Download as pdf or txt

You might also like

- Edexcel IGCSE Economics Official GlossaryDocument9 pagesEdexcel IGCSE Economics Official GlossaryAshley Lau100% (2)

- Brita CaseDocument2 pagesBrita CasePraveen Abraham100% (1)

- Income Tax & VAT Amendment 2080-81Document25 pagesIncome Tax & VAT Amendment 2080-81pokhrelsuman165No ratings yet

- Major Changes / Amendments in Income Tax and Wealth-Tax Made in Budget 2009-2010Document9 pagesMajor Changes / Amendments in Income Tax and Wealth-Tax Made in Budget 2009-2010Irfan AhmadNo ratings yet

- Amendmens in BudgetDocument21 pagesAmendmens in Budgethudarahmanrsm87No ratings yet

- RSM India Newsflash - Employees Guidance On New Vs Old Tax Regime Individuals April 2020Document17 pagesRSM India Newsflash - Employees Guidance On New Vs Old Tax Regime Individuals April 2020Rohan JainNo ratings yet

- Tax Updates For June 2012 ExamsDocument37 pagesTax Updates For June 2012 ExamsShanky MalhotraNo ratings yet

- Decoding Indian Union BudgetDocument6 pagesDecoding Indian Union BudgetkumarNo ratings yet

- Payment of Bonus ActDocument9 pagesPayment of Bonus ActPradnya Ram PNo ratings yet

- Finance Act (NO.2) 2009: Prepared byDocument46 pagesFinance Act (NO.2) 2009: Prepared bymehul rakholiyaNo ratings yet

- Tax Updates For December 2011 31 10 2011Document35 pagesTax Updates For December 2011 31 10 2011Rakhi ChaubeyNo ratings yet

- Tax Updates For December 2011 31 10 2011Document35 pagesTax Updates For December 2011 31 10 2011gangadhardaNo ratings yet

- Tax Memorandum 2011finalDocument42 pagesTax Memorandum 2011finalbazitNo ratings yet

- Income Tax AmendmentDocument10 pagesIncome Tax AmendmentBashu GuragainNo ratings yet

- Deductions Income From BusinessDocument35 pagesDeductions Income From Businesssaveen thapaNo ratings yet

- Draft File (Shafin)Document11 pagesDraft File (Shafin)MD Shafin AhmedNo ratings yet

- Amendment DirectTax FA2013Document30 pagesAmendment DirectTax FA2013Bharat LuthraNo ratings yet

- Rates of Tax:-: Individual/HUF/AOP/Artificial Juridical PersonDocument8 pagesRates of Tax:-: Individual/HUF/AOP/Artificial Juridical PersonKiran KumarNo ratings yet

- AFC NotesDocument28 pagesAFC NotesFaisal Islam ButtNo ratings yet

- Union Budget 2013-14 - Highlights of Direct Tax ProposalsDocument5 pagesUnion Budget 2013-14 - Highlights of Direct Tax Proposalsankit403No ratings yet

- Taxation Theory QuestionsDocument7 pagesTaxation Theory QuestionsPrince kumarNo ratings yet

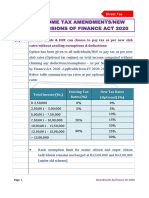

- Income Tax Amendments/New Provisions of Finance Act 2020Document46 pagesIncome Tax Amendments/New Provisions of Finance Act 2020shubhamworkNo ratings yet

- Bir Ruling No. Vat-419-2022 - Peza Vat and Non Vat HmoDocument7 pagesBir Ruling No. Vat-419-2022 - Peza Vat and Non Vat HmoJohnallen MarillaNo ratings yet

- Incomes Completely Exempt From Income TaxDocument7 pagesIncomes Completely Exempt From Income TaxMAHESHNo ratings yet

- 80TTB - Provides Deduction Benefit On Interest Income For Senior CitizensDocument1 page80TTB - Provides Deduction Benefit On Interest Income For Senior CitizensArjun VermaNo ratings yet

- Taxation 2 Prelim NotesDocument11 pagesTaxation 2 Prelim NotesMae TrabajoNo ratings yet

- Tax Rates 2078-79 - 20210719125127Document17 pagesTax Rates 2078-79 - 20210719125127shankarNo ratings yet

- 2022721177241469circular15of2002 23Document25 pages2022721177241469circular15of2002 23Ayan NoorNo ratings yet

- Finance Bill 2018Document36 pagesFinance Bill 2018Iddi KassiNo ratings yet

- Presentation TaxDocument25 pagesPresentation Taxsrihimanshu1988No ratings yet

- Income Tax ActDocument4 pagesIncome Tax ActgoborgonesNo ratings yet

- CAclubindia News - The SUPER Budget - AnalysisDocument15 pagesCAclubindia News - The SUPER Budget - AnalysisMahaveer DhelariyaNo ratings yet

