Unit 1 - Summary

Unit 1 - Summary

You might also like

- Learning Chess Workbook Step 5 PDFDocument60 pagesLearning Chess Workbook Step 5 PDFviraaj100% (24)

- Accounting Standards and Financial Reporting Requirements SaudiDocument5 pagesAccounting Standards and Financial Reporting Requirements Saudi123tottiNo ratings yet

- Accounting Standards ProjectDocument6 pagesAccounting Standards ProjectPuneet ChawlaNo ratings yet

- IFRSs For SMEs in The Kenyan ContextDocument6 pagesIFRSs For SMEs in The Kenyan ContextTerrence100% (1)

- Part D-20-SMEsDocument40 pagesPart D-20-SMEsnfakhar2808No ratings yet

- IFRS BhamineeDocument4 pagesIFRS BhamineeBhaminee patelNo ratings yet

- Study Guide Unit 1 - South African Reporting RequirementsDocument7 pagesStudy Guide Unit 1 - South African Reporting RequirementshavengroupnaNo ratings yet

- Financial Reporting For SMEsDocument3 pagesFinancial Reporting For SMEsMichele A. NacaytunaNo ratings yet

- Concepts and Pervasive PrinciplesDocument47 pagesConcepts and Pervasive PrinciplesBongani MoyoNo ratings yet

- Chapter 6 Time Period Assumption, GAAP, IFRS, and PFRSDocument19 pagesChapter 6 Time Period Assumption, GAAP, IFRS, and PFRSRafael Ganzon RiveraNo ratings yet

- Regulatory Framework.Document25 pagesRegulatory Framework.saidkhatib368No ratings yet

- Faqs - Ifrs SmesDocument5 pagesFaqs - Ifrs SmesMelicent FaithNo ratings yet

- Module 4 - FRADocument29 pagesModule 4 - FRAsrish.srccNo ratings yet

- Adv. Accountancy Paper-1Document5 pagesAdv. Accountancy Paper-1Avadhut PaymalleNo ratings yet

- Insights Into IFRS Overview 2014 15Document101 pagesInsights Into IFRS Overview 2014 15Florensia Restian100% (2)

- IFRS For Small and Medium-Sized Entities: Pocket Guide 2009Document10 pagesIFRS For Small and Medium-Sized Entities: Pocket Guide 2009Robin SicatNo ratings yet

- Background of IfrsDocument2 pagesBackground of IfrsShelze Consulting100% (1)

- IFRS For SME'sDocument26 pagesIFRS For SME'sJennybabe PetaNo ratings yet

- Thesis On Ifrs For SmesDocument7 pagesThesis On Ifrs For Smesjennyalexanderboston100% (2)

- AP 06 - PFRS For Small EntitiesDocument8 pagesAP 06 - PFRS For Small EntitiesJhona Mae Dela CruzNo ratings yet

- IFRSDocument14 pagesIFRSNishchay Dhingra100% (1)

- WRK IFRS SMEsDocument109 pagesWRK IFRS SMEsMazhar Ali JoyoNo ratings yet

- Comparative Analysis of Reporting Practices of Islamic FinancialDocument16 pagesComparative Analysis of Reporting Practices of Islamic FinancialAbdul MaroofNo ratings yet

- Ifrs As A Tool For Cross Border Reporting ImzakariDocument27 pagesIfrs As A Tool For Cross Border Reporting ImzakariBayodele7No ratings yet

- AAOIFI Vs IFRS: Accounting For Islamic FinanceDocument11 pagesAAOIFI Vs IFRS: Accounting For Islamic FinanceMuhammad Faisal Kamarul ZamanNo ratings yet

- IFRS For Small and Medium-Sized Entities: Pocket Guide 2009Document11 pagesIFRS For Small and Medium-Sized Entities: Pocket Guide 2009Robin SicatNo ratings yet

- IFRS For Small and Medium-Sized Entities: Pocket Guide 2009Document14 pagesIFRS For Small and Medium-Sized Entities: Pocket Guide 2009Robin SicatNo ratings yet

- Notes 1Document6 pagesNotes 1sjayceelynNo ratings yet

- International Financial Reporting Standards (IFRS) : Compiled By: Yogesh Bhanushali Internal Guidance: Dr. Shama ShahDocument22 pagesInternational Financial Reporting Standards (IFRS) : Compiled By: Yogesh Bhanushali Internal Guidance: Dr. Shama ShahYogesh BhanushaliNo ratings yet

