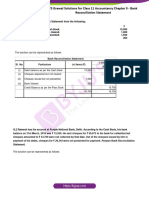

Brs Practical Questions

Brs Practical Questions

You might also like

- Auditing Concept Problems Cash and Cash EquivalentDocument7 pagesAuditing Concept Problems Cash and Cash EquivalentJoanah TayamenNo ratings yet

- Escape From Portsrood Forest ExtrasDocument5 pagesEscape From Portsrood Forest ExtrasSteveNo ratings yet

- MOD 03 - Bank ReconDocument3 pagesMOD 03 - Bank ReconIrish VargasNo ratings yet

- Computerised Accounting Practice Set Using MYOB AccountRight - Advanced Level: Australian EditionFrom EverandComputerised Accounting Practice Set Using MYOB AccountRight - Advanced Level: Australian EditionNo ratings yet

- BRS PDFDocument14 pagesBRS PDFGautam KhanwaniNo ratings yet

- Additional Practical Problems-13-1Document5 pagesAdditional Practical Problems-13-1sharmaarmaan103No ratings yet

- BRS ProblemsDocument28 pagesBRS ProblemsKutbuddin JawadwalaNo ratings yet

- Adobe Scan 05 Jan 2024Document2 pagesAdobe Scan 05 Jan 2024Harshit GargNo ratings yet

- Adobe Scan Apr 10, 2023Document12 pagesAdobe Scan Apr 10, 2023ineshbanerjee80No ratings yet

- Accountancy XI: Pankaj Rajan 9810194206Document4 pagesAccountancy XI: Pankaj Rajan 9810194206A4S ARMY Akshdeep singhNo ratings yet

- Bank Reconciliation StatementDocument13 pagesBank Reconciliation Statement20232024s5r14leungjacobNo ratings yet

- WS - Xi BRS - 2Document5 pagesWS - Xi BRS - 2richshivamshahNo ratings yet

- Chapter 9 - Bank Reconciliation StatementDocument15 pagesChapter 9 - Bank Reconciliation StatementSaurabh GohanNo ratings yet

- Worksheet BRSDocument2 pagesWorksheet BRSCA Chhavi Gupta100% (1)

- Practice With MT - BRSDocument6 pagesPractice With MT - BRSsrushtibhawsar07No ratings yet

- 6 BRS 08-2023 RegularDocument7 pages6 BRS 08-2023 RegularjahnaviNo ratings yet

- Prepare Bank Reconciliation Statement From The Following: (I) Debit Balance As Per The Cash BookDocument10 pagesPrepare Bank Reconciliation Statement From The Following: (I) Debit Balance As Per The Cash BookPragya ShuklaNo ratings yet

- BRS Class 11Document1 pageBRS Class 11tarun aroraNo ratings yet

- Ts Grewal Solutions For Class 11 Accountancy Chapter 9 BankDocument34 pagesTs Grewal Solutions For Class 11 Accountancy Chapter 9 Bankmyankjindal9No ratings yet

- Adobe Scan 5 Oct 2023Document2 pagesAdobe Scan 5 Oct 2023pushbindersingh9No ratings yet

- Dkgoel BRS 11Document15 pagesDkgoel BRS 11DhruvNo ratings yet

- Bank Reconciliaton Statement Practice Questions: ST ST STDocument2 pagesBank Reconciliaton Statement Practice Questions: ST ST STHuma SamuelNo ratings yet

- 0c26dbank Reconciliation Statement Practice QuestionsDocument2 pages0c26dbank Reconciliation Statement Practice QuestionsRahul AgarwalNo ratings yet

- Bank Reconciliation StatementDocument33 pagesBank Reconciliation StatementMd TahirNo ratings yet

- Tsgrewal BRSDocument11 pagesTsgrewal BRSDhruvNo ratings yet

- Assignment BRSDocument2 pagesAssignment BRSveydantsharma42No ratings yet

- BRS PDFDocument8 pagesBRS PDFAnshumanNo ratings yet

- 1 Accounting For CashDocument1 page1 Accounting For CashAir CrlsNo ratings yet

- Cannon Ball Review With Exercises Part 2 PDFDocument30 pagesCannon Ball Review With Exercises Part 2 PDFLayNo ratings yet

