Download as pdf or txt

You might also like

- CMFAS Module 8A (1 Edition) Mock Paper: © Singapore College of InsuranceDocument13 pagesCMFAS Module 8A (1 Edition) Mock Paper: © Singapore College of InsuranceMalvin Tan100% (2)

- Group Report For NX0441Document25 pagesGroup Report For NX0441Avinash AsokanNo ratings yet

- Couturier 2014Document267 pagesCouturier 2014kkokinovaNo ratings yet

- 7Ps of Marketing Mix of ICICI BankDocument8 pages7Ps of Marketing Mix of ICICI Bankgktest4321100% (3)

- Chapter 2 The Financial Market EnvironmentDocument35 pagesChapter 2 The Financial Market EnvironmentJames Kok67% (3)

- 13-Interest Rate Risk ManagementDocument13 pages13-Interest Rate Risk ManagementSANCHI610No ratings yet

- One LifeDocument2 pagesOne Lifeapi-3718318No ratings yet

- Criminology Notes 14Document4 pagesCriminology Notes 1456vkyfbcgqNo ratings yet

- This New Christmas Carol: KK KK KKDocument1 pageThis New Christmas Carol: KK KK KKHéctor LuzardoNo ratings yet

- RCC Intro.1Document6 pagesRCC Intro.1MovieNo ratings yet

- Froposal Report: Coci Cnariot Te ABCDocument1 pageFroposal Report: Coci Cnariot Te ABCShyam Sundar JanaNo ratings yet

- Kalbi - Eecs 203 Exam 1Document1 pageKalbi - Eecs 203 Exam 1Mahmoud ElsayedNo ratings yet

- Chemistry Practicals PDFDocument61 pagesChemistry Practicals PDFpmbhai73No ratings yet

- Oppor T Uni T I Es Busi Nesspr OposalDocument7 pagesOppor T Uni T I Es Busi Nesspr OposalLyka Jasmine PandacanNo ratings yet

- Cant 405 The Bright ForevermoreDocument1 pageCant 405 The Bright ForevermorePaulin AGOSSOUNo ratings yet

- 0wZnGVs - 0945470045Document70 pages0wZnGVs - 0945470045LuisGómezNo ratings yet

- God Rest Ye Merry Gentlemen Notes 1Document3 pagesGod Rest Ye Merry Gentlemen Notes 1SharlonWrayNo ratings yet

- LevelDocument82 pagesLevel6cwj9cpfpjNo ratings yet

- Adobe Scan 04-Feb-2021Document3 pagesAdobe Scan 04-Feb-2021Rohit KumarNo ratings yet

- Adobe Scan 1 Jun 2024Document18 pagesAdobe Scan 1 Jun 2024Chess SirNo ratings yet

- Bioelectric Potentials: Krishna Veni.P 1Document34 pagesBioelectric Potentials: Krishna Veni.P 1ramanaidu1No ratings yet

- Free ConsentDocument8 pagesFree Consentpriyadharshini2020aNo ratings yet

- Class Notes 18 Jun 2019Document6 pagesClass Notes 18 Jun 2019jeff mathewsNo ratings yet

- NMKJID31608Document18 pagesNMKJID31608prashantprNo ratings yet

- 99 Red Balloons (6 Horn) PDFDocument23 pages99 Red Balloons (6 Horn) PDFlinkycatNo ratings yet

- BBC Learning English - Syllabus - Towards AdvancedDocument6 pagesBBC Learning English - Syllabus - Towards Advanced이재연No ratings yet

- Structural Imperfections in Solids: SolidificationDocument10 pagesStructural Imperfections in Solids: SolidificationPatric PinheiroNo ratings yet

- Tell Me The Old, Old StoryDocument1 pageTell Me The Old, Old Storyherbert abbeyquayeNo ratings yet

- Nonlinear Analysis of Piled Raft FoundationsDocument24 pagesNonlinear Analysis of Piled Raft FoundationsjoryNo ratings yet

- CONAN The LiberatorDocument19 pagesCONAN The LiberatorBarny SkinnerNo ratings yet