- 12 Overview of IFRS For SMEs Version2011 01Document73 pages12 Overview of IFRS For SMEs Version2011 01tdomazetNo ratings yet

- ch6 IFRSDocument56 pagesch6 IFRSAnonymous 6aW7sZWdIL100% (1)

- Adoption of IFRSDocument13 pagesAdoption of IFRSsuryamlacwNo ratings yet

- IFRS Road AheadDocument6 pagesIFRS Road AheadjantonycaNo ratings yet

- IFRS SMEsDocument3 pagesIFRS SMEsPahladsinghNo ratings yet

- Hong Kong Company Reporting Exemption Guideline NoteDocument5 pagesHong Kong Company Reporting Exemption Guideline Notea9282518No ratings yet

- Advanced Accounting AssignmentDocument5 pagesAdvanced Accounting Assignmentmtj5yqt8y6No ratings yet

- Small and Medium-Sized EntitiesDocument36 pagesSmall and Medium-Sized EntitiesDonna DelgadoNo ratings yet

- Business FinanceDocument13 pagesBusiness FinanceMichael MendozaNo ratings yet

- Ifrs Indian ContextDocument7 pagesIfrs Indian ContextKumar Sachin DeoNo ratings yet

- Sandy Gill ProjectDocument67 pagesSandy Gill ProjectSandy Gill GillNo ratings yet

- IFRS SummaryDocument6 pagesIFRS SummaryLimenihNo ratings yet

- Assignment For Corporate Financial AccountingDocument6 pagesAssignment For Corporate Financial AccountingFlemin GeorgeNo ratings yet

- Overview of IPSAS StandardsDocument28 pagesOverview of IPSAS StandardsAkinmulewo Ayodele100% (3)

- Accounting Regulation in PakistanDocument4 pagesAccounting Regulation in Pakistanralph ravasNo ratings yet

- Convergence With IFRS in IndiaDocument32 pagesConvergence With IFRS in IndiaVimal GogriNo ratings yet

- IFRS For Small and Medium-Sized Entities: Pocket Guide 2009Document10 pagesIFRS For Small and Medium-Sized Entities: Pocket Guide 2009Robin SicatNo ratings yet

- Module - IVDocument73 pagesModule - IVRahul Singh100% (1)

- SBRIFRSForSMEs TutorSlidesDocument29 pagesSBRIFRSForSMEs TutorSlidesDipesh MagratiNo ratings yet

- Pcps FRF Sme Staff TrainingDocument44 pagesPcps FRF Sme Staff TrainingGreg MarsoNo ratings yet

- Comparison of Ind As and IFRSDocument10 pagesComparison of Ind As and IFRSAman SinghNo ratings yet

- CH 4 Financial Reposting QuestionsDocument4 pagesCH 4 Financial Reposting QuestionsAnthonny EmernegidoNo ratings yet

- IFRS1Document33 pagesIFRS1Ejiemen OkunegaNo ratings yet

- Unit 2 - GAAP and IFRSDocument15 pagesUnit 2 - GAAP and IFRSKanak RathoreNo ratings yet

- Theory QuestionsDocument6 pagesTheory Questionsanky1555No ratings yet

- Philippines IFRS ProfileDocument6 pagesPhilippines IFRS Profileaddicted17No ratings yet

- Spotting The Differences Between IFRS For SMEs and Full IFRSDocument5 pagesSpotting The Differences Between IFRS For SMEs and Full IFRSTannaoNo ratings yet

- Presentation01 (2) - 1Document21 pagesPresentation01 (2) - 1v7891283965No ratings yet

- Operating a Business and Employment in the United Kingdom: Part Three of The Investors' Guide to the United Kingdom 2015/16From EverandOperating a Business and Employment in the United Kingdom: Part Three of The Investors' Guide to the United Kingdom 2015/16No ratings yet

- Taxation Unit 7 - Concept Questions 2023Document6 pagesTaxation Unit 7 - Concept Questions 2023havengroupnaNo ratings yet

- Unit 3 Slides - VO Part 2 of 2Document10 pagesUnit 3 Slides - VO Part 2 of 2havengroupnaNo ratings yet

- Taxation Unit 3 - Tutorial QuestionDocument8 pagesTaxation Unit 3 - Tutorial QuestionhavengroupnaNo ratings yet

