Download as pdf or txt

You might also like

- Income Taxation CHAPTER 5-NOTESDocument9 pagesIncome Taxation CHAPTER 5-NOTESMark100% (5)

- Taxation 1 NotesDocument15 pagesTaxation 1 NotesTricia SandovalNo ratings yet

- Benefits of Wage Earner, Taxable and Non-Taxable BenefitsDocument33 pagesBenefits of Wage Earner, Taxable and Non-Taxable BenefitsCassandra Dianne Ferolino MacadoNo ratings yet

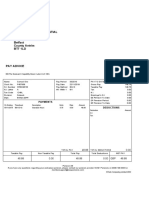

- Payslip Balp407938201933002 PDFDocument1 pagePayslip Balp407938201933002 PDFnik omek100% (1)

- Tax ReviewerDocument10 pagesTax Revieweraira nialaNo ratings yet

- Final Tax PDFDocument50 pagesFinal Tax PDFMicol Villaflor Ü100% (1)

- Principles of Taxation Law - (Week 6)Document56 pagesPrinciples of Taxation Law - (Week 6)ishikakeswani4No ratings yet

- Chpater 5 - Final Income TaxationDocument31 pagesChpater 5 - Final Income TaxationKeziah YpilNo ratings yet

- Week 6 Course Material For Income TaxationDocument8 pagesWeek 6 Course Material For Income Taxationjayannehipolito20No ratings yet

- TaxInd P1Document25 pagesTaxInd P1Rael RaelNo ratings yet

- Chapter 5 Final Income TaxationDocument26 pagesChapter 5 Final Income TaxationJason MablesNo ratings yet

- Module 06 Taxation of Corporations Regular Corp.Document6 pagesModule 06 Taxation of Corporations Regular Corp.Zoren LegaspiNo ratings yet

- 3 0-IndividualsDocument39 pages3 0-IndividualsgenadriellNo ratings yet

- Chapter 5Document22 pagesChapter 5crackheads philippinesNo ratings yet

- ItaxDocument10 pagesItaxdinglasan.dymphnaNo ratings yet

- UAE Corporate Tax On Your Finger TipsDocument48 pagesUAE Corporate Tax On Your Finger Tipsmffaani107No ratings yet

- Income Tax Prelims.Document13 pagesIncome Tax Prelims.Amber Lavarias BernabeNo ratings yet

- Final Withholding Taxes and Withholdiing of Business Taxes On Government Income Payments (Part Iii)Document109 pagesFinal Withholding Taxes and Withholdiing of Business Taxes On Government Income Payments (Part Iii)Bien Bowie A. CortezNo ratings yet

- Angel Funds FAQsDocument8 pagesAngel Funds FAQsJagdish RajanNo ratings yet

- Chapter 5 Final Income TaxDocument51 pagesChapter 5 Final Income Taxdeleonrzlyn20No ratings yet

- Income Taxation of Individuals: Citizens: Resident Non-Residents CitizensDocument4 pagesIncome Taxation of Individuals: Citizens: Resident Non-Residents CitizensJul A.No ratings yet

- Income Taxation of Individuals: Citizens: Resident Non-Residents CitizensDocument2 pagesIncome Taxation of Individuals: Citizens: Resident Non-Residents CitizenshellomynameisNo ratings yet

- Domestic AIF v. IFSC AIFDocument3 pagesDomestic AIF v. IFSC AIFblack venomNo ratings yet

- 06 Overview of Income Taxation and Income Tax For IndividualsDocument7 pages06 Overview of Income Taxation and Income Tax For IndividualsRonn Robby RosalesNo ratings yet

- Introduction To Income TaxationDocument10 pagesIntroduction To Income TaxationKatrina MaglaquiNo ratings yet

- REITDocument12 pagesREITRanjay 3GNo ratings yet

- Income TaxationDocument14 pagesIncome TaxationAlexa Daphne M. EquisabalNo ratings yet

- Denna Id No. 20201290 Tax TableDocument10 pagesDenna Id No. 20201290 Tax TableZEBULUN DOCALLASNo ratings yet

- Fera and Fema: Submitted To: Prof. Anant AmdekarDocument40 pagesFera and Fema: Submitted To: Prof. Anant AmdekarhasbicNo ratings yet

- An Overview of Fdi Regulations 1639647827Document73 pagesAn Overview of Fdi Regulations 1639647827ishaankc1510No ratings yet

- UP 2008 Taxation Law (Taxation 1)Document63 pagesUP 2008 Taxation Law (Taxation 1)Gol LumNo ratings yet

- Income Tax - Resident AlienDocument17 pagesIncome Tax - Resident AlienStela PantaleonNo ratings yet

- Individual Taxpayers (Passive Income and Dealings With Properties)Document51 pagesIndividual Taxpayers (Passive Income and Dealings With Properties)ipbsalanguitNo ratings yet

- Taxation ReviewerDocument6 pagesTaxation ReviewerNinaSharaBermudezReyesNo ratings yet