- CA F BRS WithDocument10 pagesCA F BRS WithG. DhanyaNo ratings yet

- Bank Reconciliation Statement Practice ProblemsDocument2 pagesBank Reconciliation Statement Practice ProblemsHaya DanishNo ratings yet

- Handout - Cash and Cash EquivalentsDocument5 pagesHandout - Cash and Cash Equivalentsandrea arapocNo ratings yet

- Cash N Cash Equivalent Problem Set 1Document3 pagesCash N Cash Equivalent Problem Set 1Jamaica DavidNo ratings yet

- B.R.S. Test 3Document5 pagesB.R.S. Test 3Sudhir SinhaNo ratings yet

- Proof of Cash - Sample ProblemsDocument1 pageProof of Cash - Sample ProblemsFucio, Mark JeroldNo ratings yet

- Problem SolvingDocument4 pagesProblem SolvingsunflowerNo ratings yet

- Cce Board WorkDocument3 pagesCce Board WorkNicole VinaraoNo ratings yet

- 21Document10 pages21aroranavdishNo ratings yet

- Practical - Bank Reconciliation StatementDocument5 pagesPractical - Bank Reconciliation StatementUniversal SoldierNo ratings yet

- Quiz 1Document3 pagesQuiz 1Carmi FeceroNo ratings yet

- 16772BRSDocument47 pages16772BRSSketch KathayatNo ratings yet

- 06 BRS - Practice QuestionsDocument1 page06 BRS - Practice QuestionsNeelanjana RayNo ratings yet

- Name: Section: Date:: PROBLEM NO. 1 (2pts)Document2 pagesName: Section: Date:: PROBLEM NO. 1 (2pts)Joovs JoovhoNo ratings yet

- Quiz 1 - Audit of CashDocument4 pagesQuiz 1 - Audit of CashmillescaasiNo ratings yet

- Test Aldine FinalDocument3 pagesTest Aldine FinalAkshay TulshyanNo ratings yet

- FA - Bank Rec. QuestionDocument2 pagesFA - Bank Rec. QuestionAshika JayaweeraNo ratings yet

- F005 Test 5 StudentsDocument6 pagesF005 Test 5 StudentsbhumikaaNo ratings yet

- Additional Illustrations-13Document5 pagesAdditional Illustrations-13Deepak YadavNo ratings yet

- Bank Reconciliation StatementDocument12 pagesBank Reconciliation StatementBhuvan PrajapatiNo ratings yet

- Composition of Cash Petty CashDocument7 pagesComposition of Cash Petty CashRyou ShinodaNo ratings yet

- Brs Practise SheetDocument1 pageBrs Practise Sheetapi-252642432No ratings yet

- Problem 7 - 16Document2 pagesProblem 7 - 16Jao FloresNo ratings yet

- Assignment On Chapter 5 Cash Ad ReceivablesDocument3 pagesAssignment On Chapter 5 Cash Ad Receivablesdameregasa08No ratings yet

- 1 - Cash & ReceivablesDocument7 pages1 - Cash & ReceivablesCharielle Esthelin BacuganNo ratings yet

- Bank Recon & Proof-Set ADocument2 pagesBank Recon & Proof-Set AJaypee BignoNo ratings yet

- Cash and Cash Equivalent LatestDocument54 pagesCash and Cash Equivalent LatestSafe PlaceNo ratings yet

- Encode JobDocument12 pagesEncode JobRainNo ratings yet

- Practice Set: Page 5 of 7Document3 pagesPractice Set: Page 5 of 7darren sanchezNo ratings yet

- Cash and Cash Equivalent LatestDocument53 pagesCash and Cash Equivalent LatestxagocipNo ratings yet

- BRS WorksheetDocument8 pagesBRS WorksheetMayank VermaNo ratings yet

- ProblemsDocument28 pagesProblemsYou Knock On My DoorNo ratings yet

- BS en 124 1994 PDFDocument16 pagesBS en 124 1994 PDFThupten Gedun Kelvin OngNo ratings yet

- Cosmetics OverviewDocument6 pagesCosmetics OverviewKena SamuelNo ratings yet

- See, Verdict/article23325591.eceDocument1 pageSee, Verdict/article23325591.ecevetrivelNo ratings yet

