Download as pdf or txt

You might also like

- Budget Exercises - Part II (Model Answers)Document7 pagesBudget Exercises - Part II (Model Answers)Menna AssemNo ratings yet

- Financial Management Gitman Chapter 15Document3 pagesFinancial Management Gitman Chapter 15Samuel Zefanya50% (2)

- PPT2 AnsDocument5 pagesPPT2 Anskristelle0marisseNo ratings yet

- Tugas 2 Akuntansi ManajemenDocument3 pagesTugas 2 Akuntansi ManajemenSherlin KhuNo ratings yet

- Nama: Nabila Indri Yani No. BP: 2010931037 Tugas 1: Analisis Dan Estimasi BiayaDocument4 pagesNama: Nabila Indri Yani No. BP: 2010931037 Tugas 1: Analisis Dan Estimasi BiayaInnabilaNo ratings yet

- Current Year ($) Forecasted For Next Year ($) Book Value of Debt 50 50 Market Value of Debt 62Document9 pagesCurrent Year ($) Forecasted For Next Year ($) Book Value of Debt 50 50 Market Value of Debt 62Joel Christian MascariñaNo ratings yet

- 2010 05 08 - 053020 - Case5 18Document4 pages2010 05 08 - 053020 - Case5 18ambermuNo ratings yet

- Contoh Business PlanDocument10 pagesContoh Business PlanRebbyNoviarNo ratings yet

- STRAMA Dont Like You She Likes Evreryone.. 1Document128 pagesSTRAMA Dont Like You She Likes Evreryone.. 1Jasper MonteroNo ratings yet

- Individual Assignment Case 2 - Financial Report and Control - DILEMBA 1 Mohammad Alfian Syah Siregar - 29322150Document3 pagesIndividual Assignment Case 2 - Financial Report and Control - DILEMBA 1 Mohammad Alfian Syah Siregar - 29322150iancroottNo ratings yet

- Case Chapter 02Document2 pagesCase Chapter 02Pandit PurnajuaraNo ratings yet

- Chapter 10 How Costs Behave Practice QuestionsDocument7 pagesChapter 10 How Costs Behave Practice QuestionsNCTNo ratings yet

- Cost of Goods Manufactured and Mixed Costs in A Pricing DecisionDocument7 pagesCost of Goods Manufactured and Mixed Costs in A Pricing DecisionDavid A. SanchezNo ratings yet

- Ejercicios PearsonDocument25 pagesEjercicios PearsonLINA PAOLA JIMENEZ RODRIGUEZNo ratings yet

- Cost Behavior: Analysis and Use: Exercise 5-3 (20 Minutes)Document14 pagesCost Behavior: Analysis and Use: Exercise 5-3 (20 Minutes)RiskaNo ratings yet

- 17 - Ni Putu Cherline Berliana - Problem 11.1 & 11.8Document6 pages17 - Ni Putu Cherline Berliana - Problem 11.1 & 11.8putu cherline21No ratings yet

- Hilton Macc ch9 Solution PDFDocument8 pagesHilton Macc ch9 Solution PDFVenghat BhalajiNo ratings yet

- CH# 2 Practice QuestionsDocument3 pagesCH# 2 Practice QuestionsKainat ZulfiqarNo ratings yet

- 1 FiverrNightclub Business Plan PDFDocument10 pages1 FiverrNightclub Business Plan PDFngueadoumNo ratings yet

- Chapter 3Document6 pagesChapter 3Pauline Keith Paz ManuelNo ratings yet

- Profit Analysis Worksheet: ProductionDocument18 pagesProfit Analysis Worksheet: ProductionhariveerNo ratings yet

- Case StudiesDocument6 pagesCase StudiesFrancesnova B. Dela PeñaNo ratings yet

- Assignment - Variable Ab (Q)Document2 pagesAssignment - Variable Ab (Q)Shiela Mae Pon AnNo ratings yet

- Problem 9-14 (45 Minutes) : Month April May June QuarterDocument8 pagesProblem 9-14 (45 Minutes) : Month April May June QuarterRowbby GwynNo ratings yet

- Medieval Case SolutionDocument7 pagesMedieval Case SolutionTarry BerryNo ratings yet

- ANSWER - Cost Accounting Session 2Document8 pagesANSWER - Cost Accounting Session 2Vincenttio le CloudNo ratings yet

- (Jennifer / 1901469555 / LA53) : GSLC Assignment Profit PlanningDocument5 pages(Jennifer / 1901469555 / LA53) : GSLC Assignment Profit PlanningJennifer GunawanNo ratings yet

- ENTREP Income AnalysisDocument5 pagesENTREP Income AnalysisMary Rose Bragais OgayonNo ratings yet

- Month Customer Numbers Average Spend (Food) Average Spend (Beverage)Document8 pagesMonth Customer Numbers Average Spend (Food) Average Spend (Beverage)milan shresthaNo ratings yet

- 2015 ACT Regional #1Document9 pages2015 ACT Regional #1shuxian.ho0401No ratings yet

