Islamic Banking Dissertation

Islamic Banking Dissertation

You might also like

- The Foundations of Islamic Economics and BankingFrom EverandThe Foundations of Islamic Economics and BankingNo ratings yet

- International Shariah Supervisory BoardDocument32 pagesInternational Shariah Supervisory Boardahsaniqbal100% (1)

- BBA Final Internship ReportDocument70 pagesBBA Final Internship ReportTaj Hussain100% (1)

- Term Paper On Islamic BankingDocument8 pagesTerm Paper On Islamic Bankingc5rn3sbr100% (1)

- Islamic Banking Dissertation ProposalDocument5 pagesIslamic Banking Dissertation ProposalPayingSomeoneToWriteAPaperUK100% (2)

- Dissertation Topics On Islamic BankingDocument7 pagesDissertation Topics On Islamic BankingBuyALiteratureReviewPaperCanada100% (1)

- PHD Thesis On Islamic BankingDocument5 pagesPHD Thesis On Islamic Bankingvxjgqeikd100% (2)

- Major Challenges Facing Islamic Capital Market: Building Proper Institutional FrameworkDocument4 pagesMajor Challenges Facing Islamic Capital Market: Building Proper Institutional FrameworkMuhdAfiqNo ratings yet

- PHD Thesis Islamic BankingDocument6 pagesPHD Thesis Islamic BankingGhostWriterCollegePapersUK100% (2)

- Thesis On Islamic Banking in PakistanDocument7 pagesThesis On Islamic Banking in PakistanBuyResumePaperCanada100% (2)

- Islamic Banking Term PaperDocument5 pagesIslamic Banking Term Paperafdtygyhk100% (1)

- Islamic Banking Dissertation TitlesDocument6 pagesIslamic Banking Dissertation TitlesDoMyPaperForMeUK100% (1)

- Islamic Finance Dissertation PDFDocument7 pagesIslamic Finance Dissertation PDFBuyingPapersOnlineSingapore100% (1)

- Research Papers On Islamic Banking Vs Conventional BankingDocument7 pagesResearch Papers On Islamic Banking Vs Conventional BankingvguomivndNo ratings yet

- Islamic Bank ThesisDocument8 pagesIslamic Bank ThesisWriteMyStatisticsPaperCanada100% (1)

- Literature Review of Islamic Banking in MalaysiaDocument5 pagesLiterature Review of Islamic Banking in Malaysiaafdtorpqk100% (1)

- Bachelor Thesis Islamic FinanceDocument7 pagesBachelor Thesis Islamic Financebsq1j65w100% (2)

- Customer'S Awareness Level and Customer'S Service Utilization Decision in Islamic Banking RationaleDocument5 pagesCustomer'S Awareness Level and Customer'S Service Utilization Decision in Islamic Banking Rationalemuhammad usman munawarNo ratings yet

- Islamic Banking Literature ReviewDocument5 pagesIslamic Banking Literature Reviewafmzvulgktflda100% (1)

- Islamic Banking Research PapersDocument5 pagesIslamic Banking Research Papersc9spy2qz100% (1)

- Thesis On Islamic Banking PDFDocument5 pagesThesis On Islamic Banking PDFaflnqhceeoirqy100% (2)

- Islamic Finance PHD Thesis PDFDocument7 pagesIslamic Finance PHD Thesis PDFstephaniebenjaminclarksville100% (2)

- Literature Review Islamic Banking SystemDocument9 pagesLiterature Review Islamic Banking Systemaflsqrbnq100% (1)

- PHD Thesis On Islamic Banking PDFDocument5 pagesPHD Thesis On Islamic Banking PDFcourtneybennettshreveport100% (1)

- Dissertation Islamic Banking PDFDocument4 pagesDissertation Islamic Banking PDFBestWriteMyPaperWebsiteClarksville100% (1)

- Dissertation On Islamic Banking and FinanceDocument8 pagesDissertation On Islamic Banking and FinanceWritingServicesForCollegePapersSingapore100% (1)

- Examining The Comparative Efficiency of GCC Islamic BankingDocument24 pagesExamining The Comparative Efficiency of GCC Islamic BankingNaumankhan83No ratings yet

- Dissertation On "Role of Islamic Banking in Economic Growth"Document44 pagesDissertation On "Role of Islamic Banking in Economic Growth"Noman ansariNo ratings yet

- Literature Review Islamic BankingDocument5 pagesLiterature Review Islamic Bankingaflsjzblf100% (1)

