Download as pdf or txt

You might also like

- Project For Taxation LawDocument11 pagesProject For Taxation Lawtanmaya guptaNo ratings yet

- Project On GSTDocument42 pagesProject On GSTMegha R57% (7)

- Anderson County Delinquent Tax SaleDocument4 pagesAnderson County Delinquent Tax SaleGreenville News100% (1)

- 269st pdf-1Document1 page269st pdf-1ajinkya.kadamandassociatesNo ratings yet

- Government of India Ministry of Finance Department of Revenue Central Board of Direct TaxesDocument2 pagesGovernment of India Ministry of Finance Department of Revenue Central Board of Direct TaxesBhan WatiNo ratings yet

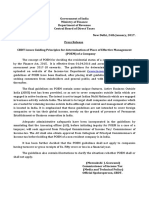

- CBDT - POEM Guidelines Press Release - January 2017Document1 pageCBDT - POEM Guidelines Press Release - January 2017bharath289No ratings yet

- Press Information Bureau Government of India Ministry of FinanceDocument3 pagesPress Information Bureau Government of India Ministry of Financekumar45caNo ratings yet

- The KnowledgeDocument13 pagesThe KnowledgeRahil AfricawalaNo ratings yet

- Canvass: Capturing News With An Analytical EdgeDocument6 pagesCanvass: Capturing News With An Analytical EdgeRanjith RoshanNo ratings yet

- Press-Release-Cbdt-Extends-Due-Date-For-Filing-Tax Audit Reports-01-11-2017Document1 pagePress-Release-Cbdt-Extends-Due-Date-For-Filing-Tax Audit Reports-01-11-2017Nithin KumarNo ratings yet

- Press Release Inclusion of Interst Income 23 03 2016Document1 pagePress Release Inclusion of Interst Income 23 03 2016Nayab PathanNo ratings yet

- 8203 Economic Environment of Business Assignment: Submitted To: DR Seema JoshiDocument7 pages8203 Economic Environment of Business Assignment: Submitted To: DR Seema JoshiKritee ManchandaNo ratings yet

- BAB I (PERPAJAKAN) - Sopian TaufikDocument10 pagesBAB I (PERPAJAKAN) - Sopian TaufikRipan saepul rohmanNo ratings yet

- Press Release Clarification On Applicability of TDS On Cash Withdrawals Dated 30-08-2019Document1 pagePress Release Clarification On Applicability of TDS On Cash Withdrawals Dated 30-08-2019Sudarshan BhangdiyaNo ratings yet

- Tax FinalDocument16 pagesTax FinalAnany UpadhyayNo ratings yet

- News Letter January 2017Document19 pagesNews Letter January 2017Sujata SinghNo ratings yet

- Hrishad - Income TaxDocument9 pagesHrishad - Income Taxkhayyum0% (1)

- Income Tax PlainingDocument57 pagesIncome Tax PlainingrohitNo ratings yet

- PressRelease Extension of Due Date of Furnishing of IITR and Audit Reports 24 10 20 PDFDocument2 pagesPressRelease Extension of Due Date of Furnishing of IITR and Audit Reports 24 10 20 PDFSaBoNo ratings yet

- The Two Sides of The BudgetDocument8 pagesThe Two Sides of The BudgetritusahrawatNo ratings yet

- Voluntary Disclosure of Black MoneyDocument6 pagesVoluntary Disclosure of Black Money777priyankaNo ratings yet

- Presentation By: Chartered Accountant No. 248, 3 Main Road, Chamrajpet, Bangalore - 560 018Document404 pagesPresentation By: Chartered Accountant No. 248, 3 Main Road, Chamrajpet, Bangalore - 560 018AATISH BANKANo ratings yet

- FINANCE (Allowances) DEPARTMENT G.O.Ms - No.6, Dated 6 January 2018Document4 pagesFINANCE (Allowances) DEPARTMENT G.O.Ms - No.6, Dated 6 January 2018vanjinathan_aNo ratings yet

- GST 2Document37 pagesGST 2jprapti317No ratings yet

- Bhs Inggris Sheren WulurDocument3 pagesBhs Inggris Sheren WulurBenediktus BaolileNo ratings yet

- Microsoft Word - 2020FIN - MS24Document1 pageMicrosoft Word - 2020FIN - MS24prakashNo ratings yet

- Analysis of The 2018 Finance BillDocument37 pagesAnalysis of The 2018 Finance BillLEENIE MUNAHNo ratings yet

- Circular No.63Document10 pagesCircular No.63Shrikant KulkarniNo ratings yet

- Central Goods and Services Tax (CGST) Rules, 2017 Part - A (Rules)Document167 pagesCentral Goods and Services Tax (CGST) Rules, 2017 Part - A (Rules)Pradeep ShahNo ratings yet

