Download as pdf or txt

You might also like

- Apple Blossom Cologne Company Common Size Financial Statement Desember 31, 2003Document1 pageApple Blossom Cologne Company Common Size Financial Statement Desember 31, 2003Lintang UtomoNo ratings yet

- Ghana Revenue Authority: Monthly Vat & Nhil Flat Rate ReturnDocument2 pagesGhana Revenue Authority: Monthly Vat & Nhil Flat Rate Returnokatakyie1990No ratings yet

- How to Handle Goods and Service Tax (GST)From EverandHow to Handle Goods and Service Tax (GST)Rating: 4.5 out of 5 stars4.5/5 (4)

- Kannada GrammerDocument15 pagesKannada GrammerPrince Vikraam SonuNo ratings yet

- Sherrod, Inc., Reported Pretax Accounting Income of $88 Million For 2018Document15 pagesSherrod, Inc., Reported Pretax Accounting Income of $88 Million For 2018laale dijaanNo ratings yet

- Income Tax Act As Amended by The Finance Act, 2008: SupplementDocument13 pagesIncome Tax Act As Amended by The Finance Act, 2008: SupplementbhavaniNo ratings yet

- Carpolaw Com Everything You Need To Know About Create Act in The PhilippinesDocument8 pagesCarpolaw Com Everything You Need To Know About Create Act in The PhilippinesShane TabunggaoNo ratings yet

- Direct Tax BookletDocument24 pagesDirect Tax Bookletmbhartia999No ratings yet

- Anubhav Sood Helga Cardoza Ragini Rastogi Sumit Kothari Vani SubramanianDocument18 pagesAnubhav Sood Helga Cardoza Ragini Rastogi Sumit Kothari Vani SubramanianSakshi TewariNo ratings yet

- Taxation of Corporation YogeshDocument4 pagesTaxation of Corporation YogeshyogeshvermastockNo ratings yet

- Taxation in India Vs AfghanistanDocument11 pagesTaxation in India Vs AfghanistanKomal AgrawalNo ratings yet

- Tax On Corporation MaterialsDocument18 pagesTax On Corporation Materialsjdy managbanagNo ratings yet

- Types of Supply GSTDocument46 pagesTypes of Supply GSTRajatKumarNo ratings yet

- Direct Tax CodeDocument8 pagesDirect Tax CodeImran HassanNo ratings yet

- Tax Updates Under CREATE LawDocument4 pagesTax Updates Under CREATE LawSandy ArticaNo ratings yet

- Tax Supplemental Reviewer - October 2019Document46 pagesTax Supplemental Reviewer - October 2019Daniel Anthony CabreraNo ratings yet

- Corporate Income Taxes StudentsDocument6 pagesCorporate Income Taxes StudentsClazther MendezNo ratings yet

- Directors' Manual 2012Document54 pagesDirectors' Manual 2012harshagarwal5No ratings yet

- Corporate Income Taxes and Tax RatesDocument38 pagesCorporate Income Taxes and Tax RatesShaheen ShahNo ratings yet

- Taxation Law Assignment by Sushali Shruti 18FLICDDN01144Document10 pagesTaxation Law Assignment by Sushali Shruti 18FLICDDN01144Shreya VermaNo ratings yet

- Changes Due To CREATE Law Corporate Income Tax (CIT) Reforms Under CREATE ActDocument7 pagesChanges Due To CREATE Law Corporate Income Tax (CIT) Reforms Under CREATE ActYietNo ratings yet

- Research On CREATE LawDocument7 pagesResearch On CREATE LawalbycadavisNo ratings yet

- Corporate Income TaxationDocument43 pagesCorporate Income TaxationRose May AdanNo ratings yet

- Benefit. The Service Tax Levied On Services Is Actually Borne byDocument6 pagesBenefit. The Service Tax Levied On Services Is Actually Borne bykarnicaNo ratings yet

- Indian Taxation SystemDocument15 pagesIndian Taxation SystemassatputeNo ratings yet

- Id Tax Indonesian Tax Guide 2019 2020 enDocument84 pagesId Tax Indonesian Tax Guide 2019 2020 enDesty Andini LarasatiNo ratings yet

