 BookletThulani NdlovuNo ratings yet

- Purchasing Foundation - BookletDocument60 pagesPurchasing Foundation - BookletThulani NdlovuNo ratings yet

- Training: April 2011Document15 pagesTraining: April 2011Thulani NdlovuNo ratings yet

- Presentation of Financial Statements: IASB Documents Published To Accompany International Accounting Standard 1Document50 pagesPresentation of Financial Statements: IASB Documents Published To Accompany International Accounting Standard 1Thulani NdlovuNo ratings yet

- 28 Fundamental BeliefsDocument29 pages28 Fundamental BeliefsThulani Ndlovu100% (1)

- bv2010 - Ias02 - Part BDocument6 pagesbv2010 - Ias02 - Part BThulani NdlovuNo ratings yet

- Encounter Series Final September 2017Document4 pagesEncounter Series Final September 2017Thulani NdlovuNo ratings yet

- Encounter Series Final June 2017Document3 pagesEncounter Series Final June 2017Thulani Ndlovu100% (1)

- FIN201 Fundamentals Finance Part 4 - ExercisesDocument13 pagesFIN201 Fundamentals Finance Part 4 - ExercisesThulani NdlovuNo ratings yet

- Encounter Series Final July 2017Document4 pagesEncounter Series Final July 2017Thulani NdlovuNo ratings yet

- Department of Accountancy Accounting 3A: Suggested SolutionDocument11 pagesDepartment of Accountancy Accounting 3A: Suggested SolutionThulani NdlovuNo ratings yet

- Financial Statement AnalysisDocument62 pagesFinancial Statement AnalysisCECILLE ALBAO100% (1)

- Financial AssumptionsDocument29 pagesFinancial AssumptionsHưng Đặng QuốcNo ratings yet

- FAR PRB Finals Dec 2017Document25 pagesFAR PRB Finals Dec 2017Dale Ponce100% (2)

- Final Term Papers MGT201 - Solved Master FileDocument129 pagesFinal Term Papers MGT201 - Solved Master Filezahidwahla150% (2)

- Mahesh Project (1) Copy-1Document53 pagesMahesh Project (1) Copy-1MohmmedKhayyumNo ratings yet

- Oil and Gas BudgetDocument32 pagesOil and Gas BudgetHarinesh PandyaNo ratings yet

- Taxation Case DigestDocument23 pagesTaxation Case DigestAnonymous vUC7HI2BNo ratings yet

- Crim2017 CampanillaDocument60 pagesCrim2017 CampanillaKing KingNo ratings yet

- D Taxation Updates For Coops by Dean Estelita C. AguirreDocument69 pagesD Taxation Updates For Coops by Dean Estelita C. AguirreDon CamuaNo ratings yet

- Bansal Roofing ProductsDocument15 pagesBansal Roofing ProductsChirag SharmaNo ratings yet

- Cambridge International AS & A Level: Business 9609/41Document16 pagesCambridge International AS & A Level: Business 9609/41Arnold VasheNo ratings yet

- Answer Key Fa RemDocument4 pagesAnswer Key Fa RemMac b IBANEZNo ratings yet

- Acct201 g1 Banyan Tree ReportDocument18 pagesAcct201 g1 Banyan Tree ReportdfghfiNo ratings yet

- Ch15 UpdatedDocument94 pagesCh15 Updatedkokmunwai717No ratings yet

- Auditing BitsDocument48 pagesAuditing BitskalyanikamineniNo ratings yet

- NCM and Dividend Payments - An Appraisal 060412Document4 pagesNCM and Dividend Payments - An Appraisal 060412ProshareNo ratings yet

- Instruction: 1. Email AddressDocument26 pagesInstruction: 1. Email AddressYeji BabeNo ratings yet

- 2010 - 05 ProspectusDocument293 pages2010 - 05 ProspectusPak DefanceNo ratings yet

- AY2022-23 KALLA PUTHIYAVEETTIL REHANA RUKSANA-ASFPR0552F-ComputationDocument3 pagesAY2022-23 KALLA PUTHIYAVEETTIL REHANA RUKSANA-ASFPR0552F-ComputationSourabh PunshiNo ratings yet

- Payment of Bonus Act Quick RevisionDocument9 pagesPayment of Bonus Act Quick Revisionshanky631No ratings yet

- UCBL Intern ReportDocument89 pagesUCBL Intern Reportziko777100% (1)

- Getting Started: Principles of FinanceDocument16 pagesGetting Started: Principles of Finance방탄트와이스 짱No ratings yet

- Impact of Corporate Social Responsibility On Profitability of Islamic and Conventional Financial InstitutionsDocument12 pagesImpact of Corporate Social Responsibility On Profitability of Islamic and Conventional Financial Institutionsnauman yunusNo ratings yet

- Marketing of Financial Services V Q IotvvzDocument12 pagesMarketing of Financial Services V Q IotvvzNageshwar SinghNo ratings yet

- Unit 3 Hindi Corporate TaxDocument44 pagesUnit 3 Hindi Corporate Taxsankiworld3No ratings yet

- Financial Management RatiosDocument6 pagesFinancial Management RatiosCharlotte PalmaNo ratings yet

- Mergers, Lbos, Divestitures, and Business FailureDocument69 pagesMergers, Lbos, Divestitures, and Business FailureRendy FranataNo ratings yet

- Audit Fot Liability Problem #2Document3 pagesAudit Fot Liability Problem #2Ma Teresa B. CerezoNo ratings yet