- Heroic AgencyDocument17 pagesHeroic AgencyAlex TurvyNo ratings yet

- Uardian: Angry BlunderDocument62 pagesUardian: Angry BlunderAlejandro MarinNo ratings yet

- Lecture Notes Taxation 1 Atty. Arnel A. Dela Rosa, CPA, REB, READocument31 pagesLecture Notes Taxation 1 Atty. Arnel A. Dela Rosa, CPA, REB, REAweewoouwu100% (1)

- Rental AgreementDocument2 pagesRental AgreementVillar MitchiNo ratings yet

- 2023 09 enDocument84 pages2023 09 enShobhit MauryaNo ratings yet

- Name of The Work:-Agreement No.: - T/94/EE/BD/PWD/BLN/B/2010-11. Name of Agency: - Sri Biplab Kr. GhoshDocument24 pagesName of The Work:-Agreement No.: - T/94/EE/BD/PWD/BLN/B/2010-11. Name of Agency: - Sri Biplab Kr. Ghoshdebashish sarkarNo ratings yet

- Unit 3 Cultural Issues and Values Exercises 10Document2 pagesUnit 3 Cultural Issues and Values Exercises 10ACHRAF DOUKARNENo ratings yet

- Transport MCQ AnswerDocument3 pagesTransport MCQ AnswerManas RanjanNo ratings yet

- Summer Breeze Strandnet enDocument19 pagesSummer Breeze Strandnet enPersfektif YansimaNo ratings yet

- PT Vloowless Kosmetik Indonesia PayslipDocument1 pagePT Vloowless Kosmetik Indonesia PayslipZyka OediNo ratings yet

- Section 8 - Due Diligence: DD/08: Pest Control and ReportingDocument2 pagesSection 8 - Due Diligence: DD/08: Pest Control and Reportingmuhammed asharudheenNo ratings yet

- The Historical Evolution of Highly Qualified Migrations: C.brandi@irpps - Cnr.itDocument18 pagesThe Historical Evolution of Highly Qualified Migrations: C.brandi@irpps - Cnr.itamayalibelulaNo ratings yet

- Cardex Home VisitationDocument2 pagesCardex Home VisitationCrisel NombilaNo ratings yet

- What Are The Modes of Winding Up of The CompaniesDocument3 pagesWhat Are The Modes of Winding Up of The CompaniesMahesh SNo ratings yet

- Rule 13 Case 19 Mendoza Vs CADocument2 pagesRule 13 Case 19 Mendoza Vs CAErwin BernardinoNo ratings yet

- ST TH: Ordinance No. 28, Series of 2017Document20 pagesST TH: Ordinance No. 28, Series of 2017Marites TaniegraNo ratings yet

- Pinellas County Sheriff's Amicus Brief in Mary's Law CaseDocument6 pagesPinellas County Sheriff's Amicus Brief in Mary's Law CaseWCTV Digital TeamNo ratings yet

- CASE NO. 114 Itogon-Suyoc Mines, Inc, v. Sangilo-Itogon Workers' Union in Behalf of Bartolome Mayo, Bernardo Aquino, Et. Al.Document7 pagesCASE NO. 114 Itogon-Suyoc Mines, Inc, v. Sangilo-Itogon Workers' Union in Behalf of Bartolome Mayo, Bernardo Aquino, Et. Al.kaizen shinichiNo ratings yet

- Data KHDocument37 pagesData KHHạnh DungNo ratings yet

- H02 - Taxes, Tax Laws and Tax AdministrationDocument10 pagesH02 - Taxes, Tax Laws and Tax Administrationnona galido100% (1)

- Property Rights PDFDocument15 pagesProperty Rights PDFbillsNo ratings yet

- Democratic SocialismDocument11 pagesDemocratic SocialismSuhani SinghNo ratings yet

- Mini Magic 6Document67 pagesMini Magic 6Venkat krishna100% (1)

- Easa Ad 2023-0009 1Document5 pagesEasa Ad 2023-0009 1Christian BruneauNo ratings yet

- PE.2019-20.0074 - Thunga HospitalDocument4 pagesPE.2019-20.0074 - Thunga HospitalAnonymous vFrxVNNo ratings yet