- Module 09 - Inclusions in Gross IncomeDocument15 pagesModule 09 - Inclusions in Gross IncomeRoligen Rose PachicoyNo ratings yet

- WHT & DtaDocument26 pagesWHT & Dtafaz watiNo ratings yet

- Income Taxation TableDocument11 pagesIncome Taxation TableRomela Eleria GasesNo ratings yet

- Assignment No. 4Document7 pagesAssignment No. 4HannahPauleneDimaanoNo ratings yet

- Tax Treatment of Income Sources Sources of Income Subject To Tax Within The Philippines Without The PhilippinesDocument15 pagesTax Treatment of Income Sources Sources of Income Subject To Tax Within The Philippines Without The PhilippinesGiee De GuzmanNo ratings yet

- Concept of Passive IncomeDocument46 pagesConcept of Passive IncomeChristine Joy Bantay100% (1)

- Final Income Taxation Flashcards - QuizletDocument5 pagesFinal Income Taxation Flashcards - QuizletcykablyatNo ratings yet

- Income From Other SourcesDocument11 pagesIncome From Other SourcesAfnanNo ratings yet

- Sources of IncomeDocument1 pageSources of IncomeGian Carlo RamonesNo ratings yet

- Final Income TaxationDocument8 pagesFinal Income TaxationJade Ivy GarciaNo ratings yet

- CT-FAQ-Update-June 2023-2023-06-04-120300Document10 pagesCT-FAQ-Update-June 2023-2023-06-04-120300marketingNo ratings yet

- SEC. 23. General Principles of Income Taxation in The Philippines. - Except WhenDocument11 pagesSEC. 23. General Principles of Income Taxation in The Philippines. - Except WhenMiguel BerguNo ratings yet

- Income Tax On Resident Foreign CorporationDocument6 pagesIncome Tax On Resident Foreign CorporationElaiNo ratings yet

- Sec Memo No. 2, s2012 - Guidelines On Securities Deposit of Branch Offices of Foreign CorporationsDocument7 pagesSec Memo No. 2, s2012 - Guidelines On Securities Deposit of Branch Offices of Foreign CorporationsfroilanrocasNo ratings yet

- ch-11 Taxation of NRIsDocument25 pagesch-11 Taxation of NRIsdean.socNo ratings yet

- Final TDS and Tax ExemptionsDocument4 pagesFinal TDS and Tax Exemptionsdpak bhusalNo ratings yet

- Income TaxationDocument31 pagesIncome TaxationJuanVictorNo ratings yet

- Tax On Individuals Part 2Document10 pagesTax On Individuals Part 2Tet AleraNo ratings yet

- Reviewer in Taxation LawDocument20 pagesReviewer in Taxation LawDred OpleNo ratings yet

- II. INCOME TAXATION (RA 8242 Tax Reform Act of 1997) A. IndividualsDocument7 pagesII. INCOME TAXATION (RA 8242 Tax Reform Act of 1997) A. IndividualsRina TravelsNo ratings yet

- TAX L002 Individual TaxationDocument18 pagesTAX L002 Individual TaxationYuri CaguioaNo ratings yet

- Section 195 TDS On Non-Resident PaymentsDocument1 pageSection 195 TDS On Non-Resident Paymentskumarsanjeev079No ratings yet

- Mamalateo Income and Withholding Taxes 2011Document95 pagesMamalateo Income and Withholding Taxes 2011CHow GatchallanNo ratings yet

- Fisher v. Trinidad (43 Phil 973) : Stock: Income TaxationDocument48 pagesFisher v. Trinidad (43 Phil 973) : Stock: Income TaxationCassey Koi Farm0% (1)

- Income Taxation Lesson 3Document6 pagesIncome Taxation Lesson 3DYLANNo ratings yet

- Module TX005 Final Income TaxationDocument5 pagesModule TX005 Final Income TaxationErwin TorresNo ratings yet

- US Taxation of International Startups and Inbound Individuals: For Founders and Executives, Updated for 2023 rulesFrom EverandUS Taxation of International Startups and Inbound Individuals: For Founders and Executives, Updated for 2023 rulesNo ratings yet

- CRDB BANK VacanciesDocument5 pagesCRDB BANK VacanciesInnocent escoNo ratings yet

- Custom Management Part 1 - 112740Document31 pagesCustom Management Part 1 - 112740Innocent escoNo ratings yet

- Questions On Professional Ethics Set 2Document4 pagesQuestions On Professional Ethics Set 2Innocent escoNo ratings yet

- Learning CurveDocument13 pagesLearning CurveInnocent escoNo ratings yet

- Decision Making Solving - Review QuestionsDocument4 pagesDecision Making Solving - Review QuestionsInnocent escoNo ratings yet

- IAS 1 FInancial Reporting - HandoutDocument19 pagesIAS 1 FInancial Reporting - HandoutInnocent escoNo ratings yet

