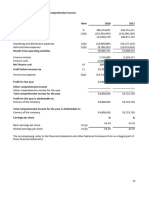

IFRS Example Consolidated Financial Statements 2023 8

IFRS Example Consolidated Financial Statements 2023 8

You might also like

- Awasr Oman and Partners SAOC - FS 2020 EnglishDocument42 pagesAwasr Oman and Partners SAOC - FS 2020 Englishabdullahsaleem91No ratings yet

- Acyava Reflection PaperDocument6 pagesAcyava Reflection PaperJustin AciertoNo ratings yet

- Bring-Your-Own-Device ("Byod") Acceptable Use PolicyDocument7 pagesBring-Your-Own-Device ("Byod") Acceptable Use PolicyAmanNo ratings yet

- Overview of The Federal Sentencing Guidelines For Organizations and Corporate Compliance Programslawrence D. Finderhaynes and Boone, Llpa. Michael Warneckehaynes and Boone, LLPDocument45 pagesOverview of The Federal Sentencing Guidelines For Organizations and Corporate Compliance Programslawrence D. Finderhaynes and Boone, Llpa. Michael Warneckehaynes and Boone, LLPLisa Stinocher OHanlonNo ratings yet

- Chapter 22 Self-TestDocument9 pagesChapter 22 Self-TestDaniel BaoNo ratings yet

- IFRS Example Consolidated Financial Statements 2023 8Document1 pageIFRS Example Consolidated Financial Statements 2023 8Gonzalo SeverssonNo ratings yet

- Time Watch Investments Limited Unaudited 2nd QTR 1HF2009 Financial Statement 090210Document13 pagesTime Watch Investments Limited Unaudited 2nd QTR 1HF2009 Financial Statement 090210WeR1 Consultants Pte LtdNo ratings yet

- P&L Fy21Document2 pagesP&L Fy21simoniuj2No ratings yet

- ENX - URD2022 - Financial Statements and Auditors ReportDocument99 pagesENX - URD2022 - Financial Statements and Auditors ReportRaghunathNo ratings yet

- Hindalco Company's Finance DepartmentDocument14 pagesHindalco Company's Finance DepartmentJaydeep SolankiNo ratings yet

- Nexa - Financial Statements 2020Document81 pagesNexa - Financial Statements 2020frankNo ratings yet

- 2016 FINCA Int Consolidated IFRS FinalDocument64 pages2016 FINCA Int Consolidated IFRS FinalSaint CutesyNo ratings yet

- Consolidated Statement of Comprehensive Income: PWC Holdings LTD and Its SubsidiariesDocument4 pagesConsolidated Statement of Comprehensive Income: PWC Holdings LTD and Its SubsidiariesTheint Myat KyalsinNo ratings yet

- Annual: Etfx Uk Group LLCDocument70 pagesAnnual: Etfx Uk Group LLCeliasNo ratings yet

- 2017 Revenues 41,381 40,859: (In Millions of Euros, Except For Per Share Data)Document37 pages2017 Revenues 41,381 40,859: (In Millions of Euros, Except For Per Share Data)Cristina PascariNo ratings yet

- Time Watch Investments 1Q2010 Results 131109Document12 pagesTime Watch Investments 1Q2010 Results 131109WeR1 Consultants Pte LtdNo ratings yet

- UntitledDocument357 pagesUntitledAlexNo ratings yet

- TFR 2023 eDocument69 pagesTFR 2023 eAntwanNo ratings yet

- Cebu AirDocument22 pagesCebu AirCamille BagadiongNo ratings yet

- FIN 422-Midterm AssDocument43 pagesFIN 422-Midterm AssTakibul HasanNo ratings yet

- Consolidated Balance Sheet For Hindustan Unilever LTDDocument11 pagesConsolidated Balance Sheet For Hindustan Unilever LTDMohit ChughNo ratings yet

