TAX LAW BALA SA BAR SERIES Export

TAX LAW BALA SA BAR SERIES Export

You might also like

- Chapter 2 - Taxes, Tax Laws, and Tax AdministrationDocument7 pagesChapter 2 - Taxes, Tax Laws, and Tax Administrationreymardico100% (2)

- Income Taxation Notes On BanggawanDocument5 pagesIncome Taxation Notes On BanggawanHopey100% (4)

- Salary-Chp 3Document38 pagesSalary-Chp 3Rozina TabassumNo ratings yet

- Key Propositions 148 SHRI KAPIL GOELDocument89 pagesKey Propositions 148 SHRI KAPIL GOELRajivShahNo ratings yet

- Bar Q&A Taxation-Volume 1: General Principles of Taxation Abelardo T. DomondonDocument17 pagesBar Q&A Taxation-Volume 1: General Principles of Taxation Abelardo T. DomondonFrance SanchezNo ratings yet

- Untitled Document-1Document3 pagesUntitled Document-1Shan Sai BuladoNo ratings yet

- Tax 1 - Unit 1. Chapter 2Document9 pagesTax 1 - Unit 1. Chapter 2Jamaica ManilaNo ratings yet

- HQ02 - Taxes, Tax Laws and Tax AdministrationDocument10 pagesHQ02 - Taxes, Tax Laws and Tax AdministrationJimmyChaoNo ratings yet

- Module-02-Taxes, Laws, Systems and AdministrationDocument8 pagesModule-02-Taxes, Laws, Systems and AdministrationElle LegaspiNo ratings yet

- Module 02 - Taxes, Laws, Systems and AdministrationDocument22 pagesModule 02 - Taxes, Laws, Systems and AdministrationElla Marie Lopez0% (1)

- Taxes, Tax Laws and Tax Administration: TAXATION - Module 2Document6 pagesTaxes, Tax Laws and Tax Administration: TAXATION - Module 2Diva Bianca MariñasNo ratings yet

- AC 2202 - Notes (1 TO 4)Document40 pagesAC 2202 - Notes (1 TO 4)SMT awesomeNo ratings yet

- M2 - Taxes, Tax Laws and Tax AdministrationDocument31 pagesM2 - Taxes, Tax Laws and Tax AdministrationTERRIUS AceNo ratings yet

- TaxationDocument2 pagesTaxationRina Bico AdvinculaNo ratings yet

- TAXATION ReviewerDocument18 pagesTAXATION ReviewerAyessa GayamoNo ratings yet

- Taxation 1 - Atty. Santos Discussion-2 PDFDocument8 pagesTaxation 1 - Atty. Santos Discussion-2 PDFmaxNo ratings yet

- Income TaxationDocument5 pagesIncome TaxationG12STEM2 Genobisa, Athea ZaneNo ratings yet

- Tax Remedies: Bacc 2 Income Taxation Franklin D. Lopez, CpaDocument4 pagesTax Remedies: Bacc 2 Income Taxation Franklin D. Lopez, CpaJaeun SooNo ratings yet

- Tax Assign1Document4 pagesTax Assign1Leoreyn Faye MedinaNo ratings yet

- Week 2 Course Material For Income TaxationDocument10 pagesWeek 2 Course Material For Income TaxationKrizel VeneracionNo ratings yet

- Processes That Are Included or Embodied in The Term "Taxation"Document4 pagesProcesses That Are Included or Embodied in The Term "Taxation"GwapaNo ratings yet

- Income TaxDocument9 pagesIncome TaxRhea MendozaNo ratings yet

- Tax 1 Reviewer - Compress Vol 3Document4 pagesTax 1 Reviewer - Compress Vol 3bingoNo ratings yet

- Juicy Notes (2011)Document89 pagesJuicy Notes (2011)Edmart VicedoNo ratings yet