- VAT Road To GSTDocument19 pagesVAT Road To GSTVarun PuriNo ratings yet

- India Tax Profile: Produced in Conjunction With The KPMG Asia Pacific Tax CentreDocument24 pagesIndia Tax Profile: Produced in Conjunction With The KPMG Asia Pacific Tax CentreUday MunjalNo ratings yet

- CREATE Salient ProvisionsDocument3 pagesCREATE Salient ProvisionsAldrin Santos AntonioNo ratings yet

- SMNV Group CDocument20 pagesSMNV Group CHeena DuaNo ratings yet

- Presenting: Direct Tax - Trends in IndiaDocument27 pagesPresenting: Direct Tax - Trends in IndiatusharNo ratings yet

- International Tax: Bangladesh Highlights 2020Document8 pagesInternational Tax: Bangladesh Highlights 2020Mehadi HasanNo ratings yet

- Goods and Services Tax - An Overview: Central Board of Excise & CustomsDocument10 pagesGoods and Services Tax - An Overview: Central Board of Excise & CustomsvsaraNo ratings yet

- Taxation System in IndiaDocument5 pagesTaxation System in IndiaSiddharth NagarNo ratings yet

- All India Legal ForumDocument7 pagesAll India Legal ForumkhushiNo ratings yet

- Goods and Services Tax (GST) in India: Ca R.K.BhallaDocument27 pagesGoods and Services Tax (GST) in India: Ca R.K.BhallaAditya V v s r kNo ratings yet

- 1) Rate Structure Under GST: GST Rates For Supply of Goods: For Inter-State Supply, IGST Rates Are: Nil, 0.25%Document2 pages1) Rate Structure Under GST: GST Rates For Supply of Goods: For Inter-State Supply, IGST Rates Are: Nil, 0.25%Mohit BNo ratings yet

- 7 Taxation Reddy SirDocument32 pages7 Taxation Reddy SirTanay BansalNo ratings yet

- Indonesian Tax Treatment For Foreign Drilling Companies FDCDocument4 pagesIndonesian Tax Treatment For Foreign Drilling Companies FDCJoko ArifiantoNo ratings yet

- GST Oct 17Document23 pagesGST Oct 17himanNo ratings yet

- 6mmmmm: M M M MDocument12 pages6mmmmm: M M M MUtsav PoddarNo ratings yet

- Tax Structure and Basic ConceptsDocument64 pagesTax Structure and Basic Conceptstushar_shetti100% (1)

- GST The Game Changer: GST Will Be A Game Changing Reform For Indian Economy byDocument6 pagesGST The Game Changer: GST Will Be A Game Changing Reform For Indian Economy bySiddiqui AdamNo ratings yet

- Japan Tax Profile: Produced in Conjunction With The KPMG Asia Pacific Tax CentreDocument15 pagesJapan Tax Profile: Produced in Conjunction With The KPMG Asia Pacific Tax CentreKris MehtaNo ratings yet

- Unit 6 eefmDocument25 pagesUnit 6 eefmpatilmadamNo ratings yet

- Presentation On GST by Himanshu and KrishnaDocument21 pagesPresentation On GST by Himanshu and KrishnahimanshuNo ratings yet

- CREATE ManualDocument98 pagesCREATE ManualGenny JovellanosNo ratings yet

- GST (Goods and Service Tax) : 120 LakhsDocument7 pagesGST (Goods and Service Tax) : 120 LakhsSayyed HuzaifNo ratings yet

- Income Tax India Basic DetailsDocument28 pagesIncome Tax India Basic DetailsrupaparaNo ratings yet

- (Goods and Services Tax) : Biggest Tax Reform Since Independence .Document80 pages(Goods and Services Tax) : Biggest Tax Reform Since Independence .isha patilNo ratings yet

- Taxation System in IndiaDocument35 pagesTaxation System in IndiaSaif UddinNo ratings yet

- Taxation SlideDocument26 pagesTaxation SlidePei Jia WahNo ratings yet

- Income Tax Quick Recap CapsulDocument24 pagesIncome Tax Quick Recap CapsulAmanNo ratings yet