- WG2W 64xou86kk9itzyv6.1Document28 pagesWG2W 64xou86kk9itzyv6.1Paul BluemnerNo ratings yet

- (A) Nature of Business of Cepatwawasan Group BerhadDocument16 pages(A) Nature of Business of Cepatwawasan Group BerhadTan Rou YingNo ratings yet

- Plaquette Annuelle 31 Decembre 2022 EN VdefsDocument80 pagesPlaquette Annuelle 31 Decembre 2022 EN VdefsAbdcNo ratings yet

- Capgemini - 2024-02-20 - 2023 Consolidated Financial StatementsDocument67 pagesCapgemini - 2024-02-20 - 2023 Consolidated Financial Statementshabiyek787No ratings yet

- 0202 - RGTECH - QR - 2020-12-31 - Radiant Globaltech Berhad - Quarterly Results - 31.12.2020 - 670632592Document20 pages0202 - RGTECH - QR - 2020-12-31 - Radiant Globaltech Berhad - Quarterly Results - 31.12.2020 - 670632592Iqbal YusufNo ratings yet

- Nexa - Financial Statements 2021Document74 pagesNexa - Financial Statements 2021Jefferson JuniorNo ratings yet

- Sapnrg-Fs q4 31 Jan 2023Document33 pagesSapnrg-Fs q4 31 Jan 2023Mohd Faizal Mohd IbrahimNo ratings yet

- Digitally Signed by Debolina Karmakar Date: 2023.08.10 12:39:40 +05'30'Document5 pagesDigitally Signed by Debolina Karmakar Date: 2023.08.10 12:39:40 +05'30'Mahesh hamneNo ratings yet

- Consolidated Financial Statements As of December 31 2020Document86 pagesConsolidated Financial Statements As of December 31 2020Raka AryawanNo ratings yet

- Balance Sheet: Titan Industries LimitedDocument4 pagesBalance Sheet: Titan Industries LimitedShalini ShreyaNo ratings yet

- EOG PresentationDocument23 pagesEOG Presentationomoba solaNo ratings yet

- Consol Result Mar23Document16 pagesConsol Result Mar23Amit KumarNo ratings yet

- Summary - Comparative (2020 vs. 2019)Document5 pagesSummary - Comparative (2020 vs. 2019)Neil David ForbesNo ratings yet

- Infot RobinsonDocument3 pagesInfot Robinsonkingofkins04No ratings yet

- GAR02 28 02 2024 FY2023 Results ReleaseDocument29 pagesGAR02 28 02 2024 FY2023 Results Releasedesifatimah87No ratings yet

- Asl Marine Holdings Ltd.Document30 pagesAsl Marine Holdings Ltd.citybizlist11No ratings yet

- Cfas Ias 1 Presentation of FS For StudentsDocument15 pagesCfas Ias 1 Presentation of FS For StudentsFreya GeslaniNo ratings yet

- ACC Financial ResultsDocument12 pagesACC Financial ResultsKKVSBNo ratings yet

- ICICI Financial StatementsDocument9 pagesICICI Financial StatementsNandini JhaNo ratings yet

- Nhs England Annual Accounts Report 2019 20Document50 pagesNhs England Annual Accounts Report 2019 20Michel LNo ratings yet

- Unlock Assignment 05Document4 pagesUnlock Assignment 05mmakgabomnisi6No ratings yet

- Q1 2023 Puma Energy Results ReportDocument11 pagesQ1 2023 Puma Energy Results ReportKA-11 Єфіменко ІванNo ratings yet

- Raymond Limited Financial StatementsDocument85 pagesRaymond Limited Financial StatementsVinay KukrejaNo ratings yet

- Statemnt of Profit and LossDocument1 pageStatemnt of Profit and LossRutuja shindeNo ratings yet

- q209 - Airtel Published FinancialsDocument7 pagesq209 - Airtel Published Financialsmixedbag100% (2)

