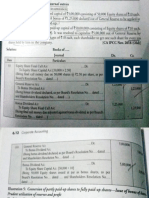

Internal Reconstruction Notes - Corporate Resructuring

Internal Reconstruction Notes - Corporate Resructuring

You might also like

- Full Solution Manual Applying International Financial Reporting Standards 3nd Edition by Ruth Picker SLW1019Document42 pagesFull Solution Manual Applying International Financial Reporting Standards 3nd Edition by Ruth Picker SLW1019Sm Help80% (5)

- Intermediate Accounting 2: a QuickStudy Digital Reference GuideFrom EverandIntermediate Accounting 2: a QuickStudy Digital Reference GuideNo ratings yet

- AE 112 Finals Summative AssessmentDocument12 pagesAE 112 Finals Summative AssessmentmercyvienhoNo ratings yet

- Submitted By: Cabling, Alvin Hachiles, Jomari Honera, Shawn Michael Miranda, Christopher Odonzo, Aldwin Salvador, ChristianDocument32 pagesSubmitted By: Cabling, Alvin Hachiles, Jomari Honera, Shawn Michael Miranda, Christopher Odonzo, Aldwin Salvador, ChristianKimberly Claire AtienzaNo ratings yet

- Internal ReconstructionDocument25 pagesInternal ReconstructionbhanubainsNo ratings yet

- Bandhan BankDocument37 pagesBandhan BankBandaru NarendrababuNo ratings yet

- 46480bosinter p5 cp7 PDFDocument50 pages46480bosinter p5 cp7 PDFMukesh jivrajikaNo ratings yet

- Internal ReconstructionDocument60 pagesInternal ReconstructionMighty RajuNo ratings yet

- CHP 6 Internal ReconstructionDocument60 pagesCHP 6 Internal ReconstructionRonak ChhabriaNo ratings yet

- ReconstructionDocument26 pagesReconstructionNikhilNo ratings yet

- AmalgamationDocument70 pagesAmalgamationjshashimohanNo ratings yet

- Capital Reorganisation Year 2Document60 pagesCapital Reorganisation Year 2janeth pallangyoNo ratings yet

- Wa0005.Document36 pagesWa0005.mitanshigoyal7No ratings yet

- What Is Reconstruction?: Need For Internal ReconstructionDocument31 pagesWhat Is Reconstruction?: Need For Internal Reconstructionneeru79200079% (14)

- Internal Reconstruction Part-IDocument19 pagesInternal Reconstruction Part-ISahil GuptaNo ratings yet

- Reconstruction InternalDocument12 pagesReconstruction InternalsviimaNo ratings yet

- Module 6Document50 pagesModule 6rohit saini75% (4)

- DR - Srinivas Madishetti Professor, School of Business Mzumbe UniversityDocument67 pagesDR - Srinivas Madishetti Professor, School of Business Mzumbe UniversityNicole TaylorNo ratings yet

- March 2023 Answer Key CorporateaccountingDocument11 pagesMarch 2023 Answer Key Corporateaccountinghisarahhh4No ratings yet

- 5 6084915055709651012Document8 pages5 6084915055709651012Ajit Yadav100% (1)

- Business CombinationsDocument18 pagesBusiness Combinationszubair afzalNo ratings yet

- Alteration & Reduction of Share CapitalDocument5 pagesAlteration & Reduction of Share CapitalHasnain MahmoodNo ratings yet

- Share Holders Equity: BOOKS and Records of A CorporationDocument5 pagesShare Holders Equity: BOOKS and Records of A CorporationQueen ValleNo ratings yet

- Financial AccountingDocument11 pagesFinancial AccountingRakesh ChauhanNo ratings yet

- Internal Reconstruction - Theory NotesDocument3 pagesInternal Reconstruction - Theory NotesNaomi SaldanhaNo ratings yet

- Module 2 Shareholders Equity Students ReferenceDocument7 pagesModule 2 Shareholders Equity Students ReferencecynangelaNo ratings yet