- Islamic Banking Dissertation PDFDocument7 pagesIslamic Banking Dissertation PDFWriteMyStatisticsPaperSingapore100% (1)

- Literature Review On Islamic Banking in UkDocument6 pagesLiterature Review On Islamic Banking in Ukc5eyjfnt100% (1)

- Examining The Comparative Efficiency of GCC Islamic Banking (Plain File)Document21 pagesExamining The Comparative Efficiency of GCC Islamic Banking (Plain File)Naumankhan83No ratings yet

- Causal Relationship Between Islamic and Conventional Banking Instruments in MalaysiaDocument8 pagesCausal Relationship Between Islamic and Conventional Banking Instruments in MalaysiaSihem SissaouiNo ratings yet

- Term Paper On Islamic BankDocument6 pagesTerm Paper On Islamic Bankafmabzmoniomdc100% (1)

- The Difference Between Islamic Banking Financing and Conventional Banking LoansDocument10 pagesThe Difference Between Islamic Banking Financing and Conventional Banking LoanssitinurNo ratings yet

- Issues and Problems of Islamic BankingDocument18 pagesIssues and Problems of Islamic BankingSyed Shaker AhmedNo ratings yet

- Literature Review Islamic FinanceDocument12 pagesLiterature Review Islamic Financeaflspfdov100% (1)

- Dissertation Topics in Islamic Banking and FinanceDocument7 pagesDissertation Topics in Islamic Banking and FinanceWriteMyPaperApaFormatArlingtonNo ratings yet

- PROFIT LOSS SHARING FORMULA BY iSLAMIC BANKSDocument47 pagesPROFIT LOSS SHARING FORMULA BY iSLAMIC BANKSseadeco1991No ratings yet

- Successful Development of Islamic Banks - 94428Document8 pagesSuccessful Development of Islamic Banks - 94428charlie simoNo ratings yet

- Deposits Mobilizationand Financing ManagementDocument165 pagesDeposits Mobilizationand Financing ManagementHasan AbdulNo ratings yet

- ACFrOgAvf56qZh8hwt9XTj6o2tzsFv69YRO7xXd0byf OQYOtpCYFekLySpwNjcYg0EWOUtdvWJsdW6ixurJFa7snFk6Y6mN 2DSD JBmNi5pN7RY8a Fr2UY ED7XcBhjIwcfYy9Rvrrm4X2J9IDocument14 pagesACFrOgAvf56qZh8hwt9XTj6o2tzsFv69YRO7xXd0byf OQYOtpCYFekLySpwNjcYg0EWOUtdvWJsdW6ixurJFa7snFk6Y6mN 2DSD JBmNi5pN7RY8a Fr2UY ED7XcBhjIwcfYy9Rvrrm4X2J9IAmal MobarakiNo ratings yet

- Screenshot 2023-06-28 at 12.08.07 AMDocument14 pagesScreenshot 2023-06-28 at 12.08.07 AMSanchit BudhirajaNo ratings yet

- Investigating The Efficiency of GCC Banking Sector An Empirical Comparison of Islamic and Conventional BanksDocument22 pagesInvestigating The Efficiency of GCC Banking Sector An Empirical Comparison of Islamic and Conventional BanksNaumankhan83No ratings yet

- Research Paper in Islamic FinanceDocument4 pagesResearch Paper in Islamic Financelyn0l1gamop2100% (1)

- Islamic Banking Topics Research Good For PHD ThesisDocument9 pagesIslamic Banking Topics Research Good For PHD Thesisvotukezez1z2No ratings yet

- What Is An Islamic Bank? How Different Is It From A Conventional Bank?Document4 pagesWhat Is An Islamic Bank? How Different Is It From A Conventional Bank?LeeyaRazakNo ratings yet

- Prospects and Problems of Shariah-Compliant Finance: Executive SummaryDocument8 pagesProspects and Problems of Shariah-Compliant Finance: Executive SummarysyedtahaaliNo ratings yet

- Thesis On Islamic Banking and FinanceDocument5 pagesThesis On Islamic Banking and Financeafknowudv100% (3)

- 20 Islamic and C BankingDocument10 pages20 Islamic and C BankingAbdoulie SallahNo ratings yet

- Research Paper On Islamic BankingDocument6 pagesResearch Paper On Islamic Bankinggw0drhkf100% (1)

