Download as pdf or txt

You might also like

- 4 FullDocument31 pages4 Fullapi-217362413No ratings yet

- Cockfighting OrdinanceDocument4 pagesCockfighting OrdinanceEden Celestino Sarabia Cacho100% (1)

- NWRB - Fees and ChargesDocument2 pagesNWRB - Fees and ChargesRALSTON TUYOKNo ratings yet

- SI 2014-56 - Mining (General) (Amendment) Regulations, 2014 (No. 18)Document8 pagesSI 2014-56 - Mining (General) (Amendment) Regulations, 2014 (No. 18)ronaldpgonyeNo ratings yet

- Permits PDFDocument12 pagesPermits PDFSterlingNo ratings yet

- Venue Hire Rates 2022 2023Document5 pagesVenue Hire Rates 2022 2023Zatus Sofwa Abdul RahmanNo ratings yet

- AFEcosts Horizontal PDFDocument1 pageAFEcosts Horizontal PDF56962645No ratings yet

- Cost CalculatorDocument4 pagesCost CalculatorVipin GuptaNo ratings yet

- SI 2021-044 Mining (General) (Amendment) Fees Regulations, 2020 (No. 24) - 0Document8 pagesSI 2021-044 Mining (General) (Amendment) Fees Regulations, 2020 (No. 24) - 0JV MortiserNo ratings yet

- Equipment RentalDocument2 pagesEquipment RentalMaricar TelanNo ratings yet

- Mining Fees Review DraftDocument15 pagesMining Fees Review DraftWhisper Davidson ZanamweNo ratings yet

- MunlocalchargesDocument2 pagesMunlocalchargesrezakurnwNo ratings yet

- Mining Tributary Regulations, 2016 (No. 19) - 0Document10 pagesMining Tributary Regulations, 2016 (No. 19) - 0Nezzy SimukayiNo ratings yet

- LPG Depot Statutory FeesDocument3 pagesLPG Depot Statutory Feessampeters.infoNo ratings yet

- Addfield Quotation TB-HB 1300 - SSSC - DUBAIDocument12 pagesAddfield Quotation TB-HB 1300 - SSSC - DUBAIMohammed Ahmed NasherNo ratings yet

- Mining Briefing - Mining Regulations June 2018Document6 pagesMining Briefing - Mining Regulations June 2018Anonymous iFZbkNwNo ratings yet

- Nep Za TariffDocument3 pagesNep Za TariffAnonymous 9ZakghkbiYNo ratings yet

- 1.0 LPG Depot Statutory Fees: S/N Milestone Fees (NGN)Document8 pages1.0 LPG Depot Statutory Fees: S/N Milestone Fees (NGN)Ismail AdebiyiNo ratings yet

- ZW Government Gazette Dated 2021 02 23 No 26Document13 pagesZW Government Gazette Dated 2021 02 23 No 26JV MortiserNo ratings yet

- 1643866512121Document3 pages1643866512121S Anjallee KumarNo ratings yet

- Property, Plant, and Equipment: Acquisition and DisposalDocument49 pagesProperty, Plant, and Equipment: Acquisition and Disposalasep_efendhiNo ratings yet

- S.I. 95 of 2020 Statutory Instrument 95 of 2020. Mining (General) (Amendment) Regulations, 2020 (No. 23)Document11 pagesS.I. 95 of 2020 Statutory Instrument 95 of 2020. Mining (General) (Amendment) Regulations, 2020 (No. 23)kayla dzwairoNo ratings yet

- Import Local Charges - 6-06-24Document4 pagesImport Local Charges - 6-06-24Arvind ChaudharyNo ratings yet

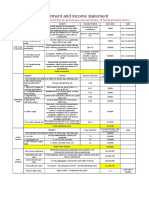

- AIMIX GROUP Investment and Income StatementDocument1 pageAIMIX GROUP Investment and Income StatementJoManadoNo ratings yet

- Batas Pambansa 265Document1 pageBatas Pambansa 265JubsNo ratings yet

- Relevent Cost / Factors For Decision MakingDocument4 pagesRelevent Cost / Factors For Decision MakingHassan KhanNo ratings yet

- Quotation JAW+JAW+CONEDocument21 pagesQuotation JAW+JAW+CONESatria PagiNo ratings yet

- Laguna Lake Development Authority BR 224Document4 pagesLaguna Lake Development Authority BR 224Roselyn Antonio TabundaNo ratings yet

- Building Dept Fee ScheduleDocument2 pagesBuilding Dept Fee SchedulerobotsNo ratings yet

- Problem 15 - 1 Books of German CompanyDocument3 pagesProblem 15 - 1 Books of German CompanyCOCO IMNIDANo ratings yet

