Solution Manual For Financial Accounting Canadian 6Th Edition by Libby Isbn 1259105695 978125910569 Full Chapter PDF

Solution Manual For Financial Accounting Canadian 6Th Edition by Libby Isbn 1259105695 978125910569 Full Chapter PDF

You might also like

- Teacher Leadership For Social Justice Building A Curriculum For Liberation Revised First Ed Edition Full ChapterDocument41 pagesTeacher Leadership For Social Justice Building A Curriculum For Liberation Revised First Ed Edition Full Chapterjamie.nettles908100% (29)

- Essentials of Human Diseases and Conditions 6th Edition Frazier Test Bank Full Chapter PDFDocument32 pagesEssentials of Human Diseases and Conditions 6th Edition Frazier Test Bank Full Chapter PDFEugeneMurraykspo100% (14)

- CHAPTER 10 - AnswerDocument5 pagesCHAPTER 10 - Answernash100% (2)

- Solution Manual For Financial Accounting Canadian Canadian 5Th Edition by Libby Isbn 0071339469 9780071339469 Full Chapter PDFDocument36 pagesSolution Manual For Financial Accounting Canadian Canadian 5Th Edition by Libby Isbn 0071339469 9780071339469 Full Chapter PDFcarmen.hall969100% (11)

- Solution Manual For Financial Accounting Canadian 6Th Edition by Harrison Isbn 0134141091 978013414109 Full Chapter PDFDocument36 pagesSolution Manual For Financial Accounting Canadian 6Th Edition by Harrison Isbn 0134141091 978013414109 Full Chapter PDFcarmen.hall969100% (11)

- Solution Manual For Financial Accounting Canadian 5Th Edition by Harrison Isbn 0132979276 9780132979276 Full Chapter PDFDocument36 pagesSolution Manual For Financial Accounting Canadian 5Th Edition by Harrison Isbn 0132979276 9780132979276 Full Chapter PDFcarmen.hall969100% (12)

- Solution Manual For Financial Accounting Fundamentals 4Th Edition by Wild Isbn 0078025591 9780078025594 Full Chapter PDFDocument36 pagesSolution Manual For Financial Accounting Fundamentals 4Th Edition by Wild Isbn 0078025591 9780078025594 Full Chapter PDFcarmen.hall969100% (12)

- Solution Manual For Financial Accounting Canadian 2Nd Edition by Waybright Isbn 0133375536 9780133375534 Full Chapter PDFDocument36 pagesSolution Manual For Financial Accounting Canadian 2Nd Edition by Waybright Isbn 0133375536 9780133375534 Full Chapter PDFcarmen.hall969100% (12)

- Enhanced Computer Concepts and Microsoft Office 2013 Illustrated 1St Edition Parsons Test Bank Full Chapter PDFDocument36 pagesEnhanced Computer Concepts and Microsoft Office 2013 Illustrated 1St Edition Parsons Test Bank Full Chapter PDFrichard.eis609100% (10)

- Enhanced Discovering Computers and Microsoft Office 2013 A Combined Fundamental Approach 1St Edition Vermaat Test Bank Full Chapter PDFDocument36 pagesEnhanced Discovering Computers and Microsoft Office 2013 A Combined Fundamental Approach 1St Edition Vermaat Test Bank Full Chapter PDFrichard.eis609100% (10)

- Solution Manual For Financial Accounting An Introduction To Concepts Methods and Uses 14th Edition by Weil ISBN 1111823456 9781111823450Document36 pagesSolution Manual For Financial Accounting An Introduction To Concepts Methods and Uses 14th Edition by Weil ISBN 1111823456 9781111823450carmen.hall969100% (11)

- Solution Manual For Financial Accounting Fundamentals 5Th Edition by Wild Isbn 0078025753 9780078025754 Full Chapter PDFDocument36 pagesSolution Manual For Financial Accounting Fundamentals 5Th Edition by Wild Isbn 0078025753 9780078025754 Full Chapter PDFcarmen.hall969100% (11)

- Enhanced Computer Concepts and Microsoft Office 2013 Illustrated 1St Edition Parsons Solutions Manual Full Chapter PDFDocument36 pagesEnhanced Computer Concepts and Microsoft Office 2013 Illustrated 1St Edition Parsons Solutions Manual Full Chapter PDFrichard.eis609100% (11)

- Engineering Problem Solving With C++ 4Th Edition Etter Test Bank Full Chapter PDFDocument26 pagesEngineering Problem Solving With C++ 4Th Edition Etter Test Bank Full Chapter PDFrichard.eis609100% (12)

- Engineering Problem Solving With C++ 4Th Edition Etter Solutions Manual Full Chapter PDFDocument36 pagesEngineering Problem Solving With C++ 4Th Edition Etter Solutions Manual Full Chapter PDFrichard.eis609100% (11)

- Engineering Mechanics Statics and Dynamics 2Nd Edition Plesha Solutions Manual Full Chapter PDFDocument46 pagesEngineering Mechanics Statics and Dynamics 2Nd Edition Plesha Solutions Manual Full Chapter PDFrichard.eis609100% (10)

- Engineering Mechanics Statics 4Th Edition Pytel Solutions Manual Full Chapter PDFDocument36 pagesEngineering Mechanics Statics 4Th Edition Pytel Solutions Manual Full Chapter PDFrichard.eis609100% (10)

- Test Bank For Psychology 1St Edition Marin Hock 0205920012 9780205920013 Full Chapter PDFDocument36 pagesTest Bank For Psychology 1St Edition Marin Hock 0205920012 9780205920013 Full Chapter PDFsamantha.garcia508100% (9)

- Creating MacrosDocument36 pagesCreating Macroschristine.jackson281100% (10)

- Engineering Mechanics Dynamics 4Th Edition Pytel Solutions Manual Full Chapter PDFDocument27 pagesEngineering Mechanics Dynamics 4Th Edition Pytel Solutions Manual Full Chapter PDFrichard.eis609100% (12)