- Final ReportDocument10 pagesFinal ReportMuhammad AliNo ratings yet

- Issues and Problems of Islamic Banking An Overview On The Review of ProblemsDocument21 pagesIssues and Problems of Islamic Banking An Overview On The Review of ProblemsMayra NiharNo ratings yet

- Research Paper On Islamic Banking in PakistanDocument4 pagesResearch Paper On Islamic Banking in Pakistaniwnlpjrif100% (1)

- Dissertation On Islamic Banking in IndiaDocument6 pagesDissertation On Islamic Banking in IndiaCustomPaperServiceUK100% (1)

- F Per 2012 InternationalDocument5 pagesF Per 2012 InternationalBrandy LeeNo ratings yet

- Dissertation On Islamic Banking in MauritiusDocument8 pagesDissertation On Islamic Banking in MauritiusBestWriteMyPaperWebsiteHighPoint100% (1)

- Issues and Problems of Islamic BankingDocument14 pagesIssues and Problems of Islamic Bankingziadiqbal19100% (9)

- Risk ManagementDocument26 pagesRisk ManagementAmal Ben RamdhaneNo ratings yet

- It's Time To Rethink Islamic Banking Regulation - Brink - The Edge of RiskDocument5 pagesIt's Time To Rethink Islamic Banking Regulation - Brink - The Edge of RiskHaHn MalekNo ratings yet

- Understanding Interest Rate Securities: An Eaglemont Career Book for StudentsFrom EverandUnderstanding Interest Rate Securities: An Eaglemont Career Book for StudentsNo ratings yet

- Weathering the Global Crisis: Can the Traits of Islamic Banking System Make a Difference?From EverandWeathering the Global Crisis: Can the Traits of Islamic Banking System Make a Difference?No ratings yet

- Organizational Theory Term Paper IdeasDocument6 pagesOrganizational Theory Term Paper IdeasHelpWithWritingPapersJackson100% (1)

- Term Paper Essay FormatDocument7 pagesTerm Paper Essay FormatHelpWithWritingPapersJackson100% (1)

- Example Term Paper LayoutDocument7 pagesExample Term Paper LayoutHelpWithWritingPapersJackson100% (1)

- Term Paper Interracial RelationshipsDocument5 pagesTerm Paper Interracial RelationshipsHelpWithWritingPapersJackson100% (1)

- Term Paper Filipino 2Document4 pagesTerm Paper Filipino 2HelpWithWritingPapersJackson100% (1)

- Dissertation Sur Le Bonheur AntigoneDocument5 pagesDissertation Sur Le Bonheur AntigoneHelpWithWritingPapersJackson100% (2)

- Hepatitis C DissertationDocument6 pagesHepatitis C DissertationHelpWithWritingPapersJackson100% (1)

- Fu Berlin Dissertation BiochemieDocument4 pagesFu Berlin Dissertation BiochemieHelpWithWritingPapersJackson100% (1)

- Dissertation ZweitstudiumDocument6 pagesDissertation ZweitstudiumHelpWithWritingPapersJackson100% (1)

- Bed Dissertation TitlesDocument6 pagesBed Dissertation TitlesHelpWithWritingPapersJackson100% (1)

- All But Dissertation TraductionDocument6 pagesAll But Dissertation TraductionHelpWithWritingPapersJackson100% (1)

- Dissertation Politics ExamplesDocument4 pagesDissertation Politics ExamplesHelpWithWritingPapersJackson100% (1)

- Dissertation Meaning WikipediaDocument7 pagesDissertation Meaning WikipediaHelpWithWritingPapersJackson100% (1)

- Dissertation Philosophique Sur La PassionDocument5 pagesDissertation Philosophique Sur La PassionHelpWithWritingPapersJackson100% (1)

- MSC Accounting Dissertation TopicsDocument5 pagesMSC Accounting Dissertation TopicsHelpWithWritingPapersJackson100% (1)

- Sport Business Dissertation IdeasDocument4 pagesSport Business Dissertation IdeasHelpWithWritingPapersJackson100% (1)

- Comment Faire Une Excellente Dissertation en PhilosophieDocument7 pagesComment Faire Une Excellente Dissertation en PhilosophieHelpWithWritingPapersJacksonNo ratings yet

- Sujet de Dissertation PoesieDocument5 pagesSujet de Dissertation PoesieHelpWithWritingPapersJackson100% (1)

- Islamic Interbank Money Market InstrumentDocument6 pagesIslamic Interbank Money Market InstrumentAnaszNazriNo ratings yet