- Retained Earnings: Appropriation and Quasi-ReorganizationDocument25 pagesRetained Earnings: Appropriation and Quasi-ReorganizationtruthNo ratings yet

- Session 3c Share Capital & Reserves: HI5020 Corporate AccountingDocument29 pagesSession 3c Share Capital & Reserves: HI5020 Corporate AccountingFeku RamNo ratings yet

- Reconstruction of A CompanyDocument9 pagesReconstruction of A Companywolverinelogan806No ratings yet

- A 11 Internal Reconstruction of A CompanyDocument18 pagesA 11 Internal Reconstruction of A CompanyDhananjay Pawar50% (2)

- Internal ReconstructionDocument8 pagesInternal Reconstructionsmit9993No ratings yet

- 23 Share Capital s22 - FinalDocument23 pages23 Share Capital s22 - FinalAphelele GqadaNo ratings yet

- Introduction To Internal Reconstruction of CompaniesDocument17 pagesIntroduction To Internal Reconstruction of CompaniesMichael NyaongoNo ratings yet

- 1 Chapter 5 Internal Reconstruction PDFDocument22 pages1 Chapter 5 Internal Reconstruction PDFAbhiramNo ratings yet

- The Statement of Changes in EquityDocument9 pagesThe Statement of Changes in EquityDanerish PabunanNo ratings yet

- PM Ipcc Acc Vol2 Chapter5Document26 pagesPM Ipcc Acc Vol2 Chapter5ShambuReddyNo ratings yet

- IFRS Chap 2Document42 pagesIFRS Chap 2Yousef Abdullah GhundulNo ratings yet

- 12 Accountancy Notes CH07 Company Accounts Issue of Shares 01Document20 pages12 Accountancy Notes CH07 Company Accounts Issue of Shares 01zainab.xf77No ratings yet

- 2017 Class 16 EquityDocument35 pages2017 Class 16 EquityChandra Sekhar ChittineniNo ratings yet

- Chapter 10 Equity Part 2Document27 pagesChapter 10 Equity Part 2LEE WEI LONGNo ratings yet

- Lecture 4-PostDocument40 pagesLecture 4-PostcoolirlbbNo ratings yet

- Statement of Changes in Equity and The Balance SheetDocument82 pagesStatement of Changes in Equity and The Balance SheetnicoNo ratings yet

- Week 7 NotesDocument6 pagesWeek 7 NotescalebNo ratings yet

- UNIT 2 & 4 MergedDocument41 pagesUNIT 2 & 4 MergedRich ManNo ratings yet

- Internal Reconstruction of CompaniesDocument4 pagesInternal Reconstruction of CompaniesZiya ShaikhNo ratings yet

- Advanced Financial Accounting IDocument7 pagesAdvanced Financial Accounting IRoNo ratings yet

- 54232bos43539cp4 U4Document53 pages54232bos43539cp4 U4Akash KamathNo ratings yet

- Take Print - Adv AccDocument11 pagesTake Print - Adv AccManikandanNo ratings yet

- CA Inter Accounts A MTP 1 Nov 2022Document13 pagesCA Inter Accounts A MTP 1 Nov 2022smartshivenduNo ratings yet

- Retained Earnings - Appropriation and Quasi-Reorganization - 0Document29 pagesRetained Earnings - Appropriation and Quasi-Reorganization - 0lilienesieraNo ratings yet

- Beams9esm Ch01Document13 pagesBeams9esm Ch01zandra SumbarNo ratings yet

- Chapter 10 - Accounting For Equity: Learning ObjectivesDocument11 pagesChapter 10 - Accounting For Equity: Learning ObjectivesBình Trần ThanhNo ratings yet

- Bv2018 Revised Conceptual FrameworkDocument18 pagesBv2018 Revised Conceptual FrameworkTeneswari RadhaNo ratings yet

- Unit - 4: Amalgamation and ReconstructionDocument54 pagesUnit - 4: Amalgamation and ReconstructionAzad AboobackerNo ratings yet