- Chapter 2Document18 pagesChapter 2geexellNo ratings yet

- Chapter 2 Taxes, Tax Laws and Tax AdministrationDocument7 pagesChapter 2 Taxes, Tax Laws and Tax AdministrationElisa Jane AbellaNo ratings yet

- Reviewer Taxation Modules 1 - 3Document11 pagesReviewer Taxation Modules 1 - 3afeiahnaniNo ratings yet

- Taxation ReviewerDocument8 pagesTaxation ReviewerDaphne FerciaNo ratings yet

- Taxation Law NotesDocument15 pagesTaxation Law NotesKuracha LoftNo ratings yet

- Tep's Tones Tax Notes 1 and 2Document80 pagesTep's Tones Tax Notes 1 and 2Paul Dean MarkNo ratings yet

- Income Tax 02 Taxes, Tax Laws and AdministrationDocument11 pagesIncome Tax 02 Taxes, Tax Laws and AdministrationJade Ivy GarciaNo ratings yet

- Feb 17, 2024 - Notes of BepitelDocument11 pagesFeb 17, 2024 - Notes of BepitelbepitelbreylleNo ratings yet

- Manila Cavite Laguna Cebu Cagayan de Oro DavaoDocument8 pagesManila Cavite Laguna Cebu Cagayan de Oro DavaoRaymond RosalesNo ratings yet

- 2019 Taxation Law Last Minute Tips PDFDocument11 pages2019 Taxation Law Last Minute Tips PDFz v100% (1)

- Taxation 1 Midterms ReviewerDocument28 pagesTaxation 1 Midterms ReviewerDenise FranchescaNo ratings yet

- Taxation LawDocument70 pagesTaxation LawJing Goal Merit100% (1)

- General Principles of Taxation.Document24 pagesGeneral Principles of Taxation.Christine RaizNo ratings yet

- EcoTax Finals ReportingDocument6 pagesEcoTax Finals Reportingmau mauNo ratings yet

- Principles of TaxationDocument6 pagesPrinciples of Taxationjohn paulNo ratings yet

- Lesson 2 (2 Hours) Taxes, Tax Laws and Tax Administration: Knowledge Engineer: Mark John D. Gonzales, Cpa, CTT, CHTS, MPBMDocument7 pagesLesson 2 (2 Hours) Taxes, Tax Laws and Tax Administration: Knowledge Engineer: Mark John D. Gonzales, Cpa, CTT, CHTS, MPBMtayrayrmp68No ratings yet

- Taxation Module 01 2023 24Document6 pagesTaxation Module 01 2023 24Julius MuicoNo ratings yet

- Income TaxationDocument12 pagesIncome TaxationPeralta Renn JethroNo ratings yet

- Tax.3301-2 Classification of TaxesDocument3 pagesTax.3301-2 Classification of TaxesDena Heart OrenioNo ratings yet

- Tax.3201-2 Classification of TaxesDocument3 pagesTax.3201-2 Classification of TaxesMira Louise HernandezNo ratings yet

- Dimaampao: Doctrine of Symbiotic Relationship: Taxes AreDocument3 pagesDimaampao: Doctrine of Symbiotic Relationship: Taxes AreCelestino LawNo ratings yet

- Chapter 1 NotesDocument12 pagesChapter 1 NotesGerald Nitz PonceNo ratings yet

- Chaper 2 Taxes, Tax, Laws and Tax AdministrationDocument35 pagesChaper 2 Taxes, Tax, Laws and Tax AdministrationPearlyn VillarinNo ratings yet

- PLS TAX Review Midterm ExamDocument72 pagesPLS TAX Review Midterm ExamKim OngNo ratings yet

- Taxpayers and Tax Compliance RequirementsDocument8 pagesTaxpayers and Tax Compliance RequirementsEric Kevin LecarosNo ratings yet

- Chapter IIDocument12 pagesChapter IIshirileon08No ratings yet

- General Principles of Taxation June 2019 College of LawDocument89 pagesGeneral Principles of Taxation June 2019 College of LawJoanna Marie100% (1)

