Financial Analysis With Key Observations

Financial Analysis With Key Observations

You might also like

- Eopt Act Comparative SummaryDocument6 pagesEopt Act Comparative Summarybbc.moniqueNo ratings yet

- Tax Rebate Calculator of Salaried Class Indviduals 2013-14Document4 pagesTax Rebate Calculator of Salaried Class Indviduals 2013-14waheedNo ratings yet

- Income Taxes: Basic ConceptsDocument7 pagesIncome Taxes: Basic ConceptsTrisha Mae Mendoza MacalinoNo ratings yet

- 1 Accounting For Taxation: Section OverviewDocument36 pages1 Accounting For Taxation: Section Overviewsimran jeswaniNo ratings yet

- Tax LawsDocument7 pagesTax Lawsbesong marlonNo ratings yet

- Chapter 3 2023Document7 pagesChapter 3 2023Linh DieuNo ratings yet

- IAS 12 BinderDocument20 pagesIAS 12 BinderUmer Shah100% (1)

- Income Tax Notes-IAS 12Document11 pagesIncome Tax Notes-IAS 12mehdi.jjh313No ratings yet

- Note On Budget Proposals-2020Document7 pagesNote On Budget Proposals-2020Mayur VartakNo ratings yet

- IAS-12 Lecture NotesDocument11 pagesIAS-12 Lecture NotesAli OptimisticNo ratings yet

- Screenshot 2023-03-28 at 9.42.11 AMDocument38 pagesScreenshot 2023-03-28 at 9.42.11 AMKinza NawazNo ratings yet

- ESS Guidance - DocDocument5 pagesESS Guidance - DocEr Sundeep RachakondaNo ratings yet

- Accounting For Income Tax FinDocument8 pagesAccounting For Income Tax FinAmparo ReyesNo ratings yet

- 2 - CIT - Tax AdjustmentsDocument56 pages2 - CIT - Tax AdjustmentsMaricarmen SilvaNo ratings yet

- Manage Taxes - 8Document1 pageManage Taxes - 8I'm RangaNo ratings yet

- Chapter 1 - Income TaxDocument30 pagesChapter 1 - Income TaxKhanh LinhNo ratings yet

- Report of The DirectorsDocument5 pagesReport of The Directorspeter9836935619No ratings yet

- Corporation Tax Liquidation Scheme 2Document3 pagesCorporation Tax Liquidation Scheme 2Lisa Weng zhangNo ratings yet

- Pas 12Document27 pagesPas 12Princess Jullyn ClaudioNo ratings yet

- Wiley Financial Management Association InternationalDocument7 pagesWiley Financial Management Association InternationalGeorge IonutNo ratings yet

- X120 Cslides 19Document19 pagesX120 Cslides 19Jowelyn Cabilleda AriasNo ratings yet

- Earnings Non Recurring Deferred TaxDocument39 pagesEarnings Non Recurring Deferred TaxKeith YohanesNo ratings yet

- Strategic Tax Management (Final Period Assignment Quiz)Document4 pagesStrategic Tax Management (Final Period Assignment Quiz)Nelia AbellanoNo ratings yet

- Ias 12Document27 pagesIas 12Kuti KuriNo ratings yet

- Salient Features of Income Tax Act 2023Document79 pagesSalient Features of Income Tax Act 2023Md. Abdullah Al ImranNo ratings yet

- Ias 12 Income TaxesDocument52 pagesIas 12 Income TaxesJames MutarauswaNo ratings yet

- (Name of Registered Business Entity) Annual Tax Incentives Report-Income-Based Tax Incentives For Calendar/Fiscal YearDocument5 pages(Name of Registered Business Entity) Annual Tax Incentives Report-Income-Based Tax Incentives For Calendar/Fiscal YearRoui Jean VillarNo ratings yet

- Income Statement PDFDocument4 pagesIncome Statement PDFMargarete DelvalleNo ratings yet

- Chapter 10: Income TaxDocument32 pagesChapter 10: Income TaxNgô Thành DanhNo ratings yet

- Suggested Answer - IND AS 103 & 12Document14 pagesSuggested Answer - IND AS 103 & 12pratikdubey9586No ratings yet

- Statement of CashflowsDocument2 pagesStatement of CashflowsLove IslamNo ratings yet

