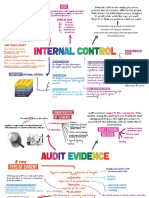

Topic 3 - Internal Control System

Topic 3 - Internal Control System

You might also like

- Iia Whitepaper - Control Assessment A Framework PDFDocument6 pagesIia Whitepaper - Control Assessment A Framework PDFPankaj GoyalNo ratings yet

- Internal Controls NotesDocument2 pagesInternal Controls NotesGraceila P. CalopeNo ratings yet

- CA Final Audit RISK ASSESSMENT AND INTERNAL CONTROL NotesDocument21 pagesCA Final Audit RISK ASSESSMENT AND INTERNAL CONTROL NotesSARASWATHI S100% (1)

- UNIT6-Audit SamplingDocument30 pagesUNIT6-Audit SamplingNoro100% (2)

- Topic 3 - Internal Control System - Part 2-StudentDocument9 pagesTopic 3 - Internal Control System - Part 2-StudentThinh NguyenNo ratings yet

- Topic 3 - Internal Control System - Part 2-StudentDocument9 pagesTopic 3 - Internal Control System - Part 2-Studentnnmnghi1409No ratings yet

- Relationship of Objectives To Risk Assessment & Control ActivitiesDocument2 pagesRelationship of Objectives To Risk Assessment & Control ActivitiesHazem El SayedNo ratings yet

- LU1 - Components of Internal ControlsDocument29 pagesLU1 - Components of Internal ControlsNqubekoNo ratings yet

- Risk Assesment & Internal ControlDocument56 pagesRisk Assesment & Internal Controlkaran kapadiaNo ratings yet

- Audcis ReviewerDocument3 pagesAudcis ReviewerSamantha CayananNo ratings yet

- AT.3608 - Considering Internal Controls and Assessing Control RiskDocument9 pagesAT.3608 - Considering Internal Controls and Assessing Control Riskrichshielanghag627No ratings yet

- PowerPoint PresentationDocument15 pagesPowerPoint PresentationMOHAMAD AMIRUL AINAN BIN BASHIR AHMAD MoeNo ratings yet

- Auditing ReviewerDocument2 pagesAuditing ReviewerQueenie de BorjaNo ratings yet

- AAI 2 Part 6A PSA 315 & PSA 265 N Internal Control - Rev PDFDocument101 pagesAAI 2 Part 6A PSA 315 & PSA 265 N Internal Control - Rev PDFAbigailNo ratings yet

- Chapter 3 Risk Assement & Internal ControlDocument54 pagesChapter 3 Risk Assement & Internal ControlRohit Kumar SantukaNo ratings yet

- Aa 3201Document4 pagesAa 3201Lance UrichNo ratings yet

- 04 Part-4Document7 pages04 Part-4Mary Joy RarangNo ratings yet

- IT Audit Mind Map chp5Document11 pagesIT Audit Mind Map chp5No IkhNo ratings yet

- INS3116 - CHAPTER 2 - Internal Control Framework - COSODocument25 pagesINS3116 - CHAPTER 2 - Internal Control Framework - COSOThuỳ Linh Bùi100% (1)

- Risk Based Audit of FSDocument1 pageRisk Based Audit of FSNavsNo ratings yet

- Chapter 6-8Document10 pagesChapter 6-8DeyNo ratings yet

- Auditing Assignment-2 Submitted To Keerti Mam Submitted by Bhavna PathakDocument9 pagesAuditing Assignment-2 Submitted To Keerti Mam Submitted by Bhavna PathakBhavnaNo ratings yet

- Types of Audits: Audit - An OverviewDocument31 pagesTypes of Audits: Audit - An OverviewRanel Clark D. TabiosNo ratings yet

- Chapter 11 Internal ControlDocument5 pagesChapter 11 Internal ControlCazia Mei JoverNo ratings yet

