Unit-6 Investment Accounting

Unit-6 Investment Accounting

You might also like

- Project Selection, Approval and Activation E. AgtarapDocument29 pagesProject Selection, Approval and Activation E. AgtarapEvangeline Chua Agtarap67% (3)

- Intermediate Accounting 2: a QuickStudy Digital Reference GuideFrom EverandIntermediate Accounting 2: a QuickStudy Digital Reference GuideNo ratings yet

- As 13 - Investment AccountsDocument6 pagesAs 13 - Investment AccountsJiya Mary JamesNo ratings yet

- Investment AccountsDocument10 pagesInvestment AccountsMani kandan.GNo ratings yet

- Accounting For InvestmentsDocument17 pagesAccounting For InvestmentsPradeep Gupta100% (1)

- MATERIALDocument8 pagesMATERIALVatsal ParmarNo ratings yet

- Investment AccountsDocument7 pagesInvestment AccountsRiju Varkey ThomasNo ratings yet

- Investment New ScopeDocument19 pagesInvestment New ScopeayinaNo ratings yet

- 7 As 13 Accounting For InvestmentsDocument32 pages7 As 13 Accounting For Investmentscloudstorage567No ratings yet

- E-Books - AS 13 Accounting For InvestmentsDocument32 pagesE-Books - AS 13 Accounting For InvestmentssmartshivenduNo ratings yet

- As 13Document12 pagesAs 13Noorul Zaman KhanNo ratings yet

- Investment Accounts: After Studying This Chapter, You Will Be Able ToDocument47 pagesInvestment Accounts: After Studying This Chapter, You Will Be Able ToRavi SharmaNo ratings yet

- Accounting - Investment AccountDocument11 pagesAccounting - Investment AccountDevansh ChhedaNo ratings yet

- Financial Accounting - Investment AccountDocument5 pagesFinancial Accounting - Investment AccountsmlingwaNo ratings yet

- 10 AS13 Invesment AccountingDocument8 pages10 AS13 Invesment Accountingprashantmis452No ratings yet

- AS 13 Accounting For Investments 1Document2 pagesAS 13 Accounting For Investments 1thre333eNo ratings yet

- B. Com 5 Sem Advance Financial Accounting 1Document9 pagesB. Com 5 Sem Advance Financial Accounting 1AlankritaNo ratings yet

- Financial Assets at Amortized CostDocument8 pagesFinancial Assets at Amortized CostbluemajaNo ratings yet

- Fa - Investment in Equity Securities - Lecture NotesDocument4 pagesFa - Investment in Equity Securities - Lecture NotesCharlene Jane EspinoNo ratings yet

- InvestmentsDocument2 pagesInvestmentsAlora EuNo ratings yet

- AS-13Document15 pagesAS-13dilipupadhyay1979No ratings yet

- As 13Document11 pagesAs 13Avinash YadavNo ratings yet

- Chapter 9Document18 pagesChapter 9Rubén ZúñigaNo ratings yet

- Investments and AcquisitionsDocument5 pagesInvestments and AcquisitionsBurhan Al MessiNo ratings yet

- Quiz On Debt InvestmentDocument2 pagesQuiz On Debt InvestmentYa NaNo ratings yet

- Investment Accounting W.R.T. As-13Document4 pagesInvestment Accounting W.R.T. As-13navin_khubchandaniNo ratings yet

- FAR 4307 Investment in Equity SecuritiesDocument3 pagesFAR 4307 Investment in Equity SecuritiesATHALIAH LUNA MERCADEJASNo ratings yet

- Mutual Funds and Venture Capital Funds And/or The Related Asset Management Companies, Banks and Public Financial InstitutionsDocument14 pagesMutual Funds and Venture Capital Funds And/or The Related Asset Management Companies, Banks and Public Financial InstitutionsrazorNo ratings yet

- Week 05 - 02 - Module 11 - Investment in Equity InstrumentsDocument10 pagesWeek 05 - 02 - Module 11 - Investment in Equity Instruments지마리No ratings yet

- Accounting Standard (As) 13Document17 pagesAccounting Standard (As) 13shital_vyas1987No ratings yet

- Exam NotesDocument9 pagesExam NotesEven JayNo ratings yet

- Chapter 16 Equity InvestmentsDocument19 pagesChapter 16 Equity InvestmentsBukhani MacabanganNo ratings yet