- Nondeductible Expenses Are Added Nontaxable Revenues Are Deducted ToDocument1 pageNondeductible Expenses Are Added Nontaxable Revenues Are Deducted ToMarvin MarianoNo ratings yet

- FR - Ias 12Document1 pageFR - Ias 12Zubair JallohNo ratings yet

- RRDocument1 pageRRNatesvar RajNo ratings yet

- PAS 12 Accounting For Income TaxDocument17 pagesPAS 12 Accounting For Income TaxReynaldNo ratings yet

- Explanations of Deferred Tax Principle DisclosureDocument3 pagesExplanations of Deferred Tax Principle Disclosureokuhle4002No ratings yet

- 2022, Tulane, FM, LeverageDocument6 pages2022, Tulane, FM, LeverageJhonnatan Ruiz EustaquioNo ratings yet

- Tabel Jurnal 2Document18 pagesTabel Jurnal 2Muhammad Dzikri HadiyarroyyanNo ratings yet

- Annual Revenue Performance: Revenue More Than Doubles in Ten YearsDocument1 pageAnnual Revenue Performance: Revenue More Than Doubles in Ten YearsBrampizzy LiboyiNo ratings yet

- 14Document106 pages14Alex liaoNo ratings yet

- Capsule Corporation Excel-2Document449 pagesCapsule Corporation Excel-2Nicola ZucchettiNo ratings yet

- Taxation Exam Part IIDocument14 pagesTaxation Exam Part IIGabriel Christopher MembrilloNo ratings yet

- Ind As 12Document5 pagesInd As 12Akshayaa KarthikaNo ratings yet

- Income TaxesDocument17 pagesIncome TaxesThomas HutahaeanNo ratings yet

- FRA - 10-Income TaxesDocument35 pagesFRA - 10-Income Taxeskmayank0723No ratings yet

- Monetary Limit - Rates To Remember in GSTDocument15 pagesMonetary Limit - Rates To Remember in GSTtholsjk14No ratings yet

- Cfas - FinalsDocument9 pagesCfas - FinalsawitakintoNo ratings yet

- 9 Mas Capital Budgeting Sessions 3 4Document14 pages9 Mas Capital Budgeting Sessions 3 4seya dummyNo ratings yet

- POWIBA NOTICE CORPORATE TAX AssessmentDocument2 pagesPOWIBA NOTICE CORPORATE TAX AssessmentHassan OmaryNo ratings yet

- FIM Exel 1 1Document46 pagesFIM Exel 1 1Bao Khanh HaNo ratings yet

- IAS 12 - Income Taxes - Measurement - Permanent DifferencesDocument4 pagesIAS 12 - Income Taxes - Measurement - Permanent DifferencesReenestus DumeniNo ratings yet

- Formal Letter of Demand: Republic of The Philippines Department of Finance Bureau of Internal RevenueDocument3 pagesFormal Letter of Demand: Republic of The Philippines Department of Finance Bureau of Internal RevenueDominic Dela VegaNo ratings yet

- Chương 1011Document7 pagesChương 1011Lê Thị Phương NhungNo ratings yet

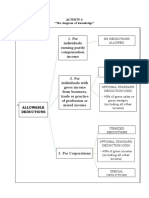

- For Individuals Earning Purely Compensation Income: Allowable DeductionsDocument4 pagesFor Individuals Earning Purely Compensation Income: Allowable DeductionsJAN FEVRIER OLETENo ratings yet

- Business PlanDocument14 pagesBusiness PlanghadaNo ratings yet

- Test 9 SolutionDocument3 pagesTest 9 Solutionlalshahbaz57No ratings yet

- Ias 12 Income TaxesDocument70 pagesIas 12 Income Taxeszulfi100% (1)

- CHAPTER 4 StudentDocument12 pagesCHAPTER 4 Studentfelicia tanNo ratings yet

- ACC2001 Lecture 4Document53 pagesACC2001 Lecture 4michael krueseiNo ratings yet

- Activity No 4Document1 pageActivity No 4Roel P. Dolaypan Jr.No ratings yet

- 28 February 2024 Letter To Juditte L. AsuncionDocument1 page28 February 2024 Letter To Juditte L. AsuncionRoel P. Dolaypan Jr.No ratings yet

- 01 March 2024 Funding For Pre Registrtaion of AC Student CooperativeDocument8 pages01 March 2024 Funding For Pre Registrtaion of AC Student CooperativeRoel P. Dolaypan Jr.No ratings yet

