Download as docx, pdf, or txt

You might also like

- ICICI Banking Corporation LTD.: Assessment of Working Capital Requirements Form Ii - Operating StatementDocument16 pagesICICI Banking Corporation LTD.: Assessment of Working Capital Requirements Form Ii - Operating StatementPravin Namokar100% (1)

- Portfolio Investment ReportDocument27 pagesPortfolio Investment ReportSowmya04No ratings yet

- Supply and Demand How To Find and Trade The Best ZonesNew PDFDocument25 pagesSupply and Demand How To Find and Trade The Best ZonesNew PDFYagnesh Patel100% (12)

- Interim Report 21BSP3460 - Pooja SureshDocument19 pagesInterim Report 21BSP3460 - Pooja SureshChahat PartapNo ratings yet

- WORKING CAPITAL DocxDocument16 pagesWORKING CAPITAL DocxGab IgnacioNo ratings yet

- Portfolio Management ReportDocument35 pagesPortfolio Management Reportfarah_hhrrNo ratings yet

- Our Favorite Inflation-Prot...Document2 pagesOur Favorite Inflation-Prot...nicole_yang_100No ratings yet

- Q1 2020 ThirdPoint-InvestorLetterDocument11 pagesQ1 2020 ThirdPoint-InvestorLetterlopaz777No ratings yet

- AFE-7-IFI International Financial Market: Student NumberDocument14 pagesAFE-7-IFI International Financial Market: Student NumberPratik BasakNo ratings yet

- Artical - Fund Trend ARTICAL - FUND TRENDSsDocument7 pagesArtical - Fund Trend ARTICAL - FUND TRENDSsharshal_gharatNo ratings yet

- Annual Report DreyfusDocument44 pagesAnnual Report DreyfusAlfieNo ratings yet

- Third Point Q2'09 Investor LetterDocument8 pagesThird Point Q2'09 Investor Lettermarketfolly.com100% (1)

- SG Allianz Income and Growth Fundcommentary enDocument4 pagesSG Allianz Income and Growth Fundcommentary enD TanNo ratings yet

- QMU Underperformance in Fixed Income Markets IFS FINAL 3.22.12 ADADocument3 pagesQMU Underperformance in Fixed Income Markets IFS FINAL 3.22.12 ADAPaulo AraujoNo ratings yet

- Mutual Fund Performance - An Empirical StudyDocument10 pagesMutual Fund Performance - An Empirical StudyAmeya ThakurNo ratings yet

- 2013 q2 Crescent Commentary Steve RomickDocument16 pages2013 q2 Crescent Commentary Steve RomickCanadianValueNo ratings yet

- Jif - Final Report - Af07Document27 pagesJif - Final Report - Af07Thu ThuNo ratings yet

- Hedge Fund Primer Vanguard)Document24 pagesHedge Fund Primer Vanguard)Lee BellNo ratings yet

- Empower July 2011Document74 pagesEmpower July 2011Priyanka AroraNo ratings yet

- Mi Bill Eigen Mid Year Outlook1Document6 pagesMi Bill Eigen Mid Year Outlook1nievinnyNo ratings yet

- Brookfield Asset Management - "Real Assets, The New Essential"Document23 pagesBrookfield Asset Management - "Real Assets, The New Essential"Equicapita Income TrustNo ratings yet

- Absolute Return Investing Strategies PDFDocument8 pagesAbsolute Return Investing Strategies PDFswopguruNo ratings yet

- Third Point Q109 LetterDocument4 pagesThird Point Q109 LetterZerohedgeNo ratings yet

- ZacksInvestmentResearchInc ZacksMarketStrategy Mar 05 2021Document85 pagesZacksInvestmentResearchInc ZacksMarketStrategy Mar 05 2021Dylan AdrianNo ratings yet

- Ten Investment Convictions For H2 2023Document5 pagesTen Investment Convictions For H2 2023blkjack8No ratings yet

- Executive SummaryDocument6 pagesExecutive SummaryhowellstechNo ratings yet

- Franklin: Global Equity FundDocument64 pagesFranklin: Global Equity FundPraveen KNNo ratings yet

- Fund SummaryDocument6 pagesFund SummaryhowellstechNo ratings yet

- Annual Report Avenue CapitalDocument44 pagesAnnual Report Avenue CapitalJoel CintrónNo ratings yet