- Ra 11534 - Corporate Recovery & Tax Incentives For Enterprises Act (Create)Document11 pagesRa 11534 - Corporate Recovery & Tax Incentives For Enterprises Act (Create)Rolly Balagon Caballero100% (1)

- Taxation System in IndiaDocument30 pagesTaxation System in IndiaSwapnil Pisal-DeshmukhNo ratings yet

- GST Unit 1Document52 pagesGST Unit 1SANSKRITI YADAV 22DM236No ratings yet

- Taxation-Reforms PRESENTATIONDocument17 pagesTaxation-Reforms PRESENTATIONRaman KumarNo ratings yet

- Assignment On Corporate Taxation in BangladeshDocument9 pagesAssignment On Corporate Taxation in Bangladeshsalekin0070% (1)

- Lesotho Tax SystemDocument6 pagesLesotho Tax Systemhenryxmphana3No ratings yet

- GST in IndiaDocument27 pagesGST in IndiaDawn LoveNo ratings yet

- PHD Research Bureau PHD Chamber of Commerce and IndustryDocument33 pagesPHD Research Bureau PHD Chamber of Commerce and IndustrySUNIL PUJARINo ratings yet

- Double TaxationDocument8 pagesDouble TaxationArun KumarNo ratings yet

- The Little Book of Valuation Book SummaryDocument12 pagesThe Little Book of Valuation Book SummaryKapil AroraNo ratings yet

- Newsletter - October 2021Document12 pagesNewsletter - October 2021Kapil AroraNo ratings yet

- Blockchain Panel DiscussionDocument5 pagesBlockchain Panel DiscussionKapil AroraNo ratings yet

- Ratio Analysis: A Study On Financial Performance of Tata MotorsDocument7 pagesRatio Analysis: A Study On Financial Performance of Tata MotorsKapil AroraNo ratings yet

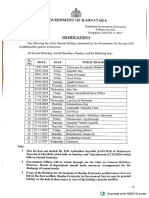

- Karnataka State Holidays List 2024 NotificationDocument5 pagesKarnataka State Holidays List 2024 NotificationKapil AroraNo ratings yet

- 100 Things Successful Leaders Do - Little Lessons in LeadershipDocument332 pages100 Things Successful Leaders Do - Little Lessons in LeadershipKapil AroraNo ratings yet

- The Financial Times Guide To Corporate Valuation Epub EbookDocument18 pagesThe Financial Times Guide To Corporate Valuation Epub EbookKapil AroraNo ratings yet

- JKLU Conf 2019Document4 pagesJKLU Conf 2019Kapil AroraNo ratings yet

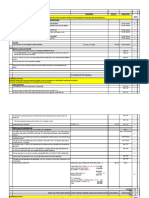

- "RATIO ANALYSIS OF ASTEC LIFESCIENCES LTD." Final ReportDocument73 pages"RATIO ANALYSIS OF ASTEC LIFESCIENCES LTD." Final ReportKapil Arora100% (1)

- Part 02 - Spoken Kannada PDFDocument50 pagesPart 02 - Spoken Kannada PDFKapil AroraNo ratings yet

- It Goi Note On Mat and AmtDocument17 pagesIt Goi Note On Mat and AmtKapil AroraNo ratings yet

- IT of Business ProfessionDocument13 pagesIT of Business ProfessionKapil AroraNo ratings yet

- BBA Course Catalogue July 2015Document82 pagesBBA Course Catalogue July 2015Kapil AroraNo ratings yet

- JKLU IET Brochure PDFDocument28 pagesJKLU IET Brochure PDFKapil AroraNo ratings yet

- BBA Course CatalogueDocument80 pagesBBA Course CatalogueKapil AroraNo ratings yet

- Assessment & Procedure & Other Concepts: Dr. Shakuntala Misra National Rehabilitation UniversityDocument14 pagesAssessment & Procedure & Other Concepts: Dr. Shakuntala Misra National Rehabilitation UniversityShubham PathakNo ratings yet

- Analysis of MCX Stock Exchange Ltd. vs. National Stock Exchange of India LTDDocument8 pagesAnalysis of MCX Stock Exchange Ltd. vs. National Stock Exchange of India LTDAyush Kumar SinghNo ratings yet