- Islamic Finance Project-MutualFundsDocument42 pagesIslamic Finance Project-MutualFundsMuhammad Mamoon Iqbal0% (1)

- Abmf3213 Islamic Banking - Tutorial 1Document4 pagesAbmf3213 Islamic Banking - Tutorial 1Bom BiBiNo ratings yet

- An Analysis of Investment Activities of Al-Arafah Islami Bank LimitedDocument9 pagesAn Analysis of Investment Activities of Al-Arafah Islami Bank Limitedmd.jewel ranaNo ratings yet

- Akta Koperasi EnglishDocument57 pagesAkta Koperasi EnglishSuraiya Abd RahmanNo ratings yet

- Islamic Finance 1.1Document60 pagesIslamic Finance 1.1Macarandas İbrahimNo ratings yet

- Historic Judgement On RibaDocument15 pagesHistoric Judgement On RibaTaha BajwaNo ratings yet

- Islamic Financial Services Industry Stability Report 2019 - enDocument118 pagesIslamic Financial Services Industry Stability Report 2019 - enSophie PonomariovaNo ratings yet

- National Events: 67th Management Accountants DayDocument9 pagesNational Events: 67th Management Accountants DayGoopNo ratings yet

- Measuring The Impact of Islamic Microfinance Product, Qarz-E-Hasna, On Poverty Alleviation in Hyderabad DistrictDocument26 pagesMeasuring The Impact of Islamic Microfinance Product, Qarz-E-Hasna, On Poverty Alleviation in Hyderabad DistrictmairaNo ratings yet

- Shinta Amalina Hazrati Havidz: JAMBI, JUNE 4TH, 1992Document2 pagesShinta Amalina Hazrati Havidz: JAMBI, JUNE 4TH, 1992wulanda septianiNo ratings yet

- 374-Article Text-866-1-10-20190925 PDFDocument37 pages374-Article Text-866-1-10-20190925 PDFVita Citra MulyandiniNo ratings yet

- Islamic FinanceDocument27 pagesIslamic FinanceChing ZhiNo ratings yet

- Women I Deposit Account (Zehrah)Document2 pagesWomen I Deposit Account (Zehrah)kefiyalew BNo ratings yet

- Conventional and Islamic Banking System: Understanding Level of Knowledge Among Students in UitmDocument9 pagesConventional and Islamic Banking System: Understanding Level of Knowledge Among Students in UitmNurul HazwaniNo ratings yet

- Fin546 Topic 2 - Shari'Ah Contracts For Islamic Financial InstrumentsDocument69 pagesFin546 Topic 2 - Shari'Ah Contracts For Islamic Financial InstrumentsMuhd DanialNo ratings yet

- FinTech Sharia 3 1 PDFDocument51 pagesFinTech Sharia 3 1 PDFMahyuniNo ratings yet

- IFB Product Services - For induction-FINAL 11-13Document152 pagesIFB Product Services - For induction-FINAL 11-13tsadikNo ratings yet

- Illegality of Contract Under The Contracts Acts 1950 in Islamic Home Financing in Malaysia: Issues and Possible ReformDocument9 pagesIllegality of Contract Under The Contracts Acts 1950 in Islamic Home Financing in Malaysia: Issues and Possible ReformMaxwilliam DanielNo ratings yet

- Mezan Intership ReportDocument151 pagesMezan Intership ReportMurtaza AkmalNo ratings yet

- Musharakah Financing ModelDocument18 pagesMusharakah Financing ModelMuhd Basier Abd MutalibNo ratings yet

- List 20150331 PDFDocument131 pagesList 20150331 PDFHuesniNo ratings yet

- FINN 441 - Islamic Banking and Finance-Syed Aun Raza RizviDocument5 pagesFINN 441 - Islamic Banking and Finance-Syed Aun Raza RizvisaminaNo ratings yet

- AITABDocument25 pagesAITABalimul imranNo ratings yet

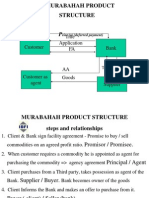

- Murabahah Product Structure: Title Application FADocument26 pagesMurabahah Product Structure: Title Application FAUmair UddinNo ratings yet

- Bisirat BekeleDocument90 pagesBisirat Bekeleselman bedruNo ratings yet

- Principle of Islamic FinanceDocument6 pagesPrinciple of Islamic FinanceumbreenNo ratings yet

