IJNRD2212031

IJNRD2212031

You might also like

- ICAZ Guidance On Code of Ethics and Other Professional Conduct RequiremeDocument6 pagesICAZ Guidance On Code of Ethics and Other Professional Conduct RequiremePrimrose NgoshiNo ratings yet

- MCQ's On EconomicsDocument43 pagesMCQ's On EconomicsDevraj Mishra100% (2)

- G I O G: Eographical Ndications F OodsDocument41 pagesG I O G: Eographical Ndications F Oodsgurjot85No ratings yet

- Chapter 10: Accounting Cycle of A Merchandising Business (FAR By: Millan)Document16 pagesChapter 10: Accounting Cycle of A Merchandising Business (FAR By: Millan)Gennelyn Lairise RiveraNo ratings yet

- CH 6 TestDocument6 pagesCH 6 TestChloe Simmons0% (1)

- AnswersDocument8 pagesAnswersRajesh BazadNo ratings yet

- Role of SEBI As Regulator in Maintaining Corporate Governance Standards in IndiaDocument4 pagesRole of SEBI As Regulator in Maintaining Corporate Governance Standards in Indiasourav kumar rayNo ratings yet

- Becg Unit-4.Document12 pagesBecg Unit-4.Bhaskaran Balamurali100% (2)

- Project On Corporate GovernanceDocument28 pagesProject On Corporate GovernanceRashmiNo ratings yet

- Certificate Course On Corporate GovernanceDocument7 pagesCertificate Course On Corporate Governancedeepak singhalNo ratings yet

- Corporate Governance in IndiaDocument22 pagesCorporate Governance in Indiaaishwaryasamanta0% (1)

- Corporate Governance & The Director (As Provided Undercompanies Act 2013)Document13 pagesCorporate Governance & The Director (As Provided Undercompanies Act 2013)Parth BindalNo ratings yet

- Corporate Governance May Be Defined As FollowsDocument7 pagesCorporate Governance May Be Defined As Followsbarkha chandnaNo ratings yet

- CSR Corporate Governance ReportDocument7 pagesCSR Corporate Governance ReportFariba NabaviNo ratings yet

- Saurabh Singh: The Clause 49 of Listing Agreement With Pertinence To Corporate Governance in IndiaDocument9 pagesSaurabh Singh: The Clause 49 of Listing Agreement With Pertinence To Corporate Governance in IndiaSaurabh singhNo ratings yet

- Project Report On Corporate GovernanceDocument39 pagesProject Report On Corporate GovernanceRahul MittalNo ratings yet

- Corporate Governance in India - Clause 49 of Listing AgreementDocument9 pagesCorporate Governance in India - Clause 49 of Listing AgreementSanjay DessaiNo ratings yet

- C P R C G N I: Onsultative Aper On Eview of Orporate Overnance Orms in NdiaDocument54 pagesC P R C G N I: Onsultative Aper On Eview of Orporate Overnance Orms in NdiaPradyoth C JohnNo ratings yet

- 8141principles of Corporate Governance - OECD Annotations and Indian ConnotationsDocument8 pages8141principles of Corporate Governance - OECD Annotations and Indian Connotations2nablsNo ratings yet

- JLSS Vol 2 No. 2 1Document6 pagesJLSS Vol 2 No. 2 1Aftab TabasamNo ratings yet

- Clause 49 Listing AgreementDocument10 pagesClause 49 Listing AgreementAarti MaanNo ratings yet

- Corporate Governance in India Comany LawDocument6 pagesCorporate Governance in India Comany LawRajeNo ratings yet

- Chapter 2 Code of Best PracticesDocument28 pagesChapter 2 Code of Best PracticesUmAli AlsalmanNo ratings yet

- Role of Sebi in Corporate Governance and Finance - (Essay Example), 2973 Words GradesFixerDocument10 pagesRole of Sebi in Corporate Governance and Finance - (Essay Example), 2973 Words GradesFixerAbid ZaidiNo ratings yet