- FM ELECT-3 Module EDITEDDocument11 pagesFM ELECT-3 Module EDITEDRoel P. Dolaypan Jr.No ratings yet

- Orientation To Quality Management System (QMS)Document20 pagesOrientation To Quality Management System (QMS)Roel P. Dolaypan Jr.No ratings yet

- Guidelines For Grant Applicants - CSO Call 2024Document36 pagesGuidelines For Grant Applicants - CSO Call 2024Roel P. Dolaypan Jr.No ratings yet

- RUBRICS For Basic PricingDocument2 pagesRUBRICS For Basic PricingRoel P. Dolaypan Jr.No ratings yet

- Provincial Cooperative and Enterprise Development Office: Section 1. TitleDocument6 pagesProvincial Cooperative and Enterprise Development Office: Section 1. TitleRoel P. Dolaypan Jr.No ratings yet

- Solution Tree KanuDocument2 pagesSolution Tree KanuRoel P. Dolaypan Jr.No ratings yet

- Lesson Guide CoopmgmntDocument3 pagesLesson Guide CoopmgmntRoel P. Dolaypan Jr.No ratings yet

- ReEntryPlanFormat PCNDocument1 pageReEntryPlanFormat PCNRoel P. Dolaypan Jr.No ratings yet

- FM ELECT-3 ModuleDocument18 pagesFM ELECT-3 ModuleRoel P. Dolaypan Jr.No ratings yet

- Gantt ChartDocument1 pageGantt ChartRoel P. Dolaypan Jr.No ratings yet

- Document and Report Writeshop & QMS OrientationDocument11 pagesDocument and Report Writeshop & QMS OrientationRoel P. Dolaypan Jr.No ratings yet

- Needed-Documents BSBADocument1 pageNeeded-Documents BSBARoel P. Dolaypan Jr.No ratings yet

- Programme 1Document1 pageProgramme 1Roel P. Dolaypan Jr.No ratings yet

- Letter Cooperative and Entrepreneurship ForumDocument4 pagesLetter Cooperative and Entrepreneurship ForumRoel P. Dolaypan Jr.No ratings yet

- Letter Cooperative and Entrepreneurship ForumDocument4 pagesLetter Cooperative and Entrepreneurship ForumRoel P. Dolaypan Jr.No ratings yet

- CAARTS Template Import QuestionsDocument3 pagesCAARTS Template Import QuestionsRoel P. Dolaypan Jr.No ratings yet

- BODs Mock Meeting Using Parliamentary ProceduresDocument3 pagesBODs Mock Meeting Using Parliamentary ProceduresRoel P. Dolaypan Jr.No ratings yet

- INTRODUCTION OF Asaki SenseiDocument1 pageINTRODUCTION OF Asaki SenseiRoel P. Dolaypan Jr.No ratings yet

- Proposed Rules and Regulations For The Ammungan Space RentalDocument3 pagesProposed Rules and Regulations For The Ammungan Space RentalRoel P. Dolaypan Jr.No ratings yet

- COMMENTS On Topic No. 1Document4 pagesCOMMENTS On Topic No. 1Roel P. Dolaypan Jr.No ratings yet

- Module 2Document19 pagesModule 2Roel P. Dolaypan Jr.No ratings yet

- Xxxsyllabus - Pricingstrat 22 23 3Document2 pagesXxxsyllabus - Pricingstrat 22 23 3Roel P. Dolaypan Jr.No ratings yet

- Conceptual Framework 1.1Document1 pageConceptual Framework 1.1Roel P. Dolaypan Jr.No ratings yet

- History of The CooperativeDocument28 pagesHistory of The CooperativeRoel P. Dolaypan Jr.No ratings yet

- Problem TreeDocument1 pageProblem TreeRoel P. Dolaypan Jr.No ratings yet

- Financial AnalysisDocument4 pagesFinancial AnalysisRoel P. Dolaypan Jr.No ratings yet

- Module 1Document11 pagesModule 1Roel P. Dolaypan Jr.No ratings yet

- Municipal Sustainability PlanDocument3 pagesMunicipal Sustainability PlanJoem'z Burlasa-Amoto Esler-DionaldoNo ratings yet

- Economic Environment (1) PPTDocument40 pagesEconomic Environment (1) PPTHimangi GuptaNo ratings yet