- Cornerstones of Financial Accounting Canadian 2Nd Edition Rich Test Bank Full Chapter PDFDocument36 pagesCornerstones of Financial Accounting Canadian 2Nd Edition Rich Test Bank Full Chapter PDFrenee.crawford887100% (12)

- Attacking The Elites What Critics Get Wrong and Right About Americas Leading Universities Derek Bok Full ChapterDocument47 pagesAttacking The Elites What Critics Get Wrong and Right About Americas Leading Universities Derek Bok Full Chaptermario.becker252100% (8)

- Cornerstones of Managerial Accounting 6Th Edition Mowen Solutions Manual Full Chapter PDFDocument36 pagesCornerstones of Managerial Accounting 6Th Edition Mowen Solutions Manual Full Chapter PDFrenee.crawford887100% (10)

- Marketing The Core 5Th Edition Kerin Test Bank Full Chapter PDFDocument36 pagesMarketing The Core 5Th Edition Kerin Test Bank Full Chapter PDFfay.rowden768100% (12)

- Test Bank For Criminal Procedure 3Rd Edition by Lippman Isbn 1506306497 9781506306490 Full Chapter PDFDocument31 pagesTest Bank For Criminal Procedure 3Rd Edition by Lippman Isbn 1506306497 9781506306490 Full Chapter PDFdouglas.valadez414100% (11)

- Test Bank For Criminal Law 1St Edition by Russell Brown Davis Isbn 1412977894 9781412977890 Full Chapter PDFDocument31 pagesTest Bank For Criminal Law 1St Edition by Russell Brown Davis Isbn 1412977894 9781412977890 Full Chapter PDFdouglas.valadez414100% (11)

- Thermodynamics An Engineering Approach 8Th Edition Cengel Test Bank Full Chapter PDFDocument32 pagesThermodynamics An Engineering Approach 8Th Edition Cengel Test Bank Full Chapter PDFgeraldine.wells536100% (11)

- Building and Using QueriesDocument36 pagesBuilding and Using Querieschristine.jackson281100% (11)

- Cornerstones of Managerial Accounting 5Th Edition Mowen Solutions Manual Full Chapter PDFDocument36 pagesCornerstones of Managerial Accounting 5Th Edition Mowen Solutions Manual Full Chapter PDFrenee.crawford887100% (9)

- Microeconomics 20Th Edition Mcconnell Solutions Manual Full Chapter PDFDocument30 pagesMicroeconomics 20Th Edition Mcconnell Solutions Manual Full Chapter PDFcythia.tait735100% (12)

- Test Bank For Psychology Perspectives and Connections 3Rd Edition Feist Rosenberg 0077861876 978007786187 Full Chapter PDFDocument46 pagesTest Bank For Psychology Perspectives and Connections 3Rd Edition Feist Rosenberg 0077861876 978007786187 Full Chapter PDFcraig.gibbons469100% (11)

- Microeconomics 2Nd Edition Goolsbee Test Bank Full Chapter PDFDocument36 pagesMicroeconomics 2Nd Edition Goolsbee Test Bank Full Chapter PDFcythia.tait735100% (12)

- Populism and Civil Society The Challenge To Constitutional Democracy Andrew Arato 2 All ChapterDocument67 pagesPopulism and Civil Society The Challenge To Constitutional Democracy Andrew Arato 2 All Chapterdenise.murry935100% (10)

- Test Bank For Business Communication Essentials 7Th Edition by Bovee Full Chapter PDFDocument36 pagesTest Bank For Business Communication Essentials 7Th Edition by Bovee Full Chapter PDFlaurence.harris245100% (11)

- Test Bank For Modern Competitive Strategy 4Th Edition Walker Madsen 1259181200 9781259181207 Full Chapter PDFDocument33 pagesTest Bank For Modern Competitive Strategy 4Th Edition Walker Madsen 1259181200 9781259181207 Full Chapter PDFkenneth.miller246100% (11)

- Feelings Transformed Philosophical Theories of The Emotions 1270 1670 Dominik Perler Full ChapterDocument67 pagesFeelings Transformed Philosophical Theories of The Emotions 1270 1670 Dominik Perler Full Chapteralfred.jessie484100% (20)

- Fundamentals of Data and Signals: Learning ObjectivesDocument32 pagesFundamentals of Data and Signals: Learning Objectivesdeborah.porter960100% (11)

- Essential University Physics 3Rd Edition Richard Wolfson Test Bank Full Chapter PDFDocument32 pagesEssential University Physics 3Rd Edition Richard Wolfson Test Bank Full Chapter PDFteresa.mccoin592100% (12)

- Test Bank For Absolute C 5Th Edition Savitch Mock 013283071X 9780132830713 Full Chapter PDFDocument31 pagesTest Bank For Absolute C 5Th Edition Savitch Mock 013283071X 9780132830713 Full Chapter PDFmiranda.barnhart699100% (12)

- 500 Act Science Questions To Know by Test Day 3Rd Edition Inc Anaxos Full ChapterDocument77 pages500 Act Science Questions To Know by Test Day 3Rd Edition Inc Anaxos Full Chapternicholas.leno709100% (8)

- Macroeconomics Canadian 8Th Edition Sayre Test Bank Full Chapter PDFDocument36 pagesMacroeconomics Canadian 8Th Edition Sayre Test Bank Full Chapter PDFkevin.reider416100% (11)

- Management Canadian 11Th Edition Robbins Test Bank Full Chapter PDFDocument36 pagesManagement Canadian 11Th Edition Robbins Test Bank Full Chapter PDFalejandro.perdue730100% (12)