- Remedies in TaxationDocument8 pagesRemedies in TaxationabcyuiopNo ratings yet

- Tax ReviewDocument7 pagesTax Reviewhydoe james elanNo ratings yet

- Legal Not Subject To Illegal SubjectDocument3 pagesLegal Not Subject To Illegal SubjectKisha Alyana ColindresNo ratings yet

- CH 2 TaxationDocument7 pagesCH 2 Taxationshannethy muñozNo ratings yet

- Module 02 Taxes, Tax Laws and AdministrationDocument7 pagesModule 02 Taxes, Tax Laws and AdministrationCris Martin IloNo ratings yet

- Fundamental Principles OF Taxation: Mr. Mario M. Castro, Cpa, Mba Tax ConsultantDocument19 pagesFundamental Principles OF Taxation: Mr. Mario M. Castro, Cpa, Mba Tax ConsultantKristine Aubrey AlvarezNo ratings yet

- 1040 Exam Prep Module III: Items Excluded from Gross IncomeFrom Everand1040 Exam Prep Module III: Items Excluded from Gross IncomeRating: 1 out of 5 stars1/5 (1)

- 1040 Exam Prep Module XI: Circular 230 and AMTFrom Everand1040 Exam Prep Module XI: Circular 230 and AMTRating: 1 out of 5 stars1/5 (1)

- TAX LAW BALA SA BAR SERIES ExportDocument10 pagesTAX LAW BALA SA BAR SERIES Exportmetrexz17.03No ratings yet

- TAX LAW BALA SA BAR SERIES ExportDocument10 pagesTAX LAW BALA SA BAR SERIES Exportmetrexz17.03No ratings yet

- Tax Law Bala Sa Bar SeriesDocument174 pagesTax Law Bala Sa Bar Seriesmetrexz17.03No ratings yet

- Ratha RemittancesDocument2 pagesRatha Remittancesmetrexz17.03No ratings yet

- Do010 2017Document2 pagesDo010 2017metrexz17.03No ratings yet

- What Is My Salary StructureDocument2 pagesWhat Is My Salary Structuredvenky85No ratings yet

- 2024 Tax III Module 1 Notes-1Document127 pages2024 Tax III Module 1 Notes-1katelynnewson07No ratings yet

- Sale 238 26-06-2023Document2 pagesSale 238 26-06-2023Creeper TechnologiesNo ratings yet

- Earnings Statement: SSN: XXX-XX-2691Document1 pageEarnings Statement: SSN: XXX-XX-2691emily ambrosino0% (2)

- Icaz Cta Zimtax Module 2022 EditedDocument272 pagesIcaz Cta Zimtax Module 2022 EditedAbigal Makweche100% (1)

- Subledger Accounting Implementation Guide Oracle R12Document342 pagesSubledger Accounting Implementation Guide Oracle R12RBalajiNo ratings yet

- Syllabus Mcom 2017Document9 pagesSyllabus Mcom 2017khalidNo ratings yet

- Block Credit Under GSTDocument2 pagesBlock Credit Under GSTparam.ginni100% (1)

- 1 Accounting Theory and PracticeDocument16 pages1 Accounting Theory and PracticeFirman PrasetyaNo ratings yet

- MGT480 Term PaperDocument32 pagesMGT480 Term PaperShurovi UrmiNo ratings yet

- Straight Problems Income Tax Bsa2Document2 pagesStraight Problems Income Tax Bsa2dimpy dNo ratings yet

- G. Telecoms, Inc.: Billing StatementDocument1 pageG. Telecoms, Inc.: Billing StatementJTPA LIMNo ratings yet

- Batas Pambansa Blg. 232 & Ra 10931 Report - Ana Mae SaysonDocument17 pagesBatas Pambansa Blg. 232 & Ra 10931 Report - Ana Mae SaysonAna Mae SaysonNo ratings yet

