Download as pdf or txt

You might also like

- Accion Venture Lab - ESOP Best Practices PDFDocument44 pagesAccion Venture Lab - ESOP Best Practices PDFjeph79No ratings yet

- Presentation On ESOPDocument16 pagesPresentation On ESOPPriyanka GuravNo ratings yet

- ICAI Guidance Note - Employee Share-Based PaymentsDocument66 pagesICAI Guidance Note - Employee Share-Based PaymentssagarganuNo ratings yet

- Chapter 4 Company Accounts 3Document150 pagesChapter 4 Company Accounts 3Shashidhar BukkaNo ratings yet

- Company Accounts: Unit - 1: ESOP and Buy-Back of SharesDocument26 pagesCompany Accounts: Unit - 1: ESOP and Buy-Back of Sharesshrayansh123No ratings yet

- 55966bos45368may20 p5 cp3 PDFDocument26 pages55966bos45368may20 p5 cp3 PDFankush sharmaNo ratings yet

- Employee Stock Option - WikipediaDocument11 pagesEmployee Stock Option - WikipediaDarshit BhovarNo ratings yet

- Call Option Compensation: Contract DifferencesDocument3 pagesCall Option Compensation: Contract Differencesnk1407No ratings yet

- Media Go - LNKDocument5 pagesMedia Go - LNKSneha ChavanNo ratings yet

- C3 Accounting For Employee Stock Option PlansDocument33 pagesC3 Accounting For Employee Stock Option PlansSUBHNo ratings yet

- Wa0035.Document48 pagesWa0035.Abhishek PokharkarNo ratings yet

- Why Companies Buy Back Shares Surplus Cash: When The Company Has A Significant Amount of Cash and There AreDocument21 pagesWhy Companies Buy Back Shares Surplus Cash: When The Company Has A Significant Amount of Cash and There AreSapna ThukralNo ratings yet

- Contemporary Strategic Compensation ChallengesDocument18 pagesContemporary Strategic Compensation ChallengesMD.Rakibul HasanNo ratings yet

- Employee Stock Option SchemeDocument6 pagesEmployee Stock Option Schemezenith chhablaniNo ratings yet

- Assignment Employee Stock Over PlansDocument5 pagesAssignment Employee Stock Over PlansManinder Singh KainthNo ratings yet

- ESOP NoteDocument7 pagesESOP NotePranav TannaNo ratings yet

- Employee Stock Option Plan 264Document21 pagesEmployee Stock Option Plan 264TejalTamboliNo ratings yet

- Stock Comp 2021Document13 pagesStock Comp 2021Parvathi M L0% (1)

- Modern Compensation TechniquesDocument18 pagesModern Compensation TechniquesSuniel100% (1)

- Equity Compensation PlansDocument18 pagesEquity Compensation PlansCharmi PoraniyaNo ratings yet

- ESOP & Sweat Equity FeaturesDocument26 pagesESOP & Sweat Equity FeaturesjayatheerthavNo ratings yet

- Accounting For Employee Stock Option Plans: After Studying This Chapter, You Will Be Able ToDocument41 pagesAccounting For Employee Stock Option Plans: After Studying This Chapter, You Will Be Able ToSandeep As SandeepNo ratings yet

- Shared Based PaymentsDocument2 pagesShared Based PaymentsBilal AzharNo ratings yet

- Accounting For Employee Stock Option PlansDocument41 pagesAccounting For Employee Stock Option Plansamit debnathNo ratings yet

- 32171final ST Mat p1 Jan13 cp7Document35 pages32171final ST Mat p1 Jan13 cp7sivanpillai ganesanNo ratings yet

- Esop Case StudyDocument28 pagesEsop Case Studyhareshms100% (2)

- ESOPDocument8 pagesESOPKiran GvNo ratings yet

- Employee Stock Option PlanDocument7 pagesEmployee Stock Option Plankrupalee100% (1)

- A034 Gopika CLDocument8 pagesA034 Gopika CLgopika mundraNo ratings yet

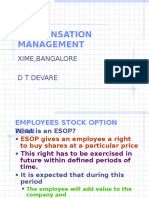

- Compensation Management: Xime, Bangalore D T DevareDocument20 pagesCompensation Management: Xime, Bangalore D T DevareJainendra SinhaNo ratings yet

- Growth of Esops (History) : A TrustDocument16 pagesGrowth of Esops (History) : A Trustcutiebabe1010No ratings yet

- Chapter 16 Dilutive Securities and Earningsper ShaDocument2 pagesChapter 16 Dilutive Securities and Earningsper ShaSatrio seno SancokoNo ratings yet

