Download as pdf or txt

You might also like

- DIY Credit Repair GuideDocument21 pagesDIY Credit Repair GuideAnthony VinsonNo ratings yet

- CBSE Accountancy 12th Term 2 CH 3Document5 pagesCBSE Accountancy 12th Term 2 CH 3AadasNo ratings yet

- XII ACCOUNTANCY SET-2 Marking Scheme Ist Pre Board 2023-24-1Document9 pagesXII ACCOUNTANCY SET-2 Marking Scheme Ist Pre Board 2023-24-1Riddhima Murarka50% (2)

- Accountancy-MS 23-24Document10 pagesAccountancy-MS 23-24Ashutosh SinghNo ratings yet

- Accountancy MSDocument11 pagesAccountancy MSmansoorbariNo ratings yet

- Accountancy 2023-24 MSDocument11 pagesAccountancy 2023-24 MSirfanoushad15No ratings yet

- Set - 1 Acc MS PB12023-24Document10 pagesSet - 1 Acc MS PB12023-24aamiralishiasbackup1No ratings yet

- Hsslive Xii Acc 3 Admission of A Partner KeyDocument8 pagesHsslive Xii Acc 3 Admission of A Partner KeyShinu ShinadNo ratings yet

- Solution Ultimate Sample Paper 2Document7 pagesSolution Ultimate Sample Paper 2Nitin KumarNo ratings yet

- Ans. Chapter-9Document6 pagesAns. Chapter-9upscmindworksNo ratings yet

- MS Accountancy Set 10Document18 pagesMS Accountancy Set 10Tanisha TibrewalNo ratings yet

- Marking Scheme Mock Test I 2023 24Document9 pagesMarking Scheme Mock Test I 2023 24HARSH CHAURASIYANo ratings yet

- 5.cpbe - Xii Accts - MSDocument18 pages5.cpbe - Xii Accts - MScommerce12onlineclassesNo ratings yet

- Accountancy - Grade 11 - MSDocument9 pagesAccountancy - Grade 11 - MSks2jq4w9cwNo ratings yet

- Issue of Shares With PremiumDocument4 pagesIssue of Shares With PremiumPankaj KandpalNo ratings yet

- TS Grewal Solutions Class 12 Accountancy Volume 1 Chapter 7 - Dissolution of Partnership FirmDocument17 pagesTS Grewal Solutions Class 12 Accountancy Volume 1 Chapter 7 - Dissolution of Partnership FirmMayank Garange100% (2)

- XII Acc SQP 1 (AP 23-24)Document11 pagesXII Acc SQP 1 (AP 23-24)Vaidehi BagraNo ratings yet

- MTP-1 (Solutions (QR Code) )Document13 pagesMTP-1 (Solutions (QR Code) )ajay.007.sngNo ratings yet

- MS Accountancy Set 2Document9 pagesMS Accountancy Set 2Tanisha TibrewalNo ratings yet

- Answer Keys & Marking Scheme Acc XiiDocument8 pagesAnswer Keys & Marking Scheme Acc XiiGHOST FFNo ratings yet

- Internal Reconstruction - HomeworkDocument25 pagesInternal Reconstruction - HomeworkYash ShewaleNo ratings yet

- Paper2 Set2 SolutionDocument7 pagesPaper2 Set2 Solutionadityatiwari122006No ratings yet

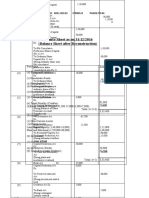

- Balance Sheet As On 31/12/2016 (Balance Sheet After Reconstruction)Document8 pagesBalance Sheet As On 31/12/2016 (Balance Sheet After Reconstruction)GauravNo ratings yet

- 2023 24 Xii Pre Board 1 MsDocument13 pages2023 24 Xii Pre Board 1 MsacguptaclassesNo ratings yet

- Class 11 Accounts SP 2 Answer KeyDocument18 pagesClass 11 Accounts SP 2 Answer KeyUdyamGNo ratings yet

- Additional Questions 9Document3 pagesAdditional Questions 910 368 Zakwan BaigNo ratings yet

- XII CBSE - Accounts HY Exam - 01-Oct-2022 (Sug)Document7 pagesXII CBSE - Accounts HY Exam - 01-Oct-2022 (Sug)naviagrawal2006No ratings yet

- Accountancy MARKING SCHEME Class-XII Set-IDocument9 pagesAccountancy MARKING SCHEME Class-XII Set-Iaamiralishiasbackup1No ratings yet

