Finf311 DRM

Finf311 DRM

You might also like

- Edexcel Gcse 9 1 Business Revision GuideDocument23 pagesEdexcel Gcse 9 1 Business Revision GuideJoko EliasNo ratings yet

- Group9 - SectionB - TruEarth Case AnalysisDocument3 pagesGroup9 - SectionB - TruEarth Case AnalysisKARAN SEHGALNo ratings yet

- Syllabus Capital MarketsDocument4 pagesSyllabus Capital MarketsAdnan MasoodNo ratings yet

- Customer Connections - New Strategies For Growth (PDFDrive)Document281 pagesCustomer Connections - New Strategies For Growth (PDFDrive)Ruchi BarejaNo ratings yet

- Changes in Business Operations: Complete The Gaps in These Sentences Using The Words From The BoxDocument3 pagesChanges in Business Operations: Complete The Gaps in These Sentences Using The Words From The BoxMariem BejiNo ratings yet

- MasDocument36 pagesMasClareng Anne57% (7)

- Econ F354 - Fin F311 - DRMDocument5 pagesEcon F354 - Fin F311 - DRMf20220292No ratings yet

- PPM123Document4 pagesPPM123sneha bhongadeNo ratings yet

- FIN F311 - Derivative and Risk Management (2) - CMSDocument6 pagesFIN F311 - Derivative and Risk Management (2) - CMSSaksham GoyalNo ratings yet

- Birla Institute of Technology and Science, Pilani Pilani Campus AUGS/ AGSR DivisionDocument6 pagesBirla Institute of Technology and Science, Pilani Pilani Campus AUGS/ AGSR DivisionArchak SinghNo ratings yet

- Econ F354 1565 20230816113358Document5 pagesEcon F354 1565 20230816113358AMAN GUPTANo ratings yet

- Credits Faculty Name Program Academic Year and Term Option, Futures and Swaps 1. Course DescriptionDocument3 pagesCredits Faculty Name Program Academic Year and Term Option, Futures and Swaps 1. Course DescriptionAyushi GautamNo ratings yet

- Course No. Course Title Instructor-In-ChargeDocument4 pagesCourse No. Course Title Instructor-In-ChargeAryan JainNo ratings yet

- First Semester 2021-22Document5 pagesFirst Semester 2021-22Anish ChettlaNo ratings yet

- Dmgt513 Derivatives and Risk ManagementDocument205 pagesDmgt513 Derivatives and Risk ManagementDivyaNo ratings yet

- UntitledDocument37 pagesUntitledMANSI JOSHINo ratings yet

- FRM Financial Risk Management BrochureDocument2 pagesFRM Financial Risk Management Brochuresikute kamongwaNo ratings yet

- Global Securities Markets: ObjectivesDocument9 pagesGlobal Securities Markets: ObjectivesAkshayNo ratings yet

- 10 GSM - SB - 191104 PDFDocument9 pages10 GSM - SB - 191104 PDFAkshayNo ratings yet

- RMD New SyllabusDocument4 pagesRMD New SyllabusRancho RanchoNo ratings yet

- Financial Derivaties - NotesDocument49 pagesFinancial Derivaties - NotesVaibhav Badgi100% (2)

- Syllabus International FinanceDocument1 pageSyllabus International FinanceRabin JoshiNo ratings yet

- Derivatives & Risk Management SyllabusDocument2 pagesDerivatives & Risk Management SyllabusDivyeshNo ratings yet

- FD - Study Material - ManagementDocument2 pagesFD - Study Material - ManagementGaurang PandyaNo ratings yet

- Risk ManagementDocument6 pagesRisk ManagementsaurabhNo ratings yet

- Dr. Jayaraman BalakrishnanDocument19 pagesDr. Jayaraman BalakrishnanAhmed MunawarNo ratings yet

- Chapter 1Document32 pagesChapter 1k60.2112340088No ratings yet

- Delgado Francisco - Derivados Financieros (2010)Document486 pagesDelgado Francisco - Derivados Financieros (2010)renex02No ratings yet