- Top Down and Bottoms Up Approach in BudgetingDocument7 pagesTop Down and Bottoms Up Approach in BudgetingChetan SaxenaNo ratings yet

- Guidelines On The Appropriation, Release, PlanningDocument20 pagesGuidelines On The Appropriation, Release, PlanningCamila Anne GambanNo ratings yet

- The Muddling Nineties: Benazir Bhutto and Nawaz Sharif (1993-1999)Document15 pagesThe Muddling Nineties: Benazir Bhutto and Nawaz Sharif (1993-1999)Shameel IrshadNo ratings yet

- Integrating Tax Expenditures Into The Budget Process, by Len BurmanDocument23 pagesIntegrating Tax Expenditures Into The Budget Process, by Len BurmanKaitlin LeeNo ratings yet

- 16th Mindanao Invitation PB CDODocument1 page16th Mindanao Invitation PB CDOChristine BernalNo ratings yet

- Enrile Welcomes Probe of Port IreneDocument9 pagesEnrile Welcomes Probe of Port IreneJPA-BJMPIX ZCZSICNo ratings yet

- Project Management - AssignmentDocument7 pagesProject Management - AssignmentAkshatNo ratings yet

- Letter of Undertaking To PS WorksDocument2 pagesLetter of Undertaking To PS Worksmac timothyNo ratings yet

- CoB 100th RS June 24 2024 2.30PMDocument4 pagesCoB 100th RS June 24 2024 2.30PMDiane Amielle Armamento - VillamielNo ratings yet

- The Code of Putinism Brian D Taylor Full ChapterDocument67 pagesThe Code of Putinism Brian D Taylor Full Chapterrobert.beam905100% (5)

- IMF Reformation of BangladeshDocument125 pagesIMF Reformation of BangladeshSajjad HossainNo ratings yet

- House Bill 2883Document3 pagesHouse Bill 2883Kristofer PlonaNo ratings yet

- Public FinanceDocument2 pagesPublic FinanceNandhuNo ratings yet

- Government Accounting: Accounting For Non-Profit OrganizationsDocument88 pagesGovernment Accounting: Accounting For Non-Profit OrganizationsDe GuzmanNo ratings yet

- Karnataka Budget AnalysisDocument4 pagesKarnataka Budget AnalysisV GowdaNo ratings yet

- India Socio Politics & Economic System Current Affairs212 - Xid-3384634 - 1Document4 pagesIndia Socio Politics & Economic System Current Affairs212 - Xid-3384634 - 1Shubham ChitkaraNo ratings yet

- How To Write Project Proposal Form and StyleDocument22 pagesHow To Write Project Proposal Form and StyleMeynard MagsinoNo ratings yet

- TSA Loose Change Report 2019Document11 pagesTSA Loose Change Report 2019Adam ForgieNo ratings yet

- Reddy Sir Basics About Fiscal PolicyDocument8 pagesReddy Sir Basics About Fiscal PolicyD PNo ratings yet

- SK Appropriation Ordinance 2023Document3 pagesSK Appropriation Ordinance 2023Cazy Mel EugenioNo ratings yet

- App-Sbfp New NormalDocument1 pageApp-Sbfp New NormalGine FrencilloNo ratings yet

- Farmers Market Funding LetterDocument1 pageFarmers Market Funding LetterRose WhiteNo ratings yet

- Purpose: ObjectiveDocument5 pagesPurpose: Objectiveteck yuNo ratings yet

- Don't Come Home America: The Case Against RetrenchmentDocument45 pagesDon't Come Home America: The Case Against RetrenchmentChucky TNo ratings yet

- Reso 002-2023Document3 pagesReso 002-2023Andy CadanganNo ratings yet

- Assignment 3 Financial Analysis Graphs Excel TemplateDocument3 pagesAssignment 3 Financial Analysis Graphs Excel TemplateDylan VanslochterenNo ratings yet

- Checklist of Requirements: Shoreland Development ClearanceDocument1 pageChecklist of Requirements: Shoreland Development ClearanceEmitz HernandezNo ratings yet

- Jurnal Ilmiah Administrasi Publik (JIAP) : Foreign Aid and Economic Development in IndonesiaDocument5 pagesJurnal Ilmiah Administrasi Publik (JIAP) : Foreign Aid and Economic Development in IndonesiaMechanical Div. EPC-HKNo ratings yet