- UntitledDocument35 pagesUntitledBenzene diazonium saltNo ratings yet

- Alfabetul Ilustrat Stegulete Decorative PDFDocument31 pagesAlfabetul Ilustrat Stegulete Decorative PDFAndreea Alexandra BocaNo ratings yet

- HGVH PDFDocument31 pagesHGVH PDFMotronea IoanNo ratings yet

- Amid The Fears That Oppress Our DayDocument1 pageAmid The Fears That Oppress Our DayGabriel FranciscoNo ratings yet

- MCQ EspDocument34 pagesMCQ EspYosef KirosNo ratings yet

- Arc Settlement Record Sheet Gce v2 2021 Anna Version Adjusted For Printing Front Back 431 8mm X 279 4mmDocument2 pagesArc Settlement Record Sheet Gce v2 2021 Anna Version Adjusted For Printing Front Back 431 8mm X 279 4mmDavid SavarinNo ratings yet

- 9 Pumping LemmaDocument36 pages9 Pumping LemmaYuko LynxNo ratings yet

- GP Ratings MCQ Revision Test - 3Document12 pagesGP Ratings MCQ Revision Test - 3RLINS MADURAINo ratings yet

- Sci-Fi & Fantasy Modeller - Volume 36Document100 pagesSci-Fi & Fantasy Modeller - Volume 36Cem Avci100% (1)

- Electric PotentialDocument25 pagesElectric Potentialaviralyadav0001No ratings yet

- Numere Pe Creioane 0-32Document101 pagesNumere Pe Creioane 0-32Adelina ZamfirNo ratings yet

- Knowledge-Based Agents: Teqnht Nohmosônh M. Koumpar KHCDocument51 pagesKnowledge-Based Agents: Teqnht Nohmosônh M. Koumpar KHCVjNo ratings yet

- Maths Formulae Bookmarks Higher AbilityDocument3 pagesMaths Formulae Bookmarks Higher AbilityReshmiNo ratings yet

- HisGuidingHand (Leland)Document1 pageHisGuidingHand (Leland)Gabriel FranciscoNo ratings yet

- UntitledDocument12 pagesUntitledSteve LinkingNo ratings yet

- Beginning String Tunes: 35 Songs With 6 Notes or Less!Document50 pagesBeginning String Tunes: 35 Songs With 6 Notes or Less!Signe Mortensen100% (1)

- Cambridge Listening 18Document8 pagesCambridge Listening 18MM Imdadul KayesNo ratings yet

- Trollip RavenDocument8 pagesTrollip Ravenjmatias765428No ratings yet

- 03 Communication ChannelsDocument5 pages03 Communication ChannelsAryanNo ratings yet

- Guia Tres de Fisica Decimo Tomas 2019-06-11Document9 pagesGuia Tres de Fisica Decimo Tomas 2019-06-11Tomas Parra CaroNo ratings yet

- Sample 2022-11-13Document2 pagesSample 2022-11-13asmae chtoukiNo ratings yet

- O Worship The King TrumpetDocument1 pageO Worship The King TrumpetScott JohnsonNo ratings yet

- ST 1 Mechanical Engineering Sem-5 Statistical TechniquesDocument21 pagesST 1 Mechanical Engineering Sem-5 Statistical Techniques21101130 nareshNo ratings yet

- Aamal E QuraniDocument74 pagesAamal E QuranipolkaboyNo ratings yet

- Paramount ExplainedDocument6 pagesParamount ExplainedCathyNo ratings yet

- Bus Trans 4Document4 pagesBus Trans 4Friendly QueenNo ratings yet

- Columns and StrutsDocument22 pagesColumns and StrutsShiri ShivaNo ratings yet

- Ic Engine Assignment-1Document3 pagesIc Engine Assignment-1Sanju GiriNo ratings yet

- Wilt Thou Be Made Whole PDFDocument1 pageWilt Thou Be Made Whole PDFboatcomNo ratings yet

- 10.electromagnetic WavesDocument108 pages10.electromagnetic Wavesdhananjayadas648No ratings yet

- Ca, 2023Document6 pagesCa, 2023ekarthiksagar1998No ratings yet

- Assignment 2 SolutionDocument5 pagesAssignment 2 SolutionRavi KiranNo ratings yet

