Download as pdf or txt

You might also like

- Westpac Choice: 03 March 2021 - 01 April 2021Document3 pagesWestpac Choice: 03 March 2021 - 01 April 2021Wenjie65No ratings yet

- World Quant AssignmentDocument11 pagesWorld Quant AssignmentAditya NalluriNo ratings yet

- KFCDocument208 pagesKFCAsHiya MiZuki50% (2)

- Prudential RegulationsDocument11 pagesPrudential RegulationsBishnu DhamalaNo ratings yet

- Bank RegulationDocument11 pagesBank RegulationGrace GarnerNo ratings yet

- Unit 2 Capital MarketDocument36 pagesUnit 2 Capital Marketshree ram prasad sahaNo ratings yet

- Key Notes To NRB ActDocument9 pagesKey Notes To NRB Actdevi ghimireNo ratings yet

- Ar 2008 FinacialoverviewDocument78 pagesAr 2008 FinacialoverviewRiaz TreynoldsNo ratings yet

- JP Morgan Chase & Co.: Abhinav Kumar Singh Simsree PGDBM-855Document25 pagesJP Morgan Chase & Co.: Abhinav Kumar Singh Simsree PGDBM-855api-19592137No ratings yet

- AFMSDocument169 pagesAFMSJAGRITI SINGH JUNo ratings yet

- Macro Economics: Computation of National IncomeDocument20 pagesMacro Economics: Computation of National IncomeAnoop MohantyNo ratings yet

- BAFIA FOR RBB Bank CLassDocument29 pagesBAFIA FOR RBB Bank CLassDagendra BasnetNo ratings yet

- Regulation 2023Document24 pagesRegulation 2023Richa ChauhanNo ratings yet

- KUPres 7 Nov 2010Document63 pagesKUPres 7 Nov 2010Hasan Irfan SiddiquiNo ratings yet

- Standalone Financial Results, Limited Review Report For September 30, 2016 (Result)Document4 pagesStandalone Financial Results, Limited Review Report For September 30, 2016 (Result)Shyam SunderNo ratings yet

- SEBI Act, 1992Document26 pagesSEBI Act, 1992saif aliNo ratings yet

- Financial Services 1Document21 pagesFinancial Services 1JEFFERSON OPSIMANo ratings yet

- About SEBI Establishment of Sebi: Securities and Exchange Board of India ActDocument17 pagesAbout SEBI Establishment of Sebi: Securities and Exchange Board of India ActFaraaz HasnainNo ratings yet

- Peso Starter Fund Prospectus - 082321Document61 pagesPeso Starter Fund Prospectus - 082321John Bernard VillarosaNo ratings yet

- Refinancing Savings Round 2: Frasers Commercial TrustDocument5 pagesRefinancing Savings Round 2: Frasers Commercial Trustcentaurus553587No ratings yet

- Ifsa 3Document36 pagesIfsa 3Avinash DasNo ratings yet

- The Securities and ExchangeDocument22 pagesThe Securities and ExchangeHappy AnthalNo ratings yet

- The Securities and Exchange Board of India (SEBI)Document33 pagesThe Securities and Exchange Board of India (SEBI)kharyarajulNo ratings yet

- Bank Regulation: Citations VerificationDocument5 pagesBank Regulation: Citations Verificationsbajaj23No ratings yet

- Finances em 2Document3 pagesFinances em 2Craaft NishiNo ratings yet

- Odey Int'l FundDocument48 pagesOdey Int'l FundcogitatorNo ratings yet

- 51 - 11219525 - Nguyễn Đỗ Thủy TiênDocument44 pages51 - 11219525 - Nguyễn Đỗ Thủy TiênThủy Tiên Nguyễn ĐỗNo ratings yet

- Ø Need For Sebi Ø Purpose of The Sebi Act 1992 Ø ManagementDocument18 pagesØ Need For Sebi Ø Purpose of The Sebi Act 1992 Ø Managementarun666No ratings yet

- Sacco Societies Act 14 of 2008Document37 pagesSacco Societies Act 14 of 2008opulitheNo ratings yet

- Central BankDocument56 pagesCentral BankSweekar HamalNo ratings yet

- Investment Banking Marshal Chapter 2Document52 pagesInvestment Banking Marshal Chapter 2ObydulRanaNo ratings yet