- Cornerstones of Managerial Accounting Canadian 2Nd Edition Mowen Solutions Manual Full Chapter PDFDocument36 pagesCornerstones of Managerial Accounting Canadian 2Nd Edition Mowen Solutions Manual Full Chapter PDFrenee.crawford887100% (7)

- Solution Manual For Hydrologic Analysis and Design 4Th Edition Mccuen 0134313127 978013431312 Full Chapter PDFDocument36 pagesSolution Manual For Hydrologic Analysis and Design 4Th Edition Mccuen 0134313127 978013431312 Full Chapter PDFchristine.jackson281100% (11)

- Microeconomics 20Th Edition Mcconnell Test Bank Full Chapter PDFDocument36 pagesMicroeconomics 20Th Edition Mcconnell Test Bank Full Chapter PDFcythia.tait735100% (10)

- Test Bank For Medical Terminology For Health Professions 7Th Edition Ehrlich Schroeder 1111543275 9781111543273 Full Chapter PDFDocument27 pagesTest Bank For Medical Terminology For Health Professions 7Th Edition Ehrlich Schroeder 1111543275 9781111543273 Full Chapter PDFkacey.perreault490100% (11)

- Essential Statistics 1St Edition Navidi Solutions Manual Full Chapter PDFDocument36 pagesEssential Statistics 1St Edition Navidi Solutions Manual Full Chapter PDFteresa.mccoin592100% (11)

- Test Bank For Abnormal Psychology Clinical Perspectives On Psychological Disorders 7th Edition Whitbourne Halgin 0078035279 9780078035272Document36 pagesTest Bank For Abnormal Psychology Clinical Perspectives On Psychological Disorders 7th Edition Whitbourne Halgin 0078035279 9780078035272miranda.barnhart699100% (11)

- Test Bank For Methods in Behavioral Research 12Th Edition Cozby Bates 0077861892 9780077861896 Full Chapter PDFDocument36 pagesTest Bank For Methods in Behavioral Research 12Th Edition Cozby Bates 0077861892 9780077861896 Full Chapter PDFpauline.ganley829100% (12)

- Corrosion Policy Decision Making Science Engineering Management and Economy Reza Javaherdashti Full ChapterDocument61 pagesCorrosion Policy Decision Making Science Engineering Management and Economy Reza Javaherdashti Full Chaptermartha.conrad799100% (10)

- Teachers Schools and Society A Brief Introduction To Education 5Th Edition Full ChapterDocument41 pagesTeachers Schools and Society A Brief Introduction To Education 5Th Edition Full Chapterjamie.nettles908100% (29)

- Chiral Building Blocks in Asymmetric Synthesis Synthesis and Applications Elzbieta Wojaczynska Full ChapterDocument67 pagesChiral Building Blocks in Asymmetric Synthesis Synthesis and Applications Elzbieta Wojaczynska Full Chapterstephine.wiedenheft739100% (9)

- If We Were Kin Race Identification and Intimate Political Appeals Lisa Beard Full ChapterDocument67 pagesIf We Were Kin Race Identification and Intimate Political Appeals Lisa Beard Full Chaptertyson.vaughan271100% (12)

- Shigleys Mechanical Engineering Design 11Th Ed 11Th Edition Richard Budynas Full Download ChapterDocument51 pagesShigleys Mechanical Engineering Design 11Th Ed 11Th Edition Richard Budynas Full Download Chapterrobert.marriot976100% (8)

- Test Bank For Public Finance and Public Policy 5Th Edition Gruber 1464143331 9781464143335 Full Chapter PDFDocument36 pagesTest Bank For Public Finance and Public Policy 5Th Edition Gruber 1464143331 9781464143335 Full Chapter PDFcraig.gibbons469100% (11)

- Solution Manual For Families and Their Social Worlds 3Rd Edition by Seccombe Isbn 0133936600 9780133936605 Full Chapter PDFDocument36 pagesSolution Manual For Families and Their Social Worlds 3Rd Edition by Seccombe Isbn 0133936600 9780133936605 Full Chapter PDFsasha.voegele1000100% (12)

- Psychopharmacology in British Literature and Culture 1780 1900 1St Ed Edition Natalie Roxburgh All ChapterDocument59 pagesPsychopharmacology in British Literature and Culture 1780 1900 1St Ed Edition Natalie Roxburgh All Chapterrita.strickland541100% (5)

- Microeconomics 3Rd Edition Hubbard Solutions Manual Full Chapter PDFDocument36 pagesMicroeconomics 3Rd Edition Hubbard Solutions Manual Full Chapter PDFcythia.tait735100% (12)

- Street On Torts 15Th Edition Full ChapterDocument41 pagesStreet On Torts 15Th Edition Full Chapterjamie.nettles908100% (26)

- Technology Now Your Companion To Sam Computer Concepts 1St Edition Corinne Hoisington Test Bank Full Chapter PDFDocument30 pagesTechnology Now Your Companion To Sam Computer Concepts 1St Edition Corinne Hoisington Test Bank Full Chapter PDFlaurence.harris245100% (10)

- Financial Accounting Canadian 6th Edition by Libby ISBN Solution ManualDocument130 pagesFinancial Accounting Canadian 6th Edition by Libby ISBN Solution Manualellen100% (31)

- Solution Manual For Financial Accounting Canadian 6Th Edition by Harrison Isbn 0134141091 978013414109 Full Chapter PDFDocument36 pagesSolution Manual For Financial Accounting Canadian 6Th Edition by Harrison Isbn 0134141091 978013414109 Full Chapter PDFcarmen.hall969100% (11)

- Solution Manual For Financial Accounting Canadian Canadian 5Th Edition by Libby Isbn 0071339469 9780071339469 Full Chapter PDFDocument36 pagesSolution Manual For Financial Accounting Canadian Canadian 5Th Edition by Libby Isbn 0071339469 9780071339469 Full Chapter PDFcarmen.hall969100% (11)