- Approximation AlgorithmDocument4 pagesApproximation AlgorithmRohit KumarNo ratings yet

- Demo Version: Cho Ral She Eet Mus Sic - PR Ractice Mp3'S Sandb Backtra AckDocument6 pagesDemo Version: Cho Ral She Eet Mus Sic - PR Ractice Mp3'S Sandb Backtra AckAnca NopceaNo ratings yet

- Madiwala MarketDocument1 pageMadiwala MarketMayank DagaNo ratings yet

- Analysis of Small Food Businesses in San Leonardo Nueva Ecija Using Creative Marketing Basis For Development of Business PlanDocument15 pagesAnalysis of Small Food Businesses in San Leonardo Nueva Ecija Using Creative Marketing Basis For Development of Business PlanIJRASETPublicationsNo ratings yet

- Media Planning Terms and ConceptsDocument27 pagesMedia Planning Terms and ConceptsAnton Kopytov100% (5)

- ECO401 Latest PaPers - SolvedSubjective Mega FileDocument41 pagesECO401 Latest PaPers - SolvedSubjective Mega FileSamra BatoolNo ratings yet

- Tos For Entrep Finals 2ND Sem 2019-2020Document3 pagesTos For Entrep Finals 2ND Sem 2019-2020Gerby GodinezNo ratings yet

- Anatomy of A Trading Range PDFDocument12 pagesAnatomy of A Trading Range PDFErezwa100% (4)

- 9708 s19 QP 11 PDFDocument12 pages9708 s19 QP 11 PDFHEMKESH CONHYENo ratings yet

- Wilkie & Moore - Marketing Contribution To SocietyDocument5 pagesWilkie & Moore - Marketing Contribution To Societysuresh puri goswamiNo ratings yet

- Samara Univrsity: College of Business and EconomicsDocument18 pagesSamara Univrsity: College of Business and Economicsethnan lNo ratings yet

- AdfjsdfjksdfDocument12 pagesAdfjsdfjksdfJohn Carlo PeruNo ratings yet

- Assignment PMDocument3 pagesAssignment PMSyeda ToobaNo ratings yet

- Olpers Final Final ReportDocument35 pagesOlpers Final Final ReportMuhammad HammadNo ratings yet

- 5 Minute Charts Explanation and Guide + Three Free SetupsDocument18 pages5 Minute Charts Explanation and Guide + Three Free Setupskalpesh kathar100% (1)

- Sam SeidenDocument3 pagesSam SeidenPro tube0% (1)

- Consumer Analysis Market Segmentation: Target Market Segment StrategyDocument4 pagesConsumer Analysis Market Segmentation: Target Market Segment StrategyKierstin Kyle RiegoNo ratings yet

- 16 Financial Ratios To Determine A Company's Strength and WeaknessesDocument5 pages16 Financial Ratios To Determine A Company's Strength and WeaknessesOld School Value88% (8)

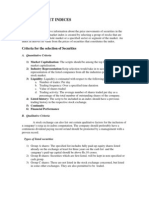

- Stock Market IndicesDocument2 pagesStock Market IndicesbijubodheswarNo ratings yet

- IAS 32 Financial InstrumentDocument6 pagesIAS 32 Financial InstrumentArem CapuliNo ratings yet

- EC1000 Tutorial 3 PDFDocument3 pagesEC1000 Tutorial 3 PDFSabin Sadaf33% (3)

- F7uk 2010 Jun QDocument9 pagesF7uk 2010 Jun QKathleen HenryNo ratings yet

- Debonair Engineering LTD (Case Study Solution)Document3 pagesDebonair Engineering LTD (Case Study Solution)Muhammad Furqan ZebNo ratings yet

- Exercises - Oligopoly: Exercise 1Document3 pagesExercises - Oligopoly: Exercise 1Teyma TouatiNo ratings yet

- How To Evaluate Business IdeasDocument3 pagesHow To Evaluate Business IdeassakshiNo ratings yet

- Trade JournalDocument16 pagesTrade Journalvenkat.sqlNo ratings yet

- IFRS 9 - Financial InstrumentsDocument37 pagesIFRS 9 - Financial InstrumentslaaybaNo ratings yet