- Capital Equipment List: Item Per Unit Quantity TotalDocument11 pagesCapital Equipment List: Item Per Unit Quantity TotalMichelle ClarkeNo ratings yet

- Proposal DISUSUN OLEH: KelompokDocument6 pagesProposal DISUSUN OLEH: KelompokSefa PrasetiaNo ratings yet

- Reviewer For Midterm XFINMAR A224and A225Document5 pagesReviewer For Midterm XFINMAR A224and A225ralph11240308No ratings yet

- Chapter V GerylleDocument15 pagesChapter V GerylleBernadeth CiprianoNo ratings yet

- Chen-Chen'S Lechon House: LocationDocument12 pagesChen-Chen'S Lechon House: LocationMardjon SalmorinNo ratings yet

- ACT 513 Summer 2021Document2 pagesACT 513 Summer 2021Md SobujNo ratings yet

- Problem 9-15 (60 Minutes) : © The Mcgraw-Hill Companies, Inc., 2008. All Rights Reserved. Solutions Manual, Chapter 9 1Document14 pagesProblem 9-15 (60 Minutes) : © The Mcgraw-Hill Companies, Inc., 2008. All Rights Reserved. Solutions Manual, Chapter 9 1Tanvir AhmedNo ratings yet

- Tutorial - BudgetsDocument3 pagesTutorial - BudgetsShiTheng Love UNo ratings yet

- Group4 Cityu8b Assignment Corporate FinanceDocument16 pagesGroup4 Cityu8b Assignment Corporate Financeđức nguyên anhNo ratings yet

- Sol ch03Document12 pagesSol ch03Ahmed MousaNo ratings yet

- Brief Exercise 7-1 (10 Minutes)Document45 pagesBrief Exercise 7-1 (10 Minutes)Ashish BhallaNo ratings yet

- (USD $ Millions) : Operating Cash FlowDocument5 pages(USD $ Millions) : Operating Cash Flowsunit dasNo ratings yet

- BAFINMAX Learning Activity 1 Finals - With Answers - StudentsDocument5 pagesBAFINMAX Learning Activity 1 Finals - With Answers - Studentsfaye pantiNo ratings yet

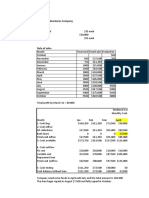

- Medieval Adventures CompanyDocument4 pagesMedieval Adventures CompanyFadhila Nurfida HanifNo ratings yet

- Business Math Accounting Cohort 11-30-23Document23 pagesBusiness Math Accounting Cohort 11-30-23desouzas.ldsNo ratings yet

- Treasury Management Vs Cash Management Answer To Warm Up ExercisesDocument8 pagesTreasury Management Vs Cash Management Answer To Warm Up Exercisesephraim0% (1)

- Healthy Bread DelightDocument11 pagesHealthy Bread DelightSetty HakeemaNo ratings yet

- Book1 (Revised)Document55 pagesBook1 (Revised)Stanly AguilarNo ratings yet

- Revenue ProjectionsDocument1 pageRevenue ProjectionsVIRIMAI SIGNINo ratings yet

- Cost Accounting IANDocument10 pagesCost Accounting IANchris ian Lestino100% (2)

- Chapter - V OriginalDocument15 pagesChapter - V OriginalBernadeth CiprianoNo ratings yet

- Acc 325 Ch. 8 AnswersDocument10 pagesAcc 325 Ch. 8 AnswersMohammad WaleedNo ratings yet

- M11 CHP 09 1 Flex Bud Variances 2011 0524Document47 pagesM11 CHP 09 1 Flex Bud Variances 2011 0524tobeh ibrahimNo ratings yet

- Project CalculationDocument16 pagesProject Calculationf2022383072No ratings yet

- Modelo Financiero GA2 WorkDocument5 pagesModelo Financiero GA2 Workfc10.garcia94No ratings yet

- Budgetassignment 4Document8 pagesBudgetassignment 4api-332895181No ratings yet

- Business Plan & Cash Budget For Dawat IndiaDocument6 pagesBusiness Plan & Cash Budget For Dawat Indiagen mailNo ratings yet

- BACOSTMX Module 2 Learning Activity StudentsDocument8 pagesBACOSTMX Module 2 Learning Activity StudentsRodolfo Jr. LasquiteNo ratings yet

- CVP Analysis QA AllDocument63 pagesCVP Analysis QA Allg8kd6r8np2No ratings yet

- Stamp Duty VicDocument3 pagesStamp Duty VicadnansertNo ratings yet

- Individual Assignment Case Chapter 4 - Aisyah Nuralam 29123362Document3 pagesIndividual Assignment Case Chapter 4 - Aisyah Nuralam 29123362Aisyah NuralamNo ratings yet

- Essay AnalysisDocument5 pagesEssay AnalysisAisyah NuralamNo ratings yet

- Individual Assignment 4A - Aisyah Nuralam 29123362Document4 pagesIndividual Assignment 4A - Aisyah Nuralam 29123362Aisyah NuralamNo ratings yet