- Accounting For InvestmentsDocument6 pagesAccounting For InvestmentsBeldineNo ratings yet

- Mutual FundDocument10 pagesMutual FundmadhuNo ratings yet

- Ilovepdf MergedDocument17 pagesIlovepdf Mergednsm2zmvnbbNo ratings yet

- Meaning of Investment: MonetaryDocument4 pagesMeaning of Investment: MonetaryshrikantNo ratings yet

- 69241asb55316 As13Document10 pages69241asb55316 As13cheyam222No ratings yet

- Marketable SecuritiesDocument5 pagesMarketable SecuritiesZAKAYO NJONYNo ratings yet

- Accounting For InvestmentsDocument7 pagesAccounting For InvestmentsPaolo Immanuel OlanoNo ratings yet

- As 13Document6 pagesAs 13abhishekkapse654No ratings yet

- Financial Accounting: by Prof. Anirban DuttaDocument18 pagesFinancial Accounting: by Prof. Anirban DuttaDixith GandheNo ratings yet

- What Are The Characteristics of A Bond Investment? AnswerDocument4 pagesWhat Are The Characteristics of A Bond Investment? AnswerAllysa Jane FajilagmagoNo ratings yet

- Chapter ThreeeDocument25 pagesChapter ThreeeTesfaye Megiso BegajoNo ratings yet

- Notes To Accounts CompanyDocument9 pagesNotes To Accounts CompanyMy NameNo ratings yet

- Accounting For InvestmentsDocument11 pagesAccounting For Investmentsstarfish85No ratings yet

- Audit of Investment-LectureDocument15 pagesAudit of Investment-LecturemoNo ratings yet

- Aa TaxDocument22 pagesAa Taxnirshan rajNo ratings yet

- IA Chap. 19, 20, and 22Document31 pagesIA Chap. 19, 20, and 22Pitel O'shoppeNo ratings yet

- Accounting Policies ModelDocument7 pagesAccounting Policies ModelShalini GuptaNo ratings yet

- Bonds and Long Term LiabilitiesDocument5 pagesBonds and Long Term LiabilitiesDivine CuasayNo ratings yet

- Reviewer in Intermediate Accounting (Midterm)Document9 pagesReviewer in Intermediate Accounting (Midterm)Czarhiena SantiagoNo ratings yet

- Financial Accounitng ASSIGNMENTDocument8 pagesFinancial Accounitng ASSIGNMENTsejal bohraNo ratings yet

- Accounting For InvestmentDocument14 pagesAccounting For Investmentefe davidNo ratings yet

- Bond InvestmentDocument2 pagesBond InvestmentPat RFNo ratings yet

- Financial Accounting and Reporting - InvestmentsDocument10 pagesFinancial Accounting and Reporting - InvestmentsLuisitoNo ratings yet

- Solution Manual For Advanced Accounting 13Th Edition Beams Anthony Bettinghaus Smith 0134472144 9780134472140 Full Chapter PDFDocument30 pagesSolution Manual For Advanced Accounting 13Th Edition Beams Anthony Bettinghaus Smith 0134472144 9780134472140 Full Chapter PDFrose.carvin242100% (19)

- AS13Document7 pagesAS13Selvi balanNo ratings yet

- 161 14 PFRS 9 Financial Instrument Investment in Financial AssetDocument5 pages161 14 PFRS 9 Financial Instrument Investment in Financial AssetRegina Gregoria SalasNo ratings yet

- Accounting For Investment SecuritiesDocument9 pagesAccounting For Investment Securitiesxpac_53No ratings yet

- Investment Is Putting Money Into Something With The Hope of Profit. More Specifically, Investment Is TheDocument19 pagesInvestment Is Putting Money Into Something With The Hope of Profit. More Specifically, Investment Is TheMadhu MathiNo ratings yet

- Cost of Capital - To SendDocument44 pagesCost of Capital - To SendTejaswini VashisthaNo ratings yet

- China Accounting StandardsDocument3 pagesChina Accounting StandardsAaron Joy Dominguez PutianNo ratings yet

- Mas PMSDocument12 pagesMas PMSprashant pohekarNo ratings yet

- 3.owner's Equity 4.income 5.expense: Five Major AccountsDocument18 pages3.owner's Equity 4.income 5.expense: Five Major AccountsMarlyn LotivioNo ratings yet