- Fatca Crs Non IndividualDocument1 pageFatca Crs Non IndividualHarsh-AgarwalNo ratings yet

- 105 Invoice (Innotronix) 22-23Document1 page105 Invoice (Innotronix) 22-23account.adminNo ratings yet

- Part-A Unit-I: Business EnvironmentDocument4 pagesPart-A Unit-I: Business EnvironmentShankar ReddyNo ratings yet

- Application of PercentDocument12 pagesApplication of PercentJericha Amparado QuinteNo ratings yet

- Tax Stamp Rps A4Document4 pagesTax Stamp Rps A4ashfaqahmadNo ratings yet

- International Financial Management Notes Unit-1Document15 pagesInternational Financial Management Notes Unit-1Geetha aptdcNo ratings yet

- Foreign Direct Investment ImperialDocument5 pagesForeign Direct Investment ImperialokiNo ratings yet

- Tax 1 Digest CompilationDocument13 pagesTax 1 Digest CompilationxyrakrezelNo ratings yet

- Multinational Companies and Its EnvironmentDocument10 pagesMultinational Companies and Its EnvironmentLoren RosariaNo ratings yet

- December 23, 2015 Tribune-PhonographDocument16 pagesDecember 23, 2015 Tribune-PhonographcwmediaNo ratings yet

- Assessment (Full) Quick RevisionDocument16 pagesAssessment (Full) Quick RevisionKush ShahNo ratings yet

- Retirement Notification FormDocument2 pagesRetirement Notification FormAbongile PhinyanaNo ratings yet

- Mutual Funds: Concept and CharacteristicsDocument179 pagesMutual Funds: Concept and CharacteristicssiddharthzalaNo ratings yet

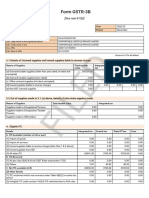

- Filed: Form GSTR-3BDocument2 pagesFiled: Form GSTR-3Bkrishswat7912No ratings yet

- I.TAx 302Document4 pagesI.TAx 302tadepalli patanjaliNo ratings yet

Download as pdf or txt

You might also like

- Chapter 2 - Taxes, Tax Laws, and Tax AdministrationDocument7 pagesChapter 2 - Taxes, Tax Laws, and Tax Administrationreymardico100% (2)

- Income Taxation Notes On BanggawanDocument5 pagesIncome Taxation Notes On BanggawanHopey100% (4)

- Salary-Chp 3Document38 pagesSalary-Chp 3Rozina TabassumNo ratings yet

- Key Propositions 148 SHRI KAPIL GOELDocument89 pagesKey Propositions 148 SHRI KAPIL GOELRajivShahNo ratings yet

- Bar Q&A Taxation-Volume 1: General Principles of Taxation Abelardo T. DomondonDocument17 pagesBar Q&A Taxation-Volume 1: General Principles of Taxation Abelardo T. DomondonFrance SanchezNo ratings yet

- Untitled Document-1Document3 pagesUntitled Document-1Shan Sai BuladoNo ratings yet

- Tax 1 - Unit 1. Chapter 2Document9 pagesTax 1 - Unit 1. Chapter 2Jamaica ManilaNo ratings yet

- HQ02 - Taxes, Tax Laws and Tax AdministrationDocument10 pagesHQ02 - Taxes, Tax Laws and Tax AdministrationJimmyChaoNo ratings yet

- Module-02-Taxes, Laws, Systems and AdministrationDocument8 pagesModule-02-Taxes, Laws, Systems and AdministrationElle LegaspiNo ratings yet

- Module 02 - Taxes, Laws, Systems and AdministrationDocument22 pagesModule 02 - Taxes, Laws, Systems and AdministrationElla Marie Lopez0% (1)

- Taxes, Tax Laws and Tax Administration: TAXATION - Module 2Document6 pagesTaxes, Tax Laws and Tax Administration: TAXATION - Module 2Diva Bianca MariñasNo ratings yet