- HDFC Ar 17Document3 pagesHDFC Ar 17baz chackoNo ratings yet

- Course IrdbmDocument1 pageCourse IrdbmRajneesh PandeyNo ratings yet

- Fincail Amrkets Analysis For Goverment OfficcialsDocument8 pagesFincail Amrkets Analysis For Goverment OfficcialsmarcoNo ratings yet

- Forex SyllabusDocument5 pagesForex Syllabussubham kumarNo ratings yet

- IJREAMV05I0452086745Document4 pagesIJREAMV05I0452086745yash wankhadeNo ratings yet

- Future of Derivatives in India: RATAN DEEP SINGH - 200628522Document52 pagesFuture of Derivatives in India: RATAN DEEP SINGH - 200628522Pranjal jainNo ratings yet

- Course IrdbmDocument1 pageCourse IrdbmrahulkatareyNo ratings yet

- Currency Risk Management: Chapter Learning ObjectivesDocument25 pagesCurrency Risk Management: Chapter Learning ObjectivesDINEO PRUDENCE NONGNo ratings yet

- This Study Resource Was: Faculty of CommerceDocument2 pagesThis Study Resource Was: Faculty of CommercePhebieon MukwenhaNo ratings yet

- Course Oultine - International FinanceDocument5 pagesCourse Oultine - International FinancemitochondriNo ratings yet

- Providence College School of Business: FIN 417 Fixed Income Securities Fall 2021 Instructor: Matthew CallahanDocument51 pagesProvidence College School of Business: FIN 417 Fixed Income Securities Fall 2021 Instructor: Matthew CallahanAlexander MaffeoNo ratings yet

- T3 FMP 4 Ch4 Derivatives v5 6121c64371ea2Document20 pagesT3 FMP 4 Ch4 Derivatives v5 6121c64371ea2Christian Rey Magtibay100% (1)

- Course Contents Financial Market 1Document2 pagesCourse Contents Financial Market 1Shariz ParvezNo ratings yet

- Derivatives and Risk ManagementDocument5 pagesDerivatives and Risk ManagementPuneet GargNo ratings yet

- Financial Economics (HE54) : Course ObjectiveDocument3 pagesFinancial Economics (HE54) : Course ObjectiveSakshi SharmaNo ratings yet

- FINM550Document1 pageFINM550shagun guptaNo ratings yet

- PGDM Syllabus FDDocument1 pagePGDM Syllabus FDAnonymous H0SJWZE8No ratings yet

- Chapter Contents PG - NO. 1 3Document27 pagesChapter Contents PG - NO. 1 3Akash KatheNo ratings yet

- 3rd Sem MBA - International FinanceDocument1 page3rd Sem MBA - International FinanceSrestha ChatterjeeNo ratings yet

- Risk ManagementDocument152 pagesRisk ManagementKim Bales BlayNo ratings yet

- Natio Onal S Stock Excha Ange O F India A Limite ED: Interes ST Rate Deri Ivatives: A Beginner's S ModuleDocument1 pageNatio Onal S Stock Excha Ange O F India A Limite ED: Interes ST Rate Deri Ivatives: A Beginner's S ModuleSushil MundelNo ratings yet

- Financial DerivativesDocument3 pagesFinancial DerivativesAnonymous XV3SIjz8bNo ratings yet

- Risk Management Using Derivatives - Online: Students Will Be Able ToDocument7 pagesRisk Management Using Derivatives - Online: Students Will Be Able ToSunil KumarNo ratings yet

- Financial Markets and InstitutionsDocument5 pagesFinancial Markets and InstitutionsEng Abdikarim WalhadNo ratings yet

- PAM Outlines 07012021 042154pmDocument7 pagesPAM Outlines 07012021 042154pmzainabNo ratings yet

- Fixed Income Markets - Term-V - Prof. Vivek RajvanshiDocument5 pagesFixed Income Markets - Term-V - Prof. Vivek RajvanshiAcademic Management SystemNo ratings yet

- IIM-UDR-FIS-2020-Outline - Will Be ModifiedDocument6 pagesIIM-UDR-FIS-2020-Outline - Will Be Modifiedim masterNo ratings yet