- RMO - NO. 9-2018 - DigestDocument5 pagesRMO - NO. 9-2018 - DigestCliff DaquioagNo ratings yet

- Date Particulars DR CRDocument6 pagesDate Particulars DR CRRyll BedasNo ratings yet

- AP-5903 - PPE & IntangiblesDocument8 pagesAP-5903 - PPE & IntangiblesDreiu EsmeleNo ratings yet

- Hall Rent - Updated f1Document2 pagesHall Rent - Updated f1Bonanza & Impetus Management LimitedNo ratings yet

- All India Import Local Charges - 2023 - 05Document4 pagesAll India Import Local Charges - 2023 - 05Purushotam TapariyaNo ratings yet

- SI 2021-101 Electricity (Licensing) (Amendment) Regulations, 2021 (No. 2) PDFDocument4 pagesSI 2021-101 Electricity (Licensing) (Amendment) Regulations, 2021 (No. 2) PDFzie conradNo ratings yet

- August 22 Rental QuotationDocument2 pagesAugust 22 Rental QuotationMaricar TelanNo ratings yet

- Quotation GeneralDocument3 pagesQuotation Generalapriansyah.fredy88No ratings yet

- Accounts Chapter-Wise Test 5 (Suggested Answers)Document7 pagesAccounts Chapter-Wise Test 5 (Suggested Answers)Shweta BhadauriaNo ratings yet

- GCMDocument22 pagesGCMIda MaharaniNo ratings yet

- Ship Registration WebsiteDocument17 pagesShip Registration Websiteapi-722943394No ratings yet

- Price List Aug 2023 2BHK 3bhkDocument2 pagesPrice List Aug 2023 2BHK 3bhkArvin DabasNo ratings yet

- Cardholder Agreement MITCDocument53 pagesCardholder Agreement MITCVishal PandeyNo ratings yet

- Auditing ActivityDocument4 pagesAuditing ActivityPrincessNo ratings yet

- S.I. 40 of 2022 Mining (General) (Amendment) Regulations, 2022 (No. 27) ImpoDocument6 pagesS.I. 40 of 2022 Mining (General) (Amendment) Regulations, 2022 (No. 27) ImpochigarasifelaniNo ratings yet

- Assignment-N02-Engr-2120 Hupana Salaysay ToledoDocument7 pagesAssignment-N02-Engr-2120 Hupana Salaysay ToledoPRINCE DAVID ART TOLEDONo ratings yet

- Assessment Rates Charges 2022 2023Document2 pagesAssessment Rates Charges 2022 2023Sneha MondalNo ratings yet

- Sale and LeasebackDocument10 pagesSale and LeasebackShinny Jewel VingnoNo ratings yet

- Assignment BDocument9 pagesAssignment BXDkillua45No ratings yet

- RCL IHC更新Document6 pagesRCL IHC更新CivicNo ratings yet

- Zambian Tax SystemDocument3 pagesZambian Tax SystemFanuel NjobvuNo ratings yet

- Depletion IFRS Vs ASPE Simple DemoDocument4 pagesDepletion IFRS Vs ASPE Simple DemonishitNo ratings yet

- Panama Marine Authority Administration Fees: Seafarers' LicencesDocument5 pagesPanama Marine Authority Administration Fees: Seafarers' Licencessaeed ghafooriNo ratings yet

- Assigment 1Document5 pagesAssigment 1Born 99No ratings yet

- LearningsDocument4 pagesLearningsPramod SakriNo ratings yet

- Circular: TelecommunicationDocument4 pagesCircular: TelecommunicationXiadrfNo ratings yet

- Mining Ver3Document14 pagesMining Ver3dominic.penielNo ratings yet

- MC 2015 05Document28 pagesMC 2015 05gregNo ratings yet

- Bygging India Limited: Sheet II - Monthly Fund Requirement - Site Expenses Month: MAY-22 Site:-Npgcl, NabinagarDocument2 pagesBygging India Limited: Sheet II - Monthly Fund Requirement - Site Expenses Month: MAY-22 Site:-Npgcl, NabinagarShahdeoNo ratings yet

- Designing Our Future: Sustainable LandscapesDocument2 pagesDesigning Our Future: Sustainable LandscapesMelissa NdayikengurukiyeNo ratings yet

- Case Study:'Tunis, Tunisia Rehabilitation of The Hafsia QuarterDocument48 pagesCase Study:'Tunis, Tunisia Rehabilitation of The Hafsia QuarterMelissa NdayikengurukiyeNo ratings yet