- Internal Control Midterm Reviewer QuizDocument4 pagesInternal Control Midterm Reviewer QuizjoshreydugyononNo ratings yet

- Unof Cis Chapter1 Test PrelimDocument6 pagesUnof Cis Chapter1 Test PrelimRoisu De KuriNo ratings yet

- Lesson 6 - Internal ControlsDocument5 pagesLesson 6 - Internal ControlsAllaina Uy BerbanoNo ratings yet

- Lecture 0824Document22 pagesLecture 0824jasonnumahnalkelNo ratings yet

- Wiley CPAexcel® EXAM REVIEW STUDY GUIDE JANUARY 2016 - AUDITING AND ATTESTATIONDocument1 pageWiley CPAexcel® EXAM REVIEW STUDY GUIDE JANUARY 2016 - AUDITING AND ATTESTATIONChristine GarciaNo ratings yet

- N1C FC Internal ControlsDocument30 pagesN1C FC Internal ControlsJehugem BayawaNo ratings yet

- AI - Modul 7 (INTERNAL CONTROL)Document30 pagesAI - Modul 7 (INTERNAL CONTROL)Lusi NuryantiNo ratings yet

- Consideratio N of Internal Control: Presented By: Hannah Binas Christine Mae FelixDocument12 pagesConsideratio N of Internal Control: Presented By: Hannah Binas Christine Mae FelixChristine Mae FelixNo ratings yet

- Chap 3 - Internal ControlDocument28 pagesChap 3 - Internal ControlhangNo ratings yet

- 01) Risk Based Internal Audit - CA. Rachana DaftaryDocument37 pages01) Risk Based Internal Audit - CA. Rachana DaftaryL N Murthy KapavarapuNo ratings yet

- In Risk Future of It Internal Controls NoexpDocument12 pagesIn Risk Future of It Internal Controls NoexpSridhair IyengarNo ratings yet

- Internal Control Over Financial Reporting: The Audit Opinion Formulation ProcessDocument5 pagesInternal Control Over Financial Reporting: The Audit Opinion Formulation ProcessRiri Canezo100% (1)

- AT 10 Understanding The Entity - S Internal ControlDocument7 pagesAT 10 Understanding The Entity - S Internal ControlPauline De VillaNo ratings yet

- 74937bos60526-Cp4 UnlockedDocument72 pages74937bos60526-Cp4 Unlockedhrudaya boysNo ratings yet

- 9 Internal Control-1Document26 pages9 Internal Control-1Muhammad FaizanNo ratings yet

- Ca PDFDocument3 pagesCa PDFHindutav aryaNo ratings yet

- KPMG MethodDocument88 pagesKPMG MethodAlexius Julio BrianNo ratings yet

- Slides - Chapter 9Document7 pagesSlides - Chapter 9Thu TrangNo ratings yet

- CH 4 - Risk AssessmentDocument35 pagesCH 4 - Risk AssessmentSUMIT SINGHNo ratings yet

- Overview of Internal ControlDocument11 pagesOverview of Internal ControlCutie HimawariNo ratings yet

- Tests of ControlsDocument40 pagesTests of ControlsMuhammad SaqibNo ratings yet

- Role of Auditing: Introduction - Regulatory FrameworkDocument19 pagesRole of Auditing: Introduction - Regulatory FrameworkGabrielle AndreaNo ratings yet

- Chapter 4 Internal ControlDocument28 pagesChapter 4 Internal Controlmt619405No ratings yet

- Module 3 Practice SetDocument6 pagesModule 3 Practice SetLee SuarezNo ratings yet

- Assurance Chapter-5 (04-09-2018)Document9 pagesAssurance Chapter-5 (04-09-2018)Shahid MahmudNo ratings yet

- Department of Accountancy: Consideration of Internal Control in An Audit of Financial StatementsDocument18 pagesDepartment of Accountancy: Consideration of Internal Control in An Audit of Financial StatementsMarian RoaNo ratings yet