- Unit 3 - Lecture Slides FINALDocument30 pagesUnit 3 - Lecture Slides FINALhavengroupnaNo ratings yet

- Taxation Unit 3 - Concept Questions 2023Document6 pagesTaxation Unit 3 - Concept Questions 2023havengroupnaNo ratings yet

- Unit 3 - Cost AssignmentDocument17 pagesUnit 3 - Cost AssignmenthavengroupnaNo ratings yet

- Unit 3 - Tut QuestionDocument1 pageUnit 3 - Tut QuestionhavengroupnaNo ratings yet

- G.R. No. 194001Document11 pagesG.R. No. 194001dlyyapNo ratings yet

- Starconnect Retail Transaction Request FormDocument1 pageStarconnect Retail Transaction Request Formatanudas001No ratings yet

- Special Leave Petition Format For SC of IndiaDocument8 pagesSpecial Leave Petition Format For SC of IndiaRahul SharmaNo ratings yet

- 07 - Chapter 1Document51 pages07 - Chapter 1Yash JaiswalNo ratings yet

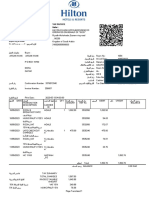

- ReceiptDocument3 pagesReceiptAhsan KhanNo ratings yet

- Zombie Gospel TractDocument8 pagesZombie Gospel TractSimplyBeliefNo ratings yet

- Legal Basis of MapehDocument34 pagesLegal Basis of MapehMaeNo ratings yet

- 4 Lives, New IntroductionDocument10 pages4 Lives, New IntroductionSaraNo ratings yet

- GR No. 92191-92 - Co - Balanquit V HRETDocument23 pagesGR No. 92191-92 - Co - Balanquit V HRETEmman FernandezNo ratings yet

- An Analysis Model of Industrial International CompetitivenessDocument4 pagesAn Analysis Model of Industrial International CompetitivenessYasir AltafNo ratings yet

- WW-II MoviesDocument68 pagesWW-II Moviesajitmondal_HUBNo ratings yet

- Japanese HamletDocument2 pagesJapanese HamlethannahNo ratings yet

- Mas Numerate ResultDocument147 pagesMas Numerate ResultNodelyn ReyesNo ratings yet

- Harper College Phlebotomy Student Handbook 2021-2022Document39 pagesHarper College Phlebotomy Student Handbook 2021-2022Ana mariaNo ratings yet

- Aadhaar CardDocument1 pageAadhaar CardkailashhapaserNo ratings yet

- Unit 10 - Market Leader AdvancedDocument4 pagesUnit 10 - Market Leader AdvancedIa GioshviliNo ratings yet

- Delhivery: COD: Check The Payable Amount On The AppDocument1 pageDelhivery: COD: Check The Payable Amount On The Appnaghmafirdous8697438306No ratings yet

- Homeopathic Materia Medica Vol 1Document259 pagesHomeopathic Materia Medica Vol 1LotusGuy Hans100% (3)

- Rajkot N-Equity QuotationDocument3 pagesRajkot N-Equity QuotationanilravraniNo ratings yet

- Hey Can I Try ThatDocument20 pagesHey Can I Try Thatapi-273078602No ratings yet

- Fil-Estate Properties Vs Spouses Go (GR No 185798, 13 Jan 2014)Document3 pagesFil-Estate Properties Vs Spouses Go (GR No 185798, 13 Jan 2014)Wilfred MartinezNo ratings yet

- YOKDIL Ingilizce SosyalbilimDocument26 pagesYOKDIL Ingilizce SosyalbilimSüleyman UlukuşNo ratings yet

- Anticipation Guide-The OutsidersDocument2 pagesAnticipation Guide-The OutsidersAnthony FabianNo ratings yet

- Halfling Rogue BackstoryDocument2 pagesHalfling Rogue BackstoryalexNo ratings yet

- COPPERMASK - FAQsDocument28 pagesCOPPERMASK - FAQsvernalbelasonNo ratings yet

- Democracy in Pakistan Hopes and Hurdles PDFDocument3 pagesDemocracy in Pakistan Hopes and Hurdles PDFGul RaazNo ratings yet

- Chapter5 PDFDocument50 pagesChapter5 PDFtowiwaNo ratings yet

- Drug Abuse ViewpointsDocument174 pagesDrug Abuse ViewpointsMhel DemabogteNo ratings yet

