SL How Top Wholesalers Succeed

SL How Top Wholesalers Succeed

You might also like

- Research Methodology Full NotesDocument87 pagesResearch Methodology Full Notesu2b1151785% (253)

- Costco Case AnalysisDocument13 pagesCostco Case Analysisthechinachief67% (3)

- Grupo Bimbo Finals 9580980Document37 pagesGrupo Bimbo Finals 9580980Abhishek Kumar83% (6)

- Costco: A Case StudyDocument5 pagesCostco: A Case StudyMisti WalkerNo ratings yet

- Tchibo Case StudyDocument10 pagesTchibo Case StudyIustina RampeltNo ratings yet

- Profit Impact of Market StrategyDocument13 pagesProfit Impact of Market Strategyrasesh_gohilNo ratings yet

- The Five Types of Successful AcquisitionsDocument7 pagesThe Five Types of Successful AcquisitionsConsulter TutorNo ratings yet

- The Five Types of Successful AcquisitionsDocument7 pagesThe Five Types of Successful Acquisitionsbubb_rubbNo ratings yet

- BB Strategies For GrowthDocument8 pagesBB Strategies For GrowthGustavo MicheliniNo ratings yet

- Krispy Kreme Doughnuts: "It Ain't Just The Doughnuts That Are Glazed!"Document9 pagesKrispy Kreme Doughnuts: "It Ain't Just The Doughnuts That Are Glazed!"dmaia12No ratings yet

- What Is The Secret Recipe For Successful Mergers and AcquisitionsDocument7 pagesWhat Is The Secret Recipe For Successful Mergers and AcquisitionsAnna SartoriNo ratings yet

- CHP 6 - BCG - Blue Ocean StrategyDocument19 pagesCHP 6 - BCG - Blue Ocean StrategyBBHR20-A1 Wang Jing TingNo ratings yet

- Case FactsDocument4 pagesCase FactsRuth QuijanoNo ratings yet

- The Five Types of Successful AcquisitionsDocument7 pagesThe Five Types of Successful Acquisitionsbubb_rubbNo ratings yet

- The BCG Matrix and GE9 MatrixDocument5 pagesThe BCG Matrix and GE9 MatrixAnshul MangalNo ratings yet

- Morningstar Economic Moats IV - ExcellentDocument22 pagesMorningstar Economic Moats IV - Excellentee1993No ratings yet

- Mexico 1Document18 pagesMexico 1nisha patelNo ratings yet

- Solution Manual For Strategic Management Theory Cases An Integrated Approach 13th Edition Charles W L Hill Melissa A Schilling Gareth R JonesDocument25 pagesSolution Manual For Strategic Management Theory Cases An Integrated Approach 13th Edition Charles W L Hill Melissa A Schilling Gareth R JonesBrandonBridgesqabm100% (36)

- Analysing Strategy (BCG Matrix)Document6 pagesAnalysing Strategy (BCG Matrix)yadavpankaj1992No ratings yet

- Updated - Growbal Player Briefing Paper On Line-V1.1Document21 pagesUpdated - Growbal Player Briefing Paper On Line-V1.1akiyama madokaNo ratings yet

- Updated - Growbal Player Briefing Paper On Line-V1.1Document21 pagesUpdated - Growbal Player Briefing Paper On Line-V1.1akiyama madokaNo ratings yet

- Case Study 1Document3 pagesCase Study 1Joss DixonNo ratings yet

- BCG Classics Revisited The Growth Share Matrix Jun 2014 Tcm80-162923Document9 pagesBCG Classics Revisited The Growth Share Matrix Jun 2014 Tcm80-162923NITINNo ratings yet

- Marketing Mix of LLoydsDocument8 pagesMarketing Mix of LLoydsAmit SrivastavaNo ratings yet

- Mid-Game ReportDocument10 pagesMid-Game ReportRamizNo ratings yet

- BCG and Ge MatrixDocument44 pagesBCG and Ge MatrixManisha SinghNo ratings yet

- Costco A Case StudyDocument5 pagesCostco A Case StudyPeejay BoadoNo ratings yet

- BCG MatrixDocument25 pagesBCG MatrixkrisshhnaNo ratings yet

- How Strong Is ChinaDocument16 pagesHow Strong Is ChinaShashank ShashuNo ratings yet

- Marico Valuation Report - Aryan KuhadDocument8 pagesMarico Valuation Report - Aryan KuhadAryan KuhadNo ratings yet