- Unaudited Financial Results For The Quarter Ended 30Th June, 2011Document1 pageUnaudited Financial Results For The Quarter Ended 30Th June, 2011Ayush JainNo ratings yet

- Chapter 4Document32 pagesChapter 4sunilNo ratings yet

- 审计年报2010316Document35 pages审计年报2010316yf zNo ratings yet

- EY-IFRS-FS-20 - Part 5Document8 pagesEY-IFRS-FS-20 - Part 5Hung LeNo ratings yet

- Standalone Cash Flow Statement: For The Year Ended March 31, 2019Document2 pagesStandalone Cash Flow Statement: For The Year Ended March 31, 2019deepzNo ratings yet

- TSAU - Financiero - ENGDocument167 pagesTSAU - Financiero - ENGMonica EscribaNo ratings yet

- INTERIM REPORT YA2021 QUARTER 4 (01 MAY 2021 Until 31 JUL 2021)Document16 pagesINTERIM REPORT YA2021 QUARTER 4 (01 MAY 2021 Until 31 JUL 2021)pes myNo ratings yet

- In Millions of Euros, Except For Per Share DataDocument24 pagesIn Millions of Euros, Except For Per Share DataGrace StylesNo ratings yet

- Directors ReportDocument14 pagesDirectors ReportGaurav JainNo ratings yet

- Infineon Annual Report 2021-153-156Document4 pagesInfineon Annual Report 2021-153-156Ddaeng StudiosNo ratings yet

- Ramco Annual Report 2014Document2 pagesRamco Annual Report 2014nithinNo ratings yet

- Airbus SN Q3-2020Document21 pagesAirbus SN Q3-2020paulouisvergnesNo ratings yet

- Income Statement and Balance Sheet ExerciseDocument2 pagesIncome Statement and Balance Sheet ExerciseMujieh NkengNo ratings yet

- Financial Statements 2015: Airbus Group SEDocument194 pagesFinancial Statements 2015: Airbus Group SEfx_ww2001No ratings yet

- Colgate 2Document11 pagesColgate 2gaurav.jain.25nNo ratings yet

- Sumarised P&LDocument1 pageSumarised P&Lgargrohan989gargNo ratings yet

- Cobalto 1 PDFDocument22 pagesCobalto 1 PDFcristamaarNo ratings yet

- SM 5Document27 pagesSM 5wtfNo ratings yet

- Bangalore To Kolkata Flight Status Today, Flight Time & Tracker - IndiGoDocument1 pageBangalore To Kolkata Flight Status Today, Flight Time & Tracker - IndiGoPragati SarafNo ratings yet

- Eti Base Code EnglishDocument4 pagesEti Base Code EnglishJohn RajeshNo ratings yet

- Blackbody Radiation Spectrum NotesDocument10 pagesBlackbody Radiation Spectrum NotesKarthick JyothieshwarNo ratings yet

- Important Decisions of RTIDocument185 pagesImportant Decisions of RTIkrishnadas100100% (1)

- Fact Analysis WorkshopDocument2 pagesFact Analysis WorkshopKaran VijayanNo ratings yet

- ABELLO vs. CIRDocument4 pagesABELLO vs. CIRFrancise Mae Montilla MordenoNo ratings yet

- Citric Acid SDS11350 PDFDocument7 pagesCitric Acid SDS11350 PDFSyafiq Mohd NohNo ratings yet

- Genitive Case FixaçãoDocument4 pagesGenitive Case Fixaçãoryan 01 da EPCArNo ratings yet

- Affidavit of Romy BuymaxxDocument2 pagesAffidavit of Romy BuymaxxanonNo ratings yet

- Je DV and Medical FinalDocument14 pagesJe DV and Medical FinalAna GoreNo ratings yet

- Case Title: G.R. No. 86693 July 2, 1990Document2 pagesCase Title: G.R. No. 86693 July 2, 1990Arnold Jr AmboangNo ratings yet

