Download as pdf or txt

You might also like

- Finessing Fixed DividendsDocument2 pagesFinessing Fixed DividendsVeeken Chaglassian100% (2)

- MATH40082 (Computational Finance) Assignment No. 2: Advanced MethodsDocument6 pagesMATH40082 (Computational Finance) Assignment No. 2: Advanced Methodscracking khalifNo ratings yet

- Basel II CheatsheetDocument8 pagesBasel II CheatsheetBhabaniParidaNo ratings yet

- MBS Modelling 3 DuringDocument22 pagesMBS Modelling 3 DuringddwadawdwadNo ratings yet

- Market Model ITRAXXDocument6 pagesMarket Model ITRAXXLeo D'AddabboNo ratings yet

- Modelling The Price of A Credit Default Swap: Agnieszka ZalewskaDocument29 pagesModelling The Price of A Credit Default Swap: Agnieszka ZalewskaJos MollenNo ratings yet

- Swaps Cms CMTDocument7 pagesSwaps Cms CMTmarketfolly.comNo ratings yet

- Calibration and Data Analysis: in This Lecture. .Document73 pagesCalibration and Data Analysis: in This Lecture. .Zohaib SiddiqueNo ratings yet

- Multi Reference Credit DerivativesDocument7 pagesMulti Reference Credit DerivativesConstantin TheodorNo ratings yet

- Girsanov, Numeraires, and All That PDFDocument9 pagesGirsanov, Numeraires, and All That PDFLe Hoang VanNo ratings yet

- Arbitrage Models of Commodity Prices: Andrea Roncoroni ESSEC Business School, Paris - SingaporeDocument9 pagesArbitrage Models of Commodity Prices: Andrea Roncoroni ESSEC Business School, Paris - Singaporegj409gj548jNo ratings yet

- SSRN Id3029321Document10 pagesSSRN Id3029321Raphaël FromEverNo ratings yet

- CQF June 2021 M6L1 Extra NotesDocument74 pagesCQF June 2021 M6L1 Extra NotesPrathameshSagareNo ratings yet

- Market Models PDFDocument14 pagesMarket Models PDF0612001No ratings yet

- IRModellingLecture Part 02Document94 pagesIRModellingLecture Part 02flatronabcdefgNo ratings yet

- CMS Swaps HaganDocument7 pagesCMS Swaps HagandjfwalkerNo ratings yet

- MFDC 10 DDocument5 pagesMFDC 10 DTu ShirotaNo ratings yet

- 4 - Girsanov, Numeraires, and All ThatDocument43 pages4 - Girsanov, Numeraires, and All Thatdoc_oz3298No ratings yet

- STCDO Model Calibration and Hedge Performance: QMF Sydney - December 13, 2006Document35 pagesSTCDO Model Calibration and Hedge Performance: QMF Sydney - December 13, 2006fviethNo ratings yet

- Credit Risk Modelling ValuationDocument26 pagesCredit Risk Modelling ValuationHana KasemNo ratings yet

- SSRN Id3228827Document10 pagesSSRN Id3228827LUXMI TRADING COMPANYNo ratings yet

- E 2 CreditRiskDocument10 pagesE 2 CreditRiskRuben KempterNo ratings yet

- OVCV Model DescriptionDocument5 pagesOVCV Model DescriptionVinceNo ratings yet

- BscholesDocument14 pagesBscholesAhsan JavedNo ratings yet

- Volatility-Smile Modeling With Density-Mixture Stochastic Differential EquationsDocument39 pagesVolatility-Smile Modeling With Density-Mixture Stochastic Differential EquationsShai Aron RNo ratings yet

- Fixed Income and Credit Risk: Prof. Michael RockingerDocument17 pagesFixed Income and Credit Risk: Prof. Michael RockingerJean BoncruNo ratings yet

- MAFS5030 hw1Document4 pagesMAFS5030 hw1RajNo ratings yet

- Equity Variance Swaps With Dividends OpenGammaDocument13 pagesEquity Variance Swaps With Dividends OpenGammamshchetkNo ratings yet

- Mathematical Modelling and Financial Engineering in The Worlds Stock MarketsDocument7 pagesMathematical Modelling and Financial Engineering in The Worlds Stock MarketsVijay ParmarNo ratings yet