- Types of ESOPDocument4 pagesTypes of ESOPangeetNo ratings yet

- Incentives and Fringe BenefitsDocument4 pagesIncentives and Fringe BenefitsPankaj2cNo ratings yet

- Sample ESOP PlanDocument6 pagesSample ESOP PlanAnjali SharmaNo ratings yet

- Employee Stock Option SchemeDocument9 pagesEmployee Stock Option Schemetrabhijith1988No ratings yet

- Equity Based CompensationDocument20 pagesEquity Based Compensationhimanshi100% (1)

- ESOP Best PracticesDocument44 pagesESOP Best PracticesPrateek Goel100% (1)

- CMS Business School (Jain Deemed-To-Be University)Document7 pagesCMS Business School (Jain Deemed-To-Be University)Bijosh ThomasNo ratings yet

- Converted 110401Document53 pagesConverted 110401Javal ChoksiNo ratings yet

- Stock OptionsDocument18 pagesStock OptionsJason GrohNo ratings yet

- KPMG Esop SurveyDocument28 pagesKPMG Esop Surveykunal2301No ratings yet

- Checklist ESOPDocument24 pagesChecklist ESOPKnowledge GuruNo ratings yet

- Mod 8Document28 pagesMod 8sri1031No ratings yet

- Advisory Note On Stock OptionsDocument5 pagesAdvisory Note On Stock Optionssmita goelNo ratings yet

- Company ProjectDocument14 pagesCompany ProjectMayank Sahu0% (1)

- Companies Act - Chapter 4 (Share Capital 2)Document14 pagesCompanies Act - Chapter 4 (Share Capital 2)shreyuttam82No ratings yet

- Financial MarketsDocument7 pagesFinancial MarketsBlade BNo ratings yet

- ESOP AnnexureDocument4 pagesESOP AnnexureDeepika GuptaNo ratings yet

- Esos EspsDocument10 pagesEsos EspsSaraf KushalNo ratings yet

- HSA Taxation Law Policy ESOPs and SARsDocument5 pagesHSA Taxation Law Policy ESOPs and SARsTomNo ratings yet

- Brief Note On Esops (Employee Stock Option Plans)Document2 pagesBrief Note On Esops (Employee Stock Option Plans)crajagNo ratings yet

- 6c656pms & Esop NewDocument24 pages6c656pms & Esop NewSasanka YalamanchiliNo ratings yet

- Buy Back, Esops and Sweat Equity RegulationsDocument55 pagesBuy Back, Esops and Sweat Equity RegulationscdhiNo ratings yet

- Exotic CuisineDocument5 pagesExotic CuisineHana Tarizkha CoganuliNo ratings yet

- 3 ChapDocument4 pages3 ChapSuhani AngelNo ratings yet

- 1.Share-Based CompensationDocument3 pages1.Share-Based CompensationFranz AppleNo ratings yet

- 2024 Becker CPA Review TCP Notes - Tax Compliance and Planning For IndividualsDocument29 pages2024 Becker CPA Review TCP Notes - Tax Compliance and Planning For IndividualscraigsappletreeNo ratings yet

- OPTIONS TRADING: Mastering the Art of Options Trading for Financial Success (2023 Guide for Beginners)From EverandOPTIONS TRADING: Mastering the Art of Options Trading for Financial Success (2023 Guide for Beginners)No ratings yet

- SWING TRADING OPTIONS: Maximizing Profits with Short-Term Option Strategies (2024 Guide for Beginners)From EverandSWING TRADING OPTIONS: Maximizing Profits with Short-Term Option Strategies (2024 Guide for Beginners)No ratings yet

- Reconciliation Govt AccountingDocument5 pagesReconciliation Govt AccountingShouvik NagNo ratings yet

- Financial StatementDocument197 pagesFinancial StatementShouvik NagNo ratings yet

- 1 Merged CompressedDocument89 pages1 Merged CompressedShouvik NagNo ratings yet

- Yeager CPA - Govt AccountingDocument73 pagesYeager CPA - Govt AccountingShouvik NagNo ratings yet

- SIMSDocument14 pagesSIMSShouvik NagNo ratings yet

- 21 Most Haunted Places in The WorldDocument10 pages21 Most Haunted Places in The WorldShouvik NagNo ratings yet

- Q.Dividend PolicyDocument2 pagesQ.Dividend PolicyHaris HasanNo ratings yet

- Prakash Kumar 10927921 Saurabh Surana 10927865 Rohit Nerurkar 10927806 Sachin Singh 10927862 Abhishek Moharana 10927912 Sushant Omer 10927871Document28 pagesPrakash Kumar 10927921 Saurabh Surana 10927865 Rohit Nerurkar 10927806 Sachin Singh 10927862 Abhishek Moharana 10927912 Sushant Omer 10927871Abhishek MoharanaNo ratings yet