- 001 2017 4 BDocument288 pages001 2017 4 BmunyatsungaNo ratings yet

- April SBIDocument5 pagesApril SBIRahul kumarNo ratings yet

- Mcqs SolvedDocument15 pagesMcqs SolvedWaqar Ahmed100% (1)

- 879Document48 pages879B. MerkurNo ratings yet

- Crime in Dar Es SalaamDocument64 pagesCrime in Dar Es SalaamUnited Nations Human Settlements Programme (UN-HABITAT)No ratings yet

- SOP For Handling of Rejected Raw MaterialDocument6 pagesSOP For Handling of Rejected Raw Materialanoushia alviNo ratings yet

- Information For Foreign ApplicantsDocument6 pagesInformation For Foreign ApplicantsMuhannad Al-AfifNo ratings yet

- We The State - Issue 10 Vol 2Document12 pagesWe The State - Issue 10 Vol 2wethestateNo ratings yet

- Aklan Revised IRR To National Building Code (Compatibility Mode)Document80 pagesAklan Revised IRR To National Building Code (Compatibility Mode)Anton_Young_1962No ratings yet

- 10000026681Document20 pages10000026681Chapter 11 DocketsNo ratings yet

- Graft CasesDocument37 pagesGraft CasesTuella RusselNo ratings yet

- WarnickJ - MGMT436 - Strategic Audit Assignment - 8.4 (Draft)Document17 pagesWarnickJ - MGMT436 - Strategic Audit Assignment - 8.4 (Draft)James WarnickNo ratings yet

- Thomas & Margaret (Reilly) Kemp of Ireland and Their Descendants in AmericaDocument8 pagesThomas & Margaret (Reilly) Kemp of Ireland and Their Descendants in AmericaThomas Jay KempNo ratings yet

- Hope, Kempe Ronald-Police Corruption and Police Reforms in Developing Societies-CRC Press (2016)Document270 pagesHope, Kempe Ronald-Police Corruption and Police Reforms in Developing Societies-CRC Press (2016)Darko Zlatkovik100% (1)

Download as xlsx, pdf, or txt

You might also like

- Awasr Oman and Partners SAOC - FS 2020 EnglishDocument42 pagesAwasr Oman and Partners SAOC - FS 2020 Englishabdullahsaleem91No ratings yet

- Acyava Reflection PaperDocument6 pagesAcyava Reflection PaperJustin AciertoNo ratings yet

- Bring-Your-Own-Device ("Byod") Acceptable Use PolicyDocument7 pagesBring-Your-Own-Device ("Byod") Acceptable Use PolicyAmanNo ratings yet

- Overview of The Federal Sentencing Guidelines For Organizations and Corporate Compliance Programslawrence D. Finderhaynes and Boone, Llpa. Michael Warneckehaynes and Boone, LLPDocument45 pagesOverview of The Federal Sentencing Guidelines For Organizations and Corporate Compliance Programslawrence D. Finderhaynes and Boone, Llpa. Michael Warneckehaynes and Boone, LLPLisa Stinocher OHanlonNo ratings yet

- Chapter 22 Self-TestDocument9 pagesChapter 22 Self-TestDaniel BaoNo ratings yet

- IFRS Example Consolidated Financial Statements 2023 8Document1 pageIFRS Example Consolidated Financial Statements 2023 8Gonzalo SeverssonNo ratings yet

- Time Watch Investments Limited Unaudited 2nd QTR 1HF2009 Financial Statement 090210Document13 pagesTime Watch Investments Limited Unaudited 2nd QTR 1HF2009 Financial Statement 090210WeR1 Consultants Pte LtdNo ratings yet

- P&L Fy21Document2 pagesP&L Fy21simoniuj2No ratings yet

- ENX - URD2022 - Financial Statements and Auditors ReportDocument99 pagesENX - URD2022 - Financial Statements and Auditors ReportRaghunathNo ratings yet