- Ticket InspectorDocument3 pagesTicket Inspectorsowhalima224No ratings yet

Download as pdf or txt

You might also like

- Learning Chess Workbook Step 5 PDFDocument60 pagesLearning Chess Workbook Step 5 PDFviraaj100% (24)

- Accounting Standards and Financial Reporting Requirements SaudiDocument5 pagesAccounting Standards and Financial Reporting Requirements Saudi123tottiNo ratings yet

- Accounting Standards ProjectDocument6 pagesAccounting Standards ProjectPuneet ChawlaNo ratings yet

- IFRSs For SMEs in The Kenyan ContextDocument6 pagesIFRSs For SMEs in The Kenyan ContextTerrence100% (1)

- Part D-20-SMEsDocument40 pagesPart D-20-SMEsnfakhar2808No ratings yet

- IFRS BhamineeDocument4 pagesIFRS BhamineeBhaminee patelNo ratings yet

- Study Guide Unit 1 - South African Reporting RequirementsDocument7 pagesStudy Guide Unit 1 - South African Reporting RequirementshavengroupnaNo ratings yet

- Financial Reporting For SMEsDocument3 pagesFinancial Reporting For SMEsMichele A. NacaytunaNo ratings yet

- Concepts and Pervasive PrinciplesDocument47 pagesConcepts and Pervasive PrinciplesBongani MoyoNo ratings yet

- Chapter 6 Time Period Assumption, GAAP, IFRS, and PFRSDocument19 pagesChapter 6 Time Period Assumption, GAAP, IFRS, and PFRSRafael Ganzon RiveraNo ratings yet

- Regulatory Framework.Document25 pagesRegulatory Framework.saidkhatib368No ratings yet

- Faqs - Ifrs SmesDocument5 pagesFaqs - Ifrs SmesMelicent FaithNo ratings yet

- Module 4 - FRADocument29 pagesModule 4 - FRAsrish.srccNo ratings yet

- Adv. Accountancy Paper-1Document5 pagesAdv. Accountancy Paper-1Avadhut PaymalleNo ratings yet

- Insights Into IFRS Overview 2014 15Document101 pagesInsights Into IFRS Overview 2014 15Florensia Restian100% (2)

- IFRS For Small and Medium-Sized Entities: Pocket Guide 2009Document10 pagesIFRS For Small and Medium-Sized Entities: Pocket Guide 2009Robin SicatNo ratings yet

- Background of IfrsDocument2 pagesBackground of IfrsShelze Consulting100% (1)

- IFRS For SME'sDocument26 pagesIFRS For SME'sJennybabe PetaNo ratings yet

- Thesis On Ifrs For SmesDocument7 pagesThesis On Ifrs For Smesjennyalexanderboston100% (2)

- AP 06 - PFRS For Small EntitiesDocument8 pagesAP 06 - PFRS For Small EntitiesJhona Mae Dela CruzNo ratings yet

- IFRSDocument14 pagesIFRSNishchay Dhingra100% (1)

- WRK IFRS SMEsDocument109 pagesWRK IFRS SMEsMazhar Ali JoyoNo ratings yet

- Comparative Analysis of Reporting Practices of Islamic FinancialDocument16 pagesComparative Analysis of Reporting Practices of Islamic FinancialAbdul MaroofNo ratings yet

- Ifrs As A Tool For Cross Border Reporting ImzakariDocument27 pagesIfrs As A Tool For Cross Border Reporting ImzakariBayodele7No ratings yet

- AAOIFI Vs IFRS: Accounting For Islamic FinanceDocument11 pagesAAOIFI Vs IFRS: Accounting For Islamic FinanceMuhammad Faisal Kamarul ZamanNo ratings yet

- IFRS For Small and Medium-Sized Entities: Pocket Guide 2009Document11 pagesIFRS For Small and Medium-Sized Entities: Pocket Guide 2009Robin SicatNo ratings yet

- IFRS For Small and Medium-Sized Entities: Pocket Guide 2009Document14 pagesIFRS For Small and Medium-Sized Entities: Pocket Guide 2009Robin SicatNo ratings yet

- Notes 1Document6 pagesNotes 1sjayceelynNo ratings yet

- International Financial Reporting Standards (IFRS) : Compiled By: Yogesh Bhanushali Internal Guidance: Dr. Shama ShahDocument22 pagesInternational Financial Reporting Standards (IFRS) : Compiled By: Yogesh Bhanushali Internal Guidance: Dr. Shama ShahYogesh BhanushaliNo ratings yet