- FMCG, Rating Methodology, Oct 2015 (Archived)Document5 pagesFMCG, Rating Methodology, Oct 2015 (Archived)Nikhilesh JoshiNo ratings yet

- Randa Hesham Aly Khattab Mohamad Ibrahim Mohamad Aboshall: Marketing AssignmentDocument5 pagesRanda Hesham Aly Khattab Mohamad Ibrahim Mohamad Aboshall: Marketing AssignmentMohamad IbrahimNo ratings yet

- 2 4 (2) - BusinessObjectivesDocument3 pages2 4 (2) - BusinessObjectivesserge.hNo ratings yet

- Marketing Manager Mindset Report Mention LivestormDocument62 pagesMarketing Manager Mindset Report Mention LivestormEstefanía Giraldo OsorioNo ratings yet

- BCG Notes FinalDocument10 pagesBCG Notes FinalHarsora UrvilNo ratings yet

- Lesson 4 - SM 1 Types of StrategiesDocument8 pagesLesson 4 - SM 1 Types of StrategiesJennie KimNo ratings yet

- Business Strategy AssignmentDocument7 pagesBusiness Strategy AssignmentHaneen ShahidNo ratings yet

- Group 5 (Reporter) - San Miguel CaseDocument8 pagesGroup 5 (Reporter) - San Miguel CaseFrancisco Marvin100% (1)

- BCG Metrix - UploadDocument19 pagesBCG Metrix - UploadSaibal DuttaNo ratings yet

- Investment Thesis Mty FoodsDocument6 pagesInvestment Thesis Mty FoodsArturoNo ratings yet

- Sena - Centro de Gestión de Mercados, Logística Y Tecnologías de La InformaciónDocument5 pagesSena - Centro de Gestión de Mercados, Logística Y Tecnologías de La InformaciónMary Esmeralda Florez QuinteroNo ratings yet

- GlobalizationDocument9 pagesGlobalizationRohitash AgnihotriNo ratings yet

- How To Do BCG MatrixDocument7 pagesHow To Do BCG MatrixMohanNo ratings yet

- Cópia de HighTechIndustryEurope - 1 - 09 - EnglishDocument2 pagesCópia de HighTechIndustryEurope - 1 - 09 - EnglishBrazil offshore jobsNo ratings yet

- DividendsDocument5 pagesDividendsMinettaLaneNo ratings yet

- BCG ItcDocument92 pagesBCG Itcprachii09No ratings yet

- BCG MatrixDocument19 pagesBCG MatrixvittamsettyNo ratings yet

- Eastboro Machine Tools CorporationDocument32 pagesEastboro Machine Tools Corporationrifki100% (2)

- RMCFDocument14 pagesRMCFzain6461No ratings yet

- Three Active Acquirers)Document3 pagesThree Active Acquirers)bellara.275No ratings yet

- Building To Win-FinalDocument51 pagesBuilding To Win-FinalKathrin BotaNo ratings yet

- BY: Vishwambar PuranikDocument27 pagesBY: Vishwambar PuranikRahul LengadeNo ratings yet

- Thesis SummaryDocument4 pagesThesis Summaryapi-278033882No ratings yet

- BCG and GeDocument30 pagesBCG and GeNishikant RanaNo ratings yet

- Strategic Management Concepts Competitiveness and Globalization 11th Edition Hitt Solutions ManualDocument32 pagesStrategic Management Concepts Competitiveness and Globalization 11th Edition Hitt Solutions Manuallifemateesculentopj100% (25)

- Sensolution 2018 Annual Report To ShareholdersDocument11 pagesSensolution 2018 Annual Report To ShareholdersNiraj KamdarNo ratings yet

- điều chỉnh cái 3 cái solutionDocument6 pagesđiều chỉnh cái 3 cái solutionHieu PhamNo ratings yet

- Boston Consulting Group Matrix: Presented byDocument19 pagesBoston Consulting Group Matrix: Presented byRaghu AnjanNo ratings yet

- WVH - AMA MWorld Winter 2006-2007Document2 pagesWVH - AMA MWorld Winter 2006-2007noble_josephNo ratings yet

- Life Sciences Sales Incentive Compensation: Sales Incentive CompensationFrom EverandLife Sciences Sales Incentive Compensation: Sales Incentive CompensationNo ratings yet

- Wholesale Price - 15 Jan 2016Document2 pagesWholesale Price - 15 Jan 2016lechiezNo ratings yet

- SHA TemplateDocument22 pagesSHA TemplatelechiezNo ratings yet

- Press Release - 6estatesDocument4 pagesPress Release - 6estateslechiezNo ratings yet