- Internal ControlDocument6 pagesInternal ControlVarun jajalNo ratings yet

- MGT 209 - Overview of Internal ControlDocument8 pagesMGT 209 - Overview of Internal ControlCrystelNo ratings yet

- 25 - PH M Như Qu NH - 050609212168 - BTCNDocument18 pages25 - PH M Như Qu NH - 050609212168 - BTCNÝ PhạmNo ratings yet

- C3A Internal Control Inter AuditDocument9 pagesC3A Internal Control Inter Auditbroabhi143No ratings yet

- Risk and MaterialityDocument4 pagesRisk and MaterialitymsyllNo ratings yet

- Internal Control DocumentationDocument42 pagesInternal Control DocumentationJhoe Marie Balintag100% (1)

- At.3508 - Considering Internal Controls and Assessing Control RiskDocument9 pagesAt.3508 - Considering Internal Controls and Assessing Control RiskJohn MaynardNo ratings yet

- Chapter 6Document2 pagesChapter 6Blessed OrtegaNo ratings yet

- Lesson 6 - Internal Controls PDFDocument5 pagesLesson 6 - Internal Controls PDFAllaina Uy BerbanoNo ratings yet

- Auditing and Assurance Chapter 5 Flashcards - QuizletDocument7 pagesAuditing and Assurance Chapter 5 Flashcards - QuizletDieter LudwigNo ratings yet

- How to Comply with Sarbanes-Oxley Section 404: Assessing the Effectiveness of Internal ControlFrom EverandHow to Comply with Sarbanes-Oxley Section 404: Assessing the Effectiveness of Internal ControlNo ratings yet

- SEC Memorandum Circular No. 6 Series of 2009: Revised Code of Corporate GovernanceDocument13 pagesSEC Memorandum Circular No. 6 Series of 2009: Revised Code of Corporate GovernanceJames FigueroaNo ratings yet

- Chapter 2 Contol and Audit of AISDocument40 pagesChapter 2 Contol and Audit of AISyonas hussenNo ratings yet

- Air Force Audit Agency Report Listing 2002 To 2007 - Obtained Via FOIADocument344 pagesAir Force Audit Agency Report Listing 2002 To 2007 - Obtained Via FOIAProject On Government Oversight100% (3)

- Bank Risk ManagementDocument14 pagesBank Risk ManagementdeloarjkkniuhrmNo ratings yet

- Auditing, Kabucho MwangiDocument22 pagesAuditing, Kabucho MwangiKafonyi JohnNo ratings yet

- Audit MTP2 QP M24 @CAInterLegendsDocument17 pagesAudit MTP2 QP M24 @CAInterLegendssharmaansshumanNo ratings yet

- 1 - Learning PacketDocument15 pages1 - Learning PacketAlrac GarciaNo ratings yet

- Internal Audit Executive: Job DescriptionDocument2 pagesInternal Audit Executive: Job DescriptionSelva Bavani SelwaduraiNo ratings yet

- Risk Assessment and Response To Assessed RiskDocument8 pagesRisk Assessment and Response To Assessed RiskJanella PatriziaNo ratings yet

- Classification of Working PaperDocument15 pagesClassification of Working PaperHillary Canlas100% (1)

- Review of Internal Control Over Financial ReportingDocument20 pagesReview of Internal Control Over Financial ReportingMark Angelo Bustos100% (1)

- CIiiiiA Part 2 - Mock Exam 2Document54 pagesCIiiiiA Part 2 - Mock Exam 2aymen marzouki100% (1)

- Audit Engagement LetterDocument25 pagesAudit Engagement LetterAsal IslamNo ratings yet

- Practical AuditingDocument61 pagesPractical Auditinglloyd100% (1)

- General Controls: (Acc 401B - Auditing EDP Environment)Document9 pagesGeneral Controls: (Acc 401B - Auditing EDP Environment)Pines MacapagalNo ratings yet