- Sources of International LawDocument3 pagesSources of International LawTrisha Emerlyn SantiaguelNo ratings yet

Download as pdf or txt

You might also like

- Auditing Concept Problems Cash and Cash EquivalentDocument7 pagesAuditing Concept Problems Cash and Cash EquivalentJoanah TayamenNo ratings yet

- Escape From Portsrood Forest ExtrasDocument5 pagesEscape From Portsrood Forest ExtrasSteveNo ratings yet

- MOD 03 - Bank ReconDocument3 pagesMOD 03 - Bank ReconIrish VargasNo ratings yet

- Computerised Accounting Practice Set Using MYOB AccountRight - Advanced Level: Australian EditionFrom EverandComputerised Accounting Practice Set Using MYOB AccountRight - Advanced Level: Australian EditionNo ratings yet

- BRS PDFDocument14 pagesBRS PDFGautam KhanwaniNo ratings yet

- Additional Practical Problems-13-1Document5 pagesAdditional Practical Problems-13-1sharmaarmaan103No ratings yet

- BRS ProblemsDocument28 pagesBRS ProblemsKutbuddin JawadwalaNo ratings yet

- Adobe Scan 05 Jan 2024Document2 pagesAdobe Scan 05 Jan 2024Harshit GargNo ratings yet

- Adobe Scan Apr 10, 2023Document12 pagesAdobe Scan Apr 10, 2023ineshbanerjee80No ratings yet

- Accountancy XI: Pankaj Rajan 9810194206Document4 pagesAccountancy XI: Pankaj Rajan 9810194206A4S ARMY Akshdeep singhNo ratings yet

- Bank Reconciliation StatementDocument13 pagesBank Reconciliation Statement20232024s5r14leungjacobNo ratings yet

- WS - Xi BRS - 2Document5 pagesWS - Xi BRS - 2richshivamshahNo ratings yet

- Chapter 9 - Bank Reconciliation StatementDocument15 pagesChapter 9 - Bank Reconciliation StatementSaurabh GohanNo ratings yet

- Worksheet BRSDocument2 pagesWorksheet BRSCA Chhavi Gupta100% (1)

- Practice With MT - BRSDocument6 pagesPractice With MT - BRSsrushtibhawsar07No ratings yet

- 6 BRS 08-2023 RegularDocument7 pages6 BRS 08-2023 RegularjahnaviNo ratings yet

- Prepare Bank Reconciliation Statement From The Following: (I) Debit Balance As Per The Cash BookDocument10 pagesPrepare Bank Reconciliation Statement From The Following: (I) Debit Balance As Per The Cash BookPragya ShuklaNo ratings yet

- BRS Class 11Document1 pageBRS Class 11tarun aroraNo ratings yet

- Ts Grewal Solutions For Class 11 Accountancy Chapter 9 BankDocument34 pagesTs Grewal Solutions For Class 11 Accountancy Chapter 9 Bankmyankjindal9No ratings yet

- Adobe Scan 5 Oct 2023Document2 pagesAdobe Scan 5 Oct 2023pushbindersingh9No ratings yet

- Dkgoel BRS 11Document15 pagesDkgoel BRS 11DhruvNo ratings yet

- Bank Reconciliaton Statement Practice Questions: ST ST STDocument2 pagesBank Reconciliaton Statement Practice Questions: ST ST STHuma SamuelNo ratings yet

- 0c26dbank Reconciliation Statement Practice QuestionsDocument2 pages0c26dbank Reconciliation Statement Practice QuestionsRahul AgarwalNo ratings yet

- Bank Reconciliation StatementDocument33 pagesBank Reconciliation StatementMd TahirNo ratings yet

- Tsgrewal BRSDocument11 pagesTsgrewal BRSDhruvNo ratings yet

- Assignment BRSDocument2 pagesAssignment BRSveydantsharma42No ratings yet

- BRS PDFDocument8 pagesBRS PDFAnshumanNo ratings yet

- 1 Accounting For CashDocument1 page1 Accounting For CashAir CrlsNo ratings yet

- Cannon Ball Review With Exercises Part 2 PDFDocument30 pagesCannon Ball Review With Exercises Part 2 PDFLayNo ratings yet