- 22 - Companies Act 2013 To Improve Corporate GovernanceDocument6 pages22 - Companies Act 2013 To Improve Corporate GovernanceImpact JournalsNo ratings yet

- Regulatory Framework For Corporate Governance in India M COM II 17-4Document9 pagesRegulatory Framework For Corporate Governance in India M COM II 17-4Monika ShaileshNo ratings yet

- Corporate GovernanceDocument7 pagesCorporate GovernanceWilliam Masterson ShahNo ratings yet

- Code of Corporate Governance FAQ'sDocument12 pagesCode of Corporate Governance FAQ'sSyed Shujat AliNo ratings yet

- Piyali Mitra - Content Submission (The Connection Between CSR and Corporate Governance-Conceptually Analysing The Concepts)Document6 pagesPiyali Mitra - Content Submission (The Connection Between CSR and Corporate Governance-Conceptually Analysing The Concepts)Piyali MitraNo ratings yet

- Desirable Corporate Governance: A CodeDocument14 pagesDesirable Corporate Governance: A CodeRahul MohanNo ratings yet

- DeliveryDocument6 pagesDeliveryVenkata Sai Varun KanuparthiNo ratings yet

- Chairman's Message: Frequently Asked Questions On The Code of Corporate Governance (Revised)Document26 pagesChairman's Message: Frequently Asked Questions On The Code of Corporate Governance (Revised)Faizan MotiwalaNo ratings yet

- Corporate Governance in Nigeria - Prospects and ProblemsDocument12 pagesCorporate Governance in Nigeria - Prospects and Problemscoliuo500100% (1)

- Corporate Regulations: Bachelor of CommerceDocument110 pagesCorporate Regulations: Bachelor of CommerceAleena BabuNo ratings yet

- Corporate Governance Comparison ModifiedDocument14 pagesCorporate Governance Comparison ModifiedTanjina RahmanNo ratings yet

- Answer Sheet Corporate Law 2 cl2Document15 pagesAnswer Sheet Corporate Law 2 cl2Muskan KhatriNo ratings yet

- Bba Corporate RegulationsDocument113 pagesBba Corporate Regulationsnadeemvp111No ratings yet

- CodeOfCorporateGovernance 2012 AmendedJuly2014Document41 pagesCodeOfCorporateGovernance 2012 AmendedJuly2014Aftab TabasamNo ratings yet

- Listed Companies COCG 2019Document57 pagesListed Companies COCG 2019Muzammil LiaquatNo ratings yet

- Irctc - 635Document7 pagesIrctc - 635Dhanush KarthikNo ratings yet

- Corporate GovernanceDocument8 pagesCorporate GovernanceAnooj SrivastavaNo ratings yet

- 4.Management-Legal Aspects of Corporate Governance For IT Companies in IndiaDocument8 pages4.Management-Legal Aspects of Corporate Governance For IT Companies in IndiaImpact JournalsNo ratings yet

- Corporate GovernanceDocument19 pagesCorporate GovernanceRajesh PaulNo ratings yet

- Assignment - CG & BEDocument4 pagesAssignment - CG & BErajesh laddhaNo ratings yet

- Corporate Governance in India: A Legal Analysis: Prabhash Dalei, Paridhi Tulsyan and Shikhar MaraviDocument3 pagesCorporate Governance in India: A Legal Analysis: Prabhash Dalei, Paridhi Tulsyan and Shikhar MaraviManoj DhamiNo ratings yet

- PDF Document E1FC588E4444 1Document8 pagesPDF Document E1FC588E4444 1sudeepNo ratings yet

- Corporate Govern Hardcopy - ComparisonDocument58 pagesCorporate Govern Hardcopy - ComparisonAnkit PandyaNo ratings yet

- Corporate Governance FrameworkDocument4 pagesCorporate Governance Frameworkvivienne mimiNo ratings yet