- Solution Manual For Financial Accounting Fundamentals 5Th Edition by Wild Isbn 0078025753 9780078025754 Full Chapter PDFDocument36 pagesSolution Manual For Financial Accounting Fundamentals 5Th Edition by Wild Isbn 0078025753 9780078025754 Full Chapter PDFcarmen.hall969100% (11)

- Solution Manual For Financial Accounting Fundamentals 4Th Edition by Wild Isbn 0078025591 9780078025594 Full Chapter PDFDocument36 pagesSolution Manual For Financial Accounting Fundamentals 4Th Edition by Wild Isbn 0078025591 9780078025594 Full Chapter PDFcarmen.hall969100% (12)

- Solution Manual For Financial Accounting Canadian 5Th Edition by Harrison Isbn 0132979276 9780132979276 Full Chapter PDFDocument36 pagesSolution Manual For Financial Accounting Canadian 5Th Edition by Harrison Isbn 0132979276 9780132979276 Full Chapter PDFcarmen.hall969100% (12)

- Solution Manual For Financial Accounting An Introduction To Concepts Methods and Uses 14th Edition by Weil ISBN 1111823456 9781111823450Document36 pagesSolution Manual For Financial Accounting An Introduction To Concepts Methods and Uses 14th Edition by Weil ISBN 1111823456 9781111823450carmen.hall969100% (11)

- Solution Manual For Financial Accounting Canadian 2Nd Edition by Waybright Isbn 0133375536 9780133375534 Full Chapter PDFDocument36 pagesSolution Manual For Financial Accounting Canadian 2Nd Edition by Waybright Isbn 0133375536 9780133375534 Full Chapter PDFcarmen.hall969100% (12)

- Fundamentals of Accounting II, Chapter 4Document71 pagesFundamentals of Accounting II, Chapter 4Mohammed AbdulselamNo ratings yet

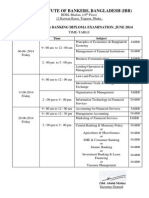

- Banking Diploma, 79thDocument1 pageBanking Diploma, 79thbrikkhoNo ratings yet

- Merc QuamtoDocument34 pagesMerc QuamtoSan Tabugan100% (3)

- Annual Review 2011Document52 pagesAnnual Review 2011Nooreza PeerooNo ratings yet

- 600 019 Advanced Petroleum Economics 600.019 Advanced Petroleum EconomicsDocument46 pages600 019 Advanced Petroleum Economics 600.019 Advanced Petroleum EconomicsRoberto MendozaNo ratings yet

- Liquidation AccountingDocument5 pagesLiquidation AccountingTomy Mathew100% (1)

- RBS-Rising Cuspy Coupon PrepaymentsDocument13 pagesRBS-Rising Cuspy Coupon PrepaymentsYiling ZhangNo ratings yet

- SbiDocument12 pagesSbiritesh ranjan singhNo ratings yet

- Telly PDFDocument19 pagesTelly PDFNaushad Ahmad60% (15)

- Great LearningDocument32 pagesGreat LearningQKNo ratings yet

- Gibson Chapter 11 Expanded Analysis (Editted)Document35 pagesGibson Chapter 11 Expanded Analysis (Editted)Ali UmerNo ratings yet

- Analysis of Section 139 A IT Act 1961Document13 pagesAnalysis of Section 139 A IT Act 1961padam jainNo ratings yet

- Auto-Sweep Facility in Your Savings Bank AccountDocument14 pagesAuto-Sweep Facility in Your Savings Bank Accountpradeepverma84No ratings yet

- Senior Deal Officer-JDDocument2 pagesSenior Deal Officer-JDgitarista007No ratings yet

- Final Exam Sample Questions Attempt Review 1Document9 pagesFinal Exam Sample Questions Attempt Review 1leieparanoicoNo ratings yet

- Project Report On Islamic BankingDocument26 pagesProject Report On Islamic BankingMichael EdwardsNo ratings yet

- Mcqs For Chapter 12: Regulation and Supervision of Islamic Financial Institutions (Ifis)Document4 pagesMcqs For Chapter 12: Regulation and Supervision of Islamic Financial Institutions (Ifis)alaaNo ratings yet

- Ch. 2 - Problems - 01+02Document2 pagesCh. 2 - Problems - 01+02NazmulAhsanNo ratings yet

- TPWGMaking Marxist Use of KeynesOCT28Document22 pagesTPWGMaking Marxist Use of KeynesOCT28Mac YoungNo ratings yet

- Problem Set 1 Simple InterestDocument2 pagesProblem Set 1 Simple InterestJeda NjobuNo ratings yet

- Nature of AccountingDocument2 pagesNature of AccountingRivera, Erica HazelNo ratings yet

- FSA Chapter 8 NotesDocument9 pagesFSA Chapter 8 NotesNadia ZahraNo ratings yet

- Midterm - ReviewerDocument11 pagesMidterm - Reviewerangel ciiiNo ratings yet

- MFSI-Unit IDocument35 pagesMFSI-Unit ISanthiya LakshmiNo ratings yet

- Chamarajpet Branch, No. 270, Albert Victor Road, 1 Main Road, Chamarajpet, Bangalore, Karnataka 560018 PH: 080-26700181Document5 pagesChamarajpet Branch, No. 270, Albert Victor Road, 1 Main Road, Chamarajpet, Bangalore, Karnataka 560018 PH: 080-26700181canilreddyNo ratings yet

- Fs Analysis MC ProblemsDocument7 pagesFs Analysis MC ProblemsarkishaNo ratings yet

- Islamic Finance in SrilankaDocument6 pagesIslamic Finance in SrilankaHameed AzharNo ratings yet

- Isbm University: "A Study On Non-Performing Assets at The Bangalore City Co-Operative Bank LTD."Document7 pagesIsbm University: "A Study On Non-Performing Assets at The Bangalore City Co-Operative Bank LTD."Dance on floorNo ratings yet