- BR Act 1949Document25 pagesBR Act 1949dranita@yahoo.comNo ratings yet

- Revised Code of Practices and Procedures For Fair Disclosure (Company Update)Document11 pagesRevised Code of Practices and Procedures For Fair Disclosure (Company Update)Shyam SunderNo ratings yet

- Article tSEBON-NewsletterDocument5 pagesArticle tSEBON-Newsletterparvez ansariNo ratings yet

- Rough GPDocument261 pagesRough GPPavan ShahNo ratings yet

- Capitec Interim2004Document1 pageCapitec Interim2004naeemrencapNo ratings yet

- IGNOU MBA MS - 04 Solved Assignment 2011Document12 pagesIGNOU MBA MS - 04 Solved Assignment 2011Nazif LcNo ratings yet

- 13 - Chapter 4Document24 pages13 - Chapter 4touffiqNo ratings yet

- Starhill Global REIT Ending 1Q14 On High NoteDocument6 pagesStarhill Global REIT Ending 1Q14 On High NoteventriaNo ratings yet

- Fuidamental AnalysisDocument3 pagesFuidamental AnalysisPrashant MujumdarNo ratings yet

- Insurance RegulationDocument186 pagesInsurance RegulationVaibhav ChudasamaNo ratings yet

- Placement Training Centre Bank Interview Questions and AnswersDocument20 pagesPlacement Training Centre Bank Interview Questions and AnswershariNo ratings yet

- 2019 인도네시아 - 진출전략 PDFDocument79 pages2019 인도네시아 - 진출전략 PDFKelly LaNo ratings yet

- Goodpack LTDDocument3 pagesGoodpack LTDventriaNo ratings yet

- The Omnibus Investments Code of 1987Document13 pagesThe Omnibus Investments Code of 1987rheyneNo ratings yet

- 2008 Hanbook IAPS 1006Document90 pages2008 Hanbook IAPS 1006Vivienne BeverNo ratings yet

- University Budget IDocument21 pagesUniversity Budget ICullen DonohueNo ratings yet

- ACCT 860: Financial Accounting Week 1: NZ External Reporting EnvironmentDocument36 pagesACCT 860: Financial Accounting Week 1: NZ External Reporting EnvironmentNam PhamNo ratings yet

- Fidelity South-East Asia Fund, A Sub-Fund of Fidelity Investment Funds, A Accumulation Shares (ISIN: GB0003879185)Document2 pagesFidelity South-East Asia Fund, A Sub-Fund of Fidelity Investment Funds, A Accumulation Shares (ISIN: GB0003879185)Nais BNo ratings yet

- Mkopo SACCO Reporting TemplateDocument45 pagesMkopo SACCO Reporting TemplateebanfaNo ratings yet

- IGNOU MBA MS - 04 Solved Assignment 2011Document16 pagesIGNOU MBA MS - 04 Solved Assignment 2011Kiran PattnaikNo ratings yet

- Introduction To Financial Accounting ProjectDocument12 pagesIntroduction To Financial Accounting ProjectYannick HarveyNo ratings yet

- 2008 13 Financial Statements Samsung 2007Document26 pages2008 13 Financial Statements Samsung 2007Wilson Edilber ValenciaNo ratings yet

- Securities and Exchange Board of IndiaDocument57 pagesSecurities and Exchange Board of IndiaTanay Kumar SinghNo ratings yet

- PD 1752-Amending The Act Creating The HDMF PDFDocument6 pagesPD 1752-Amending The Act Creating The HDMF PDFMousy GamalloNo ratings yet

- SEBI Role & FunctionsDocument27 pagesSEBI Role & FunctionsGayatri MhalsekarNo ratings yet

- Module 1.2 Regulatory FrameworkDocument28 pagesModule 1.2 Regulatory FrameworksateeshjorliNo ratings yet

- Investment Evaluation: Professor Tim Thompson Kellogg School of ManagementDocument36 pagesInvestment Evaluation: Professor Tim Thompson Kellogg School of ManagementAmund BremerNo ratings yet

- Importance, Challenges, and Financial Sector Reforms: CS Rakesh Chawla 9873302122Document26 pagesImportance, Challenges, and Financial Sector Reforms: CS Rakesh Chawla 9873302122Kunal GuptaNo ratings yet