- Hindalco Company's Finance DepartmentDocument14 pagesHindalco Company's Finance DepartmentJaydeep SolankiNo ratings yet

- Nexa - Financial Statements 2020Document81 pagesNexa - Financial Statements 2020frankNo ratings yet

- 2016 FINCA Int Consolidated IFRS FinalDocument64 pages2016 FINCA Int Consolidated IFRS FinalSaint CutesyNo ratings yet

- Consolidated Statement of Comprehensive Income: PWC Holdings LTD and Its SubsidiariesDocument4 pagesConsolidated Statement of Comprehensive Income: PWC Holdings LTD and Its SubsidiariesTheint Myat KyalsinNo ratings yet

- Annual: Etfx Uk Group LLCDocument70 pagesAnnual: Etfx Uk Group LLCeliasNo ratings yet

- 2017 Revenues 41,381 40,859: (In Millions of Euros, Except For Per Share Data)Document37 pages2017 Revenues 41,381 40,859: (In Millions of Euros, Except For Per Share Data)Cristina PascariNo ratings yet

- Time Watch Investments 1Q2010 Results 131109Document12 pagesTime Watch Investments 1Q2010 Results 131109WeR1 Consultants Pte LtdNo ratings yet

- UntitledDocument357 pagesUntitledAlexNo ratings yet

- TFR 2023 eDocument69 pagesTFR 2023 eAntwanNo ratings yet

- Cebu AirDocument22 pagesCebu AirCamille BagadiongNo ratings yet

- FIN 422-Midterm AssDocument43 pagesFIN 422-Midterm AssTakibul HasanNo ratings yet

- Consolidated Balance Sheet For Hindustan Unilever LTDDocument11 pagesConsolidated Balance Sheet For Hindustan Unilever LTDMohit ChughNo ratings yet

- WG2W 64xou86kk9itzyv6.1Document28 pagesWG2W 64xou86kk9itzyv6.1Paul BluemnerNo ratings yet

- (A) Nature of Business of Cepatwawasan Group BerhadDocument16 pages(A) Nature of Business of Cepatwawasan Group BerhadTan Rou YingNo ratings yet

- Plaquette Annuelle 31 Decembre 2022 EN VdefsDocument80 pagesPlaquette Annuelle 31 Decembre 2022 EN VdefsAbdcNo ratings yet

- Capgemini - 2024-02-20 - 2023 Consolidated Financial StatementsDocument67 pagesCapgemini - 2024-02-20 - 2023 Consolidated Financial Statementshabiyek787No ratings yet

- 0202 - RGTECH - QR - 2020-12-31 - Radiant Globaltech Berhad - Quarterly Results - 31.12.2020 - 670632592Document20 pages0202 - RGTECH - QR - 2020-12-31 - Radiant Globaltech Berhad - Quarterly Results - 31.12.2020 - 670632592Iqbal YusufNo ratings yet

- Nexa - Financial Statements 2021Document74 pagesNexa - Financial Statements 2021Jefferson JuniorNo ratings yet

- Sapnrg-Fs q4 31 Jan 2023Document33 pagesSapnrg-Fs q4 31 Jan 2023Mohd Faizal Mohd IbrahimNo ratings yet

- Digitally Signed by Debolina Karmakar Date: 2023.08.10 12:39:40 +05'30'Document5 pagesDigitally Signed by Debolina Karmakar Date: 2023.08.10 12:39:40 +05'30'Mahesh hamneNo ratings yet

- Consolidated Financial Statements As of December 31 2020Document86 pagesConsolidated Financial Statements As of December 31 2020Raka AryawanNo ratings yet

- Balance Sheet: Titan Industries LimitedDocument4 pagesBalance Sheet: Titan Industries LimitedShalini ShreyaNo ratings yet