- BCom Banking and InsuranceDocument106 pagesBCom Banking and InsuranceUtsav SinhaNo ratings yet

Download as pdf or txt

You might also like

- Teacher Leadership For Social Justice Building A Curriculum For Liberation Revised First Ed Edition Full ChapterDocument41 pagesTeacher Leadership For Social Justice Building A Curriculum For Liberation Revised First Ed Edition Full Chapterjamie.nettles908100% (29)

- Essentials of Human Diseases and Conditions 6th Edition Frazier Test Bank Full Chapter PDFDocument32 pagesEssentials of Human Diseases and Conditions 6th Edition Frazier Test Bank Full Chapter PDFEugeneMurraykspo100% (14)

- CHAPTER 10 - AnswerDocument5 pagesCHAPTER 10 - Answernash100% (2)

- Solution Manual For Financial Accounting Canadian Canadian 5Th Edition by Libby Isbn 0071339469 9780071339469 Full Chapter PDFDocument36 pagesSolution Manual For Financial Accounting Canadian Canadian 5Th Edition by Libby Isbn 0071339469 9780071339469 Full Chapter PDFcarmen.hall969100% (11)

- Solution Manual For Financial Accounting Canadian 6Th Edition by Harrison Isbn 0134141091 978013414109 Full Chapter PDFDocument36 pagesSolution Manual For Financial Accounting Canadian 6Th Edition by Harrison Isbn 0134141091 978013414109 Full Chapter PDFcarmen.hall969100% (11)

- Solution Manual For Financial Accounting Canadian 5Th Edition by Harrison Isbn 0132979276 9780132979276 Full Chapter PDFDocument36 pagesSolution Manual For Financial Accounting Canadian 5Th Edition by Harrison Isbn 0132979276 9780132979276 Full Chapter PDFcarmen.hall969100% (12)

- Solution Manual For Financial Accounting Fundamentals 4Th Edition by Wild Isbn 0078025591 9780078025594 Full Chapter PDFDocument36 pagesSolution Manual For Financial Accounting Fundamentals 4Th Edition by Wild Isbn 0078025591 9780078025594 Full Chapter PDFcarmen.hall969100% (12)

- Solution Manual For Financial Accounting Canadian 2Nd Edition by Waybright Isbn 0133375536 9780133375534 Full Chapter PDFDocument36 pagesSolution Manual For Financial Accounting Canadian 2Nd Edition by Waybright Isbn 0133375536 9780133375534 Full Chapter PDFcarmen.hall969100% (12)

- Enhanced Computer Concepts and Microsoft Office 2013 Illustrated 1St Edition Parsons Test Bank Full Chapter PDFDocument36 pagesEnhanced Computer Concepts and Microsoft Office 2013 Illustrated 1St Edition Parsons Test Bank Full Chapter PDFrichard.eis609100% (10)

- Enhanced Discovering Computers and Microsoft Office 2013 A Combined Fundamental Approach 1St Edition Vermaat Test Bank Full Chapter PDFDocument36 pagesEnhanced Discovering Computers and Microsoft Office 2013 A Combined Fundamental Approach 1St Edition Vermaat Test Bank Full Chapter PDFrichard.eis609100% (10)

- Solution Manual For Financial Accounting An Introduction To Concepts Methods and Uses 14th Edition by Weil ISBN 1111823456 9781111823450Document36 pagesSolution Manual For Financial Accounting An Introduction To Concepts Methods and Uses 14th Edition by Weil ISBN 1111823456 9781111823450carmen.hall969100% (11)

- Solution Manual For Financial Accounting Fundamentals 5Th Edition by Wild Isbn 0078025753 9780078025754 Full Chapter PDFDocument36 pagesSolution Manual For Financial Accounting Fundamentals 5Th Edition by Wild Isbn 0078025753 9780078025754 Full Chapter PDFcarmen.hall969100% (11)

- Enhanced Computer Concepts and Microsoft Office 2013 Illustrated 1St Edition Parsons Solutions Manual Full Chapter PDFDocument36 pagesEnhanced Computer Concepts and Microsoft Office 2013 Illustrated 1St Edition Parsons Solutions Manual Full Chapter PDFrichard.eis609100% (11)

- Engineering Problem Solving With C++ 4Th Edition Etter Test Bank Full Chapter PDFDocument26 pagesEngineering Problem Solving With C++ 4Th Edition Etter Test Bank Full Chapter PDFrichard.eis609100% (12)

- Engineering Problem Solving With C++ 4Th Edition Etter Solutions Manual Full Chapter PDFDocument36 pagesEngineering Problem Solving With C++ 4Th Edition Etter Solutions Manual Full Chapter PDFrichard.eis609100% (11)

- Engineering Mechanics Statics and Dynamics 2Nd Edition Plesha Solutions Manual Full Chapter PDFDocument46 pagesEngineering Mechanics Statics and Dynamics 2Nd Edition Plesha Solutions Manual Full Chapter PDFrichard.eis609100% (10)

- Engineering Mechanics Statics 4Th Edition Pytel Solutions Manual Full Chapter PDFDocument36 pagesEngineering Mechanics Statics 4Th Edition Pytel Solutions Manual Full Chapter PDFrichard.eis609100% (10)

- Test Bank For Psychology 1St Edition Marin Hock 0205920012 9780205920013 Full Chapter PDFDocument36 pagesTest Bank For Psychology 1St Edition Marin Hock 0205920012 9780205920013 Full Chapter PDFsamantha.garcia508100% (9)

- Creating MacrosDocument36 pagesCreating Macroschristine.jackson281100% (10)

- Engineering Mechanics Dynamics 4Th Edition Pytel Solutions Manual Full Chapter PDFDocument27 pagesEngineering Mechanics Dynamics 4Th Edition Pytel Solutions Manual Full Chapter PDFrichard.eis609100% (12)