- Marking Scheme: PRE - BOARD-2 (2023 - 2024)Document11 pagesMarking Scheme: PRE - BOARD-2 (2023 - 2024)Kaustav DasNo ratings yet

- MS - Accountancy - 12-Practice Paper-1Document7 pagesMS - Accountancy - 12-Practice Paper-1Arun kumarNo ratings yet

- Marking Scheme, Set-3: CLASS-12, Accountancy MM:80 Time: 3 Hrs Part A - Accounting For Partnership Firms and CompaniesDocument9 pagesMarking Scheme, Set-3: CLASS-12, Accountancy MM:80 Time: 3 Hrs Part A - Accounting For Partnership Firms and CompaniesKunwar PalNo ratings yet

- Final Accounts 1. As Per Schedule III of Companies Act 2013, Prepare Financial Statement For Gillette India PVT LTDDocument3 pagesFinal Accounts 1. As Per Schedule III of Companies Act 2013, Prepare Financial Statement For Gillette India PVT LTDermiasNo ratings yet

- CBSE Sample Paper 2024 Class 12 Accountancy MSDocument11 pagesCBSE Sample Paper 2024 Class 12 Accountancy MSskhushbusahniNo ratings yet

- Solutions of CH - RetirementDocument5 pagesSolutions of CH - RetirementDamanjot SinghNo ratings yet

- Caa Assignment SolutionsDocument39 pagesCaa Assignment Solutionschikanesakshi2001No ratings yet

- Set 2 MS, 2ND PBDocument10 pagesSet 2 MS, 2ND PBHarini NarayananNo ratings yet

- XII Accountancy MorningDocument18 pagesXII Accountancy Morningarihant jainNo ratings yet

- Internal Reconstruction PQ SolDocument17 pagesInternal Reconstruction PQ SolKaran MokhaNo ratings yet

- Sujeet Sjuje BktesDocument13 pagesSujeet Sjuje BktesPawan TalrejaNo ratings yet

- MS Accountancy Set 5Document9 pagesMS Accountancy Set 5Tanisha TibrewalNo ratings yet

- CBSE Class XII 2024 Commerce Accountancy Sample Paper SolDocument11 pagesCBSE Class XII 2024 Commerce Accountancy Sample Paper Solrajputudbhav2429No ratings yet

- Test Your Knowledge - 7Document2 pagesTest Your Knowledge - 7narangdiya602No ratings yet

- Sample Paper: Maximum Marks 4Document13 pagesSample Paper: Maximum Marks 4PurvaNo ratings yet

- Advance Accounting Solutions 36 Pages 2Document36 pagesAdvance Accounting Solutions 36 Pages 2R ChandrasekarNo ratings yet

- 6.XII Accountancy Marking SchemeDocument10 pages6.XII Accountancy Marking Schemecommerce12onlineclassesNo ratings yet

- Sample Paper-1 (Target Term - 2) Answers: Book Recommended - Ultimate Book of Accountancy Class 12Document8 pagesSample Paper-1 (Target Term - 2) Answers: Book Recommended - Ultimate Book of Accountancy Class 12Beena ShibuNo ratings yet

- P18Document23 pagesP18aleeshaNo ratings yet

- Marking SchemeDocument6 pagesMarking Schemeraghu monnappaNo ratings yet

- Pass The Journal Entries For The Following Transactions On The Dissolution of The Firm of P and Q After Various Assets - AccountancyDocument3 pagesPass The Journal Entries For The Following Transactions On The Dissolution of The Firm of P and Q After Various Assets - Accountancydhanya1995No ratings yet

- CA Foundation Accounting SolutionsDocument117 pagesCA Foundation Accounting SolutionsAkash AjayNo ratings yet

- Xii Accountancy MORNINGDocument22 pagesXii Accountancy MORNINGJonathan Ishit MasiyaNo ratings yet

- Xi See Acc 2021 Set 2 MsDocument5 pagesXi See Acc 2021 Set 2 Mss1672snehil6353No ratings yet

- Answer Key 3Document8 pagesAnswer Key 3Hari prakarsh NimiNo ratings yet

- Partnership - Admission of Partner - DPP 10 (Of Lecture 12) - (Kautilya)Document8 pagesPartnership - Admission of Partner - DPP 10 (Of Lecture 12) - (Kautilya)Shreyash JhaNo ratings yet

- MS Accountancy XIIDocument8 pagesMS Accountancy XIISahil RaikwarNo ratings yet

- Answer Key - 1 TermDocument9 pagesAnswer Key - 1 TermsamayaksahuNo ratings yet

- QUESTION PAPER 1 (Solution) : Q.1 A) Multiple Choice QuestionsDocument13 pagesQUESTION PAPER 1 (Solution) : Q.1 A) Multiple Choice QuestionsSiddharth VoraNo ratings yet