- Antibacterial Activity of Polyphenol Rich Extract of Selected Wild Honey Collected in Sabah MalaysiaDocument11 pagesAntibacterial Activity of Polyphenol Rich Extract of Selected Wild Honey Collected in Sabah MalaysialechiezNo ratings yet

- Questionnaire OCAI ToolDocument13 pagesQuestionnaire OCAI ToolVivin Yusta PratamaNo ratings yet

- Current LiabilitiesDocument94 pagesCurrent LiabilitiesDawit TilahunNo ratings yet

- Identifying RisksDocument13 pagesIdentifying Riskshabibrao253No ratings yet

- Mi LED Smart TV 4A Pro 123.2 CM 49 With Android: Grand Total 28499.00Document1 pageMi LED Smart TV 4A Pro 123.2 CM 49 With Android: Grand Total 28499.00Bharti GuptaNo ratings yet

- Business Development ProjectDocument3 pagesBusiness Development ProjectJohn MasonNo ratings yet

- Ready For Inspection - The Automotive Aftermarket in 2030: June 2018Document52 pagesReady For Inspection - The Automotive Aftermarket in 2030: June 2018MadhurimaNo ratings yet

- Mar 11 Tax CasesDocument13 pagesMar 11 Tax CasesMeg PalerNo ratings yet

- Packing ListDocument1 pagePacking ListJunior NavarroNo ratings yet

- 05 BBPM2103 - Topic01Document12 pages05 BBPM2103 - Topic01Nara ZeeNo ratings yet

- Baldwin Pa2570Document116 pagesBaldwin Pa2570Jorge J100% (1)

- New Brighton School of The Philippines: Pres. Ramon Magsaysay Ave, General Santos CityDocument6 pagesNew Brighton School of The Philippines: Pres. Ramon Magsaysay Ave, General Santos CityJofranco Gamutan LozanoNo ratings yet

- 4 5866240566815099684Document10 pages4 5866240566815099684Habteweld EdluNo ratings yet

- Full Business Analysis Study GuideDocument29 pagesFull Business Analysis Study GuideNgọc ThúyNo ratings yet

- Term Papernon Aarong's Strategic ManagementDocument33 pagesTerm Papernon Aarong's Strategic ManagementFarhan FuadNo ratings yet

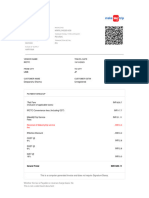

- NR7515802085704623 InvoiceDocument2 pagesNR7515802085704623 InvoiceMohit SharmaNo ratings yet

- Litepaper 10 21 22Document9 pagesLitepaper 10 21 22Yvann ArutoNo ratings yet

- CAGRDocument3 pagesCAGRlilian novarianNo ratings yet

- Subhash Dey's BST XI 2024-25 (Sample PDFDocument58 pagesSubhash Dey's BST XI 2024-25 (Sample PDFEkaspal SinghNo ratings yet

- REVISED SURVEY FORM AND SOP MSME GDocument6 pagesREVISED SURVEY FORM AND SOP MSME GAzzia Morante LopezNo ratings yet

- AIS 5102 (2nd Group)Document17 pagesAIS 5102 (2nd Group)MD Hafizul Islam HafizNo ratings yet

- Socio-Ecological Problems: Green Marketing Management DMA 557Document24 pagesSocio-Ecological Problems: Green Marketing Management DMA 557eklwgnnwlgNo ratings yet

- How Much Must You Invest Now at 7Document5 pagesHow Much Must You Invest Now at 7Azman AzmanNo ratings yet

- Bosch Project 2020 PDFDocument1 pageBosch Project 2020 PDFAvi LimerNo ratings yet

- User Tcode ZDocument108 pagesUser Tcode ZSetiady Perwira JatiNo ratings yet

- Questions On Journal Entry For StudentsDocument8 pagesQuestions On Journal Entry For Studentsveraji3735No ratings yet

- Colour Theory Handouts Goodwill - Nature and ValuationDocument13 pagesColour Theory Handouts Goodwill - Nature and ValuationAmir KhanNo ratings yet

- What Is Ambisyon Natin 2040Document2 pagesWhat Is Ambisyon Natin 2040Tino Salabsab100% (1)

- Using Career One Stop To Create Your ResumeDocument1 pageUsing Career One Stop To Create Your Resumeapi-236019943No ratings yet