- Forex Market NotesDocument9 pagesForex Market NotesInnocent escoNo ratings yet

- Decision Making Under Certain EnvironmentDocument3 pagesDecision Making Under Certain EnvironmentInnocent escoNo ratings yet

- Determinants of Economic Growth in Sub SDocument7 pagesDeterminants of Economic Growth in Sub SInnocent escoNo ratings yet

- Activity - ABCDocument1 pageActivity - ABCInnocent escoNo ratings yet

- 15.target CostingDocument9 pages15.target CostingInnocent escoNo ratings yet

- Determinants of Foreign Exchange Risks in Commercial Banks A Case of Selected Banks in IringaDocument7 pagesDeterminants of Foreign Exchange Risks in Commercial Banks A Case of Selected Banks in IringaInnocent escoNo ratings yet

- Launching A Successful E-Business ProjectDocument27 pagesLaunching A Successful E-Business ProjectInnocent escoNo ratings yet

- MAGAYU Final DraftDocument29 pagesMAGAYU Final DraftInnocent escoNo ratings yet

- Document PDFDocument2 pagesDocument PDFsherrimcateeNo ratings yet

- Income Tax Act 1947Document1,138 pagesIncome Tax Act 1947ashish poddarNo ratings yet

- File - DOS Contract With Robertson 2022Document7 pagesFile - DOS Contract With Robertson 2022Dan LehrNo ratings yet

- National Pay Scale 1973Document6 pagesNational Pay Scale 1973maomaodotthreeNo ratings yet

- Labor Cost AkinDocument18 pagesLabor Cost AkinMark Laurence SanchezNo ratings yet

- Standard vs. Itemized Deduction 2021Document2 pagesStandard vs. Itemized Deduction 2021Finn KevinNo ratings yet

- Lic Jeevan Saral Plan 165 ChartDocument3 pagesLic Jeevan Saral Plan 165 Chartkhushbu patelNo ratings yet

- DT Chart BookDocument62 pagesDT Chart BookShagun Chandrakar100% (1)

- Taxation - Singapore (TX - SGP) : Applied SkillsDocument19 pagesTaxation - Singapore (TX - SGP) : Applied SkillsLee WendyNo ratings yet

- Plaridel Security v. CIRDocument2 pagesPlaridel Security v. CIRAila AmpNo ratings yet

- E-26, Asad Street # 1, Mohallah Firdous Park, Ghazi Road, Lahore, Cantonement. Sadaat Naseem KhanDocument3 pagesE-26, Asad Street # 1, Mohallah Firdous Park, Ghazi Road, Lahore, Cantonement. Sadaat Naseem KhanZeeshanNo ratings yet

- NCC AssignmentDocument4 pagesNCC Assignmentmanishv70276No ratings yet

- Income From Salaries: (Sections 15 To 17)Document15 pagesIncome From Salaries: (Sections 15 To 17)Aliakbar SayaniNo ratings yet

- 3M 1Document1 page3M 1Rajiv VermaNo ratings yet

- ACE Bangladesh Payroll Handbook 2021Document32 pagesACE Bangladesh Payroll Handbook 2021Shuvo YeasinNo ratings yet

- This Study Resource WasDocument2 pagesThis Study Resource WasMay RamosNo ratings yet

- Novartis NPS Employee Awareness Presentation PDFDocument33 pagesNovartis NPS Employee Awareness Presentation PDFMohan CNo ratings yet

- Chapter 9 - RIT - Inclusions in Gross IncomeDocument3 pagesChapter 9 - RIT - Inclusions in Gross Incomeclaritaquijano526No ratings yet

- Illustrations ch02Document3 pagesIllustrations ch02FantayNo ratings yet

- Income Tax - ElaineDocument11 pagesIncome Tax - ElaineSamsung AccountNo ratings yet

- Dear ,: ( (Company - Currentdate) )Document5 pagesDear ,: ( (Company - Currentdate) )Abhishek RawatNo ratings yet

- Direct Tax AssignmentDocument16 pagesDirect Tax AssignmentPranjul SahuNo ratings yet

- Wages and SalariesDocument2 pagesWages and SalariesArchana RajuNo ratings yet

- Gorilla Accounting Limited Company Guide4.compressed - PDFDocument22 pagesGorilla Accounting Limited Company Guide4.compressed - PDFnivotaNo ratings yet

- Ts Schemes of Wikipedia in English MediumDocument27 pagesTs Schemes of Wikipedia in English MediumSan JayNo ratings yet

- Chapter 3Document55 pagesChapter 3Ahmed hassanNo ratings yet

- Higher Education Loans Board: Tvet-Loan/Bursary Application Form - First Time ApplicantDocument7 pagesHigher Education Loans Board: Tvet-Loan/Bursary Application Form - First Time ApplicantEdwardNo ratings yet

- Human Resource Management of StarbucksDocument6 pagesHuman Resource Management of Starbucksjemily magtanongNo ratings yet