- AC 2202 - Notes (1 TO 4)Document40 pagesAC 2202 - Notes (1 TO 4)SMT awesomeNo ratings yet

- M2 - Taxes, Tax Laws and Tax AdministrationDocument31 pagesM2 - Taxes, Tax Laws and Tax AdministrationTERRIUS AceNo ratings yet

- TaxationDocument2 pagesTaxationRina Bico AdvinculaNo ratings yet

- TAXATION ReviewerDocument18 pagesTAXATION ReviewerAyessa GayamoNo ratings yet

- Taxation 1 - Atty. Santos Discussion-2 PDFDocument8 pagesTaxation 1 - Atty. Santos Discussion-2 PDFmaxNo ratings yet

- Income TaxationDocument5 pagesIncome TaxationG12STEM2 Genobisa, Athea ZaneNo ratings yet

- Tax Remedies: Bacc 2 Income Taxation Franklin D. Lopez, CpaDocument4 pagesTax Remedies: Bacc 2 Income Taxation Franklin D. Lopez, CpaJaeun SooNo ratings yet

- Tax Assign1Document4 pagesTax Assign1Leoreyn Faye MedinaNo ratings yet

- Week 2 Course Material For Income TaxationDocument10 pagesWeek 2 Course Material For Income TaxationKrizel VeneracionNo ratings yet

- Processes That Are Included or Embodied in The Term "Taxation"Document4 pagesProcesses That Are Included or Embodied in The Term "Taxation"GwapaNo ratings yet

- Income TaxDocument9 pagesIncome TaxRhea MendozaNo ratings yet

- Tax 1 Reviewer - Compress Vol 3Document4 pagesTax 1 Reviewer - Compress Vol 3bingoNo ratings yet

- Juicy Notes (2011)Document89 pagesJuicy Notes (2011)Edmart VicedoNo ratings yet

- Chapter 2Document18 pagesChapter 2geexellNo ratings yet

- Chapter 2 Taxes, Tax Laws and Tax AdministrationDocument7 pagesChapter 2 Taxes, Tax Laws and Tax AdministrationElisa Jane AbellaNo ratings yet

- Reviewer Taxation Modules 1 - 3Document11 pagesReviewer Taxation Modules 1 - 3afeiahnaniNo ratings yet

- Taxation ReviewerDocument8 pagesTaxation ReviewerDaphne FerciaNo ratings yet

- Taxation Law NotesDocument15 pagesTaxation Law NotesKuracha LoftNo ratings yet

- Tep's Tones Tax Notes 1 and 2Document80 pagesTep's Tones Tax Notes 1 and 2Paul Dean MarkNo ratings yet

- Income Tax 02 Taxes, Tax Laws and AdministrationDocument11 pagesIncome Tax 02 Taxes, Tax Laws and AdministrationJade Ivy GarciaNo ratings yet

- Feb 17, 2024 - Notes of BepitelDocument11 pagesFeb 17, 2024 - Notes of BepitelbepitelbreylleNo ratings yet

- Manila Cavite Laguna Cebu Cagayan de Oro DavaoDocument8 pagesManila Cavite Laguna Cebu Cagayan de Oro DavaoRaymond RosalesNo ratings yet

- 2019 Taxation Law Last Minute Tips PDFDocument11 pages2019 Taxation Law Last Minute Tips PDFz v100% (1)

- Taxation 1 Midterms ReviewerDocument28 pagesTaxation 1 Midterms ReviewerDenise FranchescaNo ratings yet

- Taxation LawDocument70 pagesTaxation LawJing Goal Merit100% (1)

- General Principles of Taxation.Document24 pagesGeneral Principles of Taxation.Christine RaizNo ratings yet

- EcoTax Finals ReportingDocument6 pagesEcoTax Finals Reportingmau mauNo ratings yet

- Principles of TaxationDocument6 pagesPrinciples of Taxationjohn paulNo ratings yet