- Sale of Goods Act, 1930: Question Bank Unit:1Document10 pagesSale of Goods Act, 1930: Question Bank Unit:1gargee thakareNo ratings yet

Download as pdf or txt

You might also like

- Research Methodology Full NotesDocument87 pagesResearch Methodology Full Notesu2b1151785% (253)

- Costco Case AnalysisDocument13 pagesCostco Case Analysisthechinachief67% (3)

- Grupo Bimbo Finals 9580980Document37 pagesGrupo Bimbo Finals 9580980Abhishek Kumar83% (6)

- Costco: A Case StudyDocument5 pagesCostco: A Case StudyMisti WalkerNo ratings yet

- Tchibo Case StudyDocument10 pagesTchibo Case StudyIustina RampeltNo ratings yet

- Profit Impact of Market StrategyDocument13 pagesProfit Impact of Market Strategyrasesh_gohilNo ratings yet

- The Five Types of Successful AcquisitionsDocument7 pagesThe Five Types of Successful AcquisitionsConsulter TutorNo ratings yet

- The Five Types of Successful AcquisitionsDocument7 pagesThe Five Types of Successful Acquisitionsbubb_rubbNo ratings yet

- BB Strategies For GrowthDocument8 pagesBB Strategies For GrowthGustavo MicheliniNo ratings yet

- Krispy Kreme Doughnuts: "It Ain't Just The Doughnuts That Are Glazed!"Document9 pagesKrispy Kreme Doughnuts: "It Ain't Just The Doughnuts That Are Glazed!"dmaia12No ratings yet

- What Is The Secret Recipe For Successful Mergers and AcquisitionsDocument7 pagesWhat Is The Secret Recipe For Successful Mergers and AcquisitionsAnna SartoriNo ratings yet

- CHP 6 - BCG - Blue Ocean StrategyDocument19 pagesCHP 6 - BCG - Blue Ocean StrategyBBHR20-A1 Wang Jing TingNo ratings yet

- Case FactsDocument4 pagesCase FactsRuth QuijanoNo ratings yet

- The Five Types of Successful AcquisitionsDocument7 pagesThe Five Types of Successful Acquisitionsbubb_rubbNo ratings yet

- The BCG Matrix and GE9 MatrixDocument5 pagesThe BCG Matrix and GE9 MatrixAnshul MangalNo ratings yet

- Morningstar Economic Moats IV - ExcellentDocument22 pagesMorningstar Economic Moats IV - Excellentee1993No ratings yet

- Mexico 1Document18 pagesMexico 1nisha patelNo ratings yet

- Solution Manual For Strategic Management Theory Cases An Integrated Approach 13th Edition Charles W L Hill Melissa A Schilling Gareth R JonesDocument25 pagesSolution Manual For Strategic Management Theory Cases An Integrated Approach 13th Edition Charles W L Hill Melissa A Schilling Gareth R JonesBrandonBridgesqabm100% (36)

- Analysing Strategy (BCG Matrix)Document6 pagesAnalysing Strategy (BCG Matrix)yadavpankaj1992No ratings yet

- Updated - Growbal Player Briefing Paper On Line-V1.1Document21 pagesUpdated - Growbal Player Briefing Paper On Line-V1.1akiyama madokaNo ratings yet

- Updated - Growbal Player Briefing Paper On Line-V1.1Document21 pagesUpdated - Growbal Player Briefing Paper On Line-V1.1akiyama madokaNo ratings yet

- Case Study 1Document3 pagesCase Study 1Joss DixonNo ratings yet

- BCG Classics Revisited The Growth Share Matrix Jun 2014 Tcm80-162923Document9 pagesBCG Classics Revisited The Growth Share Matrix Jun 2014 Tcm80-162923NITINNo ratings yet

- Marketing Mix of LLoydsDocument8 pagesMarketing Mix of LLoydsAmit SrivastavaNo ratings yet

- Mid-Game ReportDocument10 pagesMid-Game ReportRamizNo ratings yet

- BCG and Ge MatrixDocument44 pagesBCG and Ge MatrixManisha SinghNo ratings yet

- Costco A Case StudyDocument5 pagesCostco A Case StudyPeejay BoadoNo ratings yet

- BCG MatrixDocument25 pagesBCG MatrixkrisshhnaNo ratings yet

- How Strong Is ChinaDocument16 pagesHow Strong Is ChinaShashank ShashuNo ratings yet

- Marico Valuation Report - Aryan KuhadDocument8 pagesMarico Valuation Report - Aryan KuhadAryan KuhadNo ratings yet