- 2023 AccountancyDocument12 pages2023 Accountancyjatt145873No ratings yet

- Accountancy SolutionsDocument5 pagesAccountancy Solutionsrajpranav239No ratings yet

- Banking CompaniesDocument38 pagesBanking CompaniesT.V.B.M.ChaitanyaNo ratings yet

- Training Manager VP Banking in Chicago IL Resume Anthony FernandezDocument2 pagesTraining Manager VP Banking in Chicago IL Resume Anthony FernandezAnthonyFernandez2No ratings yet

- Fabm - Q2 - Las-For LearnersDocument113 pagesFabm - Q2 - Las-For LearnersABM-AKRISTINE DELA CRUZNo ratings yet

- TDS Rate Chart For FY 2023-2024 (AY 2024-2025)Document8 pagesTDS Rate Chart For FY 2023-2024 (AY 2024-2025)sourabh tamhankarNo ratings yet

- Problem+Set+ 3+ Spring+2014,+0930Document8 pagesProblem+Set+ 3+ Spring+2014,+0930jessica_1292No ratings yet

- KKR - Creating Sustainable ValueDocument54 pagesKKR - Creating Sustainable ValueMariah SharpNo ratings yet

- Unit 9: Investment: Related Keynotes 1. Unit 5 Success (Pre-Intermediate Coursebook)Document3 pagesUnit 9: Investment: Related Keynotes 1. Unit 5 Success (Pre-Intermediate Coursebook)nhNo ratings yet

- Isurance CarDocument506 pagesIsurance CarLatif SugandiNo ratings yet

- MSC Accounting and Finance Dissertation TopicsDocument5 pagesMSC Accounting and Finance Dissertation TopicsAcademicPaperWritersSingapore100% (1)

- Calculadora ExternaDocument101 pagesCalculadora ExternaIgor Glingani PierineNo ratings yet

- Ifrs PaperDocument17 pagesIfrs Paperapi-290991306No ratings yet

- Estate-Taxation QAsDocument9 pagesEstate-Taxation QAsTeresaNo ratings yet

- AnnuityDocument46 pagesAnnuityJeffreyMitra100% (2)

- Fundamentals of Accounting 1Document8 pagesFundamentals of Accounting 1Kathleen MaynigoNo ratings yet

- Questioner For Finman AssessmentDocument12 pagesQuestioner For Finman AssessmentAugust Restiawan SoetisnjoNo ratings yet

- Introduction of EcgcDocument41 pagesIntroduction of Ecgcurmi_patel22100% (3)

- User Manual: Version No.: 2.0Document147 pagesUser Manual: Version No.: 2.0BabanNo ratings yet

- NXN Aarsrapport 2005 PDFDocument28 pagesNXN Aarsrapport 2005 PDFkrida puspitasariNo ratings yet

- Lpo Financing Application FormDocument2 pagesLpo Financing Application Formcharles young wambuaNo ratings yet

- Managing Corporate Performance With Balanced ScorecardDocument45 pagesManaging Corporate Performance With Balanced ScorecardHery KurniawanNo ratings yet

- Capítulo 3 - InvestimentosDocument31 pagesCapítulo 3 - InvestimentosLúcia Rodrigues da SilvaNo ratings yet

- Financial Management 2 Test 2Document3 pagesFinancial Management 2 Test 2William MushongaNo ratings yet

- m02 Government Budget and The EconomyDocument17 pagesm02 Government Budget and The EconomyAman patidarNo ratings yet

- 10 - Financing of Railway Projects - IRADocument34 pages10 - Financing of Railway Projects - IRAsakethmekalaNo ratings yet

- Investment Managers-17aug2022 1137-ExportDocument4 pagesInvestment Managers-17aug2022 1137-Exportmelody.haukongoNo ratings yet

- Savings and Credit Co-Operative League of South Africa Limited (Saccol)Document16 pagesSavings and Credit Co-Operative League of South Africa Limited (Saccol)astig79No ratings yet

- Patricia A Seitz Financial Disclosure Report For 2010Document7 pagesPatricia A Seitz Financial Disclosure Report For 2010Judicial Watch, Inc.No ratings yet

- Globalization, Urban Form and GovernanceDocument231 pagesGlobalization, Urban Form and GovernanceDelftdigitalpressNo ratings yet

- Cost and Management AccountingDocument4 pagesCost and Management AccountingHooriaNo ratings yet