Download as pdf or txt

You might also like

- Bank StatementDocument10 pagesBank StatementMuhammad Danial100% (1)

- The (Questionable) Legality of High-Speed "Pinging" and "Front Running" in The Futures MarketsDocument92 pagesThe (Questionable) Legality of High-Speed "Pinging" and "Front Running" in The Futures Marketslanassa2785No ratings yet

- Over-The-Counter Markets. Using These Principles As A Guide, The Association Seeks To Work With Congress, Regulators andDocument5 pagesOver-The-Counter Markets. Using These Principles As A Guide, The Association Seeks To Work With Congress, Regulators andMarketsWikiNo ratings yet

- Structure of Future ContractDocument3 pagesStructure of Future ContractanbuNo ratings yet

- International Repo Council/ European Repo Council Repo Trading Practice GuidelinesDocument6 pagesInternational Repo Council/ European Repo Council Repo Trading Practice GuidelinesVugar NamazovNo ratings yet

- Neal WolkoffDocument5 pagesNeal WolkoffMarketsWikiNo ratings yet

- Mat Qa FinalDocument2 pagesMat Qa FinalMarketsWikiNo ratings yet

- RTPR QaDocument3 pagesRTPR QaMarketsWikiNo ratings yet

- Re: File No. S7-06-11 - Registration and Regulation of Security-Based Swap Execution Facilities (76 Fed. Reg. 10948)Document13 pagesRe: File No. S7-06-11 - Registration and Regulation of Security-Based Swap Execution Facilities (76 Fed. Reg. 10948)MarketsWikiNo ratings yet

- Executive SummaryDocument8 pagesExecutive SummaryMarketsWikiNo ratings yet

- Forwards Contract:: Futures and Forwards Are Financial Contracts Which Are Very Similar in Nature But ThereDocument7 pagesForwards Contract:: Futures and Forwards Are Financial Contracts Which Are Very Similar in Nature But ThereFardeen KhanNo ratings yet

- Glossary For Retail FX: A American Style OptionDocument16 pagesGlossary For Retail FX: A American Style OptionJeeth RaiNo ratings yet

- Chapter 15Document20 pagesChapter 15Anji AnjikumarNo ratings yet

- Via Electronic SubmissionDocument10 pagesVia Electronic SubmissionMarketsWikiNo ratings yet

- Dhaka Stcok Exchange Automated Trading Regulations, 1999.: Dated, The 23rd October, 1999Document9 pagesDhaka Stcok Exchange Automated Trading Regulations, 1999.: Dated, The 23rd October, 1999bijon1983No ratings yet

- Microstructure of The Egyptian Stock MarketDocument21 pagesMicrostructure of The Egyptian Stock MarketZakaria HegazyNo ratings yet

- MFA3Document8 pagesMFA3MarketsWikiNo ratings yet

- Futures Industry Institute Intro To Futures & Options MKTDocument17 pagesFutures Industry Institute Intro To Futures & Options MKTalinaNo ratings yet

- Market Making Rules VFEXDocument10 pagesMarket Making Rules VFEXtaps tichNo ratings yet

- Core Principles and Other Requirements For Designated Contract MarketsDocument15 pagesCore Principles and Other Requirements For Designated Contract MarketsMarketsWikiNo ratings yet

- Succeed Derivaties: Derivatives Are Used by Investors For The FollowingDocument6 pagesSucceed Derivaties: Derivatives Are Used by Investors For The FollowingShivam ThaliaNo ratings yet

- A Theory of Price Limits in Futures Markets 1986 Journal of Financial EconomicsDocument21 pagesA Theory of Price Limits in Futures Markets 1986 Journal of Financial EconomicsZhang PeilinNo ratings yet

- Trading Procedures - EN - 20211108Document49 pagesTrading Procedures - EN - 20211108jeevitha_24No ratings yet

- Energy TradeDocument48 pagesEnergy TradeNaina Singh AdarshNo ratings yet

- Terms of BusinessDocument7 pagesTerms of BusinessAda la ki zongoNo ratings yet

- Chapter Xi: Forwards, Futures and Other Derivatives A. Forward and Futures ContractsDocument8 pagesChapter Xi: Forwards, Futures and Other Derivatives A. Forward and Futures Contractslib_01No ratings yet

- Stock ExchangeDocument30 pagesStock Exchangemansavi bihaniNo ratings yet

- 27910JanetMcGinness 1Document15 pages27910JanetMcGinness 1MarketsWikiNo ratings yet

- SEC New Rules and Ammendments 23 December 2019 PDFDocument97 pagesSEC New Rules and Ammendments 23 December 2019 PDFOluwafunto OlasemoNo ratings yet