- 5167955Document120 pages5167955Melissa NdayikengurukiyeNo ratings yet

- Ecolodge Design PrinciplesDocument1 pageEcolodge Design PrinciplesMelissa NdayikengurukiyeNo ratings yet

- BalkanMine 4Document8 pagesBalkanMine 4PéterRápliNo ratings yet

- Minerals by @captainsdugoutDocument68 pagesMinerals by @captainsdugoutAdinath RohamareNo ratings yet

- Renewable and Sustainable Energy Reviews: Pavan Kumar Naraharisetti, Tze Yuen Yeo, Jie Bu TDocument14 pagesRenewable and Sustainable Energy Reviews: Pavan Kumar Naraharisetti, Tze Yuen Yeo, Jie Bu TclaudiacarranzafNo ratings yet

- Africas Top CompaniesDocument5 pagesAfricas Top CompaniesRamchanderNo ratings yet

- The Disappearance of Harold-V4Document18 pagesThe Disappearance of Harold-V4Doug100% (2)

- Annexure 4 - Pakistan Environmental Protection Agency (IEE and EIA) RegulationsDocument11 pagesAnnexure 4 - Pakistan Environmental Protection Agency (IEE and EIA) RegulationsNaeem U. KhanNo ratings yet

- Born Horst Barron FTDocument18 pagesBorn Horst Barron FTAlma Cristina Del Castillo LondonoNo ratings yet

- Cover LetterDocument1 pageCover LetterKumardasNsNo ratings yet

- Development Area Profiles Williamsfield DA 8-1: Figure DA8-1 View of The Center of WilliamsfieldDocument42 pagesDevelopment Area Profiles Williamsfield DA 8-1: Figure DA8-1 View of The Center of WilliamsfieldGail HoadNo ratings yet

- MongoliaDocument18 pagesMongoliaGegedukNo ratings yet

- 2ND Term S3 GeographyDocument9 pages2ND Term S3 GeographyFaith OzuahNo ratings yet

- CV - Hardi Kepler SDocument7 pagesCV - Hardi Kepler SduditharyantoNo ratings yet

- La Bugal-B'laan Tribal Assn. v. DENRDocument5 pagesLa Bugal-B'laan Tribal Assn. v. DENRtemporiariNo ratings yet

- Ore Reserve Estimation of Saprolite Nickel Using IDocument7 pagesOre Reserve Estimation of Saprolite Nickel Using IJoshua Rey SapurasNo ratings yet

- SAMRASS CodebookDocument98 pagesSAMRASS Codebookbenny1004100% (1)

- The Fdi Report 2023Document32 pagesThe Fdi Report 2023Hắc MiêuNo ratings yet

- PAPER1 Minetech11Document10 pagesPAPER1 Minetech11SushantNo ratings yet

- Severstal (Main)Document18 pagesSeverstal (Main)wdsNo ratings yet

- Project To Create and Operate A Service Company For The Artisanal Mining Industry in NicaraguaDocument11 pagesProject To Create and Operate A Service Company For The Artisanal Mining Industry in Nicaraguaalfredog07No ratings yet

- Sgs Min tp2007 01 Grinding Circuit Design Using A Geometallurgical ApproachDocument10 pagesSgs Min tp2007 01 Grinding Circuit Design Using A Geometallurgical ApproachJaime Magno Gutierrez RamirezNo ratings yet

- MPT - 2 in COR 008: Physical Properties Chemical PropertiesDocument2 pagesMPT - 2 in COR 008: Physical Properties Chemical PropertiesJana Lira BautistaNo ratings yet

- Philippine Mining Act of 1995 (Ra 7942 PDFDocument32 pagesPhilippine Mining Act of 1995 (Ra 7942 PDFEdnalynTrixiaNo ratings yet

- NMDCDocument11 pagesNMDCsmruti katwaleNo ratings yet

- GeoResources Journal 4 2017Document52 pagesGeoResources Journal 4 2017ansariNo ratings yet

- Minerals: Properties and Types (Pre-Reading)Document13 pagesMinerals: Properties and Types (Pre-Reading)NIKKI GRACE MAGDALINo ratings yet

- ALTA Short Course Outline Sample Pages Copper SX EWDocument7 pagesALTA Short Course Outline Sample Pages Copper SX EWHamed PiriNo ratings yet

- DGMS Circular - 5 PDFDocument10 pagesDGMS Circular - 5 PDFgajendraNo ratings yet

- MEA Research Projects Review 2012 PDFDocument94 pagesMEA Research Projects Review 2012 PDFZhengLuNo ratings yet

- Bijahan Coal BlockDocument2 pagesBijahan Coal BlockPryas JainNo ratings yet