- ST TH THDocument23 pagesST TH THgaganNo ratings yet

- 01.07.2020 - CGST Rules, 2017 - (Part-A - Rules)Document163 pages01.07.2020 - CGST Rules, 2017 - (Part-A - Rules)rdabliNo ratings yet

- Group 4 - Emc PresentationDocument22 pagesGroup 4 - Emc PresentationOmkar SakpalNo ratings yet

- Press Release IDSDocument1 pagePress Release IDSElvisPresliiNo ratings yet

- PEM ReportDocument6 pagesPEM Reportxx69dd69xxNo ratings yet

- Update - Government Announcements - Fight Against COVID 19Document53 pagesUpdate - Government Announcements - Fight Against COVID 19Vaibhav JainNo ratings yet

- Press Release IDS 02 09 2016Document2 pagesPress Release IDS 02 09 2016ElvisPresliiNo ratings yet

- Khilji Co Tax Memorandum 2017 18Document47 pagesKhilji Co Tax Memorandum 2017 18Sami SattiNo ratings yet

- Government of India Ministry of Finance Department of Revenue Central Board of Direct TaxesDocument1 pageGovernment of India Ministry of Finance Department of Revenue Central Board of Direct TaxesJai ModiNo ratings yet

- Banking AwarenessDocument32 pagesBanking AwarenessArnab panditNo ratings yet

- 217 1 698 6 10 20170327Document14 pages217 1 698 6 10 20170327NiaPratiwiNo ratings yet

- Public Financial Management Assignment 02Document8 pagesPublic Financial Management Assignment 02Avishka IndulaNo ratings yet

- Finance Minister Announces Several Relief Measures Relating To Statutory and Regulatory Compliance Matters Across Sectors in View of COVIDDocument3 pagesFinance Minister Announces Several Relief Measures Relating To Statutory and Regulatory Compliance Matters Across Sectors in View of COVIDVenkataNo ratings yet

- Loksabhaquestions Annex 1712 AU2962Document10 pagesLoksabhaquestions Annex 1712 AU2962SreedevNo ratings yet

- Tax Amnesty Scheme in PakistanDocument5 pagesTax Amnesty Scheme in PakistanAadi KhanNo ratings yet

- Jamia Millia Islamia: Tax LawDocument17 pagesJamia Millia Islamia: Tax LawpriyanshuNo ratings yet

- Basic Agricultural Income, Residence Salary and DeductionsDocument75 pagesBasic Agricultural Income, Residence Salary and Deductionspiyush kumarNo ratings yet

- ABRY Scheme Guidelines Amended On 02 07 2021Document12 pagesABRY Scheme Guidelines Amended On 02 07 2021Mohit KhatriNo ratings yet

- Diskusi 4 Bahasa Inggris NiagaDocument2 pagesDiskusi 4 Bahasa Inggris NiagaRezyNa ChannelNo ratings yet

- Basis of BIR For Expiration of Receipts On June 30, 2013Document1 pageBasis of BIR For Expiration of Receipts On June 30, 2013Marita Ragus Victorino CabreraNo ratings yet

- Part-I (Indian Economy, World Economy, Defence) - UAI's Study Material On Current Affairs 2020Document87 pagesPart-I (Indian Economy, World Economy, Defence) - UAI's Study Material On Current Affairs 2020sanjusinsterNo ratings yet

- Seminar Report: Submitted in Partial Fulfillment For The Award of Degree ofDocument23 pagesSeminar Report: Submitted in Partial Fulfillment For The Award of Degree ofRahul ChhallaniNo ratings yet

- New Services Under Reverse Charge Mechanism Wef 1st January 2019 - Taxguru - inDocument4 pagesNew Services Under Reverse Charge Mechanism Wef 1st January 2019 - Taxguru - inPradeep MudiNo ratings yet

- PressRelease 22ndGSTCMeetingDocument2 pagesPressRelease 22ndGSTCMeetingShail MehtaNo ratings yet

- Press Release: Composition SchemeDocument2 pagesPress Release: Composition SchemeRojalin BiswsasNo ratings yet

- PressRelease 22ndGSTCMeeting PDFDocument2 pagesPressRelease 22ndGSTCMeeting PDFSaurabh SinghNo ratings yet

- Tax PlaningDocument78 pagesTax PlaningSahilSahoreNo ratings yet

- Case Study Study On Tools Used by Monetary Policy and Fiscal Policy in BhutanDocument12 pagesCase Study Study On Tools Used by Monetary Policy and Fiscal Policy in BhutanSonam Peldon (Business) [Cohort2020 RTC]No ratings yet

- 30.07.2020 - CGST Rules, 2017 - (Part-A - Rules)Document164 pages30.07.2020 - CGST Rules, 2017 - (Part-A - Rules)Dost BhawanaNo ratings yet