- Equity Strategy: The 5 Top Picks For FebruaryDocument26 pagesEquity Strategy: The 5 Top Picks For Februarymwrolim_01No ratings yet

- ING Trups DiagramDocument5 pagesING Trups DiagramhungrymonsterNo ratings yet

- The Global Cost and Availability of Capital: QuestionsDocument7 pagesThe Global Cost and Availability of Capital: QuestionsluckybellaNo ratings yet

- The GIC Weekly Update November 2015Document12 pagesThe GIC Weekly Update November 2015John MathiasNo ratings yet

- Nalysis Of: Third Time's The CharmDocument47 pagesNalysis Of: Third Time's The CharmUmair ChishtiNo ratings yet

- Hedge Fund Business PlanDocument22 pagesHedge Fund Business Planjdchandi123No ratings yet

- Ar Retail ST BondDocument40 pagesAr Retail ST BondVoiture GermanNo ratings yet

- Why Real Yields Matter - Pictet Asset ManagementDocument7 pagesWhy Real Yields Matter - Pictet Asset ManagementLOKE SENG ONNNo ratings yet

- IDFC Emergin Businesses NFODocument5 pagesIDFC Emergin Businesses NFOfinancialbondingNo ratings yet

- Legg Mason (LM) : Adding To Best Ideas On The Long SideDocument14 pagesLegg Mason (LM) : Adding To Best Ideas On The Long SideJonathanNo ratings yet

- Glide Path and Dynamic Asset Allocation of Target Date FundsDocument26 pagesGlide Path and Dynamic Asset Allocation of Target Date FundsChrabąszczWacławNo ratings yet

- GI Report February 2012Document3 pagesGI Report February 2012Bill HallmanNo ratings yet

- Fund SummaryDocument6 pagesFund SummaryhowellstechNo ratings yet

- Principal Protected Investments: Structured Investments Solution SeriesDocument8 pagesPrincipal Protected Investments: Structured Investments Solution SeriessonystdNo ratings yet

- Institute of Actuaries of India: Indicative SolutionDocument12 pagesInstitute of Actuaries of India: Indicative SolutionYogeshAgrawalNo ratings yet

- Investment Policy StatementDocument14 pagesInvestment Policy StatementHamis Rabiam MagundaNo ratings yet

- The Global Cost and Availability of Capital: QuestionsDocument7 pagesThe Global Cost and Availability of Capital: QuestionsluckybellaNo ratings yet

- PIMCO European Perspectives Bosomworth April2013Document8 pagesPIMCO European Perspectives Bosomworth April2013alphathesisNo ratings yet

- Qau 1203Document15 pagesQau 1203TBP_Think_TankNo ratings yet

- PE - Norway Pension Fund - Evaluatin Investments in PE (Ver P. 32)Document154 pagesPE - Norway Pension Fund - Evaluatin Investments in PE (Ver P. 32)Danilo Just SoaresNo ratings yet

- Review of The Second Quarter 2015: Investment NoteDocument3 pagesReview of The Second Quarter 2015: Investment NoteStephanieNo ratings yet

- CI Signature Dividend FundDocument2 pagesCI Signature Dividend Fundkirby333No ratings yet

- A Roadmap For Including Privates in An Asset Allocation 1684331189Document6 pagesA Roadmap For Including Privates in An Asset Allocation 1684331189風雲造天No ratings yet

- ICMAniacs Report Final (In Need of Finishing Touches)Document19 pagesICMAniacs Report Final (In Need of Finishing Touches)George Stuart CottonNo ratings yet

- Third Point Q1'09 Investor LetterDocument4 pagesThird Point Q1'09 Investor LetterDealBook100% (2)

- DSP BlackRock US Flexible Equity Fund - NFO Application From With KIM FormDocument16 pagesDSP BlackRock US Flexible Equity Fund - NFO Application From With KIM FormprajnacapiralNo ratings yet

- (LGT) 20210316 - DRU - Sector RotationDocument3 pages(LGT) 20210316 - DRU - Sector RotationRuehYinn YapNo ratings yet

- Running Head: GLOBAL INVESTMENTDocument4 pagesRunning Head: GLOBAL INVESTMENTCarlos AlphonceNo ratings yet

- Yv 0 Fe Ir 4Document38 pagesYv 0 Fe Ir 4StacyLoiNo ratings yet

- Roro Factor InvestingDocument9 pagesRoro Factor Investingsunny.hyxNo ratings yet