- EL For BussinessDocument18 pagesEL For Bussinesshannguyen.31221021972No ratings yet

Download as pdf or txt

You might also like

- The Foundations of Islamic Economics and BankingFrom EverandThe Foundations of Islamic Economics and BankingNo ratings yet

- International Shariah Supervisory BoardDocument32 pagesInternational Shariah Supervisory Boardahsaniqbal100% (1)

- BBA Final Internship ReportDocument70 pagesBBA Final Internship ReportTaj Hussain100% (1)

- Term Paper On Islamic BankingDocument8 pagesTerm Paper On Islamic Bankingc5rn3sbr100% (1)

- Islamic Banking Dissertation ProposalDocument5 pagesIslamic Banking Dissertation ProposalPayingSomeoneToWriteAPaperUK100% (2)

- Dissertation Topics On Islamic BankingDocument7 pagesDissertation Topics On Islamic BankingBuyALiteratureReviewPaperCanada100% (1)

- PHD Thesis On Islamic BankingDocument5 pagesPHD Thesis On Islamic Bankingvxjgqeikd100% (2)

- Major Challenges Facing Islamic Capital Market: Building Proper Institutional FrameworkDocument4 pagesMajor Challenges Facing Islamic Capital Market: Building Proper Institutional FrameworkMuhdAfiqNo ratings yet

- PHD Thesis Islamic BankingDocument6 pagesPHD Thesis Islamic BankingGhostWriterCollegePapersUK100% (2)

- Thesis On Islamic Banking in PakistanDocument7 pagesThesis On Islamic Banking in PakistanBuyResumePaperCanada100% (2)

- Islamic Banking Term PaperDocument5 pagesIslamic Banking Term Paperafdtygyhk100% (1)

- Islamic Banking Dissertation TitlesDocument6 pagesIslamic Banking Dissertation TitlesDoMyPaperForMeUK100% (1)

- Islamic Finance Dissertation PDFDocument7 pagesIslamic Finance Dissertation PDFBuyingPapersOnlineSingapore100% (1)

- Research Papers On Islamic Banking Vs Conventional BankingDocument7 pagesResearch Papers On Islamic Banking Vs Conventional BankingvguomivndNo ratings yet

- Islamic Bank ThesisDocument8 pagesIslamic Bank ThesisWriteMyStatisticsPaperCanada100% (1)

- Literature Review of Islamic Banking in MalaysiaDocument5 pagesLiterature Review of Islamic Banking in Malaysiaafdtorpqk100% (1)

- Bachelor Thesis Islamic FinanceDocument7 pagesBachelor Thesis Islamic Financebsq1j65w100% (2)

- Customer'S Awareness Level and Customer'S Service Utilization Decision in Islamic Banking RationaleDocument5 pagesCustomer'S Awareness Level and Customer'S Service Utilization Decision in Islamic Banking Rationalemuhammad usman munawarNo ratings yet

- Islamic Banking Literature ReviewDocument5 pagesIslamic Banking Literature Reviewafmzvulgktflda100% (1)

- Islamic Banking Research PapersDocument5 pagesIslamic Banking Research Papersc9spy2qz100% (1)

- Thesis On Islamic Banking PDFDocument5 pagesThesis On Islamic Banking PDFaflnqhceeoirqy100% (2)

- Islamic Finance PHD Thesis PDFDocument7 pagesIslamic Finance PHD Thesis PDFstephaniebenjaminclarksville100% (2)

- Literature Review Islamic Banking SystemDocument9 pagesLiterature Review Islamic Banking Systemaflsqrbnq100% (1)

- PHD Thesis On Islamic Banking PDFDocument5 pagesPHD Thesis On Islamic Banking PDFcourtneybennettshreveport100% (1)

- Dissertation Islamic Banking PDFDocument4 pagesDissertation Islamic Banking PDFBestWriteMyPaperWebsiteClarksville100% (1)

- Dissertation On Islamic Banking and FinanceDocument8 pagesDissertation On Islamic Banking and FinanceWritingServicesForCollegePapersSingapore100% (1)

- Examining The Comparative Efficiency of GCC Islamic BankingDocument24 pagesExamining The Comparative Efficiency of GCC Islamic BankingNaumankhan83No ratings yet

- Dissertation On "Role of Islamic Banking in Economic Growth"Document44 pagesDissertation On "Role of Islamic Banking in Economic Growth"Noman ansariNo ratings yet