- HA2032Document12 pagesHA2032Aayam SubediNo ratings yet

- CHAPTER 14 Non. 14Document6 pagesCHAPTER 14 Non. 14Ahmed AymanNo ratings yet

- Buy Back of SharesDocument17 pagesBuy Back of Shareskunaldudu345No ratings yet

- CBCS - BCOM - HONS - Sem-5 - COMMERCE - DSE 5.2 A - CORPORATE ACCOUNTING-10992Document7 pagesCBCS - BCOM - HONS - Sem-5 - COMMERCE - DSE 5.2 A - CORPORATE ACCOUNTING-10992R3shav JaiswalNo ratings yet

- Retained Earnings Appropriation and Quasi-Reorganization Retained Earnings Appropriation and Quasi-ReorganizationDocument10 pagesRetained Earnings Appropriation and Quasi-Reorganization Retained Earnings Appropriation and Quasi-ReorganizationJamie RamosNo ratings yet

- Bonus ShareDocument2 pagesBonus ShareArpan CHATTERJEENo ratings yet

- IntroductionDocument8 pagesIntroductionGustavo Alexandre GustavoNo ratings yet

- Companies Equity Share Questions Class 12thDocument19 pagesCompanies Equity Share Questions Class 12thambika9290No ratings yet

- As 20Document6 pagesAs 20Rajiv JhaNo ratings yet

- Student Interaction Form (Responses)Document4 pagesStudent Interaction Form (Responses)SATISHNo ratings yet

- Powerpoint Presentation 1Document8 pagesPowerpoint Presentation 1SATISHNo ratings yet

- Or Practice SheetDocument15 pagesOr Practice SheetSATISHNo ratings yet

- White Book AssignmentDocument73 pagesWhite Book AssignmentSATISHNo ratings yet

- LOR - 1 - AryanDocument1 pageLOR - 1 - AryanSATISHNo ratings yet

- New Microsoft Word DocumentDocument5 pagesNew Microsoft Word Documentjgfjhf arwtrNo ratings yet

- A Project Report On Financial Performance IN NTPC Ltd. RamagundamDocument81 pagesA Project Report On Financial Performance IN NTPC Ltd. RamagundamMulukallavinay ReddyNo ratings yet

- Name - KEYDocument30 pagesName - KEYjhouvanNo ratings yet

- UNIT-2 Ratio Analysis: by Shilpa Arora Assistant Professor IitmDocument60 pagesUNIT-2 Ratio Analysis: by Shilpa Arora Assistant Professor IitmTANYANo ratings yet

- Zoological Parks Board of New South Wales June 2013Document17 pagesZoological Parks Board of New South Wales June 2013Daniel ManNo ratings yet

- Business Finance ManagementDocument14 pagesBusiness Finance ManagementMuhammad Sajid SaeedNo ratings yet

- Cash Flows 500Document41 pagesCash Flows 500MUNAWAR ALI100% (2)

- Chapte 1Document27 pagesChapte 1Mary Ann Alegria MorenoNo ratings yet

- Informe Deoleo PDFDocument13 pagesInforme Deoleo PDFEneida6736No ratings yet

- Variable CostingDocument32 pagesVariable CostingNicole J. CentenoNo ratings yet

- Financial Analysis of Hòa Phát Group Joint Stock CompanyDocument36 pagesFinancial Analysis of Hòa Phát Group Joint Stock CompanySang NguyễnNo ratings yet

- Mark Scheme (Results) : Pearson Edexcel IAL Accounting in Accounting (WAC11) Paper 01 The Accounting System and CostingDocument33 pagesMark Scheme (Results) : Pearson Edexcel IAL Accounting in Accounting (WAC11) Paper 01 The Accounting System and CostingJawad NadeemNo ratings yet

- Cost BehaviorDocument15 pagesCost BehaviorUSO CLOTHINGNo ratings yet

- Bill Snow Financial Model 2004-03-09Document43 pagesBill Snow Financial Model 2004-03-09franicoleNo ratings yet