- EOG PresentationDocument23 pagesEOG Presentationomoba solaNo ratings yet

- Consol Result Mar23Document16 pagesConsol Result Mar23Amit KumarNo ratings yet

- Summary - Comparative (2020 vs. 2019)Document5 pagesSummary - Comparative (2020 vs. 2019)Neil David ForbesNo ratings yet

- Infot RobinsonDocument3 pagesInfot Robinsonkingofkins04No ratings yet

- GAR02 28 02 2024 FY2023 Results ReleaseDocument29 pagesGAR02 28 02 2024 FY2023 Results Releasedesifatimah87No ratings yet

- Asl Marine Holdings Ltd.Document30 pagesAsl Marine Holdings Ltd.citybizlist11No ratings yet

- Cfas Ias 1 Presentation of FS For StudentsDocument15 pagesCfas Ias 1 Presentation of FS For StudentsFreya GeslaniNo ratings yet

- ACC Financial ResultsDocument12 pagesACC Financial ResultsKKVSBNo ratings yet

- ICICI Financial StatementsDocument9 pagesICICI Financial StatementsNandini JhaNo ratings yet

- Nhs England Annual Accounts Report 2019 20Document50 pagesNhs England Annual Accounts Report 2019 20Michel LNo ratings yet

- Unlock Assignment 05Document4 pagesUnlock Assignment 05mmakgabomnisi6No ratings yet

- Q1 2023 Puma Energy Results ReportDocument11 pagesQ1 2023 Puma Energy Results ReportKA-11 Єфіменко ІванNo ratings yet

- Raymond Limited Financial StatementsDocument85 pagesRaymond Limited Financial StatementsVinay KukrejaNo ratings yet

- Statemnt of Profit and LossDocument1 pageStatemnt of Profit and LossRutuja shindeNo ratings yet

- q209 - Airtel Published FinancialsDocument7 pagesq209 - Airtel Published Financialsmixedbag100% (2)

- Unaudited Financial Results For The Quarter Ended 30Th June, 2011Document1 pageUnaudited Financial Results For The Quarter Ended 30Th June, 2011Ayush JainNo ratings yet

- Chapter 4Document32 pagesChapter 4sunilNo ratings yet

- 审计年报2010316Document35 pages审计年报2010316yf zNo ratings yet

- EY-IFRS-FS-20 - Part 5Document8 pagesEY-IFRS-FS-20 - Part 5Hung LeNo ratings yet

- Standalone Cash Flow Statement: For The Year Ended March 31, 2019Document2 pagesStandalone Cash Flow Statement: For The Year Ended March 31, 2019deepzNo ratings yet

- TSAU - Financiero - ENGDocument167 pagesTSAU - Financiero - ENGMonica EscribaNo ratings yet

- INTERIM REPORT YA2021 QUARTER 4 (01 MAY 2021 Until 31 JUL 2021)Document16 pagesINTERIM REPORT YA2021 QUARTER 4 (01 MAY 2021 Until 31 JUL 2021)pes myNo ratings yet

- In Millions of Euros, Except For Per Share DataDocument24 pagesIn Millions of Euros, Except For Per Share DataGrace StylesNo ratings yet

- Directors ReportDocument14 pagesDirectors ReportGaurav JainNo ratings yet

- Infineon Annual Report 2021-153-156Document4 pagesInfineon Annual Report 2021-153-156Ddaeng StudiosNo ratings yet

- Ramco Annual Report 2014Document2 pagesRamco Annual Report 2014nithinNo ratings yet

- Airbus SN Q3-2020Document21 pagesAirbus SN Q3-2020paulouisvergnesNo ratings yet

- Income Statement and Balance Sheet ExerciseDocument2 pagesIncome Statement and Balance Sheet ExerciseMujieh NkengNo ratings yet

- Financial Statements 2015: Airbus Group SEDocument194 pagesFinancial Statements 2015: Airbus Group SEfx_ww2001No ratings yet