- HW On Sinking Fund CDocument2 pagesHW On Sinking Fund CCha PampolinaNo ratings yet

- Vikas Provisional ComputationDocument6 pagesVikas Provisional ComputationAmit TyagiNo ratings yet

- A. Vocabulary: Financial Terms: Unit 6: Money (Hp3)Document4 pagesA. Vocabulary: Financial Terms: Unit 6: Money (Hp3)Phu TaNo ratings yet

- IAS 21 - Effects of Changes in Foreign Exchange PDFDocument22 pagesIAS 21 - Effects of Changes in Foreign Exchange PDFJanelle SentinaNo ratings yet

- Quant Mutual FundDocument4 pagesQuant Mutual FundSunil RawtaniNo ratings yet

- Fundamentals of Cost Accounting 5Th Edition Lanen Test Bank Full Chapter PDFDocument60 pagesFundamentals of Cost Accounting 5Th Edition Lanen Test Bank Full Chapter PDFmarrowscandentyzch4c100% (12)

- 3 E-Mai L: Chaotak@ Embarqmai L. Com - . - . % Telephone: (702) 647-7925 - . (4Document111 pages3 E-Mai L: Chaotak@ Embarqmai L. Com - . - . % Telephone: (702) 647-7925 - . (4glimmertwinsNo ratings yet

- Financial Statement Analysis: Learning OutcomesDocument6 pagesFinancial Statement Analysis: Learning Outcomestushar gargNo ratings yet

- MQ3 Spr08gDocument10 pagesMQ3 Spr08gjhouvanNo ratings yet

- Audit of LedgersDocument28 pagesAudit of LedgersShahbaz NoorNo ratings yet

- FM - UAS - OM08f - Nama Masing2Document2 pagesFM - UAS - OM08f - Nama Masing2Winda WidayantiNo ratings yet

- Draft 1 PDFDocument36 pagesDraft 1 PDFYunitasia NurliaNo ratings yet

- Group Presentation FOI 2020-21Document6 pagesGroup Presentation FOI 2020-21Amazon WorldNo ratings yet

- CorporationDocument14 pagesCorporationWonde BiruNo ratings yet

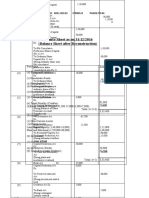

- Balance Sheet As On 31/12/2016 (Balance Sheet After Reconstruction)Document8 pagesBalance Sheet As On 31/12/2016 (Balance Sheet After Reconstruction)GauravNo ratings yet

- Portfolio Assignment-02-BUS-5110 Manegerial AccountingDocument5 pagesPortfolio Assignment-02-BUS-5110 Manegerial AccountingRasel SakilNo ratings yet

- Partnership Formation OperationsDocument8 pagesPartnership Formation OperationsSherwin Benedict Sebastian100% (1)

- The Role of Financial Management in Promoting Sustainable Business Practices and DevelopmentDocument22 pagesThe Role of Financial Management in Promoting Sustainable Business Practices and DevelopmentJosh GonzalesNo ratings yet

- FD PresentationDocument22 pagesFD PresentationAnzir FerdousNo ratings yet

- A Comparative Study On Tata Consultancy Services LTD and Infosys LTD in The Information Technology IndustryDocument7 pagesA Comparative Study On Tata Consultancy Services LTD and Infosys LTD in The Information Technology IndustryDebasmita Pr RayNo ratings yet

- Chapter 6 Testbank Topic Grid: Garrison/Noreen/Brewer, Managerial Accounting, Twelfth Edition 6-1Document6 pagesChapter 6 Testbank Topic Grid: Garrison/Noreen/Brewer, Managerial Accounting, Twelfth Edition 6-1Ivern BautistaNo ratings yet

- L4M4 Mock (7) Ethical and Responsible SourcingDocument40 pagesL4M4 Mock (7) Ethical and Responsible Sourcingrajeev ananth100% (1)

- 04-Config Check-DevDocument35 pages04-Config Check-DevsumankumarperamNo ratings yet