- Chapter 1-Masters Forensic Accounting& AuditingDocument12 pagesChapter 1-Masters Forensic Accounting& Auditingskasaera76No ratings yet

- Stourbridge Investments v. DisneyDocument63 pagesStourbridge Investments v. DisneyTHRNo ratings yet

- AT 05 Auditor - S Response To Assessed RiskDocument4 pagesAT 05 Auditor - S Response To Assessed RiskjeromyNo ratings yet

- Ratio Analysis of AccDocument24 pagesRatio Analysis of Accsatish81980% (1)

- RFM Corp Annual ReportDocument169 pagesRFM Corp Annual ReportGab RielNo ratings yet

- DNB Bank Asa, Ny, Ny: Vice President of AccountingDocument3 pagesDNB Bank Asa, Ny, Ny: Vice President of Accountingkiran2710No ratings yet

- Chapter 5 (Rick Hayes) "Client Acceptance"Document19 pagesChapter 5 (Rick Hayes) "Client Acceptance"Joan AnindaNo ratings yet

- AFS2033 - Lecture 13 - Auditing in Islamic AccountingDocument26 pagesAFS2033 - Lecture 13 - Auditing in Islamic AccountingAna FienaNo ratings yet

- ASSIGNMENT in PRELIMINARY ENGAGEMENT ACTIVITIES AND PLANNINGDocument7 pagesASSIGNMENT in PRELIMINARY ENGAGEMENT ACTIVITIES AND PLANNINGLileth ViduyaNo ratings yet

- Psa 120Document14 pagesPsa 120Kimberly LimNo ratings yet

- Fraud in The Accounting Profession Accounting 1Document23 pagesFraud in The Accounting Profession Accounting 1karen hudesNo ratings yet

- Audit Module 1Document13 pagesAudit Module 1Danica GeneralaNo ratings yet

- Audit Committee Handbook 2023Document194 pagesAudit Committee Handbook 2023Ade SetiawanNo ratings yet

- Director of Internal Audit Job DescriptionDocument3 pagesDirector of Internal Audit Job DescriptionozlemNo ratings yet

Download as pdf or txt

You might also like

- Iia Whitepaper - Control Assessment A Framework PDFDocument6 pagesIia Whitepaper - Control Assessment A Framework PDFPankaj GoyalNo ratings yet

- Internal Controls NotesDocument2 pagesInternal Controls NotesGraceila P. CalopeNo ratings yet

- CA Final Audit RISK ASSESSMENT AND INTERNAL CONTROL NotesDocument21 pagesCA Final Audit RISK ASSESSMENT AND INTERNAL CONTROL NotesSARASWATHI S100% (1)

- UNIT6-Audit SamplingDocument30 pagesUNIT6-Audit SamplingNoro100% (2)

- Topic 3 - Internal Control System - Part 2-StudentDocument9 pagesTopic 3 - Internal Control System - Part 2-StudentThinh NguyenNo ratings yet

- Topic 3 - Internal Control System - Part 2-StudentDocument9 pagesTopic 3 - Internal Control System - Part 2-Studentnnmnghi1409No ratings yet

- Relationship of Objectives To Risk Assessment & Control ActivitiesDocument2 pagesRelationship of Objectives To Risk Assessment & Control ActivitiesHazem El SayedNo ratings yet

- LU1 - Components of Internal ControlsDocument29 pagesLU1 - Components of Internal ControlsNqubekoNo ratings yet

- Risk Assesment & Internal ControlDocument56 pagesRisk Assesment & Internal Controlkaran kapadiaNo ratings yet

- Audcis ReviewerDocument3 pagesAudcis ReviewerSamantha CayananNo ratings yet

- AT.3608 - Considering Internal Controls and Assessing Control RiskDocument9 pagesAT.3608 - Considering Internal Controls and Assessing Control Riskrichshielanghag627No ratings yet

- PowerPoint PresentationDocument15 pagesPowerPoint PresentationMOHAMAD AMIRUL AINAN BIN BASHIR AHMAD MoeNo ratings yet