- Global Cost and Availability of Capital: QuestionsDocument5 pagesGlobal Cost and Availability of Capital: QuestionsCtnuralisyaNo ratings yet

- The Sector Strategist: Using New Asset Allocation Techniques to Reduce Risk and Improve Investment ReturnsFrom EverandThe Sector Strategist: Using New Asset Allocation Techniques to Reduce Risk and Improve Investment ReturnsRating: 4 out of 5 stars4/5 (1)

- Financial Markets Fundamentals: Why, how and what Products are traded on Financial Markets. Understand the Emotions that drive TradingFrom EverandFinancial Markets Fundamentals: Why, how and what Products are traded on Financial Markets. Understand the Emotions that drive TradingNo ratings yet

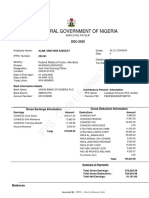

- IPPIS - Oracle E-Business Suite: Federal Government of NigeriaDocument1 pageIPPIS - Oracle E-Business Suite: Federal Government of NigeriaAlimi kehinde100% (1)

- Credit by Debraj RayDocument35 pagesCredit by Debraj RayRigzin YangdolNo ratings yet

- NHTM - BTDocument16 pagesNHTM - BTNguyễn Hải Thanh100% (1)

- JP Morgan Jargon BusterDocument24 pagesJP Morgan Jargon BusterzowpowNo ratings yet

- Presentation (1) PPTDocument15 pagesPresentation (1) PPTPrernaNo ratings yet

- FABM2 - Q1 - V2a Page 59 69Document11 pagesFABM2 - Q1 - V2a Page 59 69joiNo ratings yet

- D14Document12 pagesD14YaniNo ratings yet

- Chapter 1: The Investment SettingDocument54 pagesChapter 1: The Investment Settingcharlie tunaNo ratings yet

- Impact of Marginal Costing On Financial Performance of Manufacturing Firms in Nairobi CountyDocument13 pagesImpact of Marginal Costing On Financial Performance of Manufacturing Firms in Nairobi Countykipngetich392No ratings yet

- Iving HE AY: Work Less, Worry Less, Succeed More, Enjoy MoreDocument9 pagesIving HE AY: Work Less, Worry Less, Succeed More, Enjoy MoreWarren BuffetNo ratings yet

- Proposal For Remittance....Document18 pagesProposal For Remittance....Simon ShresthaNo ratings yet

- Block 2Document102 pagesBlock 2msk_1407No ratings yet

- 2 Financial Markets and Interest RatesDocument21 pages2 Financial Markets and Interest Ratesadib nassarNo ratings yet

- Blueprint FICO JAiDocument67 pagesBlueprint FICO JAiShyamprasadreddy KumbhamNo ratings yet

- CbloDocument6 pagesCbloPojigiNo ratings yet

- Chapter 19 Mutual FundsDocument20 pagesChapter 19 Mutual FundsdurgaselvamNo ratings yet

- Make Money Fast With Cash Fiesta New VersionDocument10 pagesMake Money Fast With Cash Fiesta New VersionClarity VnNo ratings yet

- Chapter Three PPE Copy 2Document15 pagesChapter Three PPE Copy 2nachmarket30No ratings yet

- Bond ValuationDocument50 pagesBond Valuationrenu3rdjanNo ratings yet

- Americandownload b2 Extra Tasks and KeyDocument12 pagesAmericandownload b2 Extra Tasks and Keyangelos1apostolidisNo ratings yet

- Launch Jasper ReportDocument1 pageLaunch Jasper ReportElias Abubeker AhmedNo ratings yet

- Business Valuation MethodsDocument10 pagesBusiness Valuation Methodsraj28_999No ratings yet

- Full Report MIFSDocument22 pagesFull Report MIFSWeiXin Yeo100% (1)

- Factors Affecting Valuation of SharesDocument6 pagesFactors Affecting Valuation of SharesSneha ChavanNo ratings yet

- Issue OF SHARE CAPITAL PRACTISE QUESTIONSDocument5 pagesIssue OF SHARE CAPITAL PRACTISE QUESTIONSCSCharlie GahlotNo ratings yet

- Check-In and Check-Out ScriptDocument4 pagesCheck-In and Check-Out ScriptEunice AlboNo ratings yet