- T-4 Financial Derivatives - FinalDocument4 pagesT-4 Financial Derivatives - FinalPalash AroraNo ratings yet

- Fundamentals of Perpetual FuturesDocument50 pagesFundamentals of Perpetual FuturesFatoke AdemolaNo ratings yet

- Treasury Products and PracticesDocument2 pagesTreasury Products and PracticesAbdallaNo ratings yet

- DBA 5035 - Financial Derivatives ManagementDocument277 pagesDBA 5035 - Financial Derivatives ManagementShrividhyaNo ratings yet

- Intro To DerivativeDocument45 pagesIntro To DerivativePalash HawelikarNo ratings yet

- AFA - 4e - PPT - Chap10 (For Students)Document56 pagesAFA - 4e - PPT - Chap10 (For Students)Cẩm Tú NguyễnNo ratings yet

- CFA L1 - DerivativesDocument44 pagesCFA L1 - Derivativesnur syahirah bt ab.rahmanNo ratings yet

- Currency OptionsDocument6 pagesCurrency OptionsDealCurry100% (1)

- Introduction To The Foreign Exchange & Money MarketsDocument3 pagesIntroduction To The Foreign Exchange & Money Marketsssj7cjqq2dNo ratings yet

- GSF212 EdccDocument3 pagesGSF212 EdccYash BhardwajNo ratings yet

- FINF315 FinManDocument4 pagesFINF315 FinManYash BhardwajNo ratings yet

- Eeef111 EsDocument2 pagesEeef111 EsYash BhardwajNo ratings yet

- PHYF110 PhyLabDocument19 pagesPHYF110 PhyLabYash BhardwajNo ratings yet

- Econf421 SapmDocument3 pagesEconf421 SapmYash BhardwajNo ratings yet

- MEF110 WorkshopDocument3 pagesMEF110 WorkshopYash BhardwajNo ratings yet

- Phyf111 MowDocument4 pagesPhyf111 MowYash BhardwajNo ratings yet

- CSF301 PoPLDocument2 pagesCSF301 PoPLYash BhardwajNo ratings yet

- MATHF112 Math2Document2 pagesMATHF112 Math2Yash BhardwajNo ratings yet

- Zara - Industry Analysis: Final Project Report OnDocument21 pagesZara - Industry Analysis: Final Project Report OnC J100% (1)

- Identifying Market Segments and Targets: Marketing ManagementDocument29 pagesIdentifying Market Segments and Targets: Marketing ManagementArvind KumarNo ratings yet

- Organizational Customers' Retention Strategies On CustomerDocument10 pagesOrganizational Customers' Retention Strategies On CustomerDon CM WanzalaNo ratings yet

- BPSC 105 Block - IIDocument43 pagesBPSC 105 Block - IIavinash.kumar.876424No ratings yet

- Kapilan K Resume 2020Document1 pageKapilan K Resume 2020api-547584495No ratings yet

- Mkt. Mgt. Final IMP + SolutionDocument43 pagesMkt. Mgt. Final IMP + Solutionvimalrparmar001No ratings yet

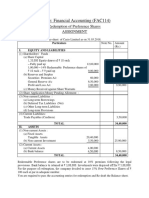

- Preference Shares AssignmentDocument4 pagesPreference Shares AssignmentDhairya ShahNo ratings yet

- COMP515 FA Formative Assignment 1 20213Document4 pagesCOMP515 FA Formative Assignment 1 20213hamzaNo ratings yet

- University of Science and Technology Chittagong: Faculty of Business Administration (FBA)Document7 pagesUniversity of Science and Technology Chittagong: Faculty of Business Administration (FBA)Pranab DharNo ratings yet

- Mr. Dhirendra Gaba (Managing Director)Document7 pagesMr. Dhirendra Gaba (Managing Director)Taruna AggarwalNo ratings yet

- Chapter 12 - The Strategy of International BusinessDocument13 pagesChapter 12 - The Strategy of International BusinessVictorie BuNo ratings yet

- Bs MorningDocument180 pagesBs MorningAwais AltafNo ratings yet

- Group 3 - HCL Technologies-FinalDocument5 pagesGroup 3 - HCL Technologies-FinalSumit RajNo ratings yet