- Aisyah Nuralam - Resume Recruitment of A StarDocument2 pagesAisyah Nuralam - Resume Recruitment of A StarAisyah NuralamNo ratings yet

- Individual Assignment Case Chapter 3 - Aisyah Nuralam 29123362Document3 pagesIndividual Assignment Case Chapter 3 - Aisyah Nuralam 29123362Aisyah NuralamNo ratings yet

- Jose Antonio MorenoDocument1 pageJose Antonio MorenoAisyah NuralamNo ratings yet

- Individual Assignment 2B - Aisyah Nuralam 29123362Document5 pagesIndividual Assignment 2B - Aisyah Nuralam 29123362Aisyah NuralamNo ratings yet

- Aisyah Nuralam - Resume Case StudyDocument1 pageAisyah Nuralam - Resume Case StudyAisyah NuralamNo ratings yet

- Individual Assignment 1A - Aisyah Nuralam 29123362Document4 pagesIndividual Assignment 1A - Aisyah Nuralam 29123362Aisyah NuralamNo ratings yet

- Individual Assignment 2A - Aisyah Nuralam 29123362Document4 pagesIndividual Assignment 2A - Aisyah Nuralam 29123362Aisyah NuralamNo ratings yet

- 9abbcdifferential Threshold & Absolute ThresholdDocument9 pages9abbcdifferential Threshold & Absolute Thresholdvipin jaiswalNo ratings yet

- Chapter 6 Factor Market and Income DistributionDocument36 pagesChapter 6 Factor Market and Income DistributionJamel C. MasagcaNo ratings yet

- Sibanye Gold - BNP Cadiz Initiating ReportDocument40 pagesSibanye Gold - BNP Cadiz Initiating ReportGuy DviriNo ratings yet

- Quotation Format For SteelDocument1 pageQuotation Format For SteelAnkur SasmalNo ratings yet

- Business Model CanvasDocument2 pagesBusiness Model CanvasMuhamad Arif RohmanNo ratings yet

- Ofcom Benchmarking 2013Document116 pagesOfcom Benchmarking 2013Ad AcrNo ratings yet

- SSRN Id728545Document37 pagesSSRN Id728545Santiago Martín DiazNo ratings yet

- Mba-Cm Me Lecture 1Document17 pagesMba-Cm Me Lecture 1api-3712367No ratings yet

- Bab 18 Standard Costing PDFDocument8 pagesBab 18 Standard Costing PDFSandi SetiawanNo ratings yet

- THE SOLAR ENERGÍA IN HONDURAS Articulo PDFDocument8 pagesTHE SOLAR ENERGÍA IN HONDURAS Articulo PDFRamón Edgardo Sarmiento MatuteNo ratings yet

- Reliance and Future GroupDocument6 pagesReliance and Future GroupManan100% (1)

- s13 14Document29 pagess13 14R GNo ratings yet

- Tutorial 5 - Derivative of Multivariable FunctionsDocument2 pagesTutorial 5 - Derivative of Multivariable FunctionsИбрагим Ибрагимов0% (1)

- Annual Report 2009Document108 pagesAnnual Report 2009Hsin-Ting WangNo ratings yet

- Multiple Choice Current AffairsDocument3 pagesMultiple Choice Current AffairsHoward R. MoirangchaNo ratings yet

- Exercise Pricing HotelDocument1 pageExercise Pricing Hotelfrancesco bellantoneNo ratings yet

- Finance Finals ExamDocument4 pagesFinance Finals Examarthur the greatNo ratings yet

- Documentary Stamp Tax FormDocument3 pagesDocumentary Stamp Tax Formnegotiator0% (1)

- Profit and Wealth MaximizationDocument3 pagesProfit and Wealth MaximizationArshad MohammedNo ratings yet

- Macroeconomics Canadian 8th Edition Sayre Solutions ManualDocument5 pagesMacroeconomics Canadian 8th Edition Sayre Solutions Manualregattabump0dt100% (36)

- Maf Seminar Slide SyafDocument19 pagesMaf Seminar Slide SyafNur SyafiqahNo ratings yet

- Labor 1 185-190Document9 pagesLabor 1 185-190Samantha CepedaNo ratings yet

- Past Year Eco Question PaperDocument11 pagesPast Year Eco Question PaperzaniNo ratings yet

- Do Restaurant Owners Have To Pay GST On The Entire Amount of The Bill If Delivery Is Done by Zomato?Document2 pagesDo Restaurant Owners Have To Pay GST On The Entire Amount of The Bill If Delivery Is Done by Zomato?pratyusha_3No ratings yet

- Supply, Demand & EquilibriumDocument4 pagesSupply, Demand & EquilibriumClarisse AnnNo ratings yet

- Central Bank Policies in Mexico: Targets, Instruments, and PerformanceDocument28 pagesCentral Bank Policies in Mexico: Targets, Instruments, and PerformanceAdrian Alberto Martínez GonzálezNo ratings yet

- Basic Concepts of EconomicsDocument20 pagesBasic Concepts of EconomicsravinbharathiNo ratings yet

- OptionsDocument30 pagesOptionsJubit JohnsonNo ratings yet