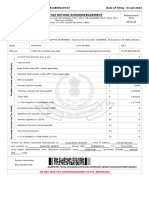

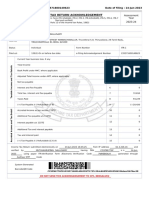

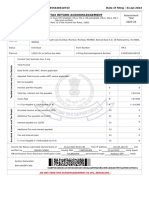

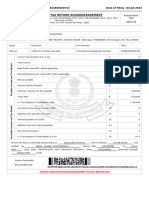

Shree Suleshvari Enterprise

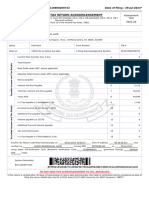

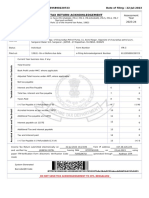

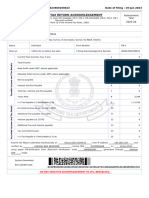

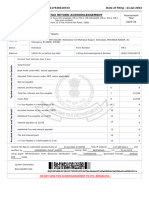

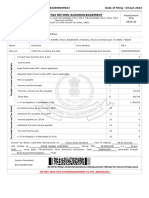

Shree Suleshvari Enterprise

You might also like

- Ward 20 2 2019-20 07EPCPS5037C1ZZ 0 20240510 031521 820Document11 pagesWard 20 2 2019-20 07EPCPS5037C1ZZ 0 20240510 031521 820Vishal DwivediNo ratings yet

- Maa Laxmi Hardware 2019-20Document4 pagesMaa Laxmi Hardware 2019-20surendrasharmaofficeNo ratings yet

- Patanjali Arogya Kendra 2018-19Document5 pagesPatanjali Arogya Kendra 2018-19tuensangnagaland2018No ratings yet

- PDF 115914800310723Document1 pagePDF 115914800310723jayanto chowdhuryNo ratings yet

- Itr 2020-21Document1 pageItr 2020-21saif.siddiqui.ablNo ratings yet

- Ramanjeet Itr 22-23Document1 pageRamanjeet Itr 22-23MK ASSOCIATESNo ratings yet

- Adobe Scan 15 Dec 2023Document1 pageAdobe Scan 15 Dec 2023gandhipl74No ratings yet

- PDF 438429930210822Document1 pagePDF 438429930210822peetamber agarwalNo ratings yet

- Ack Abxpb2604f 2022-23 857058350180722 PDFDocument1 pageAck Abxpb2604f 2022-23 857058350180722 PDFVineet KhuranaNo ratings yet

- 22-23 All PagesDocument5 pages22-23 All PagesBulbuli DasNo ratings yet

- $RX7B05VDocument1 page$RX7B05Vakxerox47No ratings yet

- Itr 2021-22Document1 pageItr 2021-22saif.siddiqui.ablNo ratings yet

- Ack Ahipk1805e 2022-23 449243480260822Document1 pageAck Ahipk1805e 2022-23 449243480260822b.ramanareddy7226No ratings yet

- Ack Ahipk1805e 2022-23 449243480260822Document1 pageAck Ahipk1805e 2022-23 449243480260822b.ramanareddy7226No ratings yet

- 231124013-1-1Document1 page231124013-1-1grudhaya16No ratings yet

- ProjectDocument1 pageProjectgaganohri0044No ratings yet

- ACK918293970310723Document1 pageACK918293970310723vikash865138No ratings yet

- Ack Aadhn6348f 2022-23 220799250290722Document1 pageAck Aadhn6348f 2022-23 220799250290722Akansha JainNo ratings yet

- Ack CKLPR7420J 2022-23 366437070310722Document1 pageAck CKLPR7420J 2022-23 366437070310722manishranjan82710No ratings yet

- Ack Cdhpa3843f 2022-23 220950670290722Document1 pageAck Cdhpa3843f 2022-23 220950670290722rtaxhelp helpNo ratings yet

- Indian Income Tax Return Acknowledgement: Acknowledgement Number: Date of FilingDocument1 pageIndian Income Tax Return Acknowledgement: Acknowledgement Number: Date of FilingchanderjagdishNo ratings yet