- VALCOM. Module 2Document3 pagesVALCOM. Module 2Christopher ApaniNo ratings yet

- QTTC KeyDocument20 pagesQTTC KeyThảo Uyên TrầnNo ratings yet

Download as pdf or txt

You might also like

- Project Selection, Approval and Activation E. AgtarapDocument29 pagesProject Selection, Approval and Activation E. AgtarapEvangeline Chua Agtarap67% (3)

- Intermediate Accounting 2: a QuickStudy Digital Reference GuideFrom EverandIntermediate Accounting 2: a QuickStudy Digital Reference GuideNo ratings yet

- As 13 - Investment AccountsDocument6 pagesAs 13 - Investment AccountsJiya Mary JamesNo ratings yet

- Investment AccountsDocument10 pagesInvestment AccountsMani kandan.GNo ratings yet

- Accounting For InvestmentsDocument17 pagesAccounting For InvestmentsPradeep Gupta100% (1)

- MATERIALDocument8 pagesMATERIALVatsal ParmarNo ratings yet

- Investment AccountsDocument7 pagesInvestment AccountsRiju Varkey ThomasNo ratings yet

- Investment New ScopeDocument19 pagesInvestment New ScopeayinaNo ratings yet

- 7 As 13 Accounting For InvestmentsDocument32 pages7 As 13 Accounting For Investmentscloudstorage567No ratings yet

- E-Books - AS 13 Accounting For InvestmentsDocument32 pagesE-Books - AS 13 Accounting For InvestmentssmartshivenduNo ratings yet

- As 13Document12 pagesAs 13Noorul Zaman KhanNo ratings yet

- Investment Accounts: After Studying This Chapter, You Will Be Able ToDocument47 pagesInvestment Accounts: After Studying This Chapter, You Will Be Able ToRavi SharmaNo ratings yet

- Accounting - Investment AccountDocument11 pagesAccounting - Investment AccountDevansh ChhedaNo ratings yet

- Financial Accounting - Investment AccountDocument5 pagesFinancial Accounting - Investment AccountsmlingwaNo ratings yet

- 10 AS13 Invesment AccountingDocument8 pages10 AS13 Invesment Accountingprashantmis452No ratings yet

- AS 13 Accounting For Investments 1Document2 pagesAS 13 Accounting For Investments 1thre333eNo ratings yet

- B. Com 5 Sem Advance Financial Accounting 1Document9 pagesB. Com 5 Sem Advance Financial Accounting 1AlankritaNo ratings yet

- Financial Assets at Amortized CostDocument8 pagesFinancial Assets at Amortized CostbluemajaNo ratings yet

- Fa - Investment in Equity Securities - Lecture NotesDocument4 pagesFa - Investment in Equity Securities - Lecture NotesCharlene Jane EspinoNo ratings yet

- InvestmentsDocument2 pagesInvestmentsAlora EuNo ratings yet

- AS-13Document15 pagesAS-13dilipupadhyay1979No ratings yet

- As 13Document11 pagesAs 13Avinash YadavNo ratings yet

- Chapter 9Document18 pagesChapter 9Rubén ZúñigaNo ratings yet

- Investments and AcquisitionsDocument5 pagesInvestments and AcquisitionsBurhan Al MessiNo ratings yet

- Quiz On Debt InvestmentDocument2 pagesQuiz On Debt InvestmentYa NaNo ratings yet

- Investment Accounting W.R.T. As-13Document4 pagesInvestment Accounting W.R.T. As-13navin_khubchandaniNo ratings yet

- FAR 4307 Investment in Equity SecuritiesDocument3 pagesFAR 4307 Investment in Equity SecuritiesATHALIAH LUNA MERCADEJASNo ratings yet

- Mutual Funds and Venture Capital Funds And/or The Related Asset Management Companies, Banks and Public Financial InstitutionsDocument14 pagesMutual Funds and Venture Capital Funds And/or The Related Asset Management Companies, Banks and Public Financial InstitutionsrazorNo ratings yet

- Week 05 - 02 - Module 11 - Investment in Equity InstrumentsDocument10 pagesWeek 05 - 02 - Module 11 - Investment in Equity Instruments지마리No ratings yet

- Accounting Standard (As) 13Document17 pagesAccounting Standard (As) 13shital_vyas1987No ratings yet