- Yri GH T Cop Yri GH T: Introduction To Interest Rate Products Lecture 3 - Vanilla Derivatives (Part 1)Document15 pagesYri GH T Cop Yri GH T: Introduction To Interest Rate Products Lecture 3 - Vanilla Derivatives (Part 1)Oussama BOUDCHICHINo ratings yet

- SOA Exam MFE Flash CardsDocument21 pagesSOA Exam MFE Flash CardsSong Liu100% (2)

- Lecture 3Document9 pagesLecture 3przemstilNo ratings yet

- Interest Rate SwapDocument13 pagesInterest Rate SwapssriraghavNo ratings yet

- Monte Carlo Option Pricing: Victor Podlozhnyuk Mark HarrisDocument15 pagesMonte Carlo Option Pricing: Victor Podlozhnyuk Mark HarrisVishwa ShanikaNo ratings yet

- Chapter 1: Interest Rates and Related ContractsDocument13 pagesChapter 1: Interest Rates and Related ContractsMirelia Kathlin Loayza TapiaNo ratings yet

- Chapter 1: Interest Rates and Related ContractsDocument13 pagesChapter 1: Interest Rates and Related ContractsMirelia Kathlin Loayza TapiaNo ratings yet

- Portfolio Management and Financial Analysis: Chapter 16 - Managing Bond Portfolios 1Document46 pagesPortfolio Management and Financial Analysis: Chapter 16 - Managing Bond Portfolios 1Moen 693No ratings yet

- Teaching Note 97-08: Pricing and Valuation of Commodity SwapsDocument13 pagesTeaching Note 97-08: Pricing and Valuation of Commodity SwapsVeeken ChaglassianNo ratings yet

- Mod 4 Exam Jan 16Document2 pagesMod 4 Exam Jan 16pallab2110No ratings yet

- Chapter 4: Interest Rate Derivatives: 4.3 SwaptionsDocument12 pagesChapter 4: Interest Rate Derivatives: 4.3 Swaptionsz_k_j_vNo ratings yet

- Modern Approaches To Stochastic Volatility CalibrationDocument43 pagesModern Approaches To Stochastic Volatility Calibrationhsch345No ratings yet

- MIT15 450F10 Assn04Document3 pagesMIT15 450F10 Assn04Logon ChristNo ratings yet

- An Introduction To Pricing Methods For Credit Derivatives: José Figueroa-LópezDocument10 pagesAn Introduction To Pricing Methods For Credit Derivatives: José Figueroa-Lópezsam4reportNo ratings yet

- DB Quiz-2007Document4 pagesDB Quiz-2007harlequin007No ratings yet

- Martin Forde - The Real P&LDocument13 pagesMartin Forde - The Real P&LfrancescomaterdonaNo ratings yet

- Swaptions: European Swap OptionsDocument4 pagesSwaptions: European Swap Optionsmiku hrshNo ratings yet

- Topics in Continuous-Time Finance, Spring 2003Document2 pagesTopics in Continuous-Time Finance, Spring 2003seanwu95No ratings yet

- Hull Chapter 26 - Interest Rate DerivativesDocument37 pagesHull Chapter 26 - Interest Rate DerivativesAbhayNo ratings yet

- Studia Univ. "Babes - BOLYAI", MATHEMATICA, Volume, Number 3, September 2003Document10 pagesStudia Univ. "Babes - BOLYAI", MATHEMATICA, Volume, Number 3, September 2003FernandoFierroGonzalezNo ratings yet

- 1 The Black-Scholes ModelDocument12 pages1 The Black-Scholes ModeloptisearchNo ratings yet

- D 1 LMM DefinitionsDocument10 pagesD 1 LMM DefinitionsJean BoncruNo ratings yet

- Two Collars and A Free LunchDocument9 pagesTwo Collars and A Free LunchLiu YanNo ratings yet

- BNP Paribas Dupire Arbitrage Pricing With Stochastic VolatilityDocument18 pagesBNP Paribas Dupire Arbitrage Pricing With Stochastic Volatilityvictormatos90949No ratings yet

- Review: Arbitrage-Free Pricing and Stochastic Calculus: Leonid KoganDocument16 pagesReview: Arbitrage-Free Pricing and Stochastic Calculus: Leonid Koganseanwu95No ratings yet

- Methods For Constructing A Yield Curve: January 2008Document19 pagesMethods For Constructing A Yield Curve: January 2008simonNo ratings yet