- FMCG, Rating Methodology, Oct 2015 (Archived)Document5 pagesFMCG, Rating Methodology, Oct 2015 (Archived)Nikhilesh JoshiNo ratings yet

- Randa Hesham Aly Khattab Mohamad Ibrahim Mohamad Aboshall: Marketing AssignmentDocument5 pagesRanda Hesham Aly Khattab Mohamad Ibrahim Mohamad Aboshall: Marketing AssignmentMohamad IbrahimNo ratings yet

- 2 4 (2) - BusinessObjectivesDocument3 pages2 4 (2) - BusinessObjectivesserge.hNo ratings yet

- Marketing Manager Mindset Report Mention LivestormDocument62 pagesMarketing Manager Mindset Report Mention LivestormEstefanía Giraldo OsorioNo ratings yet

- BCG Notes FinalDocument10 pagesBCG Notes FinalHarsora UrvilNo ratings yet

- Lesson 4 - SM 1 Types of StrategiesDocument8 pagesLesson 4 - SM 1 Types of StrategiesJennie KimNo ratings yet

- Business Strategy AssignmentDocument7 pagesBusiness Strategy AssignmentHaneen ShahidNo ratings yet

- Group 5 (Reporter) - San Miguel CaseDocument8 pagesGroup 5 (Reporter) - San Miguel CaseFrancisco Marvin100% (1)

- BCG Metrix - UploadDocument19 pagesBCG Metrix - UploadSaibal DuttaNo ratings yet

- Investment Thesis Mty FoodsDocument6 pagesInvestment Thesis Mty FoodsArturoNo ratings yet

- Sena - Centro de Gestión de Mercados, Logística Y Tecnologías de La InformaciónDocument5 pagesSena - Centro de Gestión de Mercados, Logística Y Tecnologías de La InformaciónMary Esmeralda Florez QuinteroNo ratings yet

- GlobalizationDocument9 pagesGlobalizationRohitash AgnihotriNo ratings yet

- How To Do BCG MatrixDocument7 pagesHow To Do BCG MatrixMohanNo ratings yet

- Cópia de HighTechIndustryEurope - 1 - 09 - EnglishDocument2 pagesCópia de HighTechIndustryEurope - 1 - 09 - EnglishBrazil offshore jobsNo ratings yet

- DividendsDocument5 pagesDividendsMinettaLaneNo ratings yet

- BCG ItcDocument92 pagesBCG Itcprachii09No ratings yet

- BCG MatrixDocument19 pagesBCG MatrixvittamsettyNo ratings yet

- Eastboro Machine Tools CorporationDocument32 pagesEastboro Machine Tools Corporationrifki100% (2)

- RMCFDocument14 pagesRMCFzain6461No ratings yet

- Three Active Acquirers)Document3 pagesThree Active Acquirers)bellara.275No ratings yet

- Building To Win-FinalDocument51 pagesBuilding To Win-FinalKathrin BotaNo ratings yet

- BY: Vishwambar PuranikDocument27 pagesBY: Vishwambar PuranikRahul LengadeNo ratings yet

- Thesis SummaryDocument4 pagesThesis Summaryapi-278033882No ratings yet

- BCG and GeDocument30 pagesBCG and GeNishikant RanaNo ratings yet

- Strategic Management Concepts Competitiveness and Globalization 11th Edition Hitt Solutions ManualDocument32 pagesStrategic Management Concepts Competitiveness and Globalization 11th Edition Hitt Solutions Manuallifemateesculentopj100% (25)

- Sensolution 2018 Annual Report To ShareholdersDocument11 pagesSensolution 2018 Annual Report To ShareholdersNiraj KamdarNo ratings yet

- điều chỉnh cái 3 cái solutionDocument6 pagesđiều chỉnh cái 3 cái solutionHieu PhamNo ratings yet

- Boston Consulting Group Matrix: Presented byDocument19 pagesBoston Consulting Group Matrix: Presented byRaghu AnjanNo ratings yet

- WVH - AMA MWorld Winter 2006-2007Document2 pagesWVH - AMA MWorld Winter 2006-2007noble_josephNo ratings yet

- Life Sciences Sales Incentive Compensation: Sales Incentive CompensationFrom EverandLife Sciences Sales Incentive Compensation: Sales Incentive CompensationNo ratings yet

- Wholesale Price - 15 Jan 2016Document2 pagesWholesale Price - 15 Jan 2016lechiezNo ratings yet