- Auditing ReviewerDocument2 pagesAuditing ReviewerQueenie de BorjaNo ratings yet

- AAI 2 Part 6A PSA 315 & PSA 265 N Internal Control - Rev PDFDocument101 pagesAAI 2 Part 6A PSA 315 & PSA 265 N Internal Control - Rev PDFAbigailNo ratings yet

- Chapter 3 Risk Assement & Internal ControlDocument54 pagesChapter 3 Risk Assement & Internal ControlRohit Kumar SantukaNo ratings yet

- Aa 3201Document4 pagesAa 3201Lance UrichNo ratings yet

- 04 Part-4Document7 pages04 Part-4Mary Joy RarangNo ratings yet

- IT Audit Mind Map chp5Document11 pagesIT Audit Mind Map chp5No IkhNo ratings yet

- INS3116 - CHAPTER 2 - Internal Control Framework - COSODocument25 pagesINS3116 - CHAPTER 2 - Internal Control Framework - COSOThuỳ Linh Bùi100% (1)

- Risk Based Audit of FSDocument1 pageRisk Based Audit of FSNavsNo ratings yet

- Chapter 6-8Document10 pagesChapter 6-8DeyNo ratings yet

- Auditing Assignment-2 Submitted To Keerti Mam Submitted by Bhavna PathakDocument9 pagesAuditing Assignment-2 Submitted To Keerti Mam Submitted by Bhavna PathakBhavnaNo ratings yet

- Types of Audits: Audit - An OverviewDocument31 pagesTypes of Audits: Audit - An OverviewRanel Clark D. TabiosNo ratings yet

- Chapter 11 Internal ControlDocument5 pagesChapter 11 Internal ControlCazia Mei JoverNo ratings yet

- Internal Control Midterm Reviewer QuizDocument4 pagesInternal Control Midterm Reviewer QuizjoshreydugyononNo ratings yet

- Unof Cis Chapter1 Test PrelimDocument6 pagesUnof Cis Chapter1 Test PrelimRoisu De KuriNo ratings yet

- Lesson 6 - Internal ControlsDocument5 pagesLesson 6 - Internal ControlsAllaina Uy BerbanoNo ratings yet

- Lecture 0824Document22 pagesLecture 0824jasonnumahnalkelNo ratings yet

- Wiley CPAexcel® EXAM REVIEW STUDY GUIDE JANUARY 2016 - AUDITING AND ATTESTATIONDocument1 pageWiley CPAexcel® EXAM REVIEW STUDY GUIDE JANUARY 2016 - AUDITING AND ATTESTATIONChristine GarciaNo ratings yet

- N1C FC Internal ControlsDocument30 pagesN1C FC Internal ControlsJehugem BayawaNo ratings yet

- AI - Modul 7 (INTERNAL CONTROL)Document30 pagesAI - Modul 7 (INTERNAL CONTROL)Lusi NuryantiNo ratings yet

- Consideratio N of Internal Control: Presented By: Hannah Binas Christine Mae FelixDocument12 pagesConsideratio N of Internal Control: Presented By: Hannah Binas Christine Mae FelixChristine Mae FelixNo ratings yet

- Chap 3 - Internal ControlDocument28 pagesChap 3 - Internal ControlhangNo ratings yet

- 01) Risk Based Internal Audit - CA. Rachana DaftaryDocument37 pages01) Risk Based Internal Audit - CA. Rachana DaftaryL N Murthy KapavarapuNo ratings yet

- In Risk Future of It Internal Controls NoexpDocument12 pagesIn Risk Future of It Internal Controls NoexpSridhair IyengarNo ratings yet

- Internal Control Over Financial Reporting: The Audit Opinion Formulation ProcessDocument5 pagesInternal Control Over Financial Reporting: The Audit Opinion Formulation ProcessRiri Canezo100% (1)