- PDF 235571600140623Document1 pagePDF 235571600140623Hema TNo ratings yet

- Parmjit Singh Itrv Ay 202324Document1 pageParmjit Singh Itrv Ay 202324SANJEEV KUMARNo ratings yet

- Ack 759254770280723Document1 pageAck 759254770280723Gunograhi Gouranga DasNo ratings yet

- PDF 169223670270722Document1 pagePDF 169223670270722adhya100% (1)

- Indian Income Tax Return Acknowledgement: Acknowledgement Number:611395890220723 Date of Filing: 22-Jul-2023Document1 pageIndian Income Tax Return Acknowledgement: Acknowledgement Number:611395890220723 Date of Filing: 22-Jul-2023Respect InfinityNo ratings yet

- Ack Aaecr3779g 2022-23 617424661051022Document1 pageAck Aaecr3779g 2022-23 617424661051022Sankarasubramanian KrishnanNo ratings yet

- PDF 133355440310723Document1 pagePDF 133355440310723cacarod2008No ratings yet

- PDF 923744260220722Document1 pagePDF 923744260220722Ashish SinghNo ratings yet

- TaxesDocument2 pagesTaxesRameshNadarNo ratings yet

- Atul Saini 22Document1 pageAtul Saini 22Fascino WhiteNo ratings yet

- Itr Ravi - 23Document1 pageItr Ravi - 23prahlad55437No ratings yet

- ITRVDocument1 pageITRVdeepakgaur3139No ratings yet

- GST RFD-01 - 37AABCJ1299A1ZS - EXPWOP - 201904 - FormDocument3 pagesGST RFD-01 - 37AABCJ1299A1ZS - EXPWOP - 201904 - FormkotisanampudiNo ratings yet

- Digitally Proceedings of P Hanumantharao & Sons 2018-19 S-73Document31 pagesDigitally Proceedings of P Hanumantharao & Sons 2018-19 S-73CTOAUDIT1 BLYNo ratings yet

- Itr VDocument1 pageItr VohhNo ratings yet

- PDF 161925521310324Document1 pagePDF 161925521310324db3506107No ratings yet

- PDF - 235623290290722 - ITR 22-23Document1 pagePDF - 235623290290722 - ITR 22-23ruchirmathurNo ratings yet

- Ack Cespc6304p 2022-23 811632260201122Document1 pageAck Cespc6304p 2022-23 811632260201122knowthebest787No ratings yet

- PDF 260623500190623Document1 pagePDF 260623500190623Harsha R BNo ratings yet

- GST LatestAmendments Issues 01072023Document85 pagesGST LatestAmendments Issues 01072023Selvakumar MuthurajNo ratings yet

- Ack Aaxpn5187e 2022-23 958380190240722Document1 pageAck Aaxpn5187e 2022-23 958380190240722jrgbcsputtasaraNo ratings yet

- Ack 638167400230723Document1 pageAck 638167400230723gamers SatisfactionNo ratings yet

- Ack Acmpn8839q 2022-23 777571430100722Document1 pageAck Acmpn8839q 2022-23 777571430100722salveakshay1000No ratings yet

- VineetDocument1 pageVineetRiaZ MoHamMaDNo ratings yet

- Biswajit Man. ItrDocument2 pagesBiswajit Man. Itralisahamat022No ratings yet

- Audit RajshreeDocument28 pagesAudit Rajshreeahmad.hspcoNo ratings yet

- Itr 23Document1 pageItr 23vikash pandeyNo ratings yet

- AcknowledgementDocument1 pageAcknowledgementaditya_kavangalNo ratings yet

- Ack 343831860020723Document1 pageAck 343831860020723nikhilNo ratings yet

- JOSEPDocument1 pageJOSEPtdsbolluNo ratings yet

- ACK195642050030623Document1 pageACK195642050030623Nihar RanjanNo ratings yet

- Ack 935358350080224Document1 pageAck 935358350080224jdas7061No ratings yet

- Beant Singh ITRDocument7 pagesBeant Singh ITRakhtarnadeem5636No ratings yet

- Information Risk ManagementDocument1 pageInformation Risk Managementgaganohri0044No ratings yet