- Corporate Governance in IndiaDocument7 pagesCorporate Governance in Indiaayushsinghal124No ratings yet

- Unit 3.3 - Future of CGDocument17 pagesUnit 3.3 - Future of CGNithyasri MuthuNo ratings yet

- (CG) ComparisonDocument9 pages(CG) ComparisonKatsuhiko TangNo ratings yet

- Introduction of Corporate GovernanceDocument8 pagesIntroduction of Corporate GovernanceHasanur RaselNo ratings yet

- The Malaysian Code On Corporate Governance 2017: Client Update: MalaysiaDocument6 pagesThe Malaysian Code On Corporate Governance 2017: Client Update: MalaysiaIntan NurdianaNo ratings yet

- The Companies Act 2012 Salient Features DBR 2015Document4 pagesThe Companies Act 2012 Salient Features DBR 2015Day VidNo ratings yet

- 01 - Corporate Governance - CONCEPTUAL FRAMEWORK OF CORPORATE GOVERNANCEDocument109 pages01 - Corporate Governance - CONCEPTUAL FRAMEWORK OF CORPORATE GOVERNANCEVij88888No ratings yet

- UK Corporate Governance CodeDocument6 pagesUK Corporate Governance CodeNabil Ahmed KhanNo ratings yet

- Corporate Governance Short NotesDocument8 pagesCorporate Governance Short NotesVivekNo ratings yet

- CSR and CG BeDocument3 pagesCSR and CG BeDondapati Raga Sravya ReddyNo ratings yet

- 18 Exposure DraftDocument15 pages18 Exposure DraftVaishali GaggarNo ratings yet

- FM 2 Group 7Document19 pagesFM 2 Group 7Payal PatelNo ratings yet

- Group Assignment Company's Act, 2013 Was Modified To Enhance Corporate Governance in IndiaDocument11 pagesGroup Assignment Company's Act, 2013 Was Modified To Enhance Corporate Governance in IndiaANKITA GOOMERNo ratings yet

- Categories of Software MaintenanceDocument24 pagesCategories of Software Maintenancepramodtiwari1989No ratings yet

- Internship On Harish Food ZoneDocument17 pagesInternship On Harish Food ZoneSwethaNo ratings yet

- Sri Lankan Bank Account ComparisonDocument18 pagesSri Lankan Bank Account ComparisonVaruni_Gunawardana100% (1)

- Itsm Inter MCQ - UncramDocument3 pagesItsm Inter MCQ - UncramKARTHIKNo ratings yet

- Income Based Valuation Discounted Cash Flows Group 2Document90 pagesIncome Based Valuation Discounted Cash Flows Group 2natalie clyde mates100% (1)

- DOH Manual AcronymsDocument14 pagesDOH Manual AcronymsJohn Oliver GuiangNo ratings yet

- Graphic Designing: by Hajie RosarioDocument9 pagesGraphic Designing: by Hajie RosarioHajie RosarioNo ratings yet

- Common Business Transactions Using The Rules of Debit and CreditDocument9 pagesCommon Business Transactions Using The Rules of Debit and CreditSHIERY MAE FALCONITINNo ratings yet

- SMPG Corporate Actions Events Templates - SR2021: DisclaimerDocument233 pagesSMPG Corporate Actions Events Templates - SR2021: Disclaimershivank tiwariNo ratings yet

- Market Identification Process: Stage 1 Stage 3 Stage 2Document28 pagesMarket Identification Process: Stage 1 Stage 3 Stage 2Leslie Salvo Jr.100% (1)

- Installment Promissory Note 1Document1 pageInstallment Promissory Note 1api-385482345No ratings yet

- Exercises Chapter 04Document23 pagesExercises Chapter 04vintcs181892No ratings yet

- Eloisa S. Gavilan BSBA-HR2nd YrDocument2 pagesEloisa S. Gavilan BSBA-HR2nd YrGoldengate CollegesNo ratings yet