- AT 10 Understanding The Entity - S Internal ControlDocument7 pagesAT 10 Understanding The Entity - S Internal ControlPauline De VillaNo ratings yet

- 74937bos60526-Cp4 UnlockedDocument72 pages74937bos60526-Cp4 Unlockedhrudaya boysNo ratings yet

- 9 Internal Control-1Document26 pages9 Internal Control-1Muhammad FaizanNo ratings yet

- Ca PDFDocument3 pagesCa PDFHindutav aryaNo ratings yet

- KPMG MethodDocument88 pagesKPMG MethodAlexius Julio BrianNo ratings yet

- Slides - Chapter 9Document7 pagesSlides - Chapter 9Thu TrangNo ratings yet

- CH 4 - Risk AssessmentDocument35 pagesCH 4 - Risk AssessmentSUMIT SINGHNo ratings yet

- Overview of Internal ControlDocument11 pagesOverview of Internal ControlCutie HimawariNo ratings yet

- Tests of ControlsDocument40 pagesTests of ControlsMuhammad SaqibNo ratings yet

- Role of Auditing: Introduction - Regulatory FrameworkDocument19 pagesRole of Auditing: Introduction - Regulatory FrameworkGabrielle AndreaNo ratings yet

- Chapter 4 Internal ControlDocument28 pagesChapter 4 Internal Controlmt619405No ratings yet

- Module 3 Practice SetDocument6 pagesModule 3 Practice SetLee SuarezNo ratings yet

- Assurance Chapter-5 (04-09-2018)Document9 pagesAssurance Chapter-5 (04-09-2018)Shahid MahmudNo ratings yet

- Department of Accountancy: Consideration of Internal Control in An Audit of Financial StatementsDocument18 pagesDepartment of Accountancy: Consideration of Internal Control in An Audit of Financial StatementsMarian RoaNo ratings yet

- Internal ControlDocument6 pagesInternal ControlVarun jajalNo ratings yet

- MGT 209 - Overview of Internal ControlDocument8 pagesMGT 209 - Overview of Internal ControlCrystelNo ratings yet

- 25 - PH M Như Qu NH - 050609212168 - BTCNDocument18 pages25 - PH M Như Qu NH - 050609212168 - BTCNÝ PhạmNo ratings yet

- C3A Internal Control Inter AuditDocument9 pagesC3A Internal Control Inter Auditbroabhi143No ratings yet

- Risk and MaterialityDocument4 pagesRisk and MaterialitymsyllNo ratings yet

- Internal Control DocumentationDocument42 pagesInternal Control DocumentationJhoe Marie Balintag100% (1)

- At.3508 - Considering Internal Controls and Assessing Control RiskDocument9 pagesAt.3508 - Considering Internal Controls and Assessing Control RiskJohn MaynardNo ratings yet

- Chapter 6Document2 pagesChapter 6Blessed OrtegaNo ratings yet

- Lesson 6 - Internal Controls PDFDocument5 pagesLesson 6 - Internal Controls PDFAllaina Uy BerbanoNo ratings yet

- Auditing and Assurance Chapter 5 Flashcards - QuizletDocument7 pagesAuditing and Assurance Chapter 5 Flashcards - QuizletDieter LudwigNo ratings yet

- How to Comply with Sarbanes-Oxley Section 404: Assessing the Effectiveness of Internal ControlFrom EverandHow to Comply with Sarbanes-Oxley Section 404: Assessing the Effectiveness of Internal ControlNo ratings yet

- SEC Memorandum Circular No. 6 Series of 2009: Revised Code of Corporate GovernanceDocument13 pagesSEC Memorandum Circular No. 6 Series of 2009: Revised Code of Corporate GovernanceJames FigueroaNo ratings yet

- Chapter 2 Contol and Audit of AISDocument40 pagesChapter 2 Contol and Audit of AISyonas hussenNo ratings yet