- ACK821411880290723Document1 pageACK821411880290723Atharv RanaNo ratings yet

- ITRVDocument1 pageITRVyashbaislaa1234No ratings yet

- Indian Income Tax Return Acknowledgement 2022-23: Assessment YearDocument1 pageIndian Income Tax Return Acknowledgement 2022-23: Assessment Yearehsan ahmed0% (1)

- Indian Income Tax Return Acknowledgement: Acknowledgement Number: Date of FilingDocument1 pageIndian Income Tax Return Acknowledgement: Acknowledgement Number: Date of Filingpiyushgawariya143No ratings yet

- Bacullo - THC 109Document1 pageBacullo - THC 109Ranze Angelique Concepcion BaculloNo ratings yet

- Misrepresentation PQ SolvingDocument9 pagesMisrepresentation PQ SolvingMahdi Bin MamunNo ratings yet

- Rural Litigation and Ent. Vs UPDocument8 pagesRural Litigation and Ent. Vs UPPulkitAgrawalNo ratings yet

- DHBVNDocument4 pagesDHBVNAshok SharmaNo ratings yet

- 2015 Municipal Election Bucks County League of Women Voters of Bucks CountyDocument108 pages2015 Municipal Election Bucks County League of Women Voters of Bucks CountyBucksLocalNews.comNo ratings yet

- Cheries Business PlanDocument5 pagesCheries Business PlanCheries Jane MoringNo ratings yet

- DEFENSE STRATEGIES OF A MARKET LEADER-Article ExcerptsDocument3 pagesDEFENSE STRATEGIES OF A MARKET LEADER-Article ExcerptsSweety DurejaNo ratings yet

- Annual Report 2022Document15 pagesAnnual Report 2022AARAB MaryemNo ratings yet

- Qubole Open Data Lake Platform Aws Ra PDFDocument1 pageQubole Open Data Lake Platform Aws Ra PDFwiredfrombackNo ratings yet

- Options, Futures, and Other Derivatives, 8th Edition, 1Document65 pagesOptions, Futures, and Other Derivatives, 8th Edition, 1Mohammed NajihNo ratings yet

- Meiji Era Economic Copy 2Document1 pageMeiji Era Economic Copy 2api-298392554No ratings yet

- B10 - MMT - Five GuysDocument2 pagesB10 - MMT - Five GuysNitishKhadeNo ratings yet

- SBM Dimension1 LeadershipDocument74 pagesSBM Dimension1 LeadershipCynthia LuayNo ratings yet

- Value CreationDocument15 pagesValue CreationCharis OneyemiNo ratings yet

- Assignment Getha Chandran PDFDocument24 pagesAssignment Getha Chandran PDFSamuel Lau 刘恩得No ratings yet

- Advanced Certification in Inspection EngineeringDocument14 pagesAdvanced Certification in Inspection Engineeringdanish.khan80206040No ratings yet

- Brand Analysis of HaldiramDocument21 pagesBrand Analysis of HaldiramGunjan AhujaNo ratings yet

- Einhorn Letter Q1 2021Document7 pagesEinhorn Letter Q1 2021Zerohedge100% (4)

- Service Design Itil v3Document1 pageService Design Itil v3Afif Kamal FiskaNo ratings yet

- Hempaline External FlyerDocument2 pagesHempaline External FlyerMohamed NouzerNo ratings yet

- HDG Datasheet 13 - Renovation of Hot Dip Galvanized SteelDocument1 pageHDG Datasheet 13 - Renovation of Hot Dip Galvanized SteelSam SamuelsonNo ratings yet

- Journal Paper 2299 Speedmart Case StudyDocument7 pagesJournal Paper 2299 Speedmart Case StudyNoriani ZakariaNo ratings yet

- LBC Courier Terms and ConditionsDocument3 pagesLBC Courier Terms and ConditionsTomas Diane LizardoNo ratings yet

- Shawndelle Chester Resume WBDocument2 pagesShawndelle Chester Resume WBapi-488771354No ratings yet

- Utep Accounts Payable Audit Report PDFDocument11 pagesUtep Accounts Payable Audit Report PDFyididiyayibNo ratings yet