- Ch-19 Credit RiskDocument8 pagesCh-19 Credit RiskIsha TachhekarNo ratings yet

- Transaction Costs and Non-Markovian Delta HedgingDocument14 pagesTransaction Costs and Non-Markovian Delta HedgingpostscriptNo ratings yet

- Equilibrium in A Pure Exchange EconomyDocument3 pagesEquilibrium in A Pure Exchange EconomyclosyuraisNo ratings yet

- 2 Continuous Cash Flows PDFDocument12 pages2 Continuous Cash Flows PDFSSNo ratings yet

- Mathematical Formulas for Economics and Business: A Simple IntroductionFrom EverandMathematical Formulas for Economics and Business: A Simple IntroductionRating: 4 out of 5 stars4/5 (4)

- The Spectral Theory of Toeplitz Operators. (AM-99), Volume 99From EverandThe Spectral Theory of Toeplitz Operators. (AM-99), Volume 99No ratings yet

- 12 - Backward Induction & Monte Carlo SimulationsDocument47 pages12 - Backward Induction & Monte Carlo Simulationsdoc_oz3298No ratings yet

- 15 - Counterparty Credit RiskDocument87 pages15 - Counterparty Credit Riskdoc_oz3298No ratings yet

- The Cheyette Model ClassDocument13 pagesThe Cheyette Model Classdoc_oz3298No ratings yet

- Hull White CalibrationDocument4 pagesHull White Calibrationdoc_oz3298No ratings yet

- Heath-Jarrow-Morton Model - What Is It, Formula, AssumptionsDocument10 pagesHeath-Jarrow-Morton Model - What Is It, Formula, Assumptionsdoc_oz3298No ratings yet

- Interest Rate ModelsDocument188 pagesInterest Rate Modelsdoc_oz3298No ratings yet

- 4 - Pricing - Which Interest Rate Model For Which Product - Quantitative Finance Stack ExchangeDocument3 pages4 - Pricing - Which Interest Rate Model For Which Product - Quantitative Finance Stack Exchangedoc_oz3298No ratings yet

- A Review of The Generalized Black-Scholes Formula - & It's Application To Different Underlying AssetsDocument12 pagesA Review of The Generalized Black-Scholes Formula - & It's Application To Different Underlying Assetsdoc_oz3298No ratings yet

- Pypy: A Fast and Compliant Python Implementation An IntroductionDocument32 pagesPypy: A Fast and Compliant Python Implementation An Introductiondoc_oz3298No ratings yet

- Entropy PDFDocument9 pagesEntropy PDFdoc_oz3298No ratings yet

- Quantitative Styles & MultiSector BondsDocument18 pagesQuantitative Styles & MultiSector Bondsdoc_oz3298No ratings yet

- Bushido, The Soul of Japan: Inazo NitobéDocument68 pagesBushido, The Soul of Japan: Inazo Nitobédoc_oz3298No ratings yet

- Algorithm Trading Using Q-Learning and Recurrent Reinforcement Learning PDFDocument7 pagesAlgorithm Trading Using Q-Learning and Recurrent Reinforcement Learning PDFdoc_oz3298No ratings yet

- Global Technology Fund A Acc: Janus HendersonDocument2 pagesGlobal Technology Fund A Acc: Janus Hendersondoc_oz3298No ratings yet

- Equities: J.P. Morgan MarketsDocument2 pagesEquities: J.P. Morgan Marketsdoc_oz3298No ratings yet

- Building Resistance To Stress and AgingDocument378 pagesBuilding Resistance To Stress and Agingdoc_oz3298No ratings yet

- Raspberry Pi QuickstartDocument9 pagesRaspberry Pi Quickstartdoc_oz3298No ratings yet

- Volatility Lecture PDFDocument235 pagesVolatility Lecture PDFdoc_oz3298No ratings yet

- Exercises in Advanced Risk and Portfolio Management PDFDocument281 pagesExercises in Advanced Risk and Portfolio Management PDFdoc_oz3298No ratings yet

- Abc-Consolidation With Intercompany TransactionsDocument3 pagesAbc-Consolidation With Intercompany TransactionsLeonardo MercaderNo ratings yet