- CA F BRS WithDocument10 pagesCA F BRS WithG. DhanyaNo ratings yet

- Bank Reconciliation Statement Practice ProblemsDocument2 pagesBank Reconciliation Statement Practice ProblemsHaya DanishNo ratings yet

- Handout - Cash and Cash EquivalentsDocument5 pagesHandout - Cash and Cash Equivalentsandrea arapocNo ratings yet

- Cash N Cash Equivalent Problem Set 1Document3 pagesCash N Cash Equivalent Problem Set 1Jamaica DavidNo ratings yet

- B.R.S. Test 3Document5 pagesB.R.S. Test 3Sudhir SinhaNo ratings yet

- Proof of Cash - Sample ProblemsDocument1 pageProof of Cash - Sample ProblemsFucio, Mark JeroldNo ratings yet

- Problem SolvingDocument4 pagesProblem SolvingsunflowerNo ratings yet

- Cce Board WorkDocument3 pagesCce Board WorkNicole VinaraoNo ratings yet

- 21Document10 pages21aroranavdishNo ratings yet

- Practical - Bank Reconciliation StatementDocument5 pagesPractical - Bank Reconciliation StatementUniversal SoldierNo ratings yet

- Quiz 1Document3 pagesQuiz 1Carmi FeceroNo ratings yet

- 16772BRSDocument47 pages16772BRSSketch KathayatNo ratings yet

- 06 BRS - Practice QuestionsDocument1 page06 BRS - Practice QuestionsNeelanjana RayNo ratings yet

- Name: Section: Date:: PROBLEM NO. 1 (2pts)Document2 pagesName: Section: Date:: PROBLEM NO. 1 (2pts)Joovs JoovhoNo ratings yet

- Quiz 1 - Audit of CashDocument4 pagesQuiz 1 - Audit of CashmillescaasiNo ratings yet

- Test Aldine FinalDocument3 pagesTest Aldine FinalAkshay TulshyanNo ratings yet

- FA - Bank Rec. QuestionDocument2 pagesFA - Bank Rec. QuestionAshika JayaweeraNo ratings yet

- F005 Test 5 StudentsDocument6 pagesF005 Test 5 StudentsbhumikaaNo ratings yet

- Additional Illustrations-13Document5 pagesAdditional Illustrations-13Deepak YadavNo ratings yet

- Bank Reconciliation StatementDocument12 pagesBank Reconciliation StatementBhuvan PrajapatiNo ratings yet

- Composition of Cash Petty CashDocument7 pagesComposition of Cash Petty CashRyou ShinodaNo ratings yet

- Brs Practise SheetDocument1 pageBrs Practise Sheetapi-252642432No ratings yet

- Problem 7 - 16Document2 pagesProblem 7 - 16Jao FloresNo ratings yet

- Assignment On Chapter 5 Cash Ad ReceivablesDocument3 pagesAssignment On Chapter 5 Cash Ad Receivablesdameregasa08No ratings yet

- 1 - Cash & ReceivablesDocument7 pages1 - Cash & ReceivablesCharielle Esthelin BacuganNo ratings yet

- Bank Recon & Proof-Set ADocument2 pagesBank Recon & Proof-Set AJaypee BignoNo ratings yet

- Cash and Cash Equivalent LatestDocument54 pagesCash and Cash Equivalent LatestSafe PlaceNo ratings yet

- Encode JobDocument12 pagesEncode JobRainNo ratings yet

- Practice Set: Page 5 of 7Document3 pagesPractice Set: Page 5 of 7darren sanchezNo ratings yet

- Cash and Cash Equivalent LatestDocument53 pagesCash and Cash Equivalent LatestxagocipNo ratings yet

- BRS WorksheetDocument8 pagesBRS WorksheetMayank VermaNo ratings yet

- ProblemsDocument28 pagesProblemsYou Knock On My DoorNo ratings yet

- BS en 124 1994 PDFDocument16 pagesBS en 124 1994 PDFThupten Gedun Kelvin OngNo ratings yet

- Cosmetics OverviewDocument6 pagesCosmetics OverviewKena SamuelNo ratings yet

- See, Verdict/article23325591.eceDocument1 pageSee, Verdict/article23325591.ecevetrivelNo ratings yet