- Exam NotesDocument9 pagesExam NotesEven JayNo ratings yet

- Chapter 16 Equity InvestmentsDocument19 pagesChapter 16 Equity InvestmentsBukhani MacabanganNo ratings yet

- Accounting For InvestmentsDocument6 pagesAccounting For InvestmentsBeldineNo ratings yet

- Mutual FundDocument10 pagesMutual FundmadhuNo ratings yet

- Ilovepdf MergedDocument17 pagesIlovepdf Mergednsm2zmvnbbNo ratings yet

- Meaning of Investment: MonetaryDocument4 pagesMeaning of Investment: MonetaryshrikantNo ratings yet

- 69241asb55316 As13Document10 pages69241asb55316 As13cheyam222No ratings yet

- Marketable SecuritiesDocument5 pagesMarketable SecuritiesZAKAYO NJONYNo ratings yet

- Accounting For InvestmentsDocument7 pagesAccounting For InvestmentsPaolo Immanuel OlanoNo ratings yet

- As 13Document6 pagesAs 13abhishekkapse654No ratings yet

- Financial Accounting: by Prof. Anirban DuttaDocument18 pagesFinancial Accounting: by Prof. Anirban DuttaDixith GandheNo ratings yet

- What Are The Characteristics of A Bond Investment? AnswerDocument4 pagesWhat Are The Characteristics of A Bond Investment? AnswerAllysa Jane FajilagmagoNo ratings yet

- Chapter ThreeeDocument25 pagesChapter ThreeeTesfaye Megiso BegajoNo ratings yet

- Notes To Accounts CompanyDocument9 pagesNotes To Accounts CompanyMy NameNo ratings yet

- Accounting For InvestmentsDocument11 pagesAccounting For Investmentsstarfish85No ratings yet

- Audit of Investment-LectureDocument15 pagesAudit of Investment-LecturemoNo ratings yet

- Aa TaxDocument22 pagesAa Taxnirshan rajNo ratings yet

- IA Chap. 19, 20, and 22Document31 pagesIA Chap. 19, 20, and 22Pitel O'shoppeNo ratings yet

- Accounting Policies ModelDocument7 pagesAccounting Policies ModelShalini GuptaNo ratings yet

- Bonds and Long Term LiabilitiesDocument5 pagesBonds and Long Term LiabilitiesDivine CuasayNo ratings yet

- Reviewer in Intermediate Accounting (Midterm)Document9 pagesReviewer in Intermediate Accounting (Midterm)Czarhiena SantiagoNo ratings yet

- Financial Accounitng ASSIGNMENTDocument8 pagesFinancial Accounitng ASSIGNMENTsejal bohraNo ratings yet

- Accounting For InvestmentDocument14 pagesAccounting For Investmentefe davidNo ratings yet

- Bond InvestmentDocument2 pagesBond InvestmentPat RFNo ratings yet

- Financial Accounting and Reporting - InvestmentsDocument10 pagesFinancial Accounting and Reporting - InvestmentsLuisitoNo ratings yet

- Solution Manual For Advanced Accounting 13Th Edition Beams Anthony Bettinghaus Smith 0134472144 9780134472140 Full Chapter PDFDocument30 pagesSolution Manual For Advanced Accounting 13Th Edition Beams Anthony Bettinghaus Smith 0134472144 9780134472140 Full Chapter PDFrose.carvin242100% (19)

- AS13Document7 pagesAS13Selvi balanNo ratings yet

- 161 14 PFRS 9 Financial Instrument Investment in Financial AssetDocument5 pages161 14 PFRS 9 Financial Instrument Investment in Financial AssetRegina Gregoria SalasNo ratings yet

- Accounting For Investment SecuritiesDocument9 pagesAccounting For Investment Securitiesxpac_53No ratings yet

- Investment Is Putting Money Into Something With The Hope of Profit. More Specifically, Investment Is TheDocument19 pagesInvestment Is Putting Money Into Something With The Hope of Profit. More Specifically, Investment Is TheMadhu MathiNo ratings yet

- Cost of Capital - To SendDocument44 pagesCost of Capital - To SendTejaswini VashisthaNo ratings yet

- China Accounting StandardsDocument3 pagesChina Accounting StandardsAaron Joy Dominguez PutianNo ratings yet