- Deductions From Gross Total Income: HapterDocument20 pagesDeductions From Gross Total Income: HapterJAWED MOHAMMADNo ratings yet

- Create BillDocument31 pagesCreate BillJanet PaglingayenNo ratings yet

- Changes Made in Income Tax Act 2058Document10 pagesChanges Made in Income Tax Act 2058shankarNo ratings yet

- WorkersÆ Welfare FundDocument1 pageWorkersÆ Welfare Fundtmir_1No ratings yet

- Advance AccountsDocument25 pagesAdvance Accountsashish.jhaa756No ratings yet

- Exemptions & Tax Incentives (Act 896) - Power Point PresentationDocument50 pagesExemptions & Tax Incentives (Act 896) - Power Point PresentationGabrielNo ratings yet

- DHC Budget Snapshot 2023 24Document15 pagesDHC Budget Snapshot 2023 24Jigar ShahNo ratings yet

- AFF's Tax Memorandum - Changes in Finance Bill, 2023 (Pakistan)Document14 pagesAFF's Tax Memorandum - Changes in Finance Bill, 2023 (Pakistan)salahuddin ahmedNo ratings yet

- Salient Features For The Budget 2010-11Document11 pagesSalient Features For The Budget 2010-11kaashifhassanNo ratings yet

- NIRC V. TRAInDocument11 pagesNIRC V. TRAInJin De GuzmanNo ratings yet

- Budget 2012 TPDocument26 pagesBudget 2012 TPVimukthi TwkNo ratings yet

- Cajournal March2023 14Document6 pagesCajournal March2023 14S M SHEKARNo ratings yet

- The Income Tax (Am) Act, 2020Document10 pagesThe Income Tax (Am) Act, 2020TonyNo ratings yet

- A Book: Integrated Professional Competency Course (IPCC) Paper - 1: AccountingDocument12 pagesA Book: Integrated Professional Competency Course (IPCC) Paper - 1: AccountingSipoy SatishNo ratings yet

- Budget 2021Document15 pagesBudget 2021RohitKumarDiwakarNo ratings yet

- Lae DetailDocument9 pagesLae DetailUHY HASSAN NAEEM CO.No ratings yet

- Tax AmendmentsDocument109 pagesTax AmendmentsPrincess Hazel GriñoNo ratings yet

- FIN623 Midterm Subjective By:::: Usman Attari: Rules To Prevent Double Derivation and Double Deductions: Section 73Document10 pagesFIN623 Midterm Subjective By:::: Usman Attari: Rules To Prevent Double Derivation and Double Deductions: Section 73SunitaNo ratings yet

- TRABAHO Bill, House's Version of TRAIN 2Document6 pagesTRABAHO Bill, House's Version of TRAIN 2Andrew James Tan LeeNo ratings yet

- Industrial Enterprise Act, 2020Document15 pagesIndustrial Enterprise Act, 2020Santosh ChhetriNo ratings yet

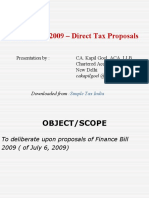

- Finance Bill 2009 - Direct Tax Proposals: Presentation By: CA. Kapil Goel, ACA, LLB Chartered Accountant New DelhiDocument43 pagesFinance Bill 2009 - Direct Tax Proposals: Presentation By: CA. Kapil Goel, ACA, LLB Chartered Accountant New DelhiPrasad KadamNo ratings yet

- EY CREATE ArticleDocument3 pagesEY CREATE ArticleTippyNo ratings yet

- Tax Amendment Acts, 2021 - UgandaDocument21 pagesTax Amendment Acts, 2021 - UgandaNyakuni NobertNo ratings yet

- DT Amendments May2024 and Nov2024_477c62a8-7eff-41ed-be34-76b0f9c4da5cDocument12 pagesDT Amendments May2024 and Nov2024_477c62a8-7eff-41ed-be34-76b0f9c4da5cALAQMARRAJNo ratings yet

- Maternity Benifit For WomenDocument10 pagesMaternity Benifit For WomenNirajNo ratings yet

- Income Tax AmendmentsNew Provisions of Finance Act 2020Document26 pagesIncome Tax AmendmentsNew Provisions of Finance Act 2020Piyush HarlalkaNo ratings yet

- Commentary On Impact of Finance Bill 2022 On IT SectorDocument10 pagesCommentary On Impact of Finance Bill 2022 On IT SectorurcapkNo ratings yet

- 11-134191-1987-Tio v. Videogram Regulatory BoardDocument9 pages11-134191-1987-Tio v. Videogram Regulatory Boarderic akoNo ratings yet

- OL 4 - BLT Study Text Suppliment 2021 - On New Tax AmmendmentsDocument28 pagesOL 4 - BLT Study Text Suppliment 2021 - On New Tax Ammendmentshte19031No ratings yet