- ACTBAS 2 Lecture 6 Adjusting EntriesDocument4 pagesACTBAS 2 Lecture 6 Adjusting EntriescsandresNo ratings yet

- Midterm Examination Spring 2010 FIN622-Corporate Finance (Session - 6)Document4 pagesMidterm Examination Spring 2010 FIN622-Corporate Finance (Session - 6)Zeeshan AhamdNo ratings yet

- Cash Flow Statement 1220159910575245 9Document17 pagesCash Flow Statement 1220159910575245 9duyphung1234No ratings yet

- Final ExamDocument3 pagesFinal ExamErica DaprosaNo ratings yet

- Expert Solution: To DetermineDocument1 pageExpert Solution: To DetermineVarun SharmaNo ratings yet

- ENTRP Week 11 20Document46 pagesENTRP Week 11 20Jr ReforbaNo ratings yet

- BalldaFAR ToFDocument12 pagesBalldaFAR ToFsantosemmanueljoseph2324No ratings yet

- Chapter 1 Test Bank - Booklet PDFDocument10 pagesChapter 1 Test Bank - Booklet PDFjasmineNo ratings yet

- Afar Quicknotes: GATO, Abdul Barri Indol MSU - Main Campus 09452146094Document19 pagesAfar Quicknotes: GATO, Abdul Barri Indol MSU - Main Campus 09452146094Zech PackNo ratings yet

- 03 Intro To AccountingDocument407 pages03 Intro To AccountingAllzoommood100% (3)

- ACCT 201 Pre-Quiz Number 6 F09Document7 pagesACCT 201 Pre-Quiz Number 6 F09bob_lahblawNo ratings yet

- T.Y.Baf Cost Accounting Sem Vi (Regular) Apr 2021: Option A Option B Option C Option DDocument5 pagesT.Y.Baf Cost Accounting Sem Vi (Regular) Apr 2021: Option A Option B Option C Option DAditya DeodharNo ratings yet

- Chapter 3 - Financial Statement AnalysisDocument4 pagesChapter 3 - Financial Statement AnalysisErlinda NavalloNo ratings yet

Download as pdf or txt

You might also like

- Full Solution Manual Applying International Financial Reporting Standards 3nd Edition by Ruth Picker SLW1019Document42 pagesFull Solution Manual Applying International Financial Reporting Standards 3nd Edition by Ruth Picker SLW1019Sm Help80% (5)

- Intermediate Accounting 2: a QuickStudy Digital Reference GuideFrom EverandIntermediate Accounting 2: a QuickStudy Digital Reference GuideNo ratings yet

- AE 112 Finals Summative AssessmentDocument12 pagesAE 112 Finals Summative AssessmentmercyvienhoNo ratings yet

- Submitted By: Cabling, Alvin Hachiles, Jomari Honera, Shawn Michael Miranda, Christopher Odonzo, Aldwin Salvador, ChristianDocument32 pagesSubmitted By: Cabling, Alvin Hachiles, Jomari Honera, Shawn Michael Miranda, Christopher Odonzo, Aldwin Salvador, ChristianKimberly Claire AtienzaNo ratings yet

- Internal ReconstructionDocument25 pagesInternal ReconstructionbhanubainsNo ratings yet

- Bandhan BankDocument37 pagesBandhan BankBandaru NarendrababuNo ratings yet

- 46480bosinter p5 cp7 PDFDocument50 pages46480bosinter p5 cp7 PDFMukesh jivrajikaNo ratings yet

- Internal ReconstructionDocument60 pagesInternal ReconstructionMighty RajuNo ratings yet

- CHP 6 Internal ReconstructionDocument60 pagesCHP 6 Internal ReconstructionRonak ChhabriaNo ratings yet

- ReconstructionDocument26 pagesReconstructionNikhilNo ratings yet

- AmalgamationDocument70 pagesAmalgamationjshashimohanNo ratings yet

- Capital Reorganisation Year 2Document60 pagesCapital Reorganisation Year 2janeth pallangyoNo ratings yet