- Lesson 2 (2 Hours) Taxes, Tax Laws and Tax Administration: Knowledge Engineer: Mark John D. Gonzales, Cpa, CTT, CHTS, MPBMDocument7 pagesLesson 2 (2 Hours) Taxes, Tax Laws and Tax Administration: Knowledge Engineer: Mark John D. Gonzales, Cpa, CTT, CHTS, MPBMtayrayrmp68No ratings yet

- Taxation Module 01 2023 24Document6 pagesTaxation Module 01 2023 24Julius MuicoNo ratings yet

- Income TaxationDocument12 pagesIncome TaxationPeralta Renn JethroNo ratings yet

- Tax.3301-2 Classification of TaxesDocument3 pagesTax.3301-2 Classification of TaxesDena Heart OrenioNo ratings yet

- Tax.3201-2 Classification of TaxesDocument3 pagesTax.3201-2 Classification of TaxesMira Louise HernandezNo ratings yet

- Dimaampao: Doctrine of Symbiotic Relationship: Taxes AreDocument3 pagesDimaampao: Doctrine of Symbiotic Relationship: Taxes AreCelestino LawNo ratings yet

- Chapter 1 NotesDocument12 pagesChapter 1 NotesGerald Nitz PonceNo ratings yet

- Chaper 2 Taxes, Tax, Laws and Tax AdministrationDocument35 pagesChaper 2 Taxes, Tax, Laws and Tax AdministrationPearlyn VillarinNo ratings yet

- PLS TAX Review Midterm ExamDocument72 pagesPLS TAX Review Midterm ExamKim OngNo ratings yet

- Taxpayers and Tax Compliance RequirementsDocument8 pagesTaxpayers and Tax Compliance RequirementsEric Kevin LecarosNo ratings yet

- Chapter IIDocument12 pagesChapter IIshirileon08No ratings yet

- General Principles of Taxation June 2019 College of LawDocument89 pagesGeneral Principles of Taxation June 2019 College of LawJoanna Marie100% (1)

- Remedies in TaxationDocument8 pagesRemedies in TaxationabcyuiopNo ratings yet

- Tax ReviewDocument7 pagesTax Reviewhydoe james elanNo ratings yet

- Legal Not Subject To Illegal SubjectDocument3 pagesLegal Not Subject To Illegal SubjectKisha Alyana ColindresNo ratings yet

- CH 2 TaxationDocument7 pagesCH 2 Taxationshannethy muñozNo ratings yet

- Module 02 Taxes, Tax Laws and AdministrationDocument7 pagesModule 02 Taxes, Tax Laws and AdministrationCris Martin IloNo ratings yet

- Fundamental Principles OF Taxation: Mr. Mario M. Castro, Cpa, Mba Tax ConsultantDocument19 pagesFundamental Principles OF Taxation: Mr. Mario M. Castro, Cpa, Mba Tax ConsultantKristine Aubrey AlvarezNo ratings yet

- 1040 Exam Prep Module III: Items Excluded from Gross IncomeFrom Everand1040 Exam Prep Module III: Items Excluded from Gross IncomeRating: 1 out of 5 stars1/5 (1)

- 1040 Exam Prep Module XI: Circular 230 and AMTFrom Everand1040 Exam Prep Module XI: Circular 230 and AMTRating: 1 out of 5 stars1/5 (1)

- TAX LAW BALA SA BAR SERIES ExportDocument10 pagesTAX LAW BALA SA BAR SERIES Exportmetrexz17.03No ratings yet

- TAX LAW BALA SA BAR SERIES ExportDocument10 pagesTAX LAW BALA SA BAR SERIES Exportmetrexz17.03No ratings yet

- Tax Law Bala Sa Bar SeriesDocument174 pagesTax Law Bala Sa Bar Seriesmetrexz17.03No ratings yet