- Literature Review Islamic BankingDocument5 pagesLiterature Review Islamic Bankingaflsjzblf100% (1)

- Islamic Banking Dissertation PDFDocument7 pagesIslamic Banking Dissertation PDFWriteMyStatisticsPaperSingapore100% (1)

- Literature Review On Islamic Banking in UkDocument6 pagesLiterature Review On Islamic Banking in Ukc5eyjfnt100% (1)

- Examining The Comparative Efficiency of GCC Islamic Banking (Plain File)Document21 pagesExamining The Comparative Efficiency of GCC Islamic Banking (Plain File)Naumankhan83No ratings yet

- Causal Relationship Between Islamic and Conventional Banking Instruments in MalaysiaDocument8 pagesCausal Relationship Between Islamic and Conventional Banking Instruments in MalaysiaSihem SissaouiNo ratings yet

- Term Paper On Islamic BankDocument6 pagesTerm Paper On Islamic Bankafmabzmoniomdc100% (1)

- The Difference Between Islamic Banking Financing and Conventional Banking LoansDocument10 pagesThe Difference Between Islamic Banking Financing and Conventional Banking LoanssitinurNo ratings yet

- Issues and Problems of Islamic BankingDocument18 pagesIssues and Problems of Islamic BankingSyed Shaker AhmedNo ratings yet

- Literature Review Islamic FinanceDocument12 pagesLiterature Review Islamic Financeaflspfdov100% (1)

- Dissertation Topics in Islamic Banking and FinanceDocument7 pagesDissertation Topics in Islamic Banking and FinanceWriteMyPaperApaFormatArlingtonNo ratings yet

- PROFIT LOSS SHARING FORMULA BY iSLAMIC BANKSDocument47 pagesPROFIT LOSS SHARING FORMULA BY iSLAMIC BANKSseadeco1991No ratings yet

- Successful Development of Islamic Banks - 94428Document8 pagesSuccessful Development of Islamic Banks - 94428charlie simoNo ratings yet

- Deposits Mobilizationand Financing ManagementDocument165 pagesDeposits Mobilizationand Financing ManagementHasan AbdulNo ratings yet

- ACFrOgAvf56qZh8hwt9XTj6o2tzsFv69YRO7xXd0byf OQYOtpCYFekLySpwNjcYg0EWOUtdvWJsdW6ixurJFa7snFk6Y6mN 2DSD JBmNi5pN7RY8a Fr2UY ED7XcBhjIwcfYy9Rvrrm4X2J9IDocument14 pagesACFrOgAvf56qZh8hwt9XTj6o2tzsFv69YRO7xXd0byf OQYOtpCYFekLySpwNjcYg0EWOUtdvWJsdW6ixurJFa7snFk6Y6mN 2DSD JBmNi5pN7RY8a Fr2UY ED7XcBhjIwcfYy9Rvrrm4X2J9IAmal MobarakiNo ratings yet

- Screenshot 2023-06-28 at 12.08.07 AMDocument14 pagesScreenshot 2023-06-28 at 12.08.07 AMSanchit BudhirajaNo ratings yet

- Investigating The Efficiency of GCC Banking Sector An Empirical Comparison of Islamic and Conventional BanksDocument22 pagesInvestigating The Efficiency of GCC Banking Sector An Empirical Comparison of Islamic and Conventional BanksNaumankhan83No ratings yet

- Research Paper in Islamic FinanceDocument4 pagesResearch Paper in Islamic Financelyn0l1gamop2100% (1)

- Islamic Banking Topics Research Good For PHD ThesisDocument9 pagesIslamic Banking Topics Research Good For PHD Thesisvotukezez1z2No ratings yet

- What Is An Islamic Bank? How Different Is It From A Conventional Bank?Document4 pagesWhat Is An Islamic Bank? How Different Is It From A Conventional Bank?LeeyaRazakNo ratings yet

- Prospects and Problems of Shariah-Compliant Finance: Executive SummaryDocument8 pagesProspects and Problems of Shariah-Compliant Finance: Executive SummarysyedtahaaliNo ratings yet

- Thesis On Islamic Banking and FinanceDocument5 pagesThesis On Islamic Banking and Financeafknowudv100% (3)

- 20 Islamic and C BankingDocument10 pages20 Islamic and C BankingAbdoulie SallahNo ratings yet

- Research Paper On Islamic BankingDocument6 pagesResearch Paper On Islamic Bankinggw0drhkf100% (1)