- Mas PMSDocument12 pagesMas PMSprashant pohekarNo ratings yet

- 3.owner's Equity 4.income 5.expense: Five Major AccountsDocument18 pages3.owner's Equity 4.income 5.expense: Five Major AccountsMarlyn LotivioNo ratings yet

- HW On Sinking Fund CDocument2 pagesHW On Sinking Fund CCha PampolinaNo ratings yet

- Vikas Provisional ComputationDocument6 pagesVikas Provisional ComputationAmit TyagiNo ratings yet

- A. Vocabulary: Financial Terms: Unit 6: Money (Hp3)Document4 pagesA. Vocabulary: Financial Terms: Unit 6: Money (Hp3)Phu TaNo ratings yet

- IAS 21 - Effects of Changes in Foreign Exchange PDFDocument22 pagesIAS 21 - Effects of Changes in Foreign Exchange PDFJanelle SentinaNo ratings yet

- Quant Mutual FundDocument4 pagesQuant Mutual FundSunil RawtaniNo ratings yet

- Fundamentals of Cost Accounting 5Th Edition Lanen Test Bank Full Chapter PDFDocument60 pagesFundamentals of Cost Accounting 5Th Edition Lanen Test Bank Full Chapter PDFmarrowscandentyzch4c100% (12)

- 3 E-Mai L: Chaotak@ Embarqmai L. Com - . - . % Telephone: (702) 647-7925 - . (4Document111 pages3 E-Mai L: Chaotak@ Embarqmai L. Com - . - . % Telephone: (702) 647-7925 - . (4glimmertwinsNo ratings yet

- Financial Statement Analysis: Learning OutcomesDocument6 pagesFinancial Statement Analysis: Learning Outcomestushar gargNo ratings yet

- MQ3 Spr08gDocument10 pagesMQ3 Spr08gjhouvanNo ratings yet

- Audit of LedgersDocument28 pagesAudit of LedgersShahbaz NoorNo ratings yet

- FM - UAS - OM08f - Nama Masing2Document2 pagesFM - UAS - OM08f - Nama Masing2Winda WidayantiNo ratings yet

- Draft 1 PDFDocument36 pagesDraft 1 PDFYunitasia NurliaNo ratings yet

- Group Presentation FOI 2020-21Document6 pagesGroup Presentation FOI 2020-21Amazon WorldNo ratings yet

- CorporationDocument14 pagesCorporationWonde BiruNo ratings yet

- Balance Sheet As On 31/12/2016 (Balance Sheet After Reconstruction)Document8 pagesBalance Sheet As On 31/12/2016 (Balance Sheet After Reconstruction)GauravNo ratings yet

- Portfolio Assignment-02-BUS-5110 Manegerial AccountingDocument5 pagesPortfolio Assignment-02-BUS-5110 Manegerial AccountingRasel SakilNo ratings yet

- Partnership Formation OperationsDocument8 pagesPartnership Formation OperationsSherwin Benedict Sebastian100% (1)

- The Role of Financial Management in Promoting Sustainable Business Practices and DevelopmentDocument22 pagesThe Role of Financial Management in Promoting Sustainable Business Practices and DevelopmentJosh GonzalesNo ratings yet

- FD PresentationDocument22 pagesFD PresentationAnzir FerdousNo ratings yet

- A Comparative Study On Tata Consultancy Services LTD and Infosys LTD in The Information Technology IndustryDocument7 pagesA Comparative Study On Tata Consultancy Services LTD and Infosys LTD in The Information Technology IndustryDebasmita Pr RayNo ratings yet

- Chapter 6 Testbank Topic Grid: Garrison/Noreen/Brewer, Managerial Accounting, Twelfth Edition 6-1Document6 pagesChapter 6 Testbank Topic Grid: Garrison/Noreen/Brewer, Managerial Accounting, Twelfth Edition 6-1Ivern BautistaNo ratings yet

- L4M4 Mock (7) Ethical and Responsible SourcingDocument40 pagesL4M4 Mock (7) Ethical and Responsible Sourcingrajeev ananth100% (1)

- 04-Config Check-DevDocument35 pages04-Config Check-DevsumankumarperamNo ratings yet

- VALCOM. Module 2Document3 pagesVALCOM. Module 2Christopher ApaniNo ratings yet

- QTTC KeyDocument20 pagesQTTC KeyThảo Uyên TrầnNo ratings yet