- BOC - WorkshopDocument21 pagesBOC - WorkshopVedanth MudholkarNo ratings yet

- Brokerage Calculator: Sample Contract NoteDocument1 pageBrokerage Calculator: Sample Contract NotebasanisujithkumarNo ratings yet

- Stock: 20 Stock Broking Firms inDocument19 pagesStock: 20 Stock Broking Firms insadanandsaharmaNo ratings yet

- Estimating Spot Rates and FWD Rates (Using Bootstrapping Method)Document3 pagesEstimating Spot Rates and FWD Rates (Using Bootstrapping Method)9210490991No ratings yet

- The Declining U.S. Equity PremiumDocument19 pagesThe Declining U.S. Equity PremiumpostscriptNo ratings yet

- Trading Terms @AllCandleSticksPatternDocument3 pagesTrading Terms @AllCandleSticksPatternLOVEPREET PURINo ratings yet

- Welcome To My: PresentationDocument8 pagesWelcome To My: PresentationImran KhanNo ratings yet

- Methodology SOXDocument5 pagesMethodology SOXsasa332138No ratings yet

- Announcement of Result of Tender Offer For Shares in FUJITSU FRONTECH LIMITED (Securities Code 6945)Document5 pagesAnnouncement of Result of Tender Offer For Shares in FUJITSU FRONTECH LIMITED (Securities Code 6945)vivektripathi11619No ratings yet

- Infinite Possible Returns With Minimal RiskDocument64 pagesInfinite Possible Returns With Minimal RiskEnrique Blanco67% (3)

- Intacc2 - Assignment 4Document3 pagesIntacc2 - Assignment 4Gray JavierNo ratings yet

- Grant Noble - The Trader's EdgeDocument128 pagesGrant Noble - The Trader's EdgeneerajmattaNo ratings yet

- PDF 14 Pengantar AkunDocument58 pagesPDF 14 Pengantar AkunPeony Risha Mulyadi PutriNo ratings yet

- Case 31 Wonder BarsDocument11 pagesCase 31 Wonder Barsasri nurfathiNo ratings yet

- Lecture - 2 Law On Negotiable InstrumentsDocument19 pagesLecture - 2 Law On Negotiable InstrumentsDaryll OraizNo ratings yet

- Financial Derivatives: Session 1Document97 pagesFinancial Derivatives: Session 1Vivek KhandelwalNo ratings yet

- Strategic Financial Management by Pavan SirDocument4 pagesStrategic Financial Management by Pavan Sirhermandeep5No ratings yet

- Credit Default Swap Pricing ModelDocument34 pagesCredit Default Swap Pricing ModeldovidsteinbergNo ratings yet

- Hunting Endangered Species: Investing in The Market For Corporate Control Fall 2012 Strategy PaperDocument15 pagesHunting Endangered Species: Investing in The Market For Corporate Control Fall 2012 Strategy PaperTobias Carlisle100% (1)

- Investment Analysis and Portfolio Management: Frank K. Reilly & Keith C. BrownDocument55 pagesInvestment Analysis and Portfolio Management: Frank K. Reilly & Keith C. BrownRagini SharmaNo ratings yet

- MODAUD2 Unit 4 Audit of Bonds Payable T31516 FINALDocument3 pagesMODAUD2 Unit 4 Audit of Bonds Payable T31516 FINALmimi960% (2)

- 12th Comm One Mark E.MDocument2 pages12th Comm One Mark E.MBasker GopalakrishnanNo ratings yet

- All Shares Islamic Index of Pakistan: (Developed by Karachi Stock Exchange and Meezan Bank Limited)Document14 pagesAll Shares Islamic Index of Pakistan: (Developed by Karachi Stock Exchange and Meezan Bank Limited)muhammad taufikNo ratings yet

- CREDO PresentationDocument23 pagesCREDO PresentationPampalini01No ratings yet

- Corporate Identity Number: U99999DL1993PLC054135: Registered Office: 12 Central Service Office: 2Document6 pagesCorporate Identity Number: U99999DL1993PLC054135: Registered Office: 12 Central Service Office: 2shakya jagaran manchNo ratings yet

- Options Theory For Professional TradingDocument4 pagesOptions Theory For Professional TradingRaju.KonduruNo ratings yet

- SEC Reports Used in SEC FilingsDocument2 pagesSEC Reports Used in SEC FilingsSECfly. IncNo ratings yet

- Long Sec Lending PaperDocument123 pagesLong Sec Lending PaperAl T-sangNo ratings yet