- Final ReportDocument10 pagesFinal ReportMuhammad AliNo ratings yet

- Issues and Problems of Islamic Banking An Overview On The Review of ProblemsDocument21 pagesIssues and Problems of Islamic Banking An Overview On The Review of ProblemsMayra NiharNo ratings yet

- Research Paper On Islamic Banking in PakistanDocument4 pagesResearch Paper On Islamic Banking in Pakistaniwnlpjrif100% (1)

- Dissertation On Islamic Banking in IndiaDocument6 pagesDissertation On Islamic Banking in IndiaCustomPaperServiceUK100% (1)

- F Per 2012 InternationalDocument5 pagesF Per 2012 InternationalBrandy LeeNo ratings yet

- Dissertation On Islamic Banking in MauritiusDocument8 pagesDissertation On Islamic Banking in MauritiusBestWriteMyPaperWebsiteHighPoint100% (1)

- Issues and Problems of Islamic BankingDocument14 pagesIssues and Problems of Islamic Bankingziadiqbal19100% (9)

- Risk ManagementDocument26 pagesRisk ManagementAmal Ben RamdhaneNo ratings yet

- It's Time To Rethink Islamic Banking Regulation - Brink - The Edge of RiskDocument5 pagesIt's Time To Rethink Islamic Banking Regulation - Brink - The Edge of RiskHaHn MalekNo ratings yet

- Understanding Interest Rate Securities: An Eaglemont Career Book for StudentsFrom EverandUnderstanding Interest Rate Securities: An Eaglemont Career Book for StudentsNo ratings yet

- Weathering the Global Crisis: Can the Traits of Islamic Banking System Make a Difference?From EverandWeathering the Global Crisis: Can the Traits of Islamic Banking System Make a Difference?No ratings yet

- Organizational Theory Term Paper IdeasDocument6 pagesOrganizational Theory Term Paper IdeasHelpWithWritingPapersJackson100% (1)

- Term Paper Essay FormatDocument7 pagesTerm Paper Essay FormatHelpWithWritingPapersJackson100% (1)

- Example Term Paper LayoutDocument7 pagesExample Term Paper LayoutHelpWithWritingPapersJackson100% (1)

- Term Paper Interracial RelationshipsDocument5 pagesTerm Paper Interracial RelationshipsHelpWithWritingPapersJackson100% (1)

- Term Paper Filipino 2Document4 pagesTerm Paper Filipino 2HelpWithWritingPapersJackson100% (1)

- Dissertation Sur Le Bonheur AntigoneDocument5 pagesDissertation Sur Le Bonheur AntigoneHelpWithWritingPapersJackson100% (2)

- Hepatitis C DissertationDocument6 pagesHepatitis C DissertationHelpWithWritingPapersJackson100% (1)

- Fu Berlin Dissertation BiochemieDocument4 pagesFu Berlin Dissertation BiochemieHelpWithWritingPapersJackson100% (1)

- Dissertation ZweitstudiumDocument6 pagesDissertation ZweitstudiumHelpWithWritingPapersJackson100% (1)

- Bed Dissertation TitlesDocument6 pagesBed Dissertation TitlesHelpWithWritingPapersJackson100% (1)

- All But Dissertation TraductionDocument6 pagesAll But Dissertation TraductionHelpWithWritingPapersJackson100% (1)

- Dissertation Politics ExamplesDocument4 pagesDissertation Politics ExamplesHelpWithWritingPapersJackson100% (1)

- Dissertation Meaning WikipediaDocument7 pagesDissertation Meaning WikipediaHelpWithWritingPapersJackson100% (1)

- Dissertation Philosophique Sur La PassionDocument5 pagesDissertation Philosophique Sur La PassionHelpWithWritingPapersJackson100% (1)

- MSC Accounting Dissertation TopicsDocument5 pagesMSC Accounting Dissertation TopicsHelpWithWritingPapersJackson100% (1)

- Sport Business Dissertation IdeasDocument4 pagesSport Business Dissertation IdeasHelpWithWritingPapersJackson100% (1)

- Comment Faire Une Excellente Dissertation en PhilosophieDocument7 pagesComment Faire Une Excellente Dissertation en PhilosophieHelpWithWritingPapersJacksonNo ratings yet

- Sujet de Dissertation PoesieDocument5 pagesSujet de Dissertation PoesieHelpWithWritingPapersJackson100% (1)

- Islamic Interbank Money Market InstrumentDocument6 pagesIslamic Interbank Money Market InstrumentAnaszNazriNo ratings yet