- Taxation - Vietnam (TX-VNM) (F6) SASG 2021 SP Amends - FinalDocument20 pagesTaxation - Vietnam (TX-VNM) (F6) SASG 2021 SP Amends - FinalXuân PhạmNo ratings yet

- Full Syllabus GST Test - 1 Without AnswersDocument19 pagesFull Syllabus GST Test - 1 Without Answersrajbhanushali3981No ratings yet

- Revised Offer Letter - ResolveTechDocument2 pagesRevised Offer Letter - ResolveTechsayali kadNo ratings yet

- 50501bos40223 L1indirecttaxDocument3 pages50501bos40223 L1indirecttaxCOMEDY WATCHNo ratings yet

- CTAA040 - CTAF080 - Test 5 Solution - 2023Document6 pagesCTAA040 - CTAF080 - Test 5 Solution - 2023Given RefilweNo ratings yet

- Taxation TheoriesDocument8 pagesTaxation TheoriesJean Fajardo BadilloNo ratings yet

- Itr-V: Income Tax Return Verification Form IndianDocument1 pageItr-V: Income Tax Return Verification Form Indianapi-25886395No ratings yet

- CSJM University Kanpur Faculty of Commerce: B. Com. (Honors) ProgramDocument30 pagesCSJM University Kanpur Faculty of Commerce: B. Com. (Honors) ProgramNitish KumarNo ratings yet

- M7 - P1 Individual Income Taxation - Students'Document66 pagesM7 - P1 Individual Income Taxation - Students'micaella pasionNo ratings yet

- Budgeting System in Ethiopia: Program Budget System: EmailDocument16 pagesBudgeting System in Ethiopia: Program Budget System: EmailtgNo ratings yet

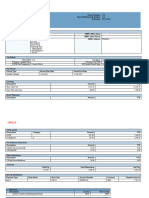

- Heads of Income Monthly Actual YTD Projected Total: EIT Services India PVT LTD Income Tax Computation StatementDocument2 pagesHeads of Income Monthly Actual YTD Projected Total: EIT Services India PVT LTD Income Tax Computation Statementsunit pattanayakNo ratings yet

- 20230513121459premium Receipt 71367008 PDFDocument1 page20230513121459premium Receipt 71367008 PDFsateesh008No ratings yet

- Ind As 12Document5 pagesInd As 12Akshayaa KarthikaNo ratings yet

- Double Taxation Avoidance AgreementDocument5 pagesDouble Taxation Avoidance Agreementabhaypandit100% (2)

- Constitutional Provisions Relating To TaxDocument9 pagesConstitutional Provisions Relating To Taxrakshitha9reddy-1No ratings yet

- Chap 6 Relief and RebateDocument15 pagesChap 6 Relief and RebateKelvin OngNo ratings yet

- HKCEE Economics Multiple ChoiceDocument244 pagesHKCEE Economics Multiple ChoiceVickie Li100% (2)

- Inventory List of Unused Official ReceiptsDocument3 pagesInventory List of Unused Official ReceiptsOlympian MedicalNo ratings yet

- Income Tax Calulator With Computation of IncomeDocument18 pagesIncome Tax Calulator With Computation of IncomeSurendra DevadigaNo ratings yet

- Simplified Tax InvoiceDocument1 pageSimplified Tax InvoiceixaxkhanNo ratings yet

- UICAnnual1099 2010 01 09 00.32.54.009000Document1 pageUICAnnual1099 2010 01 09 00.32.54.009000Paul Michael WiremanNo ratings yet

- SalarySlip 5876095Document1 pageSalarySlip 5876095Larry WackoffNo ratings yet

- CIR vs. CLDCDocument1 pageCIR vs. CLDCLouise Bolivar DadivasNo ratings yet

- 429218520-Uk-Payslip 2Document3 pages429218520-Uk-Payslip 2Vaishnavi DappureNo ratings yet

- T 4 - Co-Ownership Estate TrustDocument21 pagesT 4 - Co-Ownership Estate TrustKristine Aubrey AlvarezNo ratings yet