- Colgate 2Document11 pagesColgate 2gaurav.jain.25nNo ratings yet

- Sumarised P&LDocument1 pageSumarised P&Lgargrohan989gargNo ratings yet

- Cobalto 1 PDFDocument22 pagesCobalto 1 PDFcristamaarNo ratings yet

- SM 5Document27 pagesSM 5wtfNo ratings yet

- Bangalore To Kolkata Flight Status Today, Flight Time & Tracker - IndiGoDocument1 pageBangalore To Kolkata Flight Status Today, Flight Time & Tracker - IndiGoPragati SarafNo ratings yet

- Eti Base Code EnglishDocument4 pagesEti Base Code EnglishJohn RajeshNo ratings yet

- Blackbody Radiation Spectrum NotesDocument10 pagesBlackbody Radiation Spectrum NotesKarthick JyothieshwarNo ratings yet

- Important Decisions of RTIDocument185 pagesImportant Decisions of RTIkrishnadas100100% (1)

- Fact Analysis WorkshopDocument2 pagesFact Analysis WorkshopKaran VijayanNo ratings yet

- ABELLO vs. CIRDocument4 pagesABELLO vs. CIRFrancise Mae Montilla MordenoNo ratings yet

- Citric Acid SDS11350 PDFDocument7 pagesCitric Acid SDS11350 PDFSyafiq Mohd NohNo ratings yet

- Genitive Case FixaçãoDocument4 pagesGenitive Case Fixaçãoryan 01 da EPCArNo ratings yet

- Affidavit of Romy BuymaxxDocument2 pagesAffidavit of Romy BuymaxxanonNo ratings yet

- Je DV and Medical FinalDocument14 pagesJe DV and Medical FinalAna GoreNo ratings yet

- Case Title: G.R. No. 86693 July 2, 1990Document2 pagesCase Title: G.R. No. 86693 July 2, 1990Arnold Jr AmboangNo ratings yet

- 001 2017 4 BDocument288 pages001 2017 4 BmunyatsungaNo ratings yet

- April SBIDocument5 pagesApril SBIRahul kumarNo ratings yet

- Mcqs SolvedDocument15 pagesMcqs SolvedWaqar Ahmed100% (1)

- 879Document48 pages879B. MerkurNo ratings yet

- Crime in Dar Es SalaamDocument64 pagesCrime in Dar Es SalaamUnited Nations Human Settlements Programme (UN-HABITAT)No ratings yet

- SOP For Handling of Rejected Raw MaterialDocument6 pagesSOP For Handling of Rejected Raw Materialanoushia alviNo ratings yet

- Information For Foreign ApplicantsDocument6 pagesInformation For Foreign ApplicantsMuhannad Al-AfifNo ratings yet

- We The State - Issue 10 Vol 2Document12 pagesWe The State - Issue 10 Vol 2wethestateNo ratings yet

- Aklan Revised IRR To National Building Code (Compatibility Mode)Document80 pagesAklan Revised IRR To National Building Code (Compatibility Mode)Anton_Young_1962No ratings yet

- 10000026681Document20 pages10000026681Chapter 11 DocketsNo ratings yet

- Graft CasesDocument37 pagesGraft CasesTuella RusselNo ratings yet

- WarnickJ - MGMT436 - Strategic Audit Assignment - 8.4 (Draft)Document17 pagesWarnickJ - MGMT436 - Strategic Audit Assignment - 8.4 (Draft)James WarnickNo ratings yet

- Thomas & Margaret (Reilly) Kemp of Ireland and Their Descendants in AmericaDocument8 pagesThomas & Margaret (Reilly) Kemp of Ireland and Their Descendants in AmericaThomas Jay KempNo ratings yet

- Hope, Kempe Ronald-Police Corruption and Police Reforms in Developing Societies-CRC Press (2016)Document270 pagesHope, Kempe Ronald-Police Corruption and Police Reforms in Developing Societies-CRC Press (2016)Darko Zlatkovik100% (1)