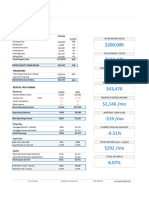

- Alexandria Public Schools Tax LevyDocument74 pagesAlexandria Public Schools Tax LevyinforumdocsNo ratings yet

- Republic of The Philippines vs. Sunlife Assurance: GR NO. 158085 OCTOBER 14, 2005Document9 pagesRepublic of The Philippines vs. Sunlife Assurance: GR NO. 158085 OCTOBER 14, 2005dingNo ratings yet

- UPSE Securities Limited v. NSE - CCI OrderDocument5 pagesUPSE Securities Limited v. NSE - CCI OrderBar & BenchNo ratings yet

- IFRS 9 Financial InstrumentsDocument38 pagesIFRS 9 Financial InstrumentsKiri chrisNo ratings yet

- Trad Ic Mock Exam Answer KeyDocument15 pagesTrad Ic Mock Exam Answer KeyGener ApolinarioNo ratings yet

- Mitul - 151479254Document3 pagesMitul - 151479254asdasdNo ratings yet

- Chapter 3: The Electronic Wallet 3.1. Introduction To E-WalletDocument7 pagesChapter 3: The Electronic Wallet 3.1. Introduction To E-WalletHoàng MiiNo ratings yet

- Impact of Elections On Indian Stock Market - Wrigh - 231125 - 225935Document10 pagesImpact of Elections On Indian Stock Market - Wrigh - 231125 - 225935test.heaventreeNo ratings yet

- Basic Accounting PrinciplesDocument5 pagesBasic Accounting PrinciplesGracie BulaquinaNo ratings yet

- Chapter 9Document30 pagesChapter 9Ita Devi SagitaNo ratings yet

- Report of Investigation: Burns Philp and Co LTDDocument41 pagesReport of Investigation: Burns Philp and Co LTDa_bleem_userNo ratings yet

- Trial Essay Questions V3 DoneDocument5 pagesTrial Essay Questions V3 DoneNguyễn Huỳnh ĐứcNo ratings yet

- NRO Vs NREDocument3 pagesNRO Vs NREsushantNo ratings yet

- Rental Investment ReportDocument5 pagesRental Investment ReportTuba TunaNo ratings yet

- 2015 Saln Form Calvert Miguel - NewDocument2 pages2015 Saln Form Calvert Miguel - NewGina Portuguese GawonNo ratings yet

- HDFC Mutual FundsDocument68 pagesHDFC Mutual FundsMohammed Dasthagir MNo ratings yet

- Why Worlds Largest AMCs Not Present in India - August 2023Document12 pagesWhy Worlds Largest AMCs Not Present in India - August 2023manindrag00No ratings yet

- Sample Paperpre Board II Acct 2324-2Document10 pagesSample Paperpre Board II Acct 2324-2kanakchauhan206No ratings yet

- 23si0055 - Ace WaterDocument1 page23si0055 - Ace WaterDeshan SingNo ratings yet

- Somali Sports Fashion Centre: S S F CDocument10 pagesSomali Sports Fashion Centre: S S F CAnonymous U5JZ8NOquNo ratings yet

- Sarbanes-Oxley Act, Internal Control, and Management AccountingDocument2 pagesSarbanes-Oxley Act, Internal Control, and Management Accountingalexandro_novora6396No ratings yet

- Netowrth CertificateDocument3 pagesNetowrth CertificateSai Charan GvNo ratings yet

- EBRSDocument20 pagesEBRSRaju BothraNo ratings yet

- Semana 10 Ingles NI EXAMENDocument31 pagesSemana 10 Ingles NI EXAMENSOLANO VIDAL RIJKAARD MAINNo ratings yet

- The Little Kingdom The Little Kingdom The Little KingdomDocument1 pageThe Little Kingdom The Little Kingdom The Little KingdomSundar VikramNo ratings yet

- Brief History of The ASEAN (1967 Present)Document6 pagesBrief History of The ASEAN (1967 Present)Redmond YuNo ratings yet

- Multiple Choice Questions 1 The Random Walk Theory Suggests ADocument2 pagesMultiple Choice Questions 1 The Random Walk Theory Suggests Atrilocksp SinghNo ratings yet

- COO EVP SVP Operations in Irvine California Resume Mark UlmerDocument3 pagesCOO EVP SVP Operations in Irvine California Resume Mark UlmerMark UlmerNo ratings yet