- Ratha RemittancesDocument2 pagesRatha Remittancesmetrexz17.03No ratings yet

- Do010 2017Document2 pagesDo010 2017metrexz17.03No ratings yet

- What Is My Salary StructureDocument2 pagesWhat Is My Salary Structuredvenky85No ratings yet

- 2024 Tax III Module 1 Notes-1Document127 pages2024 Tax III Module 1 Notes-1katelynnewson07No ratings yet

- Sale 238 26-06-2023Document2 pagesSale 238 26-06-2023Creeper TechnologiesNo ratings yet

- Earnings Statement: SSN: XXX-XX-2691Document1 pageEarnings Statement: SSN: XXX-XX-2691emily ambrosino0% (2)

- Icaz Cta Zimtax Module 2022 EditedDocument272 pagesIcaz Cta Zimtax Module 2022 EditedAbigal Makweche100% (1)

- Subledger Accounting Implementation Guide Oracle R12Document342 pagesSubledger Accounting Implementation Guide Oracle R12RBalajiNo ratings yet

- Syllabus Mcom 2017Document9 pagesSyllabus Mcom 2017khalidNo ratings yet

- Block Credit Under GSTDocument2 pagesBlock Credit Under GSTparam.ginni100% (1)

- 1 Accounting Theory and PracticeDocument16 pages1 Accounting Theory and PracticeFirman PrasetyaNo ratings yet

- MGT480 Term PaperDocument32 pagesMGT480 Term PaperShurovi UrmiNo ratings yet

- Straight Problems Income Tax Bsa2Document2 pagesStraight Problems Income Tax Bsa2dimpy dNo ratings yet

- G. Telecoms, Inc.: Billing StatementDocument1 pageG. Telecoms, Inc.: Billing StatementJTPA LIMNo ratings yet

- Batas Pambansa Blg. 232 & Ra 10931 Report - Ana Mae SaysonDocument17 pagesBatas Pambansa Blg. 232 & Ra 10931 Report - Ana Mae SaysonAna Mae SaysonNo ratings yet

- Fatca Crs Non IndividualDocument1 pageFatca Crs Non IndividualHarsh-AgarwalNo ratings yet

- 105 Invoice (Innotronix) 22-23Document1 page105 Invoice (Innotronix) 22-23account.adminNo ratings yet

- Part-A Unit-I: Business EnvironmentDocument4 pagesPart-A Unit-I: Business EnvironmentShankar ReddyNo ratings yet

- Application of PercentDocument12 pagesApplication of PercentJericha Amparado QuinteNo ratings yet

- Tax Stamp Rps A4Document4 pagesTax Stamp Rps A4ashfaqahmadNo ratings yet

- International Financial Management Notes Unit-1Document15 pagesInternational Financial Management Notes Unit-1Geetha aptdcNo ratings yet

- Foreign Direct Investment ImperialDocument5 pagesForeign Direct Investment ImperialokiNo ratings yet

- Tax 1 Digest CompilationDocument13 pagesTax 1 Digest CompilationxyrakrezelNo ratings yet

- Multinational Companies and Its EnvironmentDocument10 pagesMultinational Companies and Its EnvironmentLoren RosariaNo ratings yet

- December 23, 2015 Tribune-PhonographDocument16 pagesDecember 23, 2015 Tribune-PhonographcwmediaNo ratings yet

- Assessment (Full) Quick RevisionDocument16 pagesAssessment (Full) Quick RevisionKush ShahNo ratings yet

- Retirement Notification FormDocument2 pagesRetirement Notification FormAbongile PhinyanaNo ratings yet

- Mutual Funds: Concept and CharacteristicsDocument179 pagesMutual Funds: Concept and CharacteristicssiddharthzalaNo ratings yet

- Filed: Form GSTR-3BDocument2 pagesFiled: Form GSTR-3Bkrishswat7912No ratings yet

- I.TAx 302Document4 pagesI.TAx 302tadepalli patanjaliNo ratings yet