- Chentia Aisya Oktarina - 242221055 - Magister ManajemenDocument34 pagesChentia Aisya Oktarina - 242221055 - Magister ManajemenChentia Aisya OktarinaNo ratings yet

- The Relationship Between Customer-Focused Capabilities and Information-Focused Capabilities On Firm Performance A Moderated Mediation Model Control Variables (Company Size)Document9 pagesThe Relationship Between Customer-Focused Capabilities and Information-Focused Capabilities On Firm Performance A Moderated Mediation Model Control Variables (Company Size)International Journal of Innovative Science and Research TechnologyNo ratings yet

- MGMT 4210 L4 Internal Analysis-1 PDFDocument24 pagesMGMT 4210 L4 Internal Analysis-1 PDFSin TungNo ratings yet

- 10 IFRS 3 Business CombinationDocument2 pages10 IFRS 3 Business CombinationDM BuenconsejoNo ratings yet

- Appendix A Table A. 1. List of Voluntary Disclosure ItemsDocument3 pagesAppendix A Table A. 1. List of Voluntary Disclosure ItemsyuliaNo ratings yet

- David DeCouto RESUME - 2020 PDFDocument3 pagesDavid DeCouto RESUME - 2020 PDFDavid John DeCoutoNo ratings yet

- CFI 10 Problems With SolutionsDocument4 pagesCFI 10 Problems With SolutionsPola PolzNo ratings yet

- Bible Compounding MoneyDocument172 pagesBible Compounding Moneyrock7902100% (1)

- Information Rules: Technology Meet EconomyDocument20 pagesInformation Rules: Technology Meet EconomyMuhammad Syahrul MaulidanNo ratings yet

- 2 CVP Analysis Final PDFDocument44 pages2 CVP Analysis Final PDFmoss roffattNo ratings yet

- Gr9 EMS (English) 2020 Exemplars Possible AnswersDocument8 pagesGr9 EMS (English) 2020 Exemplars Possible AnswersZizipho MakaulaNo ratings yet

- Reflection#4 - Asset ManagementDocument2 pagesReflection#4 - Asset ManagementnerieroseNo ratings yet

Download as pdf or txt

You might also like

- Edexcel Gcse 9 1 Business Revision GuideDocument23 pagesEdexcel Gcse 9 1 Business Revision GuideJoko EliasNo ratings yet

- Group9 - SectionB - TruEarth Case AnalysisDocument3 pagesGroup9 - SectionB - TruEarth Case AnalysisKARAN SEHGALNo ratings yet

- Syllabus Capital MarketsDocument4 pagesSyllabus Capital MarketsAdnan MasoodNo ratings yet

- Customer Connections - New Strategies For Growth (PDFDrive)Document281 pagesCustomer Connections - New Strategies For Growth (PDFDrive)Ruchi BarejaNo ratings yet

- Changes in Business Operations: Complete The Gaps in These Sentences Using The Words From The BoxDocument3 pagesChanges in Business Operations: Complete The Gaps in These Sentences Using The Words From The BoxMariem BejiNo ratings yet

- MasDocument36 pagesMasClareng Anne57% (7)

- Econ F354 - Fin F311 - DRMDocument5 pagesEcon F354 - Fin F311 - DRMf20220292No ratings yet

- PPM123Document4 pagesPPM123sneha bhongadeNo ratings yet

- FIN F311 - Derivative and Risk Management (2) - CMSDocument6 pagesFIN F311 - Derivative and Risk Management (2) - CMSSaksham GoyalNo ratings yet

- Birla Institute of Technology and Science, Pilani Pilani Campus AUGS/ AGSR DivisionDocument6 pagesBirla Institute of Technology and Science, Pilani Pilani Campus AUGS/ AGSR DivisionArchak SinghNo ratings yet

- Econ F354 1565 20230816113358Document5 pagesEcon F354 1565 20230816113358AMAN GUPTANo ratings yet

- Credits Faculty Name Program Academic Year and Term Option, Futures and Swaps 1. Course DescriptionDocument3 pagesCredits Faculty Name Program Academic Year and Term Option, Futures and Swaps 1. Course DescriptionAyushi GautamNo ratings yet