- Islamic Finance Project-MutualFundsDocument42 pagesIslamic Finance Project-MutualFundsMuhammad Mamoon Iqbal0% (1)

- Abmf3213 Islamic Banking - Tutorial 1Document4 pagesAbmf3213 Islamic Banking - Tutorial 1Bom BiBiNo ratings yet

- An Analysis of Investment Activities of Al-Arafah Islami Bank LimitedDocument9 pagesAn Analysis of Investment Activities of Al-Arafah Islami Bank Limitedmd.jewel ranaNo ratings yet

- Akta Koperasi EnglishDocument57 pagesAkta Koperasi EnglishSuraiya Abd RahmanNo ratings yet

- Islamic Finance 1.1Document60 pagesIslamic Finance 1.1Macarandas İbrahimNo ratings yet

- Historic Judgement On RibaDocument15 pagesHistoric Judgement On RibaTaha BajwaNo ratings yet

- Islamic Financial Services Industry Stability Report 2019 - enDocument118 pagesIslamic Financial Services Industry Stability Report 2019 - enSophie PonomariovaNo ratings yet

- National Events: 67th Management Accountants DayDocument9 pagesNational Events: 67th Management Accountants DayGoopNo ratings yet

- Measuring The Impact of Islamic Microfinance Product, Qarz-E-Hasna, On Poverty Alleviation in Hyderabad DistrictDocument26 pagesMeasuring The Impact of Islamic Microfinance Product, Qarz-E-Hasna, On Poverty Alleviation in Hyderabad DistrictmairaNo ratings yet

- Shinta Amalina Hazrati Havidz: JAMBI, JUNE 4TH, 1992Document2 pagesShinta Amalina Hazrati Havidz: JAMBI, JUNE 4TH, 1992wulanda septianiNo ratings yet

- 374-Article Text-866-1-10-20190925 PDFDocument37 pages374-Article Text-866-1-10-20190925 PDFVita Citra MulyandiniNo ratings yet

- Islamic FinanceDocument27 pagesIslamic FinanceChing ZhiNo ratings yet

- Women I Deposit Account (Zehrah)Document2 pagesWomen I Deposit Account (Zehrah)kefiyalew BNo ratings yet

- Conventional and Islamic Banking System: Understanding Level of Knowledge Among Students in UitmDocument9 pagesConventional and Islamic Banking System: Understanding Level of Knowledge Among Students in UitmNurul HazwaniNo ratings yet

- Fin546 Topic 2 - Shari'Ah Contracts For Islamic Financial InstrumentsDocument69 pagesFin546 Topic 2 - Shari'Ah Contracts For Islamic Financial InstrumentsMuhd DanialNo ratings yet

- FinTech Sharia 3 1 PDFDocument51 pagesFinTech Sharia 3 1 PDFMahyuniNo ratings yet

- IFB Product Services - For induction-FINAL 11-13Document152 pagesIFB Product Services - For induction-FINAL 11-13tsadikNo ratings yet

- Illegality of Contract Under The Contracts Acts 1950 in Islamic Home Financing in Malaysia: Issues and Possible ReformDocument9 pagesIllegality of Contract Under The Contracts Acts 1950 in Islamic Home Financing in Malaysia: Issues and Possible ReformMaxwilliam DanielNo ratings yet

- Mezan Intership ReportDocument151 pagesMezan Intership ReportMurtaza AkmalNo ratings yet

- Musharakah Financing ModelDocument18 pagesMusharakah Financing ModelMuhd Basier Abd MutalibNo ratings yet

- List 20150331 PDFDocument131 pagesList 20150331 PDFHuesniNo ratings yet

- FINN 441 - Islamic Banking and Finance-Syed Aun Raza RizviDocument5 pagesFINN 441 - Islamic Banking and Finance-Syed Aun Raza RizvisaminaNo ratings yet

- AITABDocument25 pagesAITABalimul imranNo ratings yet

- Murabahah Product Structure: Title Application FADocument26 pagesMurabahah Product Structure: Title Application FAUmair UddinNo ratings yet

- Bisirat BekeleDocument90 pagesBisirat Bekeleselman bedruNo ratings yet

- Principle of Islamic FinanceDocument6 pagesPrinciple of Islamic FinanceumbreenNo ratings yet

- EL For BussinessDocument18 pagesEL For Bussinesshannguyen.31221021972No ratings yet