- Algorithmic TradingDocument18 pagesAlgorithmic TradingFramurz Patel0% (1)

- Vol-7 Futures Trading Guide PDFDocument26 pagesVol-7 Futures Trading Guide PDFUtkarshNo ratings yet

- Assignment 3, International Banking Shafiqullah, Reg No, Su-17-01-021-001, Bba 8th.Document5 pagesAssignment 3, International Banking Shafiqullah, Reg No, Su-17-01-021-001, Bba 8th.Shafiq UllahNo ratings yet

- Submitted Via Agency WebsiteDocument7 pagesSubmitted Via Agency WebsiteMarketsWikiNo ratings yet

- Re: File Number S7-34-10 - Proposed Rules: Regulation SBSR - Reporting and Dissemination of Security-Based Swap InformationDocument7 pagesRe: File Number S7-34-10 - Proposed Rules: Regulation SBSR - Reporting and Dissemination of Security-Based Swap InformationMarketsWikiNo ratings yet

- Executive SummaryDocument5 pagesExecutive SummaryMarketsWikiNo ratings yet

- Risk MGMTDocument28 pagesRisk MGMTAmina AltafNo ratings yet

- Option Chain Part-9Document3 pagesOption Chain Part-9ramyatan SinghNo ratings yet

- Report-Role of Derivative in Economic DevelopmentDocument22 pagesReport-Role of Derivative in Economic DevelopmentKanika AnejaNo ratings yet

- Stock Exchange MechanismDocument24 pagesStock Exchange MechanismSandeep Sandeep SinghNo ratings yet

- 3 DRM Contract DesignDocument18 pages3 DRM Contract DesignPrasanjit BiswasNo ratings yet

- Silber - 1984 - Marketmaker Behavior in An Auction Market, An Analysis of Scalpers in Futures MarketsDocument18 pagesSilber - 1984 - Marketmaker Behavior in An Auction Market, An Analysis of Scalpers in Futures MarketsjpkoningNo ratings yet

- Swap ParticipantsDocument6 pagesSwap ParticipantsMarketsWikiNo ratings yet

- Order Execution Policy NBRB Capital ComDocument6 pagesOrder Execution Policy NBRB Capital ComSidney-SultanoNo ratings yet

- Structure of Forwards Future MarketsDocument23 pagesStructure of Forwards Future MarketsRahimullah QaziNo ratings yet

- Bulk and Block DifferenceDocument4 pagesBulk and Block DifferenceRituNo ratings yet

- Liffe AbbrDocument17 pagesLiffe AbbrshturmanjokerNo ratings yet

- What Are DerivativesDocument7 pagesWhat Are DerivativesMohit ModiNo ratings yet

- WORK SHEET - Financial Derivatives: Q1) Enumerate The Basic Differences Between Forward and Futures ContractsDocument5 pagesWORK SHEET - Financial Derivatives: Q1) Enumerate The Basic Differences Between Forward and Futures ContractsBhavesh RathiNo ratings yet

- D D D ! " #$% D & ' D (Document9 pagesD D D ! " #$% D & ' D (Zubair TahirNo ratings yet

- Copy (2) of Futures Market Trading Mechanism-1Document14 pagesCopy (2) of Futures Market Trading Mechanism-1Pradipta Sahoo100% (1)

- Future & Options FinalDocument8 pagesFuture & Options Finalabhiraj_bangeraNo ratings yet

- CHAPTER5Document3 pagesCHAPTER5RODELYN MIRANNo ratings yet

- 26598MGEXDocument4 pages26598MGEXMarketsWikiNo ratings yet

- Isda and SifmaDocument15 pagesIsda and SifmaMarketsWikiNo ratings yet

- Basics of Futures TradingDocument4 pagesBasics of Futures TradingSlobodan SlovicNo ratings yet

- Options, Futures, and Othe R Derivatives: Chapter 1 IntroductionDocument32 pagesOptions, Futures, and Othe R Derivatives: Chapter 1 IntroductionBasappaSarkarNo ratings yet

- Defination of Futures Difference Between Forward and Futures Futures Mechanism in Stock ExchangeDocument20 pagesDefination of Futures Difference Between Forward and Futures Futures Mechanism in Stock Exchangenipul_agrawalNo ratings yet

- Via Electronic Mail: Chief Executive OfficerDocument5 pagesVia Electronic Mail: Chief Executive OfficerMarketsWikiNo ratings yet