Download as pdf or txt

You might also like

- Eopt Act Comparative SummaryDocument6 pagesEopt Act Comparative Summarybbc.moniqueNo ratings yet

- Tax Rebate Calculator of Salaried Class Indviduals 2013-14Document4 pagesTax Rebate Calculator of Salaried Class Indviduals 2013-14waheedNo ratings yet

- Income Taxes: Basic ConceptsDocument7 pagesIncome Taxes: Basic ConceptsTrisha Mae Mendoza MacalinoNo ratings yet

- 1 Accounting For Taxation: Section OverviewDocument36 pages1 Accounting For Taxation: Section Overviewsimran jeswaniNo ratings yet

- Tax LawsDocument7 pagesTax Lawsbesong marlonNo ratings yet

- Chapter 3 2023Document7 pagesChapter 3 2023Linh DieuNo ratings yet

- IAS 12 BinderDocument20 pagesIAS 12 BinderUmer Shah100% (1)

- Income Tax Notes-IAS 12Document11 pagesIncome Tax Notes-IAS 12mehdi.jjh313No ratings yet

- Note On Budget Proposals-2020Document7 pagesNote On Budget Proposals-2020Mayur VartakNo ratings yet

- IAS-12 Lecture NotesDocument11 pagesIAS-12 Lecture NotesAli OptimisticNo ratings yet

- Screenshot 2023-03-28 at 9.42.11 AMDocument38 pagesScreenshot 2023-03-28 at 9.42.11 AMKinza NawazNo ratings yet

- ESS Guidance - DocDocument5 pagesESS Guidance - DocEr Sundeep RachakondaNo ratings yet

- Accounting For Income Tax FinDocument8 pagesAccounting For Income Tax FinAmparo ReyesNo ratings yet

- 2 - CIT - Tax AdjustmentsDocument56 pages2 - CIT - Tax AdjustmentsMaricarmen SilvaNo ratings yet

- Manage Taxes - 8Document1 pageManage Taxes - 8I'm RangaNo ratings yet

- Chapter 1 - Income TaxDocument30 pagesChapter 1 - Income TaxKhanh LinhNo ratings yet

- Report of The DirectorsDocument5 pagesReport of The Directorspeter9836935619No ratings yet

- Corporation Tax Liquidation Scheme 2Document3 pagesCorporation Tax Liquidation Scheme 2Lisa Weng zhangNo ratings yet

- Pas 12Document27 pagesPas 12Princess Jullyn ClaudioNo ratings yet

- Wiley Financial Management Association InternationalDocument7 pagesWiley Financial Management Association InternationalGeorge IonutNo ratings yet

- X120 Cslides 19Document19 pagesX120 Cslides 19Jowelyn Cabilleda AriasNo ratings yet

- Earnings Non Recurring Deferred TaxDocument39 pagesEarnings Non Recurring Deferred TaxKeith YohanesNo ratings yet

- Strategic Tax Management (Final Period Assignment Quiz)Document4 pagesStrategic Tax Management (Final Period Assignment Quiz)Nelia AbellanoNo ratings yet

- Ias 12Document27 pagesIas 12Kuti KuriNo ratings yet

- Salient Features of Income Tax Act 2023Document79 pagesSalient Features of Income Tax Act 2023Md. Abdullah Al ImranNo ratings yet

- Ias 12 Income TaxesDocument52 pagesIas 12 Income TaxesJames MutarauswaNo ratings yet

- (Name of Registered Business Entity) Annual Tax Incentives Report-Income-Based Tax Incentives For Calendar/Fiscal YearDocument5 pages(Name of Registered Business Entity) Annual Tax Incentives Report-Income-Based Tax Incentives For Calendar/Fiscal YearRoui Jean VillarNo ratings yet

- Income Statement PDFDocument4 pagesIncome Statement PDFMargarete DelvalleNo ratings yet

- Chapter 10: Income TaxDocument32 pagesChapter 10: Income TaxNgô Thành DanhNo ratings yet

- Suggested Answer - IND AS 103 & 12Document14 pagesSuggested Answer - IND AS 103 & 12pratikdubey9586No ratings yet

- Statement of CashflowsDocument2 pagesStatement of CashflowsLove IslamNo ratings yet