- Industrial Enterprises Act 2020 (2076): A brief Overview and Comparative AnalysisFrom EverandIndustrial Enterprises Act 2020 (2076): A brief Overview and Comparative AnalysisNo ratings yet

- Marketing Plan PresentationDocument40 pagesMarketing Plan Presentationapi-493988205No ratings yet

- Moneymood 2023Document10 pagesMoneymood 2023AR HemantNo ratings yet

- BBM Lead-Magnet Beginner Popular-IndicatorsDocument10 pagesBBM Lead-Magnet Beginner Popular-IndicatorsFotis PapatheofanousNo ratings yet

- Problem Tree 1Document1 pageProblem Tree 1bhbfc project-1No ratings yet

- Family BudgetDocument3 pagesFamily BudgetThuoNo ratings yet

- TCW Module 3 Pre FinalDocument21 pagesTCW Module 3 Pre FinalMark Jade BurlatNo ratings yet

- Chapter 7 Strategy Formulation: Corporate Strategy: Strategic Management & Business Policy, 13e (Wheelen/Hunger)Document22 pagesChapter 7 Strategy Formulation: Corporate Strategy: Strategic Management & Business Policy, 13e (Wheelen/Hunger)Anonymous 7CxwuBUJz3No ratings yet

- Project On Effectiveness of Training Program OF Grasim Industries Limited Staple Fibre DivisionDocument52 pagesProject On Effectiveness of Training Program OF Grasim Industries Limited Staple Fibre Divisiondave_sourabhNo ratings yet

- ACC201 Seminar 1 - T06 - Grace KangDocument102 pagesACC201 Seminar 1 - T06 - Grace Kang潘 家德No ratings yet

- Intern Report - Sanima BankDocument11 pagesIntern Report - Sanima BankRajan ParajuliNo ratings yet

- 603 - Retail Banking: Prepayments Charges Collected by Branches Should Be Credited To Which Account?Document3 pages603 - Retail Banking: Prepayments Charges Collected by Branches Should Be Credited To Which Account?Harsh SinghalNo ratings yet

- Momentex LLC: Executive SummaryDocument25 pagesMomentex LLC: Executive SummaryEdoardo SmookedNo ratings yet

- GST Issues For Works Contract CA Yashwant Kasar - 31st July 2021Document73 pagesGST Issues For Works Contract CA Yashwant Kasar - 31st July 2021fintech ConsultancyNo ratings yet

- Answer To The Question No: 4.17: Summary InputDocument1 pageAnswer To The Question No: 4.17: Summary Inputtjarnob13No ratings yet

- Unit 4. 21st Century Literacies C. Savings and Banking D. Avoiding Financial Scams I.Introduction / RationaleDocument10 pagesUnit 4. 21st Century Literacies C. Savings and Banking D. Avoiding Financial Scams I.Introduction / RationaleLance AustriaNo ratings yet

- Cash Flow StatementDocument10 pagesCash Flow Statementabhishekanandsingh123goNo ratings yet

- Godrej Industries LimitedDocument17 pagesGodrej Industries LimitedsurajlalkushwahaNo ratings yet

- Danshui Plant No. 2Document10 pagesDanshui Plant No. 2AnandNo ratings yet

- I To B Ok AssignmentDocument4 pagesI To B Ok AssignmentHashim MalikNo ratings yet

- The Financial Management Practices of Small To Medium EnterprisesDocument22 pagesThe Financial Management Practices of Small To Medium EnterprisesalliahnahNo ratings yet

- Webinar ISEI Jakarta 21 Juli 2022 Nailul HUdaDocument50 pagesWebinar ISEI Jakarta 21 Juli 2022 Nailul HUdanora lizaNo ratings yet

- MBA-AFM Theory QBDocument18 pagesMBA-AFM Theory QBkanikaNo ratings yet

- Maceda Law Realty Installment Buyer Protection Act: Own House CondominiumDocument4 pagesMaceda Law Realty Installment Buyer Protection Act: Own House CondominiumsherwinNo ratings yet

- Warranties and Premiums Garison Music Emporium Carries A Wide Va PDFDocument1 pageWarranties and Premiums Garison Music Emporium Carries A Wide Va PDFAnbu jaromiaNo ratings yet

- Concept Paper ThesisDocument5 pagesConcept Paper ThesisSteven Z. CondeNo ratings yet

- Challenges To Implementing CECLDocument20 pagesChallenges To Implementing CECLDudenNo ratings yet

- MCQ's Total Marks 100: Sbp-Sbots (Get-Fs) Sunday, October 14, 2012Document13 pagesMCQ's Total Marks 100: Sbp-Sbots (Get-Fs) Sunday, October 14, 2012ShakeelNo ratings yet

- Macroeconomics EC2065 CHAPTER 6 - MONEY AND MONETARY POLICYDocument54 pagesMacroeconomics EC2065 CHAPTER 6 - MONEY AND MONETARY POLICYkaylaNo ratings yet