- Course No. Course Title Instructor-In-ChargeDocument4 pagesCourse No. Course Title Instructor-In-ChargeAryan JainNo ratings yet

- First Semester 2021-22Document5 pagesFirst Semester 2021-22Anish ChettlaNo ratings yet

- Dmgt513 Derivatives and Risk ManagementDocument205 pagesDmgt513 Derivatives and Risk ManagementDivyaNo ratings yet

- UntitledDocument37 pagesUntitledMANSI JOSHINo ratings yet

- FRM Financial Risk Management BrochureDocument2 pagesFRM Financial Risk Management Brochuresikute kamongwaNo ratings yet

- Global Securities Markets: ObjectivesDocument9 pagesGlobal Securities Markets: ObjectivesAkshayNo ratings yet

- 10 GSM - SB - 191104 PDFDocument9 pages10 GSM - SB - 191104 PDFAkshayNo ratings yet

- RMD New SyllabusDocument4 pagesRMD New SyllabusRancho RanchoNo ratings yet

- Financial Derivaties - NotesDocument49 pagesFinancial Derivaties - NotesVaibhav Badgi100% (2)

- Syllabus International FinanceDocument1 pageSyllabus International FinanceRabin JoshiNo ratings yet

- Derivatives & Risk Management SyllabusDocument2 pagesDerivatives & Risk Management SyllabusDivyeshNo ratings yet

- FD - Study Material - ManagementDocument2 pagesFD - Study Material - ManagementGaurang PandyaNo ratings yet

- Risk ManagementDocument6 pagesRisk ManagementsaurabhNo ratings yet

- Dr. Jayaraman BalakrishnanDocument19 pagesDr. Jayaraman BalakrishnanAhmed MunawarNo ratings yet

- Chapter 1Document32 pagesChapter 1k60.2112340088No ratings yet

- Delgado Francisco - Derivados Financieros (2010)Document486 pagesDelgado Francisco - Derivados Financieros (2010)renex02No ratings yet

- HDFC Ar 17Document3 pagesHDFC Ar 17baz chackoNo ratings yet

- Course IrdbmDocument1 pageCourse IrdbmRajneesh PandeyNo ratings yet

- Fincail Amrkets Analysis For Goverment OfficcialsDocument8 pagesFincail Amrkets Analysis For Goverment OfficcialsmarcoNo ratings yet

- Forex SyllabusDocument5 pagesForex Syllabussubham kumarNo ratings yet

- IJREAMV05I0452086745Document4 pagesIJREAMV05I0452086745yash wankhadeNo ratings yet

- Future of Derivatives in India: RATAN DEEP SINGH - 200628522Document52 pagesFuture of Derivatives in India: RATAN DEEP SINGH - 200628522Pranjal jainNo ratings yet

- Course IrdbmDocument1 pageCourse IrdbmrahulkatareyNo ratings yet

- Currency Risk Management: Chapter Learning ObjectivesDocument25 pagesCurrency Risk Management: Chapter Learning ObjectivesDINEO PRUDENCE NONGNo ratings yet

- This Study Resource Was: Faculty of CommerceDocument2 pagesThis Study Resource Was: Faculty of CommercePhebieon MukwenhaNo ratings yet

- Course Oultine - International FinanceDocument5 pagesCourse Oultine - International FinancemitochondriNo ratings yet

- Providence College School of Business: FIN 417 Fixed Income Securities Fall 2021 Instructor: Matthew CallahanDocument51 pagesProvidence College School of Business: FIN 417 Fixed Income Securities Fall 2021 Instructor: Matthew CallahanAlexander MaffeoNo ratings yet

- T3 FMP 4 Ch4 Derivatives v5 6121c64371ea2Document20 pagesT3 FMP 4 Ch4 Derivatives v5 6121c64371ea2Christian Rey Magtibay100% (1)

- Course Contents Financial Market 1Document2 pagesCourse Contents Financial Market 1Shariz ParvezNo ratings yet

- Derivatives and Risk ManagementDocument5 pagesDerivatives and Risk ManagementPuneet GargNo ratings yet