- Heroic AgencyDocument17 pagesHeroic AgencyAlex TurvyNo ratings yet

- Uardian: Angry BlunderDocument62 pagesUardian: Angry BlunderAlejandro MarinNo ratings yet

- Lecture Notes Taxation 1 Atty. Arnel A. Dela Rosa, CPA, REB, READocument31 pagesLecture Notes Taxation 1 Atty. Arnel A. Dela Rosa, CPA, REB, REAweewoouwu100% (1)

- Rental AgreementDocument2 pagesRental AgreementVillar MitchiNo ratings yet

- 2023 09 enDocument84 pages2023 09 enShobhit MauryaNo ratings yet

- Name of The Work:-Agreement No.: - T/94/EE/BD/PWD/BLN/B/2010-11. Name of Agency: - Sri Biplab Kr. GhoshDocument24 pagesName of The Work:-Agreement No.: - T/94/EE/BD/PWD/BLN/B/2010-11. Name of Agency: - Sri Biplab Kr. Ghoshdebashish sarkarNo ratings yet

- Unit 3 Cultural Issues and Values Exercises 10Document2 pagesUnit 3 Cultural Issues and Values Exercises 10ACHRAF DOUKARNENo ratings yet

- Transport MCQ AnswerDocument3 pagesTransport MCQ AnswerManas RanjanNo ratings yet

- Summer Breeze Strandnet enDocument19 pagesSummer Breeze Strandnet enPersfektif YansimaNo ratings yet

- PT Vloowless Kosmetik Indonesia PayslipDocument1 pagePT Vloowless Kosmetik Indonesia PayslipZyka OediNo ratings yet

- Section 8 - Due Diligence: DD/08: Pest Control and ReportingDocument2 pagesSection 8 - Due Diligence: DD/08: Pest Control and Reportingmuhammed asharudheenNo ratings yet

- The Historical Evolution of Highly Qualified Migrations: C.brandi@irpps - Cnr.itDocument18 pagesThe Historical Evolution of Highly Qualified Migrations: C.brandi@irpps - Cnr.itamayalibelulaNo ratings yet

- Cardex Home VisitationDocument2 pagesCardex Home VisitationCrisel NombilaNo ratings yet

- What Are The Modes of Winding Up of The CompaniesDocument3 pagesWhat Are The Modes of Winding Up of The CompaniesMahesh SNo ratings yet

- Rule 13 Case 19 Mendoza Vs CADocument2 pagesRule 13 Case 19 Mendoza Vs CAErwin BernardinoNo ratings yet

- ST TH: Ordinance No. 28, Series of 2017Document20 pagesST TH: Ordinance No. 28, Series of 2017Marites TaniegraNo ratings yet

- Pinellas County Sheriff's Amicus Brief in Mary's Law CaseDocument6 pagesPinellas County Sheriff's Amicus Brief in Mary's Law CaseWCTV Digital TeamNo ratings yet

- CASE NO. 114 Itogon-Suyoc Mines, Inc, v. Sangilo-Itogon Workers' Union in Behalf of Bartolome Mayo, Bernardo Aquino, Et. Al.Document7 pagesCASE NO. 114 Itogon-Suyoc Mines, Inc, v. Sangilo-Itogon Workers' Union in Behalf of Bartolome Mayo, Bernardo Aquino, Et. Al.kaizen shinichiNo ratings yet

- Data KHDocument37 pagesData KHHạnh DungNo ratings yet

- H02 - Taxes, Tax Laws and Tax AdministrationDocument10 pagesH02 - Taxes, Tax Laws and Tax Administrationnona galido100% (1)

- Property Rights PDFDocument15 pagesProperty Rights PDFbillsNo ratings yet

- Democratic SocialismDocument11 pagesDemocratic SocialismSuhani SinghNo ratings yet

- Mini Magic 6Document67 pagesMini Magic 6Venkat krishna100% (1)

- Easa Ad 2023-0009 1Document5 pagesEasa Ad 2023-0009 1Christian BruneauNo ratings yet

- PE.2019-20.0074 - Thunga HospitalDocument4 pagesPE.2019-20.0074 - Thunga HospitalAnonymous vFrxVNNo ratings yet

- Sources of International LawDocument3 pagesSources of International LawTrisha Emerlyn SantiaguelNo ratings yet