- Cornerstones of Financial Accounting Canadian 2Nd Edition Rich Test Bank Full Chapter PDFDocument36 pagesCornerstones of Financial Accounting Canadian 2Nd Edition Rich Test Bank Full Chapter PDFrenee.crawford887100% (12)

- Attacking The Elites What Critics Get Wrong and Right About Americas Leading Universities Derek Bok Full ChapterDocument47 pagesAttacking The Elites What Critics Get Wrong and Right About Americas Leading Universities Derek Bok Full Chaptermario.becker252100% (8)

- Cornerstones of Managerial Accounting 6Th Edition Mowen Solutions Manual Full Chapter PDFDocument36 pagesCornerstones of Managerial Accounting 6Th Edition Mowen Solutions Manual Full Chapter PDFrenee.crawford887100% (10)

- Marketing The Core 5Th Edition Kerin Test Bank Full Chapter PDFDocument36 pagesMarketing The Core 5Th Edition Kerin Test Bank Full Chapter PDFfay.rowden768100% (12)

- Test Bank For Criminal Procedure 3Rd Edition by Lippman Isbn 1506306497 9781506306490 Full Chapter PDFDocument31 pagesTest Bank For Criminal Procedure 3Rd Edition by Lippman Isbn 1506306497 9781506306490 Full Chapter PDFdouglas.valadez414100% (11)

- Test Bank For Criminal Law 1St Edition by Russell Brown Davis Isbn 1412977894 9781412977890 Full Chapter PDFDocument31 pagesTest Bank For Criminal Law 1St Edition by Russell Brown Davis Isbn 1412977894 9781412977890 Full Chapter PDFdouglas.valadez414100% (11)

- Thermodynamics An Engineering Approach 8Th Edition Cengel Test Bank Full Chapter PDFDocument32 pagesThermodynamics An Engineering Approach 8Th Edition Cengel Test Bank Full Chapter PDFgeraldine.wells536100% (11)

- Building and Using QueriesDocument36 pagesBuilding and Using Querieschristine.jackson281100% (11)

- Cornerstones of Managerial Accounting 5Th Edition Mowen Solutions Manual Full Chapter PDFDocument36 pagesCornerstones of Managerial Accounting 5Th Edition Mowen Solutions Manual Full Chapter PDFrenee.crawford887100% (9)

- Microeconomics 20Th Edition Mcconnell Solutions Manual Full Chapter PDFDocument30 pagesMicroeconomics 20Th Edition Mcconnell Solutions Manual Full Chapter PDFcythia.tait735100% (12)

- Test Bank For Psychology Perspectives and Connections 3Rd Edition Feist Rosenberg 0077861876 978007786187 Full Chapter PDFDocument46 pagesTest Bank For Psychology Perspectives and Connections 3Rd Edition Feist Rosenberg 0077861876 978007786187 Full Chapter PDFcraig.gibbons469100% (11)

- Microeconomics 2Nd Edition Goolsbee Test Bank Full Chapter PDFDocument36 pagesMicroeconomics 2Nd Edition Goolsbee Test Bank Full Chapter PDFcythia.tait735100% (12)

- Populism and Civil Society The Challenge To Constitutional Democracy Andrew Arato 2 All ChapterDocument67 pagesPopulism and Civil Society The Challenge To Constitutional Democracy Andrew Arato 2 All Chapterdenise.murry935100% (10)

- Test Bank For Business Communication Essentials 7Th Edition by Bovee Full Chapter PDFDocument36 pagesTest Bank For Business Communication Essentials 7Th Edition by Bovee Full Chapter PDFlaurence.harris245100% (11)

- Test Bank For Modern Competitive Strategy 4Th Edition Walker Madsen 1259181200 9781259181207 Full Chapter PDFDocument33 pagesTest Bank For Modern Competitive Strategy 4Th Edition Walker Madsen 1259181200 9781259181207 Full Chapter PDFkenneth.miller246100% (11)

- Feelings Transformed Philosophical Theories of The Emotions 1270 1670 Dominik Perler Full ChapterDocument67 pagesFeelings Transformed Philosophical Theories of The Emotions 1270 1670 Dominik Perler Full Chapteralfred.jessie484100% (20)

- Fundamentals of Data and Signals: Learning ObjectivesDocument32 pagesFundamentals of Data and Signals: Learning Objectivesdeborah.porter960100% (11)

- Essential University Physics 3Rd Edition Richard Wolfson Test Bank Full Chapter PDFDocument32 pagesEssential University Physics 3Rd Edition Richard Wolfson Test Bank Full Chapter PDFteresa.mccoin592100% (12)

- Test Bank For Absolute C 5Th Edition Savitch Mock 013283071X 9780132830713 Full Chapter PDFDocument31 pagesTest Bank For Absolute C 5Th Edition Savitch Mock 013283071X 9780132830713 Full Chapter PDFmiranda.barnhart699100% (12)

- 500 Act Science Questions To Know by Test Day 3Rd Edition Inc Anaxos Full ChapterDocument77 pages500 Act Science Questions To Know by Test Day 3Rd Edition Inc Anaxos Full Chapternicholas.leno709100% (8)

- Macroeconomics Canadian 8Th Edition Sayre Test Bank Full Chapter PDFDocument36 pagesMacroeconomics Canadian 8Th Edition Sayre Test Bank Full Chapter PDFkevin.reider416100% (11)

- Management Canadian 11Th Edition Robbins Test Bank Full Chapter PDFDocument36 pagesManagement Canadian 11Th Edition Robbins Test Bank Full Chapter PDFalejandro.perdue730100% (12)

- Cornerstones of Managerial Accounting Canadian 2Nd Edition Mowen Solutions Manual Full Chapter PDFDocument36 pagesCornerstones of Managerial Accounting Canadian 2Nd Edition Mowen Solutions Manual Full Chapter PDFrenee.crawford887100% (7)