- Wa0005.Document36 pagesWa0005.mitanshigoyal7No ratings yet

- What Is Reconstruction?: Need For Internal ReconstructionDocument31 pagesWhat Is Reconstruction?: Need For Internal Reconstructionneeru79200079% (14)

- Internal Reconstruction Part-IDocument19 pagesInternal Reconstruction Part-ISahil GuptaNo ratings yet

- Reconstruction InternalDocument12 pagesReconstruction InternalsviimaNo ratings yet

- Module 6Document50 pagesModule 6rohit saini75% (4)

- DR - Srinivas Madishetti Professor, School of Business Mzumbe UniversityDocument67 pagesDR - Srinivas Madishetti Professor, School of Business Mzumbe UniversityNicole TaylorNo ratings yet

- March 2023 Answer Key CorporateaccountingDocument11 pagesMarch 2023 Answer Key Corporateaccountinghisarahhh4No ratings yet

- 5 6084915055709651012Document8 pages5 6084915055709651012Ajit Yadav100% (1)

- Business CombinationsDocument18 pagesBusiness Combinationszubair afzalNo ratings yet

- Alteration & Reduction of Share CapitalDocument5 pagesAlteration & Reduction of Share CapitalHasnain MahmoodNo ratings yet

- Share Holders Equity: BOOKS and Records of A CorporationDocument5 pagesShare Holders Equity: BOOKS and Records of A CorporationQueen ValleNo ratings yet

- Financial AccountingDocument11 pagesFinancial AccountingRakesh ChauhanNo ratings yet

- Internal Reconstruction - Theory NotesDocument3 pagesInternal Reconstruction - Theory NotesNaomi SaldanhaNo ratings yet

- Module 2 Shareholders Equity Students ReferenceDocument7 pagesModule 2 Shareholders Equity Students ReferencecynangelaNo ratings yet

- Retained Earnings: Appropriation and Quasi-ReorganizationDocument25 pagesRetained Earnings: Appropriation and Quasi-ReorganizationtruthNo ratings yet

- Session 3c Share Capital & Reserves: HI5020 Corporate AccountingDocument29 pagesSession 3c Share Capital & Reserves: HI5020 Corporate AccountingFeku RamNo ratings yet

- Reconstruction of A CompanyDocument9 pagesReconstruction of A Companywolverinelogan806No ratings yet

- A 11 Internal Reconstruction of A CompanyDocument18 pagesA 11 Internal Reconstruction of A CompanyDhananjay Pawar50% (2)

- Internal ReconstructionDocument8 pagesInternal Reconstructionsmit9993No ratings yet

- 23 Share Capital s22 - FinalDocument23 pages23 Share Capital s22 - FinalAphelele GqadaNo ratings yet

- Introduction To Internal Reconstruction of CompaniesDocument17 pagesIntroduction To Internal Reconstruction of CompaniesMichael NyaongoNo ratings yet

- 1 Chapter 5 Internal Reconstruction PDFDocument22 pages1 Chapter 5 Internal Reconstruction PDFAbhiramNo ratings yet

- The Statement of Changes in EquityDocument9 pagesThe Statement of Changes in EquityDanerish PabunanNo ratings yet

- PM Ipcc Acc Vol2 Chapter5Document26 pagesPM Ipcc Acc Vol2 Chapter5ShambuReddyNo ratings yet

- IFRS Chap 2Document42 pagesIFRS Chap 2Yousef Abdullah GhundulNo ratings yet

- 12 Accountancy Notes CH07 Company Accounts Issue of Shares 01Document20 pages12 Accountancy Notes CH07 Company Accounts Issue of Shares 01zainab.xf77No ratings yet

- 2017 Class 16 EquityDocument35 pages2017 Class 16 EquityChandra Sekhar ChittineniNo ratings yet

- Chapter 10 Equity Part 2Document27 pagesChapter 10 Equity Part 2LEE WEI LONGNo ratings yet