- Sources of Finance: Different Ways A Business Can Obtain MoneyDocument19 pagesSources of Finance: Different Ways A Business Can Obtain MoneyJayaNo ratings yet

- Enderes vs. Lee TSNDocument3 pagesEnderes vs. Lee TSNLowell MadrilenoNo ratings yet

- Essay RecoveryDocument7 pagesEssay RecoveryTanya SinghNo ratings yet

- Estimates OF: State Domestic Product, OdishaDocument28 pagesEstimates OF: State Domestic Product, Odishaphc kallumarriNo ratings yet

- Maj Concslb 043 0Document3 pagesMaj Concslb 043 0Mohammed JassimNo ratings yet

Download as pdf or txt

You might also like

- Ward 20 2 2019-20 07EPCPS5037C1ZZ 0 20240510 031521 820Document11 pagesWard 20 2 2019-20 07EPCPS5037C1ZZ 0 20240510 031521 820Vishal DwivediNo ratings yet

- Maa Laxmi Hardware 2019-20Document4 pagesMaa Laxmi Hardware 2019-20surendrasharmaofficeNo ratings yet

- Patanjali Arogya Kendra 2018-19Document5 pagesPatanjali Arogya Kendra 2018-19tuensangnagaland2018No ratings yet

- PDF 115914800310723Document1 pagePDF 115914800310723jayanto chowdhuryNo ratings yet

- Itr 2020-21Document1 pageItr 2020-21saif.siddiqui.ablNo ratings yet

- Ramanjeet Itr 22-23Document1 pageRamanjeet Itr 22-23MK ASSOCIATESNo ratings yet

- Adobe Scan 15 Dec 2023Document1 pageAdobe Scan 15 Dec 2023gandhipl74No ratings yet

- PDF 438429930210822Document1 pagePDF 438429930210822peetamber agarwalNo ratings yet

- Ack Abxpb2604f 2022-23 857058350180722 PDFDocument1 pageAck Abxpb2604f 2022-23 857058350180722 PDFVineet KhuranaNo ratings yet

- 22-23 All PagesDocument5 pages22-23 All PagesBulbuli DasNo ratings yet

- $RX7B05VDocument1 page$RX7B05Vakxerox47No ratings yet

- Itr 2021-22Document1 pageItr 2021-22saif.siddiqui.ablNo ratings yet

- Ack Ahipk1805e 2022-23 449243480260822Document1 pageAck Ahipk1805e 2022-23 449243480260822b.ramanareddy7226No ratings yet

- Ack Ahipk1805e 2022-23 449243480260822Document1 pageAck Ahipk1805e 2022-23 449243480260822b.ramanareddy7226No ratings yet

- 231124013-1-1Document1 page231124013-1-1grudhaya16No ratings yet

- ProjectDocument1 pageProjectgaganohri0044No ratings yet

- ACK918293970310723Document1 pageACK918293970310723vikash865138No ratings yet

- Ack Aadhn6348f 2022-23 220799250290722Document1 pageAck Aadhn6348f 2022-23 220799250290722Akansha JainNo ratings yet

- Ack CKLPR7420J 2022-23 366437070310722Document1 pageAck CKLPR7420J 2022-23 366437070310722manishranjan82710No ratings yet

- Ack Cdhpa3843f 2022-23 220950670290722Document1 pageAck Cdhpa3843f 2022-23 220950670290722rtaxhelp helpNo ratings yet

- Indian Income Tax Return Acknowledgement: Acknowledgement Number: Date of FilingDocument1 pageIndian Income Tax Return Acknowledgement: Acknowledgement Number: Date of FilingchanderjagdishNo ratings yet

- PDF 235571600140623Document1 pagePDF 235571600140623Hema TNo ratings yet

- Parmjit Singh Itrv Ay 202324Document1 pageParmjit Singh Itrv Ay 202324SANJEEV KUMARNo ratings yet

- Ack 759254770280723Document1 pageAck 759254770280723Gunograhi Gouranga DasNo ratings yet

- PDF 169223670270722Document1 pagePDF 169223670270722adhya100% (1)

- Indian Income Tax Return Acknowledgement: Acknowledgement Number:611395890220723 Date of Filing: 22-Jul-2023Document1 pageIndian Income Tax Return Acknowledgement: Acknowledgement Number:611395890220723 Date of Filing: 22-Jul-2023Respect InfinityNo ratings yet