- Solution Manual For Hydrologic Analysis and Design 4Th Edition Mccuen 0134313127 978013431312 Full Chapter PDFDocument36 pagesSolution Manual For Hydrologic Analysis and Design 4Th Edition Mccuen 0134313127 978013431312 Full Chapter PDFchristine.jackson281100% (11)

- Microeconomics 20Th Edition Mcconnell Test Bank Full Chapter PDFDocument36 pagesMicroeconomics 20Th Edition Mcconnell Test Bank Full Chapter PDFcythia.tait735100% (10)

- Test Bank For Medical Terminology For Health Professions 7Th Edition Ehrlich Schroeder 1111543275 9781111543273 Full Chapter PDFDocument27 pagesTest Bank For Medical Terminology For Health Professions 7Th Edition Ehrlich Schroeder 1111543275 9781111543273 Full Chapter PDFkacey.perreault490100% (11)

- Essential Statistics 1St Edition Navidi Solutions Manual Full Chapter PDFDocument36 pagesEssential Statistics 1St Edition Navidi Solutions Manual Full Chapter PDFteresa.mccoin592100% (11)

- Test Bank For Abnormal Psychology Clinical Perspectives On Psychological Disorders 7th Edition Whitbourne Halgin 0078035279 9780078035272Document36 pagesTest Bank For Abnormal Psychology Clinical Perspectives On Psychological Disorders 7th Edition Whitbourne Halgin 0078035279 9780078035272miranda.barnhart699100% (11)

- Test Bank For Methods in Behavioral Research 12Th Edition Cozby Bates 0077861892 9780077861896 Full Chapter PDFDocument36 pagesTest Bank For Methods in Behavioral Research 12Th Edition Cozby Bates 0077861892 9780077861896 Full Chapter PDFpauline.ganley829100% (12)

- Corrosion Policy Decision Making Science Engineering Management and Economy Reza Javaherdashti Full ChapterDocument61 pagesCorrosion Policy Decision Making Science Engineering Management and Economy Reza Javaherdashti Full Chaptermartha.conrad799100% (10)

- Teachers Schools and Society A Brief Introduction To Education 5Th Edition Full ChapterDocument41 pagesTeachers Schools and Society A Brief Introduction To Education 5Th Edition Full Chapterjamie.nettles908100% (29)

- Chiral Building Blocks in Asymmetric Synthesis Synthesis and Applications Elzbieta Wojaczynska Full ChapterDocument67 pagesChiral Building Blocks in Asymmetric Synthesis Synthesis and Applications Elzbieta Wojaczynska Full Chapterstephine.wiedenheft739100% (9)

- If We Were Kin Race Identification and Intimate Political Appeals Lisa Beard Full ChapterDocument67 pagesIf We Were Kin Race Identification and Intimate Political Appeals Lisa Beard Full Chaptertyson.vaughan271100% (12)

- Shigleys Mechanical Engineering Design 11Th Ed 11Th Edition Richard Budynas Full Download ChapterDocument51 pagesShigleys Mechanical Engineering Design 11Th Ed 11Th Edition Richard Budynas Full Download Chapterrobert.marriot976100% (8)

- Test Bank For Public Finance and Public Policy 5Th Edition Gruber 1464143331 9781464143335 Full Chapter PDFDocument36 pagesTest Bank For Public Finance and Public Policy 5Th Edition Gruber 1464143331 9781464143335 Full Chapter PDFcraig.gibbons469100% (11)

- Solution Manual For Families and Their Social Worlds 3Rd Edition by Seccombe Isbn 0133936600 9780133936605 Full Chapter PDFDocument36 pagesSolution Manual For Families and Their Social Worlds 3Rd Edition by Seccombe Isbn 0133936600 9780133936605 Full Chapter PDFsasha.voegele1000100% (12)

- Psychopharmacology in British Literature and Culture 1780 1900 1St Ed Edition Natalie Roxburgh All ChapterDocument59 pagesPsychopharmacology in British Literature and Culture 1780 1900 1St Ed Edition Natalie Roxburgh All Chapterrita.strickland541100% (5)

- Microeconomics 3Rd Edition Hubbard Solutions Manual Full Chapter PDFDocument36 pagesMicroeconomics 3Rd Edition Hubbard Solutions Manual Full Chapter PDFcythia.tait735100% (12)

- Street On Torts 15Th Edition Full ChapterDocument41 pagesStreet On Torts 15Th Edition Full Chapterjamie.nettles908100% (26)

- Technology Now Your Companion To Sam Computer Concepts 1St Edition Corinne Hoisington Test Bank Full Chapter PDFDocument30 pagesTechnology Now Your Companion To Sam Computer Concepts 1St Edition Corinne Hoisington Test Bank Full Chapter PDFlaurence.harris245100% (10)

- Financial Accounting Canadian 6th Edition by Libby ISBN Solution ManualDocument130 pagesFinancial Accounting Canadian 6th Edition by Libby ISBN Solution Manualellen100% (31)

- Solution Manual For Financial Accounting Canadian 6Th Edition by Harrison Isbn 0134141091 978013414109 Full Chapter PDFDocument36 pagesSolution Manual For Financial Accounting Canadian 6Th Edition by Harrison Isbn 0134141091 978013414109 Full Chapter PDFcarmen.hall969100% (11)

- Solution Manual For Financial Accounting Canadian Canadian 5Th Edition by Libby Isbn 0071339469 9780071339469 Full Chapter PDFDocument36 pagesSolution Manual For Financial Accounting Canadian Canadian 5Th Edition by Libby Isbn 0071339469 9780071339469 Full Chapter PDFcarmen.hall969100% (11)