- Lecture 4-PostDocument40 pagesLecture 4-PostcoolirlbbNo ratings yet

- Statement of Changes in Equity and The Balance SheetDocument82 pagesStatement of Changes in Equity and The Balance SheetnicoNo ratings yet

- Week 7 NotesDocument6 pagesWeek 7 NotescalebNo ratings yet

- UNIT 2 & 4 MergedDocument41 pagesUNIT 2 & 4 MergedRich ManNo ratings yet

- Internal Reconstruction of CompaniesDocument4 pagesInternal Reconstruction of CompaniesZiya ShaikhNo ratings yet

- Advanced Financial Accounting IDocument7 pagesAdvanced Financial Accounting IRoNo ratings yet

- 54232bos43539cp4 U4Document53 pages54232bos43539cp4 U4Akash KamathNo ratings yet

- Take Print - Adv AccDocument11 pagesTake Print - Adv AccManikandanNo ratings yet

- CA Inter Accounts A MTP 1 Nov 2022Document13 pagesCA Inter Accounts A MTP 1 Nov 2022smartshivenduNo ratings yet

- Retained Earnings - Appropriation and Quasi-Reorganization - 0Document29 pagesRetained Earnings - Appropriation and Quasi-Reorganization - 0lilienesieraNo ratings yet

- Beams9esm Ch01Document13 pagesBeams9esm Ch01zandra SumbarNo ratings yet

- Chapter 10 - Accounting For Equity: Learning ObjectivesDocument11 pagesChapter 10 - Accounting For Equity: Learning ObjectivesBình Trần ThanhNo ratings yet

- Bv2018 Revised Conceptual FrameworkDocument18 pagesBv2018 Revised Conceptual FrameworkTeneswari RadhaNo ratings yet

- Unit - 4: Amalgamation and ReconstructionDocument54 pagesUnit - 4: Amalgamation and ReconstructionAzad AboobackerNo ratings yet

- HA2032Document12 pagesHA2032Aayam SubediNo ratings yet

- CHAPTER 14 Non. 14Document6 pagesCHAPTER 14 Non. 14Ahmed AymanNo ratings yet

- Buy Back of SharesDocument17 pagesBuy Back of Shareskunaldudu345No ratings yet

- CBCS - BCOM - HONS - Sem-5 - COMMERCE - DSE 5.2 A - CORPORATE ACCOUNTING-10992Document7 pagesCBCS - BCOM - HONS - Sem-5 - COMMERCE - DSE 5.2 A - CORPORATE ACCOUNTING-10992R3shav JaiswalNo ratings yet

- Retained Earnings Appropriation and Quasi-Reorganization Retained Earnings Appropriation and Quasi-ReorganizationDocument10 pagesRetained Earnings Appropriation and Quasi-Reorganization Retained Earnings Appropriation and Quasi-ReorganizationJamie RamosNo ratings yet

- Bonus ShareDocument2 pagesBonus ShareArpan CHATTERJEENo ratings yet

- IntroductionDocument8 pagesIntroductionGustavo Alexandre GustavoNo ratings yet

- Companies Equity Share Questions Class 12thDocument19 pagesCompanies Equity Share Questions Class 12thambika9290No ratings yet

- As 20Document6 pagesAs 20Rajiv JhaNo ratings yet

- Student Interaction Form (Responses)Document4 pagesStudent Interaction Form (Responses)SATISHNo ratings yet

- Powerpoint Presentation 1Document8 pagesPowerpoint Presentation 1SATISHNo ratings yet

- Or Practice SheetDocument15 pagesOr Practice SheetSATISHNo ratings yet

- White Book AssignmentDocument73 pagesWhite Book AssignmentSATISHNo ratings yet

- LOR - 1 - AryanDocument1 pageLOR - 1 - AryanSATISHNo ratings yet

- New Microsoft Word DocumentDocument5 pagesNew Microsoft Word Documentjgfjhf arwtrNo ratings yet