- Air Force Audit Agency Report Listing 2002 To 2007 - Obtained Via FOIADocument344 pagesAir Force Audit Agency Report Listing 2002 To 2007 - Obtained Via FOIAProject On Government Oversight100% (3)

- Bank Risk ManagementDocument14 pagesBank Risk ManagementdeloarjkkniuhrmNo ratings yet

- Auditing, Kabucho MwangiDocument22 pagesAuditing, Kabucho MwangiKafonyi JohnNo ratings yet

- Audit MTP2 QP M24 @CAInterLegendsDocument17 pagesAudit MTP2 QP M24 @CAInterLegendssharmaansshumanNo ratings yet

- 1 - Learning PacketDocument15 pages1 - Learning PacketAlrac GarciaNo ratings yet

- Internal Audit Executive: Job DescriptionDocument2 pagesInternal Audit Executive: Job DescriptionSelva Bavani SelwaduraiNo ratings yet

- Risk Assessment and Response To Assessed RiskDocument8 pagesRisk Assessment and Response To Assessed RiskJanella PatriziaNo ratings yet

- Classification of Working PaperDocument15 pagesClassification of Working PaperHillary Canlas100% (1)

- Review of Internal Control Over Financial ReportingDocument20 pagesReview of Internal Control Over Financial ReportingMark Angelo Bustos100% (1)

- CIiiiiA Part 2 - Mock Exam 2Document54 pagesCIiiiiA Part 2 - Mock Exam 2aymen marzouki100% (1)

- Audit Engagement LetterDocument25 pagesAudit Engagement LetterAsal IslamNo ratings yet

- Practical AuditingDocument61 pagesPractical Auditinglloyd100% (1)

- General Controls: (Acc 401B - Auditing EDP Environment)Document9 pagesGeneral Controls: (Acc 401B - Auditing EDP Environment)Pines MacapagalNo ratings yet

- Chapter 1-Masters Forensic Accounting& AuditingDocument12 pagesChapter 1-Masters Forensic Accounting& Auditingskasaera76No ratings yet

- Stourbridge Investments v. DisneyDocument63 pagesStourbridge Investments v. DisneyTHRNo ratings yet

- AT 05 Auditor - S Response To Assessed RiskDocument4 pagesAT 05 Auditor - S Response To Assessed RiskjeromyNo ratings yet

- Ratio Analysis of AccDocument24 pagesRatio Analysis of Accsatish81980% (1)

- RFM Corp Annual ReportDocument169 pagesRFM Corp Annual ReportGab RielNo ratings yet

- DNB Bank Asa, Ny, Ny: Vice President of AccountingDocument3 pagesDNB Bank Asa, Ny, Ny: Vice President of Accountingkiran2710No ratings yet

- Chapter 5 (Rick Hayes) "Client Acceptance"Document19 pagesChapter 5 (Rick Hayes) "Client Acceptance"Joan AnindaNo ratings yet

- AFS2033 - Lecture 13 - Auditing in Islamic AccountingDocument26 pagesAFS2033 - Lecture 13 - Auditing in Islamic AccountingAna FienaNo ratings yet

- ASSIGNMENT in PRELIMINARY ENGAGEMENT ACTIVITIES AND PLANNINGDocument7 pagesASSIGNMENT in PRELIMINARY ENGAGEMENT ACTIVITIES AND PLANNINGLileth ViduyaNo ratings yet

- Psa 120Document14 pagesPsa 120Kimberly LimNo ratings yet

- Fraud in The Accounting Profession Accounting 1Document23 pagesFraud in The Accounting Profession Accounting 1karen hudesNo ratings yet

- Audit Module 1Document13 pagesAudit Module 1Danica GeneralaNo ratings yet

- Audit Committee Handbook 2023Document194 pagesAudit Committee Handbook 2023Ade SetiawanNo ratings yet

- Director of Internal Audit Job DescriptionDocument3 pagesDirector of Internal Audit Job DescriptionozlemNo ratings yet