- Financial Economics (HE54) : Course ObjectiveDocument3 pagesFinancial Economics (HE54) : Course ObjectiveSakshi SharmaNo ratings yet

- FINM550Document1 pageFINM550shagun guptaNo ratings yet

- PGDM Syllabus FDDocument1 pagePGDM Syllabus FDAnonymous H0SJWZE8No ratings yet

- Chapter Contents PG - NO. 1 3Document27 pagesChapter Contents PG - NO. 1 3Akash KatheNo ratings yet

- 3rd Sem MBA - International FinanceDocument1 page3rd Sem MBA - International FinanceSrestha ChatterjeeNo ratings yet

- Risk ManagementDocument152 pagesRisk ManagementKim Bales BlayNo ratings yet

- Natio Onal S Stock Excha Ange O F India A Limite ED: Interes ST Rate Deri Ivatives: A Beginner's S ModuleDocument1 pageNatio Onal S Stock Excha Ange O F India A Limite ED: Interes ST Rate Deri Ivatives: A Beginner's S ModuleSushil MundelNo ratings yet

- Financial DerivativesDocument3 pagesFinancial DerivativesAnonymous XV3SIjz8bNo ratings yet

- Risk Management Using Derivatives - Online: Students Will Be Able ToDocument7 pagesRisk Management Using Derivatives - Online: Students Will Be Able ToSunil KumarNo ratings yet

- Financial Markets and InstitutionsDocument5 pagesFinancial Markets and InstitutionsEng Abdikarim WalhadNo ratings yet

- PAM Outlines 07012021 042154pmDocument7 pagesPAM Outlines 07012021 042154pmzainabNo ratings yet

- Fixed Income Markets - Term-V - Prof. Vivek RajvanshiDocument5 pagesFixed Income Markets - Term-V - Prof. Vivek RajvanshiAcademic Management SystemNo ratings yet

- IIM-UDR-FIS-2020-Outline - Will Be ModifiedDocument6 pagesIIM-UDR-FIS-2020-Outline - Will Be Modifiedim masterNo ratings yet

- T-4 Financial Derivatives - FinalDocument4 pagesT-4 Financial Derivatives - FinalPalash AroraNo ratings yet

- Fundamentals of Perpetual FuturesDocument50 pagesFundamentals of Perpetual FuturesFatoke AdemolaNo ratings yet

- Treasury Products and PracticesDocument2 pagesTreasury Products and PracticesAbdallaNo ratings yet

- DBA 5035 - Financial Derivatives ManagementDocument277 pagesDBA 5035 - Financial Derivatives ManagementShrividhyaNo ratings yet

- Intro To DerivativeDocument45 pagesIntro To DerivativePalash HawelikarNo ratings yet

- AFA - 4e - PPT - Chap10 (For Students)Document56 pagesAFA - 4e - PPT - Chap10 (For Students)Cẩm Tú NguyễnNo ratings yet

- CFA L1 - DerivativesDocument44 pagesCFA L1 - Derivativesnur syahirah bt ab.rahmanNo ratings yet

- Currency OptionsDocument6 pagesCurrency OptionsDealCurry100% (1)

- Introduction To The Foreign Exchange & Money MarketsDocument3 pagesIntroduction To The Foreign Exchange & Money Marketsssj7cjqq2dNo ratings yet

- GSF212 EdccDocument3 pagesGSF212 EdccYash BhardwajNo ratings yet

- FINF315 FinManDocument4 pagesFINF315 FinManYash BhardwajNo ratings yet

- Eeef111 EsDocument2 pagesEeef111 EsYash BhardwajNo ratings yet

- PHYF110 PhyLabDocument19 pagesPHYF110 PhyLabYash BhardwajNo ratings yet

- Econf421 SapmDocument3 pagesEconf421 SapmYash BhardwajNo ratings yet

- MEF110 WorkshopDocument3 pagesMEF110 WorkshopYash BhardwajNo ratings yet

- Phyf111 MowDocument4 pagesPhyf111 MowYash BhardwajNo ratings yet

- CSF301 PoPLDocument2 pagesCSF301 PoPLYash BhardwajNo ratings yet

- MATHF112 Math2Document2 pagesMATHF112 Math2Yash BhardwajNo ratings yet

- Zara - Industry Analysis: Final Project Report OnDocument21 pagesZara - Industry Analysis: Final Project Report OnC J100% (1)