- Nondeductible Expenses Are Added Nontaxable Revenues Are Deducted ToDocument1 pageNondeductible Expenses Are Added Nontaxable Revenues Are Deducted ToMarvin MarianoNo ratings yet

- FR - Ias 12Document1 pageFR - Ias 12Zubair JallohNo ratings yet

- RRDocument1 pageRRNatesvar RajNo ratings yet

- PAS 12 Accounting For Income TaxDocument17 pagesPAS 12 Accounting For Income TaxReynaldNo ratings yet

- Explanations of Deferred Tax Principle DisclosureDocument3 pagesExplanations of Deferred Tax Principle Disclosureokuhle4002No ratings yet

- 2022, Tulane, FM, LeverageDocument6 pages2022, Tulane, FM, LeverageJhonnatan Ruiz EustaquioNo ratings yet

- Tabel Jurnal 2Document18 pagesTabel Jurnal 2Muhammad Dzikri HadiyarroyyanNo ratings yet

- Annual Revenue Performance: Revenue More Than Doubles in Ten YearsDocument1 pageAnnual Revenue Performance: Revenue More Than Doubles in Ten YearsBrampizzy LiboyiNo ratings yet

- 14Document106 pages14Alex liaoNo ratings yet

- Capsule Corporation Excel-2Document449 pagesCapsule Corporation Excel-2Nicola ZucchettiNo ratings yet

- Taxation Exam Part IIDocument14 pagesTaxation Exam Part IIGabriel Christopher MembrilloNo ratings yet

- Ind As 12Document5 pagesInd As 12Akshayaa KarthikaNo ratings yet

- Income TaxesDocument17 pagesIncome TaxesThomas HutahaeanNo ratings yet

- FRA - 10-Income TaxesDocument35 pagesFRA - 10-Income Taxeskmayank0723No ratings yet

- Monetary Limit - Rates To Remember in GSTDocument15 pagesMonetary Limit - Rates To Remember in GSTtholsjk14No ratings yet

- Cfas - FinalsDocument9 pagesCfas - FinalsawitakintoNo ratings yet

- 9 Mas Capital Budgeting Sessions 3 4Document14 pages9 Mas Capital Budgeting Sessions 3 4seya dummyNo ratings yet

- POWIBA NOTICE CORPORATE TAX AssessmentDocument2 pagesPOWIBA NOTICE CORPORATE TAX AssessmentHassan OmaryNo ratings yet

- FIM Exel 1 1Document46 pagesFIM Exel 1 1Bao Khanh HaNo ratings yet

- IAS 12 - Income Taxes - Measurement - Permanent DifferencesDocument4 pagesIAS 12 - Income Taxes - Measurement - Permanent DifferencesReenestus DumeniNo ratings yet

- Formal Letter of Demand: Republic of The Philippines Department of Finance Bureau of Internal RevenueDocument3 pagesFormal Letter of Demand: Republic of The Philippines Department of Finance Bureau of Internal RevenueDominic Dela VegaNo ratings yet

- Chương 1011Document7 pagesChương 1011Lê Thị Phương NhungNo ratings yet

- For Individuals Earning Purely Compensation Income: Allowable DeductionsDocument4 pagesFor Individuals Earning Purely Compensation Income: Allowable DeductionsJAN FEVRIER OLETENo ratings yet

- Business PlanDocument14 pagesBusiness PlanghadaNo ratings yet

- Test 9 SolutionDocument3 pagesTest 9 Solutionlalshahbaz57No ratings yet

- Ias 12 Income TaxesDocument70 pagesIas 12 Income Taxeszulfi100% (1)

- CHAPTER 4 StudentDocument12 pagesCHAPTER 4 Studentfelicia tanNo ratings yet

- ACC2001 Lecture 4Document53 pagesACC2001 Lecture 4michael krueseiNo ratings yet

- Activity No 4Document1 pageActivity No 4Roel P. Dolaypan Jr.No ratings yet

- 28 February 2024 Letter To Juditte L. AsuncionDocument1 page28 February 2024 Letter To Juditte L. AsuncionRoel P. Dolaypan Jr.No ratings yet

- 01 March 2024 Funding For Pre Registrtaion of AC Student CooperativeDocument8 pages01 March 2024 Funding For Pre Registrtaion of AC Student CooperativeRoel P. Dolaypan Jr.No ratings yet