- 12 Overview of IFRS For SMEs Version2011 01Document73 pages12 Overview of IFRS For SMEs Version2011 01tdomazetNo ratings yet

- ch6 IFRSDocument56 pagesch6 IFRSAnonymous 6aW7sZWdIL100% (1)

- Adoption of IFRSDocument13 pagesAdoption of IFRSsuryamlacwNo ratings yet

- IFRS Road AheadDocument6 pagesIFRS Road AheadjantonycaNo ratings yet

- IFRS SMEsDocument3 pagesIFRS SMEsPahladsinghNo ratings yet

- Hong Kong Company Reporting Exemption Guideline NoteDocument5 pagesHong Kong Company Reporting Exemption Guideline Notea9282518No ratings yet

- Advanced Accounting AssignmentDocument5 pagesAdvanced Accounting Assignmentmtj5yqt8y6No ratings yet

- Small and Medium-Sized EntitiesDocument36 pagesSmall and Medium-Sized EntitiesDonna DelgadoNo ratings yet

- Business FinanceDocument13 pagesBusiness FinanceMichael MendozaNo ratings yet

- Ifrs Indian ContextDocument7 pagesIfrs Indian ContextKumar Sachin DeoNo ratings yet

- Sandy Gill ProjectDocument67 pagesSandy Gill ProjectSandy Gill GillNo ratings yet

- IFRS SummaryDocument6 pagesIFRS SummaryLimenihNo ratings yet

- Assignment For Corporate Financial AccountingDocument6 pagesAssignment For Corporate Financial AccountingFlemin GeorgeNo ratings yet

- Overview of IPSAS StandardsDocument28 pagesOverview of IPSAS StandardsAkinmulewo Ayodele100% (3)

- Accounting Regulation in PakistanDocument4 pagesAccounting Regulation in Pakistanralph ravasNo ratings yet

- Convergence With IFRS in IndiaDocument32 pagesConvergence With IFRS in IndiaVimal GogriNo ratings yet

- IFRS For Small and Medium-Sized Entities: Pocket Guide 2009Document10 pagesIFRS For Small and Medium-Sized Entities: Pocket Guide 2009Robin SicatNo ratings yet

- Module - IVDocument73 pagesModule - IVRahul Singh100% (1)

- SBRIFRSForSMEs TutorSlidesDocument29 pagesSBRIFRSForSMEs TutorSlidesDipesh MagratiNo ratings yet

- Pcps FRF Sme Staff TrainingDocument44 pagesPcps FRF Sme Staff TrainingGreg MarsoNo ratings yet

- Comparison of Ind As and IFRSDocument10 pagesComparison of Ind As and IFRSAman SinghNo ratings yet

- CH 4 Financial Reposting QuestionsDocument4 pagesCH 4 Financial Reposting QuestionsAnthonny EmernegidoNo ratings yet

- IFRS1Document33 pagesIFRS1Ejiemen OkunegaNo ratings yet

- Unit 2 - GAAP and IFRSDocument15 pagesUnit 2 - GAAP and IFRSKanak RathoreNo ratings yet

- Theory QuestionsDocument6 pagesTheory Questionsanky1555No ratings yet

- Philippines IFRS ProfileDocument6 pagesPhilippines IFRS Profileaddicted17No ratings yet

- Spotting The Differences Between IFRS For SMEs and Full IFRSDocument5 pagesSpotting The Differences Between IFRS For SMEs and Full IFRSTannaoNo ratings yet

- Presentation01 (2) - 1Document21 pagesPresentation01 (2) - 1v7891283965No ratings yet

- Operating a Business and Employment in the United Kingdom: Part Three of The Investors' Guide to the United Kingdom 2015/16From EverandOperating a Business and Employment in the United Kingdom: Part Three of The Investors' Guide to the United Kingdom 2015/16No ratings yet

- Taxation Unit 7 - Concept Questions 2023Document6 pagesTaxation Unit 7 - Concept Questions 2023havengroupnaNo ratings yet

- Unit 3 Slides - VO Part 2 of 2Document10 pagesUnit 3 Slides - VO Part 2 of 2havengroupnaNo ratings yet

- Taxation Unit 3 - Tutorial QuestionDocument8 pagesTaxation Unit 3 - Tutorial QuestionhavengroupnaNo ratings yet