- 3-Statement CompactDocument4 pages3-Statement CompactJames BondNo ratings yet

- Sugar Annual - Kingston - Jamaica - 04-15-2021Document8 pagesSugar Annual - Kingston - Jamaica - 04-15-2021Zineil BlackwoodNo ratings yet

- What Is The Keynesian MultiplierDocument17 pagesWhat Is The Keynesian MultiplierjamesNo ratings yet

- The Empirical Analysis of Agricultural Exports and Economic Growth in NigeriaDocument10 pagesThe Empirical Analysis of Agricultural Exports and Economic Growth in NigeriaYusif AxundovNo ratings yet

- Chapter 9 - Interim Financial ReportingDocument17 pagesChapter 9 - Interim Financial Reportingarlynajero.ckcNo ratings yet

- Impact of Currency Fluctuations On International Business and Cost Effectiveness in NigeriaDocument9 pagesImpact of Currency Fluctuations On International Business and Cost Effectiveness in NigeriaOpen Access JournalNo ratings yet

- Art. 1164. The Creditor Has A Right To The Fruits of The Thing From The Time The Obligation ToDocument3 pagesArt. 1164. The Creditor Has A Right To The Fruits of The Thing From The Time The Obligation ToKinitDelfinCelestial100% (3)

- Hoisery ManufacturesDocument83 pagesHoisery ManufacturesJamalSultan0% (1)

- The Economist 2021 PDFDocument412 pagesThe Economist 2021 PDFHsn Gn76% (21)

- Office of The Municipal AgriculturistDocument27 pagesOffice of The Municipal AgriculturistReynole DulaganNo ratings yet

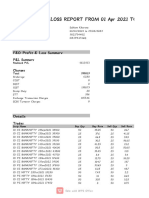

- Fno Profit & Loss Report From 01 Apr 2021 ToDocument8 pagesFno Profit & Loss Report From 01 Apr 2021 ToSourabh AhujaNo ratings yet

- GENERAL MATHEMATICS Week 1Document36 pagesGENERAL MATHEMATICS Week 1Jeweljoy PudaNo ratings yet

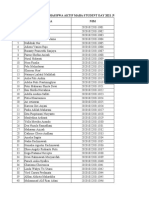

- Daftar Hadir Peserta Maba Student Day 2021 Minggu Ke-5Document55 pagesDaftar Hadir Peserta Maba Student Day 2021 Minggu Ke-5Tiara Arana MaudyNo ratings yet

- The Global Economic CrisisDocument417 pagesThe Global Economic CrisisAbdus Salam TambeNo ratings yet

- Accounting For Revenue Workout EmptyDocument3 pagesAccounting For Revenue Workout EmptyRgchiNo ratings yet

- Unit 1 Family Life - SpeakingDocument12 pagesUnit 1 Family Life - Speakingphong phanNo ratings yet

- Chapter 5 SolutionsDocument29 pagesChapter 5 SolutionsFahad BataviaNo ratings yet

- Topic 5 - Contemporary Model of Development & UnderdevelopmentDocument6 pagesTopic 5 - Contemporary Model of Development & UnderdevelopmentKathlene BalicoNo ratings yet

- Thesis On Banking in IndiaDocument4 pagesThesis On Banking in Indiamichellebojorqueznorwalk100% (2)

- SCSM 2022 Runners Information GuideDocument36 pagesSCSM 2022 Runners Information GuideDollar SurvivorNo ratings yet

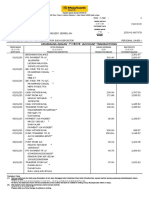

- Debit Note: Invoice No: HINV21070262Document1 pageDebit Note: Invoice No: HINV21070262Ng AllenNo ratings yet

- RIsk FactorsDocument8 pagesRIsk FactorsMAHA ZENABNo ratings yet

- 4PS Module Answer Sheets ChecklistDocument2 pages4PS Module Answer Sheets Checklistusep manatadNo ratings yet

- Volatile: Strategies For Volatile ViewDocument12 pagesVolatile: Strategies For Volatile ViewAshutosh ChauhanNo ratings yet

- Rbi Email IDDocument2 pagesRbi Email IDsanjayb19760% (1)

- India PostDocument29 pagesIndia PostGPS COMPUTER HATI100% (1)

- Foreign Exchange Operation of Union Bank of IndiaDocument2 pagesForeign Exchange Operation of Union Bank of IndiaPRO FilmmakerNo ratings yet

- 11th Economics Lesson 789 Model Question Paper English MediumDocument4 pages11th Economics Lesson 789 Model Question Paper English MediumRajkumarNo ratings yet

- Thesis Proposal International RelationsDocument7 pagesThesis Proposal International Relationsmak0dug0vuk2100% (2)