- A New Day For SustainabilityDocument9 pagesA New Day For SustainabilityswaraNo ratings yet

- Request NDT Welder TestDocument1 pageRequest NDT Welder TestFerdie OSNo ratings yet

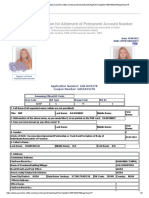

- Form 49A Application For Allotment of Permanent Account NumberDocument2 pagesForm 49A Application For Allotment of Permanent Account NumberRAHUL TIWARINo ratings yet

- Environmental Analysis 2Document33 pagesEnvironmental Analysis 2Nitesh BoutaniveNo ratings yet

- PlanDocument120 pagesPlantariq19870% (1)

- Accounting Controls and Bureaucratic Strategies in Municipal GovernmentDocument24 pagesAccounting Controls and Bureaucratic Strategies in Municipal GovernmentRian LiraldoNo ratings yet

- Product: Marketing Mix For NvidiaDocument8 pagesProduct: Marketing Mix For NvidiaMohammed QatariNo ratings yet

- B0175 Dsday2 Atlstmts - Linex.dsstmts - 4408 - Ddastmts 04212020Document1 pageB0175 Dsday2 Atlstmts - Linex.dsstmts - 4408 - Ddastmts 04212020Coughman MattNo ratings yet

- Circular W.E.F 19th May'22Document224 pagesCircular W.E.F 19th May'22Mohit MohataNo ratings yet

- ProjcetbovontosDocument59 pagesProjcetbovontosjhkljhkNo ratings yet

- Insidethecircle TradeModelDocument25 pagesInsidethecircle TradeModelArif AgustianNo ratings yet

- Keya Cosmetics LTDDocument2 pagesKeya Cosmetics LTDTanveer HasanNo ratings yet

- The Odisha Factories Rules 1950Document297 pagesThe Odisha Factories Rules 1950Lalatendu Mahanta0% (1)

Download as pdf or txt

You might also like

- ICAZ Guidance On Code of Ethics and Other Professional Conduct RequiremeDocument6 pagesICAZ Guidance On Code of Ethics and Other Professional Conduct RequiremePrimrose NgoshiNo ratings yet

- MCQ's On EconomicsDocument43 pagesMCQ's On EconomicsDevraj Mishra100% (2)

- G I O G: Eographical Ndications F OodsDocument41 pagesG I O G: Eographical Ndications F Oodsgurjot85No ratings yet

- Chapter 10: Accounting Cycle of A Merchandising Business (FAR By: Millan)Document16 pagesChapter 10: Accounting Cycle of A Merchandising Business (FAR By: Millan)Gennelyn Lairise RiveraNo ratings yet

- CH 6 TestDocument6 pagesCH 6 TestChloe Simmons0% (1)

- AnswersDocument8 pagesAnswersRajesh BazadNo ratings yet

- Role of SEBI As Regulator in Maintaining Corporate Governance Standards in IndiaDocument4 pagesRole of SEBI As Regulator in Maintaining Corporate Governance Standards in Indiasourav kumar rayNo ratings yet

- Becg Unit-4.Document12 pagesBecg Unit-4.Bhaskaran Balamurali100% (2)

- Project On Corporate GovernanceDocument28 pagesProject On Corporate GovernanceRashmiNo ratings yet

- Certificate Course On Corporate GovernanceDocument7 pagesCertificate Course On Corporate Governancedeepak singhalNo ratings yet

- Corporate Governance in IndiaDocument22 pagesCorporate Governance in Indiaaishwaryasamanta0% (1)

- Corporate Governance & The Director (As Provided Undercompanies Act 2013)Document13 pagesCorporate Governance & The Director (As Provided Undercompanies Act 2013)Parth BindalNo ratings yet