- A Project Report On Financial Performance IN NTPC Ltd. RamagundamDocument81 pagesA Project Report On Financial Performance IN NTPC Ltd. RamagundamMulukallavinay ReddyNo ratings yet

- Name - KEYDocument30 pagesName - KEYjhouvanNo ratings yet

- UNIT-2 Ratio Analysis: by Shilpa Arora Assistant Professor IitmDocument60 pagesUNIT-2 Ratio Analysis: by Shilpa Arora Assistant Professor IitmTANYANo ratings yet

- Zoological Parks Board of New South Wales June 2013Document17 pagesZoological Parks Board of New South Wales June 2013Daniel ManNo ratings yet

- Business Finance ManagementDocument14 pagesBusiness Finance ManagementMuhammad Sajid SaeedNo ratings yet

- Cash Flows 500Document41 pagesCash Flows 500MUNAWAR ALI100% (2)

- Chapte 1Document27 pagesChapte 1Mary Ann Alegria MorenoNo ratings yet

- Informe Deoleo PDFDocument13 pagesInforme Deoleo PDFEneida6736No ratings yet

- Variable CostingDocument32 pagesVariable CostingNicole J. CentenoNo ratings yet

- Financial Analysis of Hòa Phát Group Joint Stock CompanyDocument36 pagesFinancial Analysis of Hòa Phát Group Joint Stock CompanySang NguyễnNo ratings yet

- Mark Scheme (Results) : Pearson Edexcel IAL Accounting in Accounting (WAC11) Paper 01 The Accounting System and CostingDocument33 pagesMark Scheme (Results) : Pearson Edexcel IAL Accounting in Accounting (WAC11) Paper 01 The Accounting System and CostingJawad NadeemNo ratings yet

- Cost BehaviorDocument15 pagesCost BehaviorUSO CLOTHINGNo ratings yet

- Bill Snow Financial Model 2004-03-09Document43 pagesBill Snow Financial Model 2004-03-09franicoleNo ratings yet

- ACTBAS 2 Lecture 6 Adjusting EntriesDocument4 pagesACTBAS 2 Lecture 6 Adjusting EntriescsandresNo ratings yet

- Midterm Examination Spring 2010 FIN622-Corporate Finance (Session - 6)Document4 pagesMidterm Examination Spring 2010 FIN622-Corporate Finance (Session - 6)Zeeshan AhamdNo ratings yet

- Cash Flow Statement 1220159910575245 9Document17 pagesCash Flow Statement 1220159910575245 9duyphung1234No ratings yet

- Final ExamDocument3 pagesFinal ExamErica DaprosaNo ratings yet

- Expert Solution: To DetermineDocument1 pageExpert Solution: To DetermineVarun SharmaNo ratings yet

- ENTRP Week 11 20Document46 pagesENTRP Week 11 20Jr ReforbaNo ratings yet

- BalldaFAR ToFDocument12 pagesBalldaFAR ToFsantosemmanueljoseph2324No ratings yet

- Chapter 1 Test Bank - Booklet PDFDocument10 pagesChapter 1 Test Bank - Booklet PDFjasmineNo ratings yet

- Afar Quicknotes: GATO, Abdul Barri Indol MSU - Main Campus 09452146094Document19 pagesAfar Quicknotes: GATO, Abdul Barri Indol MSU - Main Campus 09452146094Zech PackNo ratings yet

- 03 Intro To AccountingDocument407 pages03 Intro To AccountingAllzoommood100% (3)

- ACCT 201 Pre-Quiz Number 6 F09Document7 pagesACCT 201 Pre-Quiz Number 6 F09bob_lahblawNo ratings yet

- T.Y.Baf Cost Accounting Sem Vi (Regular) Apr 2021: Option A Option B Option C Option DDocument5 pagesT.Y.Baf Cost Accounting Sem Vi (Regular) Apr 2021: Option A Option B Option C Option DAditya DeodharNo ratings yet

- Chapter 3 - Financial Statement AnalysisDocument4 pagesChapter 3 - Financial Statement AnalysisErlinda NavalloNo ratings yet