- Solution Manual For Financial Accounting Fundamentals 5Th Edition by Wild Isbn 0078025753 9780078025754 Full Chapter PDFDocument36 pagesSolution Manual For Financial Accounting Fundamentals 5Th Edition by Wild Isbn 0078025753 9780078025754 Full Chapter PDFcarmen.hall969100% (11)

- Solution Manual For Financial Accounting Fundamentals 4Th Edition by Wild Isbn 0078025591 9780078025594 Full Chapter PDFDocument36 pagesSolution Manual For Financial Accounting Fundamentals 4Th Edition by Wild Isbn 0078025591 9780078025594 Full Chapter PDFcarmen.hall969100% (12)

- Solution Manual For Financial Accounting Canadian 5Th Edition by Harrison Isbn 0132979276 9780132979276 Full Chapter PDFDocument36 pagesSolution Manual For Financial Accounting Canadian 5Th Edition by Harrison Isbn 0132979276 9780132979276 Full Chapter PDFcarmen.hall969100% (12)

- Solution Manual For Financial Accounting An Introduction To Concepts Methods and Uses 14th Edition by Weil ISBN 1111823456 9781111823450Document36 pagesSolution Manual For Financial Accounting An Introduction To Concepts Methods and Uses 14th Edition by Weil ISBN 1111823456 9781111823450carmen.hall969100% (11)

- Solution Manual For Financial Accounting Canadian 2Nd Edition by Waybright Isbn 0133375536 9780133375534 Full Chapter PDFDocument36 pagesSolution Manual For Financial Accounting Canadian 2Nd Edition by Waybright Isbn 0133375536 9780133375534 Full Chapter PDFcarmen.hall969100% (12)

- Fundamentals of Accounting II, Chapter 4Document71 pagesFundamentals of Accounting II, Chapter 4Mohammed AbdulselamNo ratings yet

- Banking Diploma, 79thDocument1 pageBanking Diploma, 79thbrikkhoNo ratings yet

- Merc QuamtoDocument34 pagesMerc QuamtoSan Tabugan100% (3)

- Annual Review 2011Document52 pagesAnnual Review 2011Nooreza PeerooNo ratings yet

- 600 019 Advanced Petroleum Economics 600.019 Advanced Petroleum EconomicsDocument46 pages600 019 Advanced Petroleum Economics 600.019 Advanced Petroleum EconomicsRoberto MendozaNo ratings yet

- Liquidation AccountingDocument5 pagesLiquidation AccountingTomy Mathew100% (1)

- RBS-Rising Cuspy Coupon PrepaymentsDocument13 pagesRBS-Rising Cuspy Coupon PrepaymentsYiling ZhangNo ratings yet

- SbiDocument12 pagesSbiritesh ranjan singhNo ratings yet

- Telly PDFDocument19 pagesTelly PDFNaushad Ahmad60% (15)

- Great LearningDocument32 pagesGreat LearningQKNo ratings yet

- Gibson Chapter 11 Expanded Analysis (Editted)Document35 pagesGibson Chapter 11 Expanded Analysis (Editted)Ali UmerNo ratings yet

- Analysis of Section 139 A IT Act 1961Document13 pagesAnalysis of Section 139 A IT Act 1961padam jainNo ratings yet

- Auto-Sweep Facility in Your Savings Bank AccountDocument14 pagesAuto-Sweep Facility in Your Savings Bank Accountpradeepverma84No ratings yet

- Senior Deal Officer-JDDocument2 pagesSenior Deal Officer-JDgitarista007No ratings yet

- Final Exam Sample Questions Attempt Review 1Document9 pagesFinal Exam Sample Questions Attempt Review 1leieparanoicoNo ratings yet

- Project Report On Islamic BankingDocument26 pagesProject Report On Islamic BankingMichael EdwardsNo ratings yet

- Mcqs For Chapter 12: Regulation and Supervision of Islamic Financial Institutions (Ifis)Document4 pagesMcqs For Chapter 12: Regulation and Supervision of Islamic Financial Institutions (Ifis)alaaNo ratings yet

- Ch. 2 - Problems - 01+02Document2 pagesCh. 2 - Problems - 01+02NazmulAhsanNo ratings yet

- TPWGMaking Marxist Use of KeynesOCT28Document22 pagesTPWGMaking Marxist Use of KeynesOCT28Mac YoungNo ratings yet

- Problem Set 1 Simple InterestDocument2 pagesProblem Set 1 Simple InterestJeda NjobuNo ratings yet

- Nature of AccountingDocument2 pagesNature of AccountingRivera, Erica HazelNo ratings yet

- FSA Chapter 8 NotesDocument9 pagesFSA Chapter 8 NotesNadia ZahraNo ratings yet

- Midterm - ReviewerDocument11 pagesMidterm - Reviewerangel ciiiNo ratings yet

- MFSI-Unit IDocument35 pagesMFSI-Unit ISanthiya LakshmiNo ratings yet

- Chamarajpet Branch, No. 270, Albert Victor Road, 1 Main Road, Chamarajpet, Bangalore, Karnataka 560018 PH: 080-26700181Document5 pagesChamarajpet Branch, No. 270, Albert Victor Road, 1 Main Road, Chamarajpet, Bangalore, Karnataka 560018 PH: 080-26700181canilreddyNo ratings yet

- Fs Analysis MC ProblemsDocument7 pagesFs Analysis MC ProblemsarkishaNo ratings yet

- Islamic Finance in SrilankaDocument6 pagesIslamic Finance in SrilankaHameed AzharNo ratings yet

- Isbm University: "A Study On Non-Performing Assets at The Bangalore City Co-Operative Bank LTD."Document7 pagesIsbm University: "A Study On Non-Performing Assets at The Bangalore City Co-Operative Bank LTD."Dance on floorNo ratings yet

- BCom Banking and InsuranceDocument106 pagesBCom Banking and InsuranceUtsav SinhaNo ratings yet