- Unit 3 - Lecture Slides FINALDocument30 pagesUnit 3 - Lecture Slides FINALhavengroupnaNo ratings yet

- Taxation Unit 3 - Concept Questions 2023Document6 pagesTaxation Unit 3 - Concept Questions 2023havengroupnaNo ratings yet

- Unit 3 - Cost AssignmentDocument17 pagesUnit 3 - Cost AssignmenthavengroupnaNo ratings yet

- Unit 3 - Tut QuestionDocument1 pageUnit 3 - Tut QuestionhavengroupnaNo ratings yet

- G.R. No. 194001Document11 pagesG.R. No. 194001dlyyapNo ratings yet

- Starconnect Retail Transaction Request FormDocument1 pageStarconnect Retail Transaction Request Formatanudas001No ratings yet

- Special Leave Petition Format For SC of IndiaDocument8 pagesSpecial Leave Petition Format For SC of IndiaRahul SharmaNo ratings yet

- 07 - Chapter 1Document51 pages07 - Chapter 1Yash JaiswalNo ratings yet

- ReceiptDocument3 pagesReceiptAhsan KhanNo ratings yet

- Zombie Gospel TractDocument8 pagesZombie Gospel TractSimplyBeliefNo ratings yet

- Legal Basis of MapehDocument34 pagesLegal Basis of MapehMaeNo ratings yet

- 4 Lives, New IntroductionDocument10 pages4 Lives, New IntroductionSaraNo ratings yet

- GR No. 92191-92 - Co - Balanquit V HRETDocument23 pagesGR No. 92191-92 - Co - Balanquit V HRETEmman FernandezNo ratings yet

- An Analysis Model of Industrial International CompetitivenessDocument4 pagesAn Analysis Model of Industrial International CompetitivenessYasir AltafNo ratings yet

- WW-II MoviesDocument68 pagesWW-II Moviesajitmondal_HUBNo ratings yet

- Japanese HamletDocument2 pagesJapanese HamlethannahNo ratings yet

- Mas Numerate ResultDocument147 pagesMas Numerate ResultNodelyn ReyesNo ratings yet

- Harper College Phlebotomy Student Handbook 2021-2022Document39 pagesHarper College Phlebotomy Student Handbook 2021-2022Ana mariaNo ratings yet

- Aadhaar CardDocument1 pageAadhaar CardkailashhapaserNo ratings yet

- Unit 10 - Market Leader AdvancedDocument4 pagesUnit 10 - Market Leader AdvancedIa GioshviliNo ratings yet

- Delhivery: COD: Check The Payable Amount On The AppDocument1 pageDelhivery: COD: Check The Payable Amount On The Appnaghmafirdous8697438306No ratings yet

- Homeopathic Materia Medica Vol 1Document259 pagesHomeopathic Materia Medica Vol 1LotusGuy Hans100% (3)

- Rajkot N-Equity QuotationDocument3 pagesRajkot N-Equity QuotationanilravraniNo ratings yet

- Hey Can I Try ThatDocument20 pagesHey Can I Try Thatapi-273078602No ratings yet

- Fil-Estate Properties Vs Spouses Go (GR No 185798, 13 Jan 2014)Document3 pagesFil-Estate Properties Vs Spouses Go (GR No 185798, 13 Jan 2014)Wilfred MartinezNo ratings yet

- YOKDIL Ingilizce SosyalbilimDocument26 pagesYOKDIL Ingilizce SosyalbilimSüleyman UlukuşNo ratings yet

- Anticipation Guide-The OutsidersDocument2 pagesAnticipation Guide-The OutsidersAnthony FabianNo ratings yet

- Halfling Rogue BackstoryDocument2 pagesHalfling Rogue BackstoryalexNo ratings yet

- COPPERMASK - FAQsDocument28 pagesCOPPERMASK - FAQsvernalbelasonNo ratings yet

- Democracy in Pakistan Hopes and Hurdles PDFDocument3 pagesDemocracy in Pakistan Hopes and Hurdles PDFGul RaazNo ratings yet

- Chapter5 PDFDocument50 pagesChapter5 PDFtowiwaNo ratings yet

- Drug Abuse ViewpointsDocument174 pagesDrug Abuse ViewpointsMhel DemabogteNo ratings yet

- Ticket InspectorDocument3 pagesTicket Inspectorsowhalima224No ratings yet