- Funds AnalysisDocument21 pagesFunds AnalysisvvkmassNo ratings yet

- CH3 - Financial Report StandardsDocument38 pagesCH3 - Financial Report StandardsStudent Sokha ChanchesdaNo ratings yet

- How to Retire Early on Dividends: Dividend Growth Machine: Mastering the Art of Maximizing Returns Through Dividend InvestingFrom EverandHow to Retire Early on Dividends: Dividend Growth Machine: Mastering the Art of Maximizing Returns Through Dividend InvestingNo ratings yet

- Ordinary Annuity ModuleDocument27 pagesOrdinary Annuity ModuleVincent Andrei Dela CruzNo ratings yet

- Mhban01256350000013286 2015Document1 pageMhban01256350000013286 2015katiyar81No ratings yet

- New KRUTESH TANDEL PROJECT 2Document99 pagesNew KRUTESH TANDEL PROJECT 2Harshal ThakurNo ratings yet

- Customer Financing Application PDFDocument7 pagesCustomer Financing Application PDFAlvin PhuongNo ratings yet

- Pami Dua Monetary PolicyDocument38 pagesPami Dua Monetary PolicyIshika KumariNo ratings yet

- Lender ListDocument1 pageLender ListKrist LlöydNo ratings yet

- Sanction LetterDocument3 pagesSanction LetterDipak BagadeNo ratings yet

- Capital Gains Group F6Document2 pagesCapital Gains Group F6Wajih RehmanNo ratings yet

- SAPNA ExpensesDocument1 pageSAPNA ExpensesramudadaNo ratings yet

- Class 8 Chapter 15 Compound Interest Exercise 15b DownloadDocument4 pagesClass 8 Chapter 15 Compound Interest Exercise 15b DownloadSikander KhanNo ratings yet

- Simple Annuity 1Document13 pagesSimple Annuity 1Kelvin BarceLon0% (1)

- 1Document5 pages1firoozdasmanNo ratings yet

- Kelly 2020Document2 pagesKelly 2020Cheryl MajeskiNo ratings yet

- Utkarsh: Smatl Finance Bank AugustDocument2 pagesUtkarsh: Smatl Finance Bank AugustGamer JiNo ratings yet

- Draft Jeevan AnkurDocument17 pagesDraft Jeevan AnkurShekhar RakheNo ratings yet

- NPS Transaction Statement For Tier I Account: Current Scheme PreferenceDocument4 pagesNPS Transaction Statement For Tier I Account: Current Scheme PreferencerahulNo ratings yet

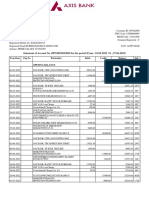

- Icici Bank StatementDocument20 pagesIcici Bank Statementsatishsingh0171No ratings yet

- Tool Test 2023 Aug Middle East - Seema - DataDocument1 pageTool Test 2023 Aug Middle East - Seema - DataMohammad AslamNo ratings yet

- LoanApplication 23660000180829Document12 pagesLoanApplication 23660000180829vijaybhaskar damireddyNo ratings yet

- BANK UnlockedDocument6 pagesBANK UnlockedRaghav Sharma100% (1)

- Tata Business Support Services LTD: 00110283 KhushbuDocument1 pageTata Business Support Services LTD: 00110283 KhushbuKhushbu SinghNo ratings yet

- Credit Analysis Procedure Applied by Bank of India For Agriculture LendingDocument28 pagesCredit Analysis Procedure Applied by Bank of India For Agriculture LendingNaveen KumarNo ratings yet

- Opening Case Corporate GovernanceDocument2 pagesOpening Case Corporate GovernanceSandyNo ratings yet

- D6.1 - LawDocument2 pagesD6.1 - LawAngelica DeniseNo ratings yet

- Pdic LawDocument5 pagesPdic LawDiaz, Bryan ChristopherNo ratings yet

- Cashflow Without RentalsDocument17 pagesCashflow Without RentalsSadegh SimorghNo ratings yet

- Chapter 2 Bank ReconciliationDocument5 pagesChapter 2 Bank ReconciliationNicka NavarroNo ratings yet

- VOUCHERDocument1 pageVOUCHERYou first MdciNo ratings yet