- SHA TemplateDocument22 pagesSHA TemplatelechiezNo ratings yet

- Press Release - 6estatesDocument4 pagesPress Release - 6estateslechiezNo ratings yet

- Antibacterial Activity of Polyphenol Rich Extract of Selected Wild Honey Collected in Sabah MalaysiaDocument11 pagesAntibacterial Activity of Polyphenol Rich Extract of Selected Wild Honey Collected in Sabah MalaysialechiezNo ratings yet

- Questionnaire OCAI ToolDocument13 pagesQuestionnaire OCAI ToolVivin Yusta PratamaNo ratings yet

- Current LiabilitiesDocument94 pagesCurrent LiabilitiesDawit TilahunNo ratings yet

- Identifying RisksDocument13 pagesIdentifying Riskshabibrao253No ratings yet

- Mi LED Smart TV 4A Pro 123.2 CM 49 With Android: Grand Total 28499.00Document1 pageMi LED Smart TV 4A Pro 123.2 CM 49 With Android: Grand Total 28499.00Bharti GuptaNo ratings yet

- Business Development ProjectDocument3 pagesBusiness Development ProjectJohn MasonNo ratings yet

- Ready For Inspection - The Automotive Aftermarket in 2030: June 2018Document52 pagesReady For Inspection - The Automotive Aftermarket in 2030: June 2018MadhurimaNo ratings yet

- Mar 11 Tax CasesDocument13 pagesMar 11 Tax CasesMeg PalerNo ratings yet

- Packing ListDocument1 pagePacking ListJunior NavarroNo ratings yet

- 05 BBPM2103 - Topic01Document12 pages05 BBPM2103 - Topic01Nara ZeeNo ratings yet

- Baldwin Pa2570Document116 pagesBaldwin Pa2570Jorge J100% (1)

- New Brighton School of The Philippines: Pres. Ramon Magsaysay Ave, General Santos CityDocument6 pagesNew Brighton School of The Philippines: Pres. Ramon Magsaysay Ave, General Santos CityJofranco Gamutan LozanoNo ratings yet

- 4 5866240566815099684Document10 pages4 5866240566815099684Habteweld EdluNo ratings yet

- Full Business Analysis Study GuideDocument29 pagesFull Business Analysis Study GuideNgọc ThúyNo ratings yet

- Term Papernon Aarong's Strategic ManagementDocument33 pagesTerm Papernon Aarong's Strategic ManagementFarhan FuadNo ratings yet

- NR7515802085704623 InvoiceDocument2 pagesNR7515802085704623 InvoiceMohit SharmaNo ratings yet

- Litepaper 10 21 22Document9 pagesLitepaper 10 21 22Yvann ArutoNo ratings yet

- CAGRDocument3 pagesCAGRlilian novarianNo ratings yet

- Subhash Dey's BST XI 2024-25 (Sample PDFDocument58 pagesSubhash Dey's BST XI 2024-25 (Sample PDFEkaspal SinghNo ratings yet

- REVISED SURVEY FORM AND SOP MSME GDocument6 pagesREVISED SURVEY FORM AND SOP MSME GAzzia Morante LopezNo ratings yet

- AIS 5102 (2nd Group)Document17 pagesAIS 5102 (2nd Group)MD Hafizul Islam HafizNo ratings yet

- Socio-Ecological Problems: Green Marketing Management DMA 557Document24 pagesSocio-Ecological Problems: Green Marketing Management DMA 557eklwgnnwlgNo ratings yet

- How Much Must You Invest Now at 7Document5 pagesHow Much Must You Invest Now at 7Azman AzmanNo ratings yet

- Bosch Project 2020 PDFDocument1 pageBosch Project 2020 PDFAvi LimerNo ratings yet

- User Tcode ZDocument108 pagesUser Tcode ZSetiady Perwira JatiNo ratings yet

- Questions On Journal Entry For StudentsDocument8 pagesQuestions On Journal Entry For Studentsveraji3735No ratings yet

- Colour Theory Handouts Goodwill - Nature and ValuationDocument13 pagesColour Theory Handouts Goodwill - Nature and ValuationAmir KhanNo ratings yet

- What Is Ambisyon Natin 2040Document2 pagesWhat Is Ambisyon Natin 2040Tino Salabsab100% (1)

- Using Career One Stop To Create Your ResumeDocument1 pageUsing Career One Stop To Create Your Resumeapi-236019943No ratings yet

- Sale of Goods Act, 1930: Question Bank Unit:1Document10 pagesSale of Goods Act, 1930: Question Bank Unit:1gargee thakareNo ratings yet