- FM ELECT-3 Module EDITEDDocument11 pagesFM ELECT-3 Module EDITEDRoel P. Dolaypan Jr.No ratings yet

- Orientation To Quality Management System (QMS)Document20 pagesOrientation To Quality Management System (QMS)Roel P. Dolaypan Jr.No ratings yet

- Guidelines For Grant Applicants - CSO Call 2024Document36 pagesGuidelines For Grant Applicants - CSO Call 2024Roel P. Dolaypan Jr.No ratings yet

- RUBRICS For Basic PricingDocument2 pagesRUBRICS For Basic PricingRoel P. Dolaypan Jr.No ratings yet

- Provincial Cooperative and Enterprise Development Office: Section 1. TitleDocument6 pagesProvincial Cooperative and Enterprise Development Office: Section 1. TitleRoel P. Dolaypan Jr.No ratings yet

- Solution Tree KanuDocument2 pagesSolution Tree KanuRoel P. Dolaypan Jr.No ratings yet

- Lesson Guide CoopmgmntDocument3 pagesLesson Guide CoopmgmntRoel P. Dolaypan Jr.No ratings yet

- ReEntryPlanFormat PCNDocument1 pageReEntryPlanFormat PCNRoel P. Dolaypan Jr.No ratings yet

- FM ELECT-3 ModuleDocument18 pagesFM ELECT-3 ModuleRoel P. Dolaypan Jr.No ratings yet

- Gantt ChartDocument1 pageGantt ChartRoel P. Dolaypan Jr.No ratings yet

- Document and Report Writeshop & QMS OrientationDocument11 pagesDocument and Report Writeshop & QMS OrientationRoel P. Dolaypan Jr.No ratings yet

- Needed-Documents BSBADocument1 pageNeeded-Documents BSBARoel P. Dolaypan Jr.No ratings yet

- Programme 1Document1 pageProgramme 1Roel P. Dolaypan Jr.No ratings yet

- Letter Cooperative and Entrepreneurship ForumDocument4 pagesLetter Cooperative and Entrepreneurship ForumRoel P. Dolaypan Jr.No ratings yet

- Letter Cooperative and Entrepreneurship ForumDocument4 pagesLetter Cooperative and Entrepreneurship ForumRoel P. Dolaypan Jr.No ratings yet

- CAARTS Template Import QuestionsDocument3 pagesCAARTS Template Import QuestionsRoel P. Dolaypan Jr.No ratings yet

- BODs Mock Meeting Using Parliamentary ProceduresDocument3 pagesBODs Mock Meeting Using Parliamentary ProceduresRoel P. Dolaypan Jr.No ratings yet

- INTRODUCTION OF Asaki SenseiDocument1 pageINTRODUCTION OF Asaki SenseiRoel P. Dolaypan Jr.No ratings yet

- Proposed Rules and Regulations For The Ammungan Space RentalDocument3 pagesProposed Rules and Regulations For The Ammungan Space RentalRoel P. Dolaypan Jr.No ratings yet

- COMMENTS On Topic No. 1Document4 pagesCOMMENTS On Topic No. 1Roel P. Dolaypan Jr.No ratings yet

- Module 2Document19 pagesModule 2Roel P. Dolaypan Jr.No ratings yet

- Xxxsyllabus - Pricingstrat 22 23 3Document2 pagesXxxsyllabus - Pricingstrat 22 23 3Roel P. Dolaypan Jr.No ratings yet

- Conceptual Framework 1.1Document1 pageConceptual Framework 1.1Roel P. Dolaypan Jr.No ratings yet

- History of The CooperativeDocument28 pagesHistory of The CooperativeRoel P. Dolaypan Jr.No ratings yet

- Problem TreeDocument1 pageProblem TreeRoel P. Dolaypan Jr.No ratings yet

- Financial AnalysisDocument4 pagesFinancial AnalysisRoel P. Dolaypan Jr.No ratings yet

- Module 1Document11 pagesModule 1Roel P. Dolaypan Jr.No ratings yet

- Municipal Sustainability PlanDocument3 pagesMunicipal Sustainability PlanJoem'z Burlasa-Amoto Esler-DionaldoNo ratings yet

- Economic Environment (1) PPTDocument40 pagesEconomic Environment (1) PPTHimangi GuptaNo ratings yet