- Law of Torts Assignment "Brief Overview of Finance Ministry of India"Document5 pagesLaw of Torts Assignment "Brief Overview of Finance Ministry of India"Dsingh SinghNo ratings yet

- Business Wage: Subsidy (SBWS) ProgramDocument11 pagesBusiness Wage: Subsidy (SBWS) ProgramNANNo ratings yet

- Indonesian Taxation: for Academics and Foreign Business Practitioners Doing Business in IndonesiaFrom EverandIndonesian Taxation: for Academics and Foreign Business Practitioners Doing Business in IndonesiaNo ratings yet

- Tally Prime Exercise 3Document9 pagesTally Prime Exercise 3MohanNo ratings yet

- Apollo Medicine InvoiceOct 14 2022 23 25Document2 pagesApollo Medicine InvoiceOct 14 2022 23 25mani kandanNo ratings yet

- KIA QuotationDocument1 pageKIA Quotationshishir tiwariNo ratings yet

- CIR Vs ST LukesDocument1 pageCIR Vs ST LukesMeAnn TumbagaNo ratings yet

- Direct Tax Challan ReportDocument2 pagesDirect Tax Challan ReportVivek MurtadakNo ratings yet

- Aug 2023Document1 pageAug 2023Dheeraj yadavNo ratings yet

- RR 04-08 (Sale of RP)Document7 pagesRR 04-08 (Sale of RP)joefieNo ratings yet

- Declaration Return of Income 2015 5440019711101Document3 pagesDeclaration Return of Income 2015 5440019711101Ahlia Waqas AnjumNo ratings yet

- t1 Ovp S 15eDocument2 pagest1 Ovp S 15etstscribdNo ratings yet

- Ilovepdf MergedDocument5 pagesIlovepdf Mergedlkobharat 00No ratings yet

- Roedl Partner India GST EnglishDocument3 pagesRoedl Partner India GST EnglishPrathamesh MujumaleNo ratings yet

- Form Template Format Slip Gaji Karyawan Swasta Sederhana Dalam ExcelDocument1 pageForm Template Format Slip Gaji Karyawan Swasta Sederhana Dalam ExcelGita RahmayaniNo ratings yet

- Indian Income Tax Return Acknowledgement 2021-22: Assessment YearDocument1 pageIndian Income Tax Return Acknowledgement 2021-22: Assessment YearRaveendra MoodithayaNo ratings yet

- Salary SlipDocument1 pageSalary SlipPhagun BehlNo ratings yet

- EE - Assignment Chapter 7 SolutionDocument7 pagesEE - Assignment Chapter 7 SolutionXuân ThànhNo ratings yet

- Application Instructions For PETRONAS Powering Knowledge Education Sponsorship - Mid Education 2024 2Document16 pagesApplication Instructions For PETRONAS Powering Knowledge Education Sponsorship - Mid Education 2024 2Mohankummar MuniandyNo ratings yet

- Tax Invoice: Thyssenkrupp Elevator (India) Pvt. LTDDocument1 pageTax Invoice: Thyssenkrupp Elevator (India) Pvt. LTDgajendrabanshiwal8905No ratings yet

- Earnings Statement: Non-NegotiableDocument1 pageEarnings Statement: Non-NegotiableAnthony JohnsonNo ratings yet

- 3 BMW Motorrad Price March 2021.PDF - Asset.1616655326065Document2 pages3 BMW Motorrad Price March 2021.PDF - Asset.1616655326065AnilNo ratings yet

- XtolDocument2 pagesXtolsujal JainNo ratings yet

- Tax Declaration SampleDocument1 pageTax Declaration SampleLara De los Santos100% (1)

- CTC Structure Jan DemoDocument4 pagesCTC Structure Jan DemoPrashant BedaseNo ratings yet

- Uma Devi Jan PayslipDocument1 pageUma Devi Jan PayslipThivagaran NagapanNo ratings yet

- Gutierrez v. CIR - SubaDocument1 pageGutierrez v. CIR - SubaPaul Joshua SubaNo ratings yet

- Hallmark Projects: Project - Hallmark Vicinia Apartments at NarsingiDocument1 pageHallmark Projects: Project - Hallmark Vicinia Apartments at Narsingikrishna TejaNo ratings yet

- TX-UK and ATX-UK - FA 2020 Exam Docs June 21 To March 22 - FinalDocument7 pagesTX-UK and ATX-UK - FA 2020 Exam Docs June 21 To March 22 - FinalRidwan AhmedNo ratings yet

- It PPT For F.Y 2023-24Document24 pagesIt PPT For F.Y 2023-24iampnkjjnNo ratings yet

- Flipkart Labels 23 Aug 2021 04 16Document42 pagesFlipkart Labels 23 Aug 2021 04 16Sudip SenNo ratings yet

- Sep Pay SlipDocument1 pageSep Pay SlipNN DINESHKUMARNo ratings yet