- Ack Aaecr3779g 2022-23 617424661051022Document1 pageAck Aaecr3779g 2022-23 617424661051022Sankarasubramanian KrishnanNo ratings yet

- PDF 133355440310723Document1 pagePDF 133355440310723cacarod2008No ratings yet

- PDF 923744260220722Document1 pagePDF 923744260220722Ashish SinghNo ratings yet

- TaxesDocument2 pagesTaxesRameshNadarNo ratings yet

- Atul Saini 22Document1 pageAtul Saini 22Fascino WhiteNo ratings yet

- Itr Ravi - 23Document1 pageItr Ravi - 23prahlad55437No ratings yet

- ITRVDocument1 pageITRVdeepakgaur3139No ratings yet

- GST RFD-01 - 37AABCJ1299A1ZS - EXPWOP - 201904 - FormDocument3 pagesGST RFD-01 - 37AABCJ1299A1ZS - EXPWOP - 201904 - FormkotisanampudiNo ratings yet

- Digitally Proceedings of P Hanumantharao & Sons 2018-19 S-73Document31 pagesDigitally Proceedings of P Hanumantharao & Sons 2018-19 S-73CTOAUDIT1 BLYNo ratings yet

- Itr VDocument1 pageItr VohhNo ratings yet

- PDF 161925521310324Document1 pagePDF 161925521310324db3506107No ratings yet

- PDF - 235623290290722 - ITR 22-23Document1 pagePDF - 235623290290722 - ITR 22-23ruchirmathurNo ratings yet

- Ack Cespc6304p 2022-23 811632260201122Document1 pageAck Cespc6304p 2022-23 811632260201122knowthebest787No ratings yet

- PDF 260623500190623Document1 pagePDF 260623500190623Harsha R BNo ratings yet

- GST LatestAmendments Issues 01072023Document85 pagesGST LatestAmendments Issues 01072023Selvakumar MuthurajNo ratings yet

- Ack Aaxpn5187e 2022-23 958380190240722Document1 pageAck Aaxpn5187e 2022-23 958380190240722jrgbcsputtasaraNo ratings yet

- Ack 638167400230723Document1 pageAck 638167400230723gamers SatisfactionNo ratings yet

- Ack Acmpn8839q 2022-23 777571430100722Document1 pageAck Acmpn8839q 2022-23 777571430100722salveakshay1000No ratings yet

- VineetDocument1 pageVineetRiaZ MoHamMaDNo ratings yet

- Biswajit Man. ItrDocument2 pagesBiswajit Man. Itralisahamat022No ratings yet

- Audit RajshreeDocument28 pagesAudit Rajshreeahmad.hspcoNo ratings yet

- Itr 23Document1 pageItr 23vikash pandeyNo ratings yet

- AcknowledgementDocument1 pageAcknowledgementaditya_kavangalNo ratings yet

- Ack 343831860020723Document1 pageAck 343831860020723nikhilNo ratings yet

- JOSEPDocument1 pageJOSEPtdsbolluNo ratings yet

- ACK195642050030623Document1 pageACK195642050030623Nihar RanjanNo ratings yet

- Ack 935358350080224Document1 pageAck 935358350080224jdas7061No ratings yet

- Beant Singh ITRDocument7 pagesBeant Singh ITRakhtarnadeem5636No ratings yet

- Information Risk ManagementDocument1 pageInformation Risk Managementgaganohri0044No ratings yet

- ACK821411880290723Document1 pageACK821411880290723Atharv RanaNo ratings yet

- ITRVDocument1 pageITRVyashbaislaa1234No ratings yet

- Indian Income Tax Return Acknowledgement 2022-23: Assessment YearDocument1 pageIndian Income Tax Return Acknowledgement 2022-23: Assessment Yearehsan ahmed0% (1)

- Indian Income Tax Return Acknowledgement: Acknowledgement Number: Date of FilingDocument1 pageIndian Income Tax Return Acknowledgement: Acknowledgement Number: Date of Filingpiyushgawariya143No ratings yet