- Corporate Governance May Be Defined As FollowsDocument7 pagesCorporate Governance May Be Defined As Followsbarkha chandnaNo ratings yet

- CSR Corporate Governance ReportDocument7 pagesCSR Corporate Governance ReportFariba NabaviNo ratings yet

- Saurabh Singh: The Clause 49 of Listing Agreement With Pertinence To Corporate Governance in IndiaDocument9 pagesSaurabh Singh: The Clause 49 of Listing Agreement With Pertinence To Corporate Governance in IndiaSaurabh singhNo ratings yet

- Project Report On Corporate GovernanceDocument39 pagesProject Report On Corporate GovernanceRahul MittalNo ratings yet

- Corporate Governance in India - Clause 49 of Listing AgreementDocument9 pagesCorporate Governance in India - Clause 49 of Listing AgreementSanjay DessaiNo ratings yet

- C P R C G N I: Onsultative Aper On Eview of Orporate Overnance Orms in NdiaDocument54 pagesC P R C G N I: Onsultative Aper On Eview of Orporate Overnance Orms in NdiaPradyoth C JohnNo ratings yet

- 8141principles of Corporate Governance - OECD Annotations and Indian ConnotationsDocument8 pages8141principles of Corporate Governance - OECD Annotations and Indian Connotations2nablsNo ratings yet

- JLSS Vol 2 No. 2 1Document6 pagesJLSS Vol 2 No. 2 1Aftab TabasamNo ratings yet

- Clause 49 Listing AgreementDocument10 pagesClause 49 Listing AgreementAarti MaanNo ratings yet

- Corporate Governance in India Comany LawDocument6 pagesCorporate Governance in India Comany LawRajeNo ratings yet

- Chapter 2 Code of Best PracticesDocument28 pagesChapter 2 Code of Best PracticesUmAli AlsalmanNo ratings yet

- Role of Sebi in Corporate Governance and Finance - (Essay Example), 2973 Words GradesFixerDocument10 pagesRole of Sebi in Corporate Governance and Finance - (Essay Example), 2973 Words GradesFixerAbid ZaidiNo ratings yet

- 22 - Companies Act 2013 To Improve Corporate GovernanceDocument6 pages22 - Companies Act 2013 To Improve Corporate GovernanceImpact JournalsNo ratings yet

- Regulatory Framework For Corporate Governance in India M COM II 17-4Document9 pagesRegulatory Framework For Corporate Governance in India M COM II 17-4Monika ShaileshNo ratings yet

- Corporate GovernanceDocument7 pagesCorporate GovernanceWilliam Masterson ShahNo ratings yet

- Code of Corporate Governance FAQ'sDocument12 pagesCode of Corporate Governance FAQ'sSyed Shujat AliNo ratings yet

- Piyali Mitra - Content Submission (The Connection Between CSR and Corporate Governance-Conceptually Analysing The Concepts)Document6 pagesPiyali Mitra - Content Submission (The Connection Between CSR and Corporate Governance-Conceptually Analysing The Concepts)Piyali MitraNo ratings yet

- Desirable Corporate Governance: A CodeDocument14 pagesDesirable Corporate Governance: A CodeRahul MohanNo ratings yet

- DeliveryDocument6 pagesDeliveryVenkata Sai Varun KanuparthiNo ratings yet

- Chairman's Message: Frequently Asked Questions On The Code of Corporate Governance (Revised)Document26 pagesChairman's Message: Frequently Asked Questions On The Code of Corporate Governance (Revised)Faizan MotiwalaNo ratings yet

- Corporate Governance in Nigeria - Prospects and ProblemsDocument12 pagesCorporate Governance in Nigeria - Prospects and Problemscoliuo500100% (1)

- Corporate Regulations: Bachelor of CommerceDocument110 pagesCorporate Regulations: Bachelor of CommerceAleena BabuNo ratings yet