- Identifying Market Segments and Targets: Marketing ManagementDocument29 pagesIdentifying Market Segments and Targets: Marketing ManagementArvind KumarNo ratings yet

- Organizational Customers' Retention Strategies On CustomerDocument10 pagesOrganizational Customers' Retention Strategies On CustomerDon CM WanzalaNo ratings yet

- BPSC 105 Block - IIDocument43 pagesBPSC 105 Block - IIavinash.kumar.876424No ratings yet

- Kapilan K Resume 2020Document1 pageKapilan K Resume 2020api-547584495No ratings yet

- Mkt. Mgt. Final IMP + SolutionDocument43 pagesMkt. Mgt. Final IMP + Solutionvimalrparmar001No ratings yet

- Preference Shares AssignmentDocument4 pagesPreference Shares AssignmentDhairya ShahNo ratings yet

- COMP515 FA Formative Assignment 1 20213Document4 pagesCOMP515 FA Formative Assignment 1 20213hamzaNo ratings yet

- University of Science and Technology Chittagong: Faculty of Business Administration (FBA)Document7 pagesUniversity of Science and Technology Chittagong: Faculty of Business Administration (FBA)Pranab DharNo ratings yet

- Mr. Dhirendra Gaba (Managing Director)Document7 pagesMr. Dhirendra Gaba (Managing Director)Taruna AggarwalNo ratings yet

- Chapter 12 - The Strategy of International BusinessDocument13 pagesChapter 12 - The Strategy of International BusinessVictorie BuNo ratings yet

- Bs MorningDocument180 pagesBs MorningAwais AltafNo ratings yet

- Group 3 - HCL Technologies-FinalDocument5 pagesGroup 3 - HCL Technologies-FinalSumit RajNo ratings yet

- Chentia Aisya Oktarina - 242221055 - Magister ManajemenDocument34 pagesChentia Aisya Oktarina - 242221055 - Magister ManajemenChentia Aisya OktarinaNo ratings yet

- The Relationship Between Customer-Focused Capabilities and Information-Focused Capabilities On Firm Performance A Moderated Mediation Model Control Variables (Company Size)Document9 pagesThe Relationship Between Customer-Focused Capabilities and Information-Focused Capabilities On Firm Performance A Moderated Mediation Model Control Variables (Company Size)International Journal of Innovative Science and Research TechnologyNo ratings yet

- MGMT 4210 L4 Internal Analysis-1 PDFDocument24 pagesMGMT 4210 L4 Internal Analysis-1 PDFSin TungNo ratings yet

- 10 IFRS 3 Business CombinationDocument2 pages10 IFRS 3 Business CombinationDM BuenconsejoNo ratings yet

- Appendix A Table A. 1. List of Voluntary Disclosure ItemsDocument3 pagesAppendix A Table A. 1. List of Voluntary Disclosure ItemsyuliaNo ratings yet

- David DeCouto RESUME - 2020 PDFDocument3 pagesDavid DeCouto RESUME - 2020 PDFDavid John DeCoutoNo ratings yet

- CFI 10 Problems With SolutionsDocument4 pagesCFI 10 Problems With SolutionsPola PolzNo ratings yet

- Bible Compounding MoneyDocument172 pagesBible Compounding Moneyrock7902100% (1)

- Information Rules: Technology Meet EconomyDocument20 pagesInformation Rules: Technology Meet EconomyMuhammad Syahrul MaulidanNo ratings yet

- 2 CVP Analysis Final PDFDocument44 pages2 CVP Analysis Final PDFmoss roffattNo ratings yet

- Gr9 EMS (English) 2020 Exemplars Possible AnswersDocument8 pagesGr9 EMS (English) 2020 Exemplars Possible AnswersZizipho MakaulaNo ratings yet

- Reflection#4 - Asset ManagementDocument2 pagesReflection#4 - Asset ManagementnerieroseNo ratings yet