- Bacullo - THC 109Document1 pageBacullo - THC 109Ranze Angelique Concepcion BaculloNo ratings yet

- Misrepresentation PQ SolvingDocument9 pagesMisrepresentation PQ SolvingMahdi Bin MamunNo ratings yet

- Rural Litigation and Ent. Vs UPDocument8 pagesRural Litigation and Ent. Vs UPPulkitAgrawalNo ratings yet

- DHBVNDocument4 pagesDHBVNAshok SharmaNo ratings yet

- 2015 Municipal Election Bucks County League of Women Voters of Bucks CountyDocument108 pages2015 Municipal Election Bucks County League of Women Voters of Bucks CountyBucksLocalNews.comNo ratings yet

- Cheries Business PlanDocument5 pagesCheries Business PlanCheries Jane MoringNo ratings yet

- DEFENSE STRATEGIES OF A MARKET LEADER-Article ExcerptsDocument3 pagesDEFENSE STRATEGIES OF A MARKET LEADER-Article ExcerptsSweety DurejaNo ratings yet

- Annual Report 2022Document15 pagesAnnual Report 2022AARAB MaryemNo ratings yet

- Qubole Open Data Lake Platform Aws Ra PDFDocument1 pageQubole Open Data Lake Platform Aws Ra PDFwiredfrombackNo ratings yet

- Options, Futures, and Other Derivatives, 8th Edition, 1Document65 pagesOptions, Futures, and Other Derivatives, 8th Edition, 1Mohammed NajihNo ratings yet

- Meiji Era Economic Copy 2Document1 pageMeiji Era Economic Copy 2api-298392554No ratings yet

- B10 - MMT - Five GuysDocument2 pagesB10 - MMT - Five GuysNitishKhadeNo ratings yet

- SBM Dimension1 LeadershipDocument74 pagesSBM Dimension1 LeadershipCynthia LuayNo ratings yet

- Value CreationDocument15 pagesValue CreationCharis OneyemiNo ratings yet

- Assignment Getha Chandran PDFDocument24 pagesAssignment Getha Chandran PDFSamuel Lau 刘恩得No ratings yet

- Advanced Certification in Inspection EngineeringDocument14 pagesAdvanced Certification in Inspection Engineeringdanish.khan80206040No ratings yet

- Brand Analysis of HaldiramDocument21 pagesBrand Analysis of HaldiramGunjan AhujaNo ratings yet

- Einhorn Letter Q1 2021Document7 pagesEinhorn Letter Q1 2021Zerohedge100% (4)

- Service Design Itil v3Document1 pageService Design Itil v3Afif Kamal FiskaNo ratings yet

- Hempaline External FlyerDocument2 pagesHempaline External FlyerMohamed NouzerNo ratings yet

- HDG Datasheet 13 - Renovation of Hot Dip Galvanized SteelDocument1 pageHDG Datasheet 13 - Renovation of Hot Dip Galvanized SteelSam SamuelsonNo ratings yet

- Journal Paper 2299 Speedmart Case StudyDocument7 pagesJournal Paper 2299 Speedmart Case StudyNoriani ZakariaNo ratings yet

- LBC Courier Terms and ConditionsDocument3 pagesLBC Courier Terms and ConditionsTomas Diane LizardoNo ratings yet

- Shawndelle Chester Resume WBDocument2 pagesShawndelle Chester Resume WBapi-488771354No ratings yet

- Utep Accounts Payable Audit Report PDFDocument11 pagesUtep Accounts Payable Audit Report PDFyididiyayibNo ratings yet

- Sources of Finance: Different Ways A Business Can Obtain MoneyDocument19 pagesSources of Finance: Different Ways A Business Can Obtain MoneyJayaNo ratings yet

- Enderes vs. Lee TSNDocument3 pagesEnderes vs. Lee TSNLowell MadrilenoNo ratings yet

- Essay RecoveryDocument7 pagesEssay RecoveryTanya SinghNo ratings yet

- Estimates OF: State Domestic Product, OdishaDocument28 pagesEstimates OF: State Domestic Product, Odishaphc kallumarriNo ratings yet

- Maj Concslb 043 0Document3 pagesMaj Concslb 043 0Mohammed JassimNo ratings yet