- Top Down and Bottoms Up Approach in BudgetingDocument7 pagesTop Down and Bottoms Up Approach in BudgetingChetan SaxenaNo ratings yet

- Guidelines On The Appropriation, Release, PlanningDocument20 pagesGuidelines On The Appropriation, Release, PlanningCamila Anne GambanNo ratings yet

- The Muddling Nineties: Benazir Bhutto and Nawaz Sharif (1993-1999)Document15 pagesThe Muddling Nineties: Benazir Bhutto and Nawaz Sharif (1993-1999)Shameel IrshadNo ratings yet

- Integrating Tax Expenditures Into The Budget Process, by Len BurmanDocument23 pagesIntegrating Tax Expenditures Into The Budget Process, by Len BurmanKaitlin LeeNo ratings yet

- 16th Mindanao Invitation PB CDODocument1 page16th Mindanao Invitation PB CDOChristine BernalNo ratings yet

- Enrile Welcomes Probe of Port IreneDocument9 pagesEnrile Welcomes Probe of Port IreneJPA-BJMPIX ZCZSICNo ratings yet

- Project Management - AssignmentDocument7 pagesProject Management - AssignmentAkshatNo ratings yet

- Letter of Undertaking To PS WorksDocument2 pagesLetter of Undertaking To PS Worksmac timothyNo ratings yet

- CoB 100th RS June 24 2024 2.30PMDocument4 pagesCoB 100th RS June 24 2024 2.30PMDiane Amielle Armamento - VillamielNo ratings yet

- The Code of Putinism Brian D Taylor Full ChapterDocument67 pagesThe Code of Putinism Brian D Taylor Full Chapterrobert.beam905100% (5)

- IMF Reformation of BangladeshDocument125 pagesIMF Reformation of BangladeshSajjad HossainNo ratings yet

- House Bill 2883Document3 pagesHouse Bill 2883Kristofer PlonaNo ratings yet

- Public FinanceDocument2 pagesPublic FinanceNandhuNo ratings yet

- Government Accounting: Accounting For Non-Profit OrganizationsDocument88 pagesGovernment Accounting: Accounting For Non-Profit OrganizationsDe GuzmanNo ratings yet

- Karnataka Budget AnalysisDocument4 pagesKarnataka Budget AnalysisV GowdaNo ratings yet

- India Socio Politics & Economic System Current Affairs212 - Xid-3384634 - 1Document4 pagesIndia Socio Politics & Economic System Current Affairs212 - Xid-3384634 - 1Shubham ChitkaraNo ratings yet

- How To Write Project Proposal Form and StyleDocument22 pagesHow To Write Project Proposal Form and StyleMeynard MagsinoNo ratings yet

- TSA Loose Change Report 2019Document11 pagesTSA Loose Change Report 2019Adam ForgieNo ratings yet

- Reddy Sir Basics About Fiscal PolicyDocument8 pagesReddy Sir Basics About Fiscal PolicyD PNo ratings yet

- SK Appropriation Ordinance 2023Document3 pagesSK Appropriation Ordinance 2023Cazy Mel EugenioNo ratings yet

- App-Sbfp New NormalDocument1 pageApp-Sbfp New NormalGine FrencilloNo ratings yet

- Farmers Market Funding LetterDocument1 pageFarmers Market Funding LetterRose WhiteNo ratings yet

- Purpose: ObjectiveDocument5 pagesPurpose: Objectiveteck yuNo ratings yet

- Don't Come Home America: The Case Against RetrenchmentDocument45 pagesDon't Come Home America: The Case Against RetrenchmentChucky TNo ratings yet

- Reso 002-2023Document3 pagesReso 002-2023Andy CadanganNo ratings yet

- Assignment 3 Financial Analysis Graphs Excel TemplateDocument3 pagesAssignment 3 Financial Analysis Graphs Excel TemplateDylan VanslochterenNo ratings yet

- Checklist of Requirements: Shoreland Development ClearanceDocument1 pageChecklist of Requirements: Shoreland Development ClearanceEmitz HernandezNo ratings yet

- Jurnal Ilmiah Administrasi Publik (JIAP) : Foreign Aid and Economic Development in IndonesiaDocument5 pagesJurnal Ilmiah Administrasi Publik (JIAP) : Foreign Aid and Economic Development in IndonesiaMechanical Div. EPC-HKNo ratings yet