- Corporate Governance Comparison ModifiedDocument14 pagesCorporate Governance Comparison ModifiedTanjina RahmanNo ratings yet

- Answer Sheet Corporate Law 2 cl2Document15 pagesAnswer Sheet Corporate Law 2 cl2Muskan KhatriNo ratings yet

- Bba Corporate RegulationsDocument113 pagesBba Corporate Regulationsnadeemvp111No ratings yet

- CodeOfCorporateGovernance 2012 AmendedJuly2014Document41 pagesCodeOfCorporateGovernance 2012 AmendedJuly2014Aftab TabasamNo ratings yet

- Listed Companies COCG 2019Document57 pagesListed Companies COCG 2019Muzammil LiaquatNo ratings yet

- Irctc - 635Document7 pagesIrctc - 635Dhanush KarthikNo ratings yet

- Corporate GovernanceDocument8 pagesCorporate GovernanceAnooj SrivastavaNo ratings yet

- 4.Management-Legal Aspects of Corporate Governance For IT Companies in IndiaDocument8 pages4.Management-Legal Aspects of Corporate Governance For IT Companies in IndiaImpact JournalsNo ratings yet

- Corporate GovernanceDocument19 pagesCorporate GovernanceRajesh PaulNo ratings yet

- Assignment - CG & BEDocument4 pagesAssignment - CG & BErajesh laddhaNo ratings yet

- Corporate Governance in India: A Legal Analysis: Prabhash Dalei, Paridhi Tulsyan and Shikhar MaraviDocument3 pagesCorporate Governance in India: A Legal Analysis: Prabhash Dalei, Paridhi Tulsyan and Shikhar MaraviManoj DhamiNo ratings yet

- PDF Document E1FC588E4444 1Document8 pagesPDF Document E1FC588E4444 1sudeepNo ratings yet

- Corporate Govern Hardcopy - ComparisonDocument58 pagesCorporate Govern Hardcopy - ComparisonAnkit PandyaNo ratings yet

- Corporate Governance FrameworkDocument4 pagesCorporate Governance Frameworkvivienne mimiNo ratings yet

- Corporate Governance in IndiaDocument7 pagesCorporate Governance in Indiaayushsinghal124No ratings yet

- Unit 3.3 - Future of CGDocument17 pagesUnit 3.3 - Future of CGNithyasri MuthuNo ratings yet

- (CG) ComparisonDocument9 pages(CG) ComparisonKatsuhiko TangNo ratings yet

- Introduction of Corporate GovernanceDocument8 pagesIntroduction of Corporate GovernanceHasanur RaselNo ratings yet

- The Malaysian Code On Corporate Governance 2017: Client Update: MalaysiaDocument6 pagesThe Malaysian Code On Corporate Governance 2017: Client Update: MalaysiaIntan NurdianaNo ratings yet

- The Companies Act 2012 Salient Features DBR 2015Document4 pagesThe Companies Act 2012 Salient Features DBR 2015Day VidNo ratings yet

- 01 - Corporate Governance - CONCEPTUAL FRAMEWORK OF CORPORATE GOVERNANCEDocument109 pages01 - Corporate Governance - CONCEPTUAL FRAMEWORK OF CORPORATE GOVERNANCEVij88888No ratings yet

- UK Corporate Governance CodeDocument6 pagesUK Corporate Governance CodeNabil Ahmed KhanNo ratings yet

- Corporate Governance Short NotesDocument8 pagesCorporate Governance Short NotesVivekNo ratings yet

- CSR and CG BeDocument3 pagesCSR and CG BeDondapati Raga Sravya ReddyNo ratings yet

- 18 Exposure DraftDocument15 pages18 Exposure DraftVaishali GaggarNo ratings yet

- FM 2 Group 7Document19 pagesFM 2 Group 7Payal PatelNo ratings yet

- Group Assignment Company's Act, 2013 Was Modified To Enhance Corporate Governance in IndiaDocument11 pagesGroup Assignment Company's Act, 2013 Was Modified To Enhance Corporate Governance in IndiaANKITA GOOMERNo ratings yet

- Categories of Software MaintenanceDocument24 pagesCategories of Software Maintenancepramodtiwari1989No ratings yet

- Internship On Harish Food ZoneDocument17 pagesInternship On Harish Food ZoneSwethaNo ratings yet

- Sri Lankan Bank Account ComparisonDocument18 pagesSri Lankan Bank Account ComparisonVaruni_Gunawardana100% (1)

- Itsm Inter MCQ - UncramDocument3 pagesItsm Inter MCQ - UncramKARTHIKNo ratings yet

- Income Based Valuation Discounted Cash Flows Group 2Document90 pagesIncome Based Valuation Discounted Cash Flows Group 2natalie clyde mates100% (1)

- DOH Manual AcronymsDocument14 pagesDOH Manual AcronymsJohn Oliver GuiangNo ratings yet

- Graphic Designing: by Hajie RosarioDocument9 pagesGraphic Designing: by Hajie RosarioHajie RosarioNo ratings yet

- Common Business Transactions Using The Rules of Debit and CreditDocument9 pagesCommon Business Transactions Using The Rules of Debit and CreditSHIERY MAE FALCONITINNo ratings yet

- SMPG Corporate Actions Events Templates - SR2021: DisclaimerDocument233 pagesSMPG Corporate Actions Events Templates - SR2021: Disclaimershivank tiwariNo ratings yet

- Market Identification Process: Stage 1 Stage 3 Stage 2Document28 pagesMarket Identification Process: Stage 1 Stage 3 Stage 2Leslie Salvo Jr.100% (1)

- Installment Promissory Note 1Document1 pageInstallment Promissory Note 1api-385482345No ratings yet

- Exercises Chapter 04Document23 pagesExercises Chapter 04vintcs181892No ratings yet

- Eloisa S. Gavilan BSBA-HR2nd YrDocument2 pagesEloisa S. Gavilan BSBA-HR2nd YrGoldengate CollegesNo ratings yet

- A New Day For SustainabilityDocument9 pagesA New Day For SustainabilityswaraNo ratings yet

- Request NDT Welder TestDocument1 pageRequest NDT Welder TestFerdie OSNo ratings yet

- Form 49A Application For Allotment of Permanent Account NumberDocument2 pagesForm 49A Application For Allotment of Permanent Account NumberRAHUL TIWARINo ratings yet

- Environmental Analysis 2Document33 pagesEnvironmental Analysis 2Nitesh BoutaniveNo ratings yet

- PlanDocument120 pagesPlantariq19870% (1)

- Accounting Controls and Bureaucratic Strategies in Municipal GovernmentDocument24 pagesAccounting Controls and Bureaucratic Strategies in Municipal GovernmentRian LiraldoNo ratings yet

- Product: Marketing Mix For NvidiaDocument8 pagesProduct: Marketing Mix For NvidiaMohammed QatariNo ratings yet

- B0175 Dsday2 Atlstmts - Linex.dsstmts - 4408 - Ddastmts 04212020Document1 pageB0175 Dsday2 Atlstmts - Linex.dsstmts - 4408 - Ddastmts 04212020Coughman MattNo ratings yet

- Circular W.E.F 19th May'22Document224 pagesCircular W.E.F 19th May'22Mohit MohataNo ratings yet

- ProjcetbovontosDocument59 pagesProjcetbovontosjhkljhkNo ratings yet

- Insidethecircle TradeModelDocument25 pagesInsidethecircle TradeModelArif AgustianNo ratings yet

- Keya Cosmetics LTDDocument2 pagesKeya Cosmetics LTDTanveer HasanNo ratings yet

- The Odisha Factories Rules 1950Document297 pagesThe Odisha